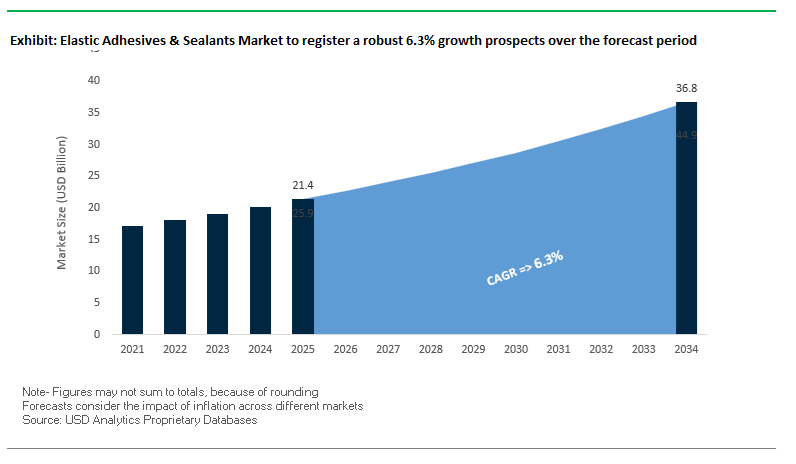

The Global Elastic Adhesives and Sealants Market is projected to grow from $25.9 billion in 2025 to $44.9 billion by 2034, at a CAGR of 6.3%. Elastic adhesives and sealants have moved from ancillary sealants to strategic engineering materials because they simultaneously enable lightweight multi-material designs, manage heat in high-energy assemblies, and satisfy tightening environmental and fire-safety requirements. Demand is anchored in three commercial drivers: OEM mandates to replace mechanical fasteners in cell-to-body (CTB) and cell-to-pack battery architectures to cut mass and assembly complexity; the need for thermally conductive yet electrically isolating interface materials inside high-density EV packs; and construction-sector adoption of solvent-free, low-VOC chemistries for façade, glazing and movement joints. Leading manufacturers position thermally conductive adhesives, silane-modified polymers (SMP) and engineered polyurethanes as the accepted solution set for these combined requirements.

The structural shift is visible in substitution patterns and measurable performance outcomes. PU and SMP systems are displacing spot welding and rivets in automotive battery and multi-material body assemblies because they deliver predictable elasticity, adhesion across dissimilar substrates and improved crash energy distribution while enabling simpler, lower-mass designs; manufacturers report thermally conductive adhesive families spanning ~0.8–3 W/m·K depending on formulation, and UL94-V0 rated material stacks are commercially available for pack insulation and gasketing. Waterborne acrylic and neutral-curing silicone sealants dominate high-movement building joints to meet low-VOC targets without sacrificing durability across −40 °C to +90 °C service windows. These material choices translate directly to business outcomes: reduced part count and machining/fastener cost, lower pack/system mass, improved battery thermal management (supporting stated manufacturer gains in heat-transfer efficiency), longer joint uptime under cyclic loads, and fewer warranty events tied to adhesive/cohesive failures.

Over the forecast period, manufacturers and OEMs will concentrate sourcing on validated, UL/ISO/SAE-aligned chemistries and on scale-proven formulations (thermally conductive adhesives, flame-retardant elastomers, SMPs and pressure-sensitive tapes) that ease automation in high-volume EV and façade assembly lines while meeting VOC and fire-safety compliance

Key Industry Insights

- Thermal Management: Advanced polyurethane and SMP adhesives enhance heat dissipation by 15%+ in EV battery modules, improving performance and safety.

- Green Building Adoption: Modern construction projects specify low-VOC, solvent-free sealants, driving market transition toward SMP and aqueous acrylic chemistries.

- Automotive Shift: Elastic structural adhesives strong growth in demand for CTB and mixed-material bonding applications.

- Fire Safety Focus: FR-grade elastic PSA tapes are gaining traction in EV and electronics, meeting UL 94 V-0 standards for insulation and flame resistance.

- Durability in Extremes: New PU and SMP sealants sustain elastic modulus stability between −40°C and +90°C, ensuring consistent joint performance in extreme climates.

The elastic adhesives and sealants industry is entering a transformative decade, driven by the dual imperatives of electrification and sustainability. Manufacturers are prioritizing eco-friendly chemistries, bio-based formulations, and isocyanate-free SMP systems to align with global environmental regulations while enhancing mechanical performance. Key developments between February 2025 and September 2025 reveal strong momentum toward localized production, green materials, and advanced bonding technologies across construction, transportation, and packaging sectors.

In September 2025, Sonoco Products Company committed $30 million to expand adhesive and sealant production, bolstering supply resilience for industrial assembly and flexible packaging customers. The same month, H.B. Fuller highlighted the expanding role of its butyl and elastic tapes in infrastructure and vehicle sealing, emphasizing their moisture resistance and long-term flexibility. In August 2025, a leading global manufacturer (e.g., Sika or Dow) launched a room-temperature-curing elastic adhesive series for EV battery bonding, offering faster assembly cycles and superior crash energy management — a key advancement for electric mobility.

Strategic acquisitions continued shaping the industry landscape. In July 2025, a major diversified materials company acquired a European manufacturer of acrylic PSA tapes, strengthening its foothold in electronics and medical device assembly adhesives. Meanwhile, H.B. Fuller’s June 2025 sustainability report demonstrated tangible progress toward bio-based and low-carbon hot melt production, showcasing innovation aligned with global circular economy targets.

In May 2025, Mapei SpA opened a new sealant production facility in Southeast Asia, expanding capacity for hybrid PU and MS-polymer adhesives catering to fast-growing infrastructure markets. 3M’s April 2025 innovation in VHB™ Tape technology introduced a new elastic acrylic core, enhancing bonding strength to low surface energy (LSE) substrates like plastics and composites. In March 2025, Bostik (Arkema Group) released a new 100% isocyanate-free SMP sealant line, fully REACH-compliant for safer use in building applications. Finally, Sika AG’s February 2025 product launch unveiled solvent-free silicone and MS-polymer facade sealants, delivering enhanced UV and climate resistance for modern architectural glazing.

The architectural shift toward energy-efficient and flexible facade systems is transforming demand for high-movement, weatherproof elastic sealants capable of maintaining adhesion and structural integrity under wide temperature and load variations. Traditional ±25% movement capacity sealants are being replaced by next-generation silicone and hybrid polymer systems rated up to ±50%, a performance leap essential for large-format curtain wall, glass, and metal panel systems.

According to EN 15651-1 and ASTM C920 standards, ultra-low-modulus silicone elastomeric sealants surpass legacy “25 LM” classifications. Leading manufacturers have introduced neutral-cure silicone sealants that not only achieve the ±50% movement threshold but also provide enhanced UV resistance, low shrinkage, and long-term color stability. These properties are crucial for façade joints exposed to seismic and thermal cycling, particularly in climates with extreme temperature fluctuations.

Independent case studies have validated the superior performance of elastic façade sealants in long-term weathering simulations. In one study, high-performance silicone sealants maintained structural cohesion after thousands of stress cycles, outperforming mechanical joints prone to fatigue and failure. With modern façade systems increasingly relying on invisible bonding rather than mechanical fixings, high-movement capability and durable elasticity have become defining metrics for product specification in global architecture.

The electrification of mobility has triggered a new wave of R&D in thermally conductive yet flexible adhesives, essential for EV battery assemblies that must manage both mechanical vibration and intense heat dissipation. Advanced two-component silicone and polyurethane adhesives are engineered to deliver thermal conductivity up to 1.5 W/m·K, while maintaining elongation at break between 20–25%, a vital balance for absorbing expansion stresses within battery cells during charge and discharge cycles.

In next-generation Cell-to-Pack (CTP) and Cell-to-Chassis (CTC) battery systems, elastic adhesives serve dual functions: heat transfer and structural reinforcement. The ability to retain adhesion from −60°C to 200°C ensures stability under extreme operational environments. In parallel, room temperature vulcanizing (RTV) silicones—which achieve over 2 MPa adhesion strength within minutes via infrared (IR) or laser curing—are streamlining automated production in battery assembly plants.

As global EV output scales rapidly, these flexible, thermally conductive adhesives are redefining battery design safety, efficiency, and recyclability. They not only secure cells and modules but also replace traditional gaskets and mechanical fixtures, contributing to overall weight reduction and improved power-to-mass ratios. The positions elastic adhesives at the core of thermal interface management and lightweight e-mobility engineering.

The global construction industry’s transition toward sustainable building materials has propelled Mass Timber Construction (MTC) into a high-growth category, creating immense potential for elastic adhesives and sealants tailored to wooden substrates. Products like Cross-Laminated Timber (CLT) and Glued-Laminated Timber (Glulam) exhibit strong environmental performance but also unique hygroscopic behavior—expanding and contracting with changes in moisture content.

Academic and field research report that timber moisture levels can vary between 12–14% (fabrication) and 20–30% during construction exposure, imposing dynamic stress on joints and connectors. These shifts necessitate moisture-tolerant, permanently elastic adhesives to prevent cracking, delamination, and moisture ingress in façade and envelope joints.

High-performance polyurethane and silane-modified polymer sealants are gaining traction for the reason—they allow joint widths of up to 35 mm, resist swelling under wet conditions, and retain high tensile strength even under cyclic deformation. As the number of mid-rise and high-rise timber structures rises in markets like North America, Japan, and Europe, manufacturers offering long-life elastic timber adhesives are positioned to dominate the fast-emerging segment of sustainable construction materials.

The intersection of electronics miniaturization and flexible materials science has opened vast opportunities for ultra-elastic conductive adhesives (ECAs) that enable next-generation Flexible Hybrid Electronics (FHE)—combining sensors, circuits, and communication systems within soft, bendable substrates. The future of wearable medical devices, foldable displays, and soft robotics depends on adhesive systems that can maintain both electrical conductivity and mechanical resilience under continuous deformation.

Recent advancements in polyurethane/polymer composite ECAs have demonstrated resistivity as low as 3.8×10⁻⁵ Ω·cm, while maintaining conductivity even after 1,000 bending and twisting cycles. The performance is critical for biocompatible, skin-contact electronics and wearable health patches that experience constant mechanical stress.

Industry consortia such as NextFlex (U.S.) are investing heavily in R&D for flexible hybrid manufacturing ecosystems, targeting adhesive materials that combine low-temperature curing, high elongation, and durable conductivity. The integration of silver nanoparticle or carbon-based conductive fillers within elastic matrices further enhances electrical continuity in stretchable circuits. The paves the way for ultra-stretchable ECAs designed for smart clothing, health monitoring sensors, and soft robotics.

Elastic Adhesives & Sealants Market Share Insights, 2025-2034

The building and construction sector represents nearly half of the global elastic adhesives and sealants market, underscoring its status as the most dominant and influential end-use industry. These materials are integral to modern construction due to their ability to absorb structural movement, seal expansion joints, and provide long-term weatherproofing across commercial, residential, and infrastructure projects. They are indispensable in structural glazing, curtain wall bonding, waterproofing membranes, façade assembly, and flooring systems, where mechanical flexibility and chemical durability are essential. The global emphasis on energy-efficient and sustainable construction practices—such as airtight building envelopes and green-certified projects—has further accelerated demand for high-performance, low-VOC, and isocyanate-free elastic sealants. Moreover, the rapid expansion of urban infrastructure and smart city projects in Asia-Pacific and the Middle East continues to boost market penetration, while North America and Europe witness stable consumption through large-scale renovation and retrofitting initiatives. This segment’s growth trajectory is closely tied to global megatrends such as urbanization, environmental sustainability, and modular construction, ensuring that construction remains the cornerstone of the elastic adhesives and sealants industry through 2034.

The automotive and transportation industry is the second-largest end-use segment, driven by the adoption of elastic adhesives and sealants for structural bonding, seam sealing, and noise, vibration, and harshness (NVH) damping applications. These products play a pivotal role in enabling lightweight vehicle designs, replacing mechanical fasteners to reduce overall weight and improve fuel efficiency while maintaining safety and structural integrity. Elastic formulations such as MS polymers, silicones, and polyurethane-based sealants are used for direct glazing, bonding composite body panels, and sealing seams exposed to vibration and thermal expansion. In electric vehicles (EVs), elastic adhesives are gaining strategic importance in battery pack assembly, cell encapsulation, and thermal management systems, where vibration control and environmental sealing are vital for longevity and safety. The transportation sector’s shift toward electrification, modular design, and improved passenger comfort continues to push demand for high-durability, low-emission formulations that can bond dissimilar materials (metal, glass, composites, and plastics) effectively. This evolving use case spectrum makes the automotive segment one of the fastest-growing contributors to the global elastic adhesives and sealants market.

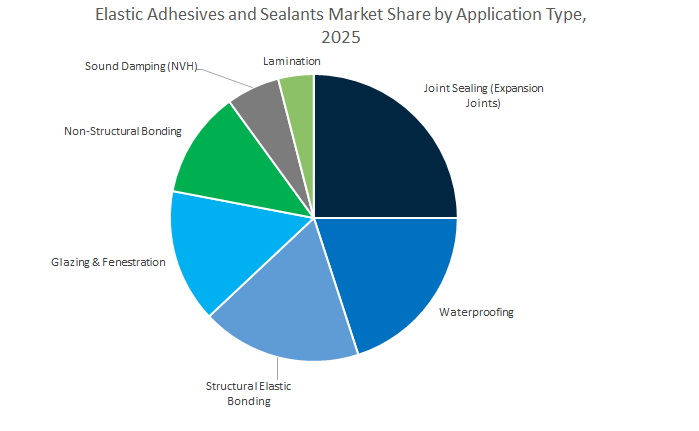

Joint sealing and waterproofing account for nearly half of the global elastic adhesives and sealants industry, reflecting their indispensable roles in both structural integrity and environmental protection. Joint sealing, representing about 25.7% of the market, is vital in buildings, bridges, and pavements to accommodate movement caused by temperature changes, load shifts, and seismic activity. Waterproofing applications, holding approximately 20.4%, are equally critical for below-grade structures, roofing, wet rooms, and façade systems, where long-term resistance to moisture ingress determines the lifespan of buildings. Elastic sealants—especially those based on polyurethane (PU), silane-modified polymer (SMP), and silicone chemistries—are the materials of choice due to their high elasticity, weather resistance, and strong adhesion to concrete, glass, and metal. The global rise in infrastructure investment and climate-resilient construction—particularly in flood-prone and high-humidity regions—has reinforced demand for waterproofing and sealing materials that maintain flexibility under extreme environmental conditions. Moreover, the retrofit and renovation sector continues to drive recurring consumption, making these foundational applications the most stable and lucrative in the market.

Structural elastic bonding and glazing applications represent the high-performance backbone of the elastic adhesives and sealants industry. Structural bonding involves the adhesion of panels, façades, and dissimilar substrates where both strength and flexibility are required to sustain mechanical loads and environmental stresses. These systems are heavily used in curtain wall façades, modular construction, and vehicle assembly, where traditional fasteners are being replaced by lightweight, high-strength adhesive bonds. Meanwhile, glazing and fenestration applications depend on elastic sealants for durable, weatherproof joints that resist UV radiation, temperature extremes, and moisture intrusion over decades of service life. Neutral-cure silicone sealants dominate this segment for their exceptional long-term stability, low shrinkage, and compatibility with glass and metal substrates. As global energy efficiency standards tighten, the use of high-performance glazing sealants in insulating glass units (IGUs) and structural glazing systems is increasing, especially in smart buildings and zero-energy architecture. These applications, while lower in volume than general sealing, represent a premium market characterized by advanced chemistry and high-value formulations that command strong margins and technical differentiation.

The global elastic adhesives and sealants market is led by a concentrated group of high-performance material innovators—Sika AG, Bostik (Arkema Group), H.B. Fuller Company, 3M Company, and Mapei SpA. These industry frontrunners dominate across construction, automotive, transportation, and consumer applications, leveraging advanced chemistries, localized production, and sustainability-focused R&D. Their collective focus remains on multi-material bonding, isocyanate-free technologies, and VOC reduction while meeting rigorous mechanical, thermal, and environmental performance standards.

Sika AG continues to set industry benchmarks in polyurethane and hybrid Sikaflex® sealants, delivering long-term elasticity and adhesion under dynamic load. The company’s SikaForce® and Sikaflex® platforms dominate infrastructure and vehicle assembly, while the Sika Solution Center provides deep technical integration support for large-scale construction envelope projects. Its Target Market Strategy focuses on infrastructure, transportation, and waterproofing systems where elastic sealants are paired with liquid-applied membranes for total protection. Sika’s new-generation elastic PU and SMP sealants address sustainability goals with low-VOC formulations, ensuring REACH compliance and occupational safety.

Bostik, part of the Arkema Group, is a pioneer in Silyl Modified Polymer (SMP) adhesives and sealants, offering isocyanate-free alternatives for construction, mobility, and disposable hygiene. Its smart adhesive portfolio includes solutions for elastic battery pack bonding, stretchable hygiene adhesives, and high-movement construction joints. The company’s “Wall & Floor” system integrates waterproofing, tile adhesives, and joint sealants for professional contractors. Bostik’s elastic technologies emphasize bio-based, solvent-free chemistries aligned with Arkema’s sustainability roadmap and are designed to enhance energy efficiency in green buildings and EV mobility platforms.

H.B. Fuller maintains a strong position as a pure-play adhesives manufacturer, specializing in elastic hot melt systems and urethane-based sealants under brands like Full-Care® and Swift®. Its elastic hot melt adhesives are widely used in durable assembly, packaging, and hygiene applications, offering flexibility, low odor, and superior bond integrity under thermal cycling. The company’s Swift® range is optimized for woodworking, furniture assembly, and industrial bonding, featuring high adhesion to multiple substrates. H.B. Fuller is also investing in additive manufacturing and precision dispensing technologies to enable high-speed, automated adhesive application, reinforcing its competitive position in advanced manufacturing.

3M Company continues to lead the viscoelastic adhesive market with its flagship 3M™ VHB™ Tapes, which replace traditional fasteners in automotive, construction, and aerospace applications. These acrylic foam-based tapes provide permanent elastic bonding, superior stress dissipation, and compatibility with low surface energy (LSE) substrates. 3M also integrates complementary products like Polyurethane Sealant 540 and Adhesive Sealant 730 UV, offering long-term UV stability and elasticity. Its recent innovation in conductive and thermal elastic materials supports EV and electronic module bonding, reflecting a strategic expansion into thermal interface adhesives for energy-efficient assemblies.

Mapei SpA has established a strong presence in construction and infrastructure adhesives, offering elastic systems designed for tile installation, facade sealing, and expansion joints. Its MAPEFLEX series includes low-VOC polyurethane sealants with excellent adhesion to concrete, glass, and aluminum. The company focuses on high-movement, high-modulus elastic materials to ensure substrate stability under temperature fluctuations. Mapei’s commitment to sustainable building is reflected in its green-certified formulations and energy-efficient ETICS systems, where elastic bonding agents play a key role in crack prevention and durability. The company’s Southeast Asian expansion (May 2025) strengthens its position in hybrid PU and MS-polymer sealants for regional infrastructure growth.

China remains the largest and fastest-growing market for elastic adhesives and sealants, driven by a dual focus on EV manufacturing scale-up and urban construction megaprojects. In 2024, DuPont inaugurated its new automotive adhesive manufacturing facility in Zhangjiagang, Jiangsu Province, emphasizing advanced elastic bonding solutions tailored to local EV assembly lines. Meanwhile, CATL and other Chinese battery manufacturers are increasing adhesive consumption by up to 15% per EV, as cell-to-pack integration requires fire-resistant, thermally conductive elastic adhesives for structural stability.

The acquisition of Shenzhen Landun Holding by Sika AG strengthened the company’s waterproofing and elastic sealant portfolio in China, addressing rapid infrastructure and real estate expansion. Concurrently, BASF SE’s partnership with Youyi Group supports domestic production of polyurethane and acrylic-based elastic systems, ensuring a resilient raw material supply chain. With strong regulatory momentum under the 14th Five-Year Plan, China’s construction sector continues to prioritize durable façade bonding and modular building adhesives, reinforcing its leadership in Asia-Pacific elastic sealant production and innovation.

The United States elastic adhesives and sealants market is characterized by strong R&D intensity and regulatory-driven innovation, particularly in automotive, aerospace, and construction sectors. American manufacturers such as 3M and H.B. Fuller are investing heavily in bio-based and low-VOC SMP elastic adhesives that replace mechanical fasteners like welds and bolts, promoting lighter and more sustainable assembly methods. 3M’s 2024 launch of next-generation high-strength elastic adhesives highlights a shift toward structural bonding solutions for vehicle chassis, composites, and prefabricated building panels.

The EPA’s tightening VOC regulations—particularly in California and the Midwest—are accelerating market adoption of water-based polyurethane and silyl-modified polymer (SMP) formulations for energy-efficient construction. The aerospace sector, led by Boeing and Lockheed Martin, continues to demand lightweight, fire-resistant elastic bonding materials capable of withstanding high vibration and extreme temperature fluctuations. Federal infrastructure investment programs, under the Infrastructure Investment and Jobs Act (IIJA), are also fueling large-scale use of PU joint sealants and silicone-based expansion systems in roads and bridges.

Germany remains a European leader in specialty chemical and adhesive innovation, anchored by advanced R&D in automotive bonding, construction sealants, and circular economy solutions. Sika AG and Wacker Chemie AG are at the forefront of next-generation polyurethane and silane-terminated polymer (SMP) development, including innovations such as GENIOSIL XM 20 and XM 25, which deliver enhanced elasticity, adhesion, and environmental safety. German suppliers are also advancing crash-toughened elastic polyurethane adhesives, enabling bonding of steel-aluminum hybrid structures without pre-heating—reducing production energy by over 20%.

The Industrieverband Klebstoffe (IVK) reports that elastic adhesives are integral to Europe’s circular economy, particularly in repairable and recyclable automotive, wind energy, and building products. Altana’s Byk division has introduced AI-assisted digital laboratories to accelerate elastic chemical formulation, furthering Germany’s leadership in high-precision industrial adhesives. Regulatory frameworks under EU REACH and the Green Deal continue to steer manufacturers toward solvent-free and low-emission elastic materials, making Germany the benchmark for sustainable adhesive technologies globally.

India’s elastic adhesives and sealants industry is growing rapidly, underpinned by record infrastructure investments, EV manufacturing expansion, and a flourishing construction sector. Major government programs, including Smart Cities Mission and National Infrastructure Pipeline (NIP), are driving large-scale adoption of weather-resistant silicone and SMP elastic sealants for bridge expansion joints, glass façades, and modular construction systems. In 2024, Dow partnered with Glass Wall Systems India to supply DOWSIL façade bonding solutions, catering to the surge in high-rise and commercial construction across metropolitan cities.

The automotive industry is another key driver, with manufacturers increasingly using elastic polyurethane adhesives for two-wheeler and four-wheeler assembly, ensuring lightweight and fuel-efficient designs. Henkel India’s expansion in Pune strengthens supply chain responsiveness to major automotive hubs. Local manufacturers, such as Pidilite Industries, are also investing in fast-setting, moisture-curing formulations to meet the growing need for high-speed adhesive applications in infrastructure and packaging. The trend toward eco-friendly, durable elastic systems positions India as a crucial growth hub in the South Asia construction adhesives market.

Japan continues to define the frontier of precision elastic adhesives and advanced polymer chemistry, supported by strong collaborations among its leading manufacturers such as LINTEC Corp., Toagosei Group, and ThreeBond Co. Ltd. The country is pioneering elastic bonding materials for precision electronics, semiconductors, and automotive applications, where high performance and long-term reliability are critical. R&D efforts are focused on SMP-based systems that deliver high adhesion to composite substrates while maintaining low shrinkage and excellent fatigue resistance.

Japan’s construction industry, guided by stringent seismic building standards, is heavily dependent on highly elastic silicone sealants to absorb structural movement and preserve weatherproofing integrity. Simultaneously, the transportation and EV sectors are expanding use of lightweight elastic structural adhesives to reduce NVH (Noise, Vibration, Harshness) levels. Continuous investment in automated adhesive dispensing technologies ensures precision and repeatability in mass manufacturing, reinforcing Japan’s reputation as a leader in industrial bonding efficiency and quality control.

Switzerland serves as a global innovation hub for specialty elastic adhesives, led by Sika AG’s pioneering developments in polyurethane, hybrid, and silicone-based elastic bonding systems. Sika’s patented Purform® technology has redefined industry standards by reducing monomer content in polyurethane prepolymers, enhancing sustainability and workplace safety while maintaining exceptional durability and elasticity. The technology underpins flagship products such as Sikaflex®, widely used in infrastructure, construction, and automotive manufacturing.

The company’s continuous investment in structural glazing and façade bonding systems supports modern architectural applications requiring high-performance elastic sealants capable of withstanding thermal and dynamic stresses. Sika’s global acquisition strategy—focusing on complementary adhesive firms—has solidified its presence across multiple regions, enabling scalability and innovation. Swiss R&D centers emphasize low-emission, LEED- and BREEAM-compliant sealants, contributing to the global sustainable building materials market. Additionally, Switzerland remains a testing and certification leader, ensuring long-term product reliability under extreme climatic and mechanical stress.

Elastic Adhesives & Sealants Market Report Scope

Elastic Adhesives & Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.9 Billion

|

|

Market Size (2034)

|

$44.9 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Polymer Chemistry (Polyurethane, Silyl-Modified Polymer, Silicone, Epoxy, Acrylic, Others), By Product Type (Adhesives, Sealants), By Formulation (1-Component, 2-Component, Hot Melt, Solvent-Based, Water-Based), By End-Use Industry (Building & Construction, Automotive & Transportation, Industrial Assembly, DIY/Consumer), By Application (Structural Elastic Bonding, Non-Structural Bonding, Glazing & Fenestration, Joint Sealing, Waterproofing, Sound Damping, Lamination), By Function (Elasticity/Flexibility, Cure Rate, Adhesion to Substrates, Durability, Fire Resistance

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, 3M Company, H.B. Fuller Company, Arkema Group, Dow Inc., Wacker Chemie AG, Huntsman Corporation, BASF SE, RPM International Inc., DuPont, Illinois Tool Works Inc., Pidilite Industries Ltd., Kaneka Corporation, Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Polymer Chemistry

- Polyurethane

- Silyl-Modified Polymer

- Silicone

- Epoxy

- Acrylic

- Others

By Product Type

By Formulation/Technology

- 1-Component

- 2-Component

- Hot Melt

- Solvent-Based

- Water-Based

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Industrial Assembly

- DIY/Consumer

By Application Type

- Structural Elastic Bonding

- Non-Structural Bonding

- Glazing & Fenestration

- Joint Sealing

- Waterproofing

- Sound Damping

- Lamination

By Function

- Elasticity/Flexibility

- Cure Rate

- Adhesion to Substrates

- Durability

- Fire Resistance

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- Sika AG

- 3M Company

- H.B. Fuller Company

- Arkema Group

- Dow Inc.

- Wacker Chemie AG

- Huntsman Corporation

- BASF SE

- RPM International Inc.

- DuPont

- Illinois Tool Works Inc.

- Pidilite Industries Ltd.

- Kaneka Corporation

- Jowat SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Elastic Adhesives and Sealants Market with a decision-grade lens on performance, sustainability, and total cost-in-use across construction, mobility, electronics, and industrial assembly. It presents analysis reviews of polymer chemistries, cure technologies, and end-use workflows; highlights breakthroughs in isocyanate-free SMP platforms, low-VOC/solvent-free systems, thermally conductive elastic bond-lines for EV battery architectures, and high-movement façade sealants validated to international standards. The study integrates specification trends, regulatory inflection points, sourcing risks, and capacity shifts to benchmark suppliers and map profitable niches through 2034—making this report an essential resource for materials strategists, R&D formulators, procurement leaders, application engineers, and investors seeking defensible choices on product design, supplier selection, and market entry.

Scope Highlights

Segmentation:

- By Polymer Chemistry: Polyurethane; Silyl-Modified Polymer; Silicone; Epoxy; Acrylic; Others.

- By Product Type: Adhesives; Sealants.

- By Formulation/Technology: 1-Component; 2-Component; Hot Melt; Solvent-Based; Water-Based.

- By End-Use Industry: Building & Construction; Automotive & Transportation; Industrial Assembly; DIY/Consumer.

- By Application Type: Structural Elastic Bonding; Non-Structural Bonding; Glazing & Fenestration; Joint Sealing; Waterproofing; Sound Damping; Lamination.

- By Function: Elasticity/Flexibility; Cure Rate; Adhesion to Substrates; Durability; Fire Resistance.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: 15+ company analyses/profiles covering portfolios, pipeline innovations, sustainability pathways, and go-to-market strategies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.