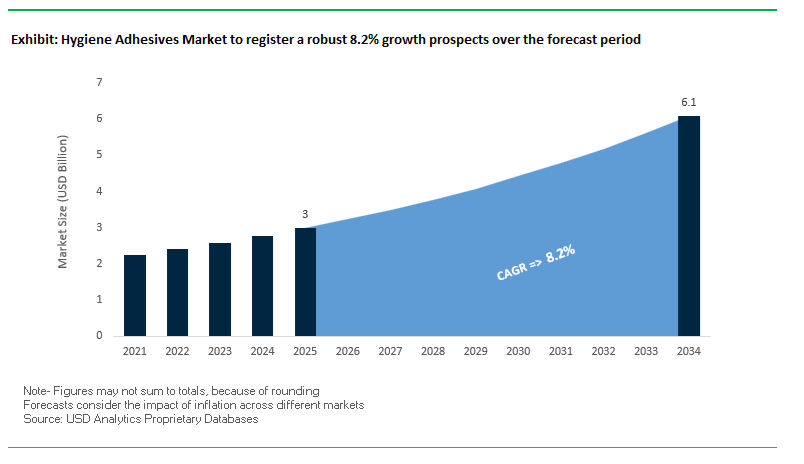

The Global Hygiene Adhesives Market is projected to expand from USD 3.0 billion in 2025 to USD 6.1 billion by 2034, advancing at a CAGR of 8.2%, as hygiene product manufacturers recalibrate adhesive selection around skin safety, process efficiency, and lifecycle sustainability. Growth is structurally anchored in rising global output of baby diapers, adult incontinence products, and feminine hygiene solutions, where adhesives are no longer auxiliary materials but core functional components governing fit, comfort, odor neutrality, and long-duration wear performance. This shift is accelerating the replacement of legacy rubber-based systems with low-VOC hot melt adhesives built on metallocene polyolefin (mPO) and advanced olefin chemistries, which deliver consistent bonding at reduced coat weights while supporting increasingly stringent environmental and consumer safety expectations.

From a performance and OEM qualification standpoint, hygiene adhesives are being engineered to meet mechanical durability under dynamic strain rather than peak bond strength alone. Leading suppliers such as Henkel, H.B. Fuller, and Arkema (Bostik) have focused R&D on elastic attachment and construction adhesives that maintain high creep resistance at low application weights, a critical requirement in pull-ups and adult incontinence products where elastic fatigue directly correlates with leakage risk and wearer dissatisfaction. In parallel, low-odor and hypoallergenic formulations have moved from premium features to baseline specifications, particularly in baby and feminine hygiene categories, as brand owners increasingly differentiate on skin health, sensory neutrality, and consumer trust rather than absorbency alone.

Manufacturing economics and sustainability targets are reinforcing these material transitions. mPO-based hygiene HMAs offer superior thermal stability in melt tanks, significantly reducing char formation, gel build-up, and unplanned downtime on high-speed nonwoven converting lines—an operational advantage that directly improves yield and asset utilization at scale. At the same time, sustainability has become a procurement gate rather than a marketing claim. Major adhesive producers are commercializing bio-based hygiene adhesives with bio-content exceeding 70%, enabling global FMCG companies to advance EU Green Deal alignment, Scope 3 emission reduction, and circular economy commitments without disrupting established production platforms.

The hygiene adhesives market is advancing rapidly with collaborative decarbonization projects, regulatory interventions, and product efficiency innovations defining the competitive landscape.

In October 2025, Henkel Adhesive Technologies expanded its partnership with Dow, marking a pivotal move toward low-carbon adhesive manufacturing. By integrating renewable feedstocks, Henkel aims to cut product carbon footprints by up to 40%, setting a new sustainability benchmark for hot melt hygiene adhesives in Europe and North America. The same month, several U.S. state legislatures implemented free menstrual product programs—a policy shift expanding institutional demand for feminine hygiene supplies, creating predictable, large-volume adhesive procurement channels. Meanwhile, the U.S. FDA’s ongoing investigations (September 2025) into raw material safety in tampons and pads highlight the growing regulatory scrutiny surrounding adhesive components and trace materials, compelling manufacturers to tighten compliance and material transparency.

May 2025 saw H.B. Fuller Company launch a breakthrough Full-Care® core stabilization adhesive, delivering 30% cost-in-use savings via low-temperature application and improved core penetration. This innovation enhances absorbency efficiency and material integrity while reducing energy consumption—a major sustainability advantage. Similarly, Henkel refined its Technomelt Dispomelt range in November 2024, optimizing adhesion to plant-based nonwovens used in next-generation sustainable diapers.

In parallel, Bostik (Arkema Group) advanced its renewable energy sourcing strategy (October 2024) for U.S. operations, underscoring an industry-wide commitment to carbon neutrality in adhesive production. Meridian Adhesives Group strengthened its Asian footprint through the acquisition of PAS Bangkok (December 2024) and the opening of the Penang Application Development Center (March 2025), enhancing localized R&D capabilities for high-speed nonwoven manufacturing in China, Thailand, and Malaysia.

The surge in consumer awareness of skin health and comfort is reshaping adhesive chemistry in the hygiene industry. Increasing sensitivity toward Medical Adhesive-Related Skin Injuries (MARSI)—particularly in geriatric and infant populations—is compelling global manufacturers to innovate atraumatic, hypoallergenic, and breathable hygiene adhesives. Traditional acrylate-based pressure-sensitive adhesives (PSAs), though strong, can cause epidermal stripping upon removal, leading to irritation and skin trauma. The has accelerated research into silicone-based and breathable adhesive technologies, which combine strong adhesion with superior skin compatibility.

Recent academic developments emphasize that specialized silicone PSAs, featuring a low storage modulus (<3×10⁵ Pa), are engineered to maintain consistent tack on rough or irregular skin surfaces while minimizing removal trauma. These formulations offer balanced adhesion and gentle detachment, making them ideal for premium baby diapers, adult incontinence products, and medical-grade sanitary pads. Industry leaders have successfully adapted medical-grade silicone adhesives with pull-off strengths exceeding 3 N/cm²—providing both secure fixation and skin breathability that reduces maceration risks caused by moisture buildup.

In addition, the growing prevalence of Incontinence-Associated Dermatitis (IAD)—with studies showing up to 5.5% incidence among newly incontinent nursing home residents—drives the critical role of hypoallergenic, moisture-resistant adhesives in preventing skin breakdown. The adoption of moisture-vapor-permeable adhesives, combined with nonwoven breathable backsheet technologies, is a key differentiator for brands prioritizing patient comfort, skin integrity, and product safety. As product differentiation increasingly revolves around skin-friendliness and long-wear comfort, manufacturers adopting ultra-gentle silicone or advanced polyolefin adhesives are securing a competitive advantage in the premium hygiene segment.

The hygiene adhesives industry is witnessing a decisive move toward bio-based, renewable, and compostable formulations, driven by global sustainability commitments and tightening environmental regulations. As disposable hygiene products face scrutiny for their environmental footprint, adhesive manufacturers are pioneering eco-friendly hot melt adhesive (HMA) chemistries that combine performance durability with end-of-life degradability.

Recent commercial advancements highlight the successful introduction of bio-based HMAs containing up to 70% renewable raw materials, including natural resins and terpene derivatives, without compromising bonding strength or heat stability. These formulations ensure low odor, high cohesion, and stable viscosity across high-speed manufacturing processes, making them ideal for diaper construction, core stabilization, and feminine care components.

Additionally, global suppliers have introduced bio-derived tackifiers with high optical clarity and superior thermal stability, enabling their use as sustainable substitutes for conventional hydrogenated hydrocarbon resins. These innovations facilitate sustainable diaper production while maintaining high adhesion performance in dynamic conditions. The emphasis on renewable adhesive chemistries is not only a compliance-driven initiative but also a brand differentiation strategy, as hygiene manufacturers integrate carbon reduction, biodegradability, and circular packaging into their long-term ESG frameworks. With regulatory bodies promoting eco-compliance for single-use products, bio-based and compostable hygiene adhesives are fast emerging as a central pillar of next-generation product innovation.

The global rise in aging populations and the increasing destigmatization of adult incontinence are creating a powerful growth engine for the hygiene adhesives industry. As the number of individuals aged 60 and above is expected to nearly double by 2050, the adult incontinence product market is forecasted to expand at double-digit growth rates, driving adhesive demand across elastic attachment, construction, and positioning applications.

Modern adult incontinence products require adhesives that deliver secure fit, elasticity retention, and sustained comfort during extended wear. Adhesives in the category must exhibit exceptional creep resistance—maintaining high bond integrity under continuous stress and elevated temperatures typical of body contact. Recent technological advances in polyolefin-based construction adhesives demonstrate outstanding mechanical and thermal stability, even at low add-on weights, making them ideal for heavy-duty, high-performance applications.

Further, the shift toward body-conforming designs and breathable nonwoven materials necessitates adhesives that ensure seamless integration with elastic components, enhancing wearer comfort and mobility. Manufacturers focusing on low-odor, skin-safe, and temperature-tolerant adhesives are poised to dominate the adult incontinence segment, which represents one of the largest and most lucrative end-use categories within the disposable hygiene adhesives market.

A transformative opportunity lies in the development of flushable, biodegradable, and water-dispersible adhesives designed for next-generation hygiene products. As environmental and waste management concerns intensify, particularly regarding single-use feminine and baby care items, manufacturers are investing in adhesive technologies that enable products to decompose rapidly or disperse safely in wastewater systems.

A landmark innovation in the domain is the world’s first flushable sanitary pad, employing a water-based biodegradable adhesive that dissolves post-use into natural fibers within 30 days, fully meeting global biodegradation standards. The demonstrates a viable path toward reducing solid hygiene waste and redefining sustainability in feminine hygiene. Additionally, the International Water Services Flushability Group (IWSFG) standards are setting industry-wide benchmarks for dispersibility, prompting adhesive suppliers to develop flushable, low-viscosity systems that break down without causing plumbing blockages.

Manufacturers are also establishing flushability testing laboratories to validate compliance, ensuring their products meet global infrastructure compatibility standards. The resulting dispersible adhesives provide strong performance during product use yet degrade efficiently after disposal, representing a critical step toward zero-waste hygiene design. The opportunity aligns with the industry’s larger goal of creating fully sustainable, circular, and environmentally safe hygiene products—bridging the gap between performance and biodegradability.

Hygiene Adhesives Market Share Insights, 2025-2034

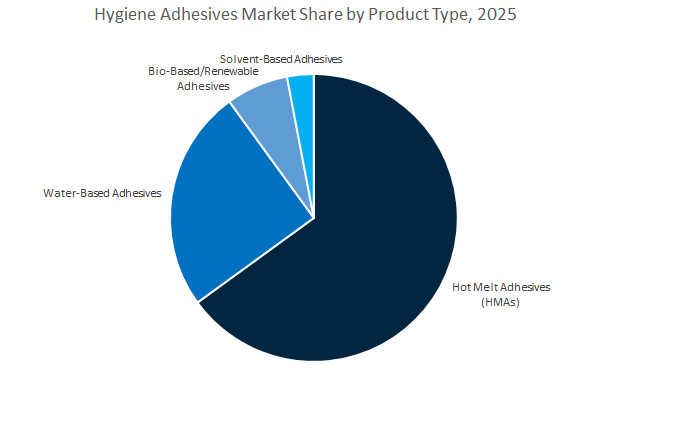

The hot melt adhesives (HMAs) segment dominates the global hygiene adhesives market, accounting for a projected 63.5% share in 2025, firmly establishing its role as the adhesive backbone of diaper, feminine hygiene, and adult incontinence product manufacturing. HMAs are prized for their fast setting time, strong bonding capability, and compatibility with non-woven, film, and elastic substrates, enabling seamless integration into high-speed, automated production lines that can operate at over 1,000 units per minute. These thermoplastic adhesives ensure reliable lamination of topsheets, cores, and backsheets, providing both product integrity and wearer comfort. Their excellent thermal stability, low odor, and controlled open time make them ideal for continuous operations with minimal maintenance downtime. Key innovations in polyolefin- and metallocene-based hot melt systems have improved oxidative stability, tack retention, and substrate versatility, aligning with manufacturers’ efficiency and sustainability goals. Moreover, the rise of bio-compatible and skin-friendly formulations has expanded HMAs’ use in premium hygiene products targeting sensitive consumers and infants.

Water-based adhesives continue to hold a substantial market position, favored for their softness, breathability, and low odor profile, which enhance skin comfort and air permeability in products with direct dermal contact. Their use in core stabilization and construction lamination supports breathable hygiene designs, particularly in premium baby diapers and feminine care lines emphasizing comfort and natural feel. Meanwhile, bio-based and renewable adhesives represent the fastest-growing segment, driven by global sustainability initiatives and brand owners’ commitments to circular economy targets. Derived from renewable feedstocks such as bio-polyolefins and starch derivatives, these adhesives reduce carbon footprints while matching the bonding strength of traditional petrochemical-based systems. They are increasingly adopted by European and North American hygiene brands seeking eco-label certifications and sustainable product differentiation. On the other hand, solvent-based adhesives, once common in earlier hygiene designs, have seen a steep decline due to volatile organic compound (VOC) regulations, odor issues, and operator safety concerns.

The construction adhesives segment commands the highest share of the global hygiene adhesives market, projected at 42.2% in 2025, underscoring its essential role as the structural backbone in diaper and hygiene article manufacturing. These adhesives bond nonwoven topsheets, absorbent cores, and breathable backsheets, creating the multilayer architecture that defines product integrity. Their dominance stems from the demand for high cohesive strength, temperature stability, and controlled viscosity, ensuring consistent lamination under high-speed production conditions. Construction adhesives are optimized for thermal and humidity resistance, preserving adhesion even in varying storage and use conditions. Manufacturers are investing in low-viscosity, high-penetration polyolefin hot melts that enhance line efficiency, reduce char formation, and maintain substrate softness, meeting consumer expectations for lightweight, flexible, and comfortable hygiene products.

Elastic attachment adhesives represent the second-largest application area, driven by their critical role in bonding elastic threads, waistbands, and leg cuffs that ensure fit, comfort, and leak protection. These adhesives must maintain high elasticity, creep resistance, and tack retention under repetitive movement, making them central to the performance of premium diapers and adult incontinence products. The growth of active-lifestyle consumers and high-performance hygiene solutions continues to drive demand for elastic adhesives engineered for softness, flexibility, and stretch recovery. Positioning adhesives are strategically vital for feminine hygiene pads, panty liners, and certain adult incontinence products, where light, repositionable tack ensures product placement without residue or discomfort. Manufacturers are focusing on low-odor, non-staining formulations compatible with both nonwoven and textile substrates, aligning with evolving consumer safety and comfort preferences.

Core stabilization adhesives and wetness indicator adhesives, while smaller market segments, serve critical functional roles in product performance and user experience. Core stabilization adhesives enhance absorbent core integrity, preventing material shifting or bunching, which improves liquid management efficiency. Meanwhile, wetness indicator adhesives, often formulated with color-changing additives, add a visual cue for product change timing—particularly valuable in infant and geriatric care segments. These specialized adhesives combine chemical stability, skin safety, and print compatibility, reflecting the industry’s move toward intelligent hygiene products with added functionality.

The Global Hygiene Adhesives Industry is led by key innovators such as H.B. Fuller Company, Henkel AG & Co. KGaA, Bostik (Arkema Group), 3M Company, and Jowat SE. These players dominate the market through advanced polymer chemistry, bio-based innovation, and application-specific expertise across nonwoven, medical, and personal care products.

H.B. Fuller leads in hygiene adhesive innovation with its Full-Care® line, serving baby care, feminine hygiene, and adult incontinence segments. The Full-Care® 7885 formulation allows low-temperature application, cutting energy use and cost by up to 30% while enhancing absorbent core bonding efficiency. Its third-generation olefin technology enables rapid reformulation in response to supply challenges, ensuring global supply assurance. The Full-Care® 9300 line’s low-odor, moisture-indicating properties improve user confidence and brand differentiation. A strategic sustainability push positions the Full-Care® portfolio as central to the industry’s circular economy transition.

Henkel’s Technomelt Dispomelt remains the gold standard for low-odor, process-stable hot melt adhesives in hygiene product construction. The company’s 2025 partnership with Dow introduced low-carbon feedstocks, achieving up to 40% carbon footprint reduction. Henkel also supports noise-free and skin-friendly bonding solutions, critical for premium hygiene products. Its Easyflow® pressure-sensitive adhesives (PSAs) enhance bonding to complex substrates like PE films and sustainable nonwovens, while its AQUENCE® water-based adhesives complement high-speed applications.

Bostik (Arkema Group): Driving Circularity and Performance through Smart Adhesive Technology

Bostik, part of Arkema Group, leverages its smart adhesives expertise to enhance sustainability across disposable hygiene applications. With strict adherence to SBTi-validated 2030 climate goals, Bostik integrates bio-based and recycled raw materials into its hygiene adhesives. The company’s R&D emphasizes performance optimization for lightweight, discreet hygiene products, balancing adhesion strength with reduced material usage. Bostik’s compliance-focused design philosophy ensures its adhesives meet future global health and safety standards, positioning it as a leading partner for ESG-driven manufacturers.

3M Company: Technical Adhesives for Skin-Friendliness and Rapid Manufacturing

3M plays a strategic role in the medical and hygiene adhesive segment, delivering pressure-sensitive and hot melt systems optimized for skin contact safety and rapid bonding performance. Its adhesives achieve instant adhesion within seconds, critical for automated nonwoven converting lines. 3M’s expertise in high-bond medical tapes and PSA systems extends to adult incontinence and medical disposables, emphasizing hypoallergenic and durable adhesion. The company’s innovation pipeline also supports recyclable adhesive technologies, contributing to eco-friendly product end-of-life solutions.

Jowat SE: Engineering Precision Adhesives for Elastic Attachment and Nonwoven Lamination

Jowat SE offers tailored hot melt adhesives for nonwoven product construction, specializing in elastic attachment, core stabilization, and backsheet lamination. Its formulations allow low-temperature application, lowering energy usage and thermal stress on substrates. Designed for spandex/elastic bonding, Jowat’s HMAs provide outstanding cohesion and adhesion, ensuring durable elasticity and wearer comfort. Through its technical advisory network, Jowat optimizes customer processes for machine compatibility and consistent runnability, making it a preferred partner for customized hygiene adhesive solutions.

The United States hygiene adhesives market stands at the forefront of technological innovation, particularly in medical-grade wearables, bio-based polymers, and low-VOC formulations. With a strong alignment between regulatory policies, sustainability goals, and industry R&D investments, the U.S. is driving global trends in skin-friendly, high-performance hygiene adhesive systems.

A key milestone was set by 3M Company, which unveiled an advanced medical adhesive capable of maintaining skin adhesion for up to 28 days, doubling the industry benchmark for long-term wearables and sensors. The breakthrough represents a significant step forward for transdermal drug delivery patches and remote health monitoring devices, both heavily reliant on gentle, biocompatible adhesives.

In parallel, the Adhesive and Sealant Council (ASC) is spearheading its Sustainability Initiative, promoting Circular Economy principles through education and collaboration among major players like Arkema’s Bostik and H.B. Fuller Company. Bostik’s $27 million expansion of its Middleton, Massachusetts plant boosts polyester resin capacity crucial for high molecular weight hygiene adhesives, while the U.S. Environmental Protection Agency (EPA) continues to advocate for sustainable manufacturing practices, reinforcing the shift toward low-emission and biodegradable adhesive chemistries.

Innovators such as H.B. Fuller are also introducing Swift Melt™ 1515-I, a biocompatible adhesive specifically designed for microporous medical tapes, meeting ISO 10993 standards. The developments position the U.S. as a global center of excellence for sustainable, long-wear hygiene adhesive technologies serving both medical and consumer care markets.

China continues to dominate the Asia-Pacific hygiene adhesives market, driven by exponential growth in nonwoven materials production, smart hygiene product R&D, and green manufacturing initiatives. In 2024 alone, China added 24 spunlace, 142 needlepunch, and 32 spunbond/meltblown lines, dramatically increasing nonwoven output and cementing its position as a global supply hub for diapers, feminine hygiene, and adult incontinence products.

Government-led initiatives under China’s green policy framework are accelerating the adoption of eco-friendly adhesive chemistries, favoring low-VOC and solvent-free systems across hygiene applications. Moreover, R&D is expanding into Smart Hygiene Adhesives that integrate functionalities such as humidity-sensing technology in adult incontinence products, showcasing the industry’s move toward intelligent, functional hygiene materials. China’s combination of massive production capacity and advancing technology ensures its continued dominance as a key driver of innovation and supply in the global hygiene adhesives sector.

Germany represents Europe’s most progressive hub for sustainable hygiene adhesive technologies, underpinned by stringent EU environmental standards and corporate carbon-neutral commitments. Henkel AG & Co. KGaA, a global adhesives leader, aims for carbon-neutral production by 2030 across its Adhesive Technologies business, including its flagship TECHNOMELT hygiene portfolio—demonstrating Germany’s strategic commitment to sustainable manufacturing excellence.

The newly implemented Ecodesign for Sustainable Products Regulation (ESPR) and the EU Circular Economy Action Plan are reshaping adhesive innovation by demanding durability, recyclability, and repairability across all physical products. European manufacturers are responding by developing Debond-on-Demand Adhesives, which enable easier separation of nonwoven materials during recycling, aligning with the EU’s closed-loop resource recovery goals.

Furthermore, new textile waste directives require producers to finance the collection and recycling of hygiene-related nonwovens, spurring demand for low-contamination adhesive systems that facilitate material reuse. Henkel’s introduction of an isobornyl acrylate (IBOA)-free, light-cure medical adhesive marks another milestone, ensuring superior skin safety and compliance with REACH and MDR regulations.

Japan’s hygiene adhesives market is characterized by unmatched innovation in precision skin-contact adhesives, pressure-sensitive systems, and wearable-compatible bonding technologies. With companies like Nitto Denko Corporation and Lintec Corporation leading R&D, Japan continues to refine adhesive formulations that prioritize comfort, safety, and extended wear duration.

Japanese manufacturers are developing highly specialized PSAs that balance gentle skin adhesion, breathability, and flexibility, essential for transdermal patches, medical sensors, and baby care products. Innovations support up to 30 days of wear, providing durable adhesion without residue or skin irritation—ideal for healthcare monitoring devices and aging population care solutions.

Furthermore, Japan’s rapidly aging demographic continues to boost demand in the adult incontinence (AI) market, fostering continuous innovation in stretch adhesives, odor barrier films, and wetness indicator bonds. Material scientists are also advancing breathable, moisture-regulating adhesive compositions for greater comfort in baby and adult hygiene applications. By integrating skin science, material engineering, and consumer safety, Japan sets the global standard for precision-engineered hygiene adhesive performance.

Brazil is rapidly emerging as a strategic hub for hygiene adhesives innovation in Latin America, fueled by local investments, eco-regulation reforms, and rising personal care manufacturing capacity. Henkel’s announcement to build a new Inspiration Center for Adhesive Technologies in São Paulo marks a major step in regionalizing R&D, enabling faster collaboration with local hygiene product manufacturers and expanding sustainable adhesive portfolios.

In parallel, Actega consolidated all its Brazilian operations into a state-of-the-art facility in Araçariguama, strengthening regional production of specialty coatings, inks, and adhesives, while All4Labels’ €3 million investment in Northeastern Brazil enhances the availability of adhesive label solutions for food, health, and hygiene applications.

Brazil’s environmental legislation mandates lower VOC emissions, accelerating the shift toward bio-based and eco-friendly adhesive systems. Combined with the country’s growing nonwoven and personal care manufacturing sectors, Brazil is positioning itself as the Latin American leader in sustainable hygiene adhesive production, leveraging its natural resource base and rapidly modernizing industrial ecosystem.

Hygiene Adhesives Market Report Scope

Hygiene Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3 Billion

|

|

Market Size (2034)

|

$6.1 Billion

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Product Type (Hot Melt Adhesives, Water-Based Adhesives, Solvent-Based Adhesives, Bio-Based/Renewable Adhesives), By Application (Construction Adhesives, Elastic Attachment Adhesives, Positioning Adhesives, Core Stabilization Adhesives, Wetness Indicator Adhesives), By End-User (Baby Diapers, Adult Incontinence Products, Feminine Hygiene Products, Medical Disposables, Wipes

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema S.A., 3M Company, Dow Inc., Sika AG, Jowat SE, Wacker Chemie AG, DIC Corporation, Pidilite Industries Ltd., Bemis Associates Inc., Adhesives Research, Inc., Paramelt B.V., Colquímica Adhesives, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type/Resin Base

- Hot Melt Adhesives

- Water-Based Adhesives

- Solvent-Based Adhesives

- Bio-Based/Renewable Adhesives

By Application/Function

- Construction Adhesives

- Elastic Attachment Adhesives

- Positioning Adhesives

- Core Stabilization Adhesives

- Wetness Indicator Adhesives

By End-Use Product

- Baby Diapers

- Adult Incontinence Products

- Feminine Hygiene Products

- Medical Disposables

- Wipes

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Arkema S.A.

- 3M Company

- Dow Inc.

- Sika AG

- Jowat SE

- Wacker Chemie AG

- DIC Corporation

- Pidilite Industries Ltd.

- Bemis Associates Inc.

- Adhesives Research, Inc.

- Paramelt B.V.

- Colquímica Adhesives

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

Tailored for brand owners, converters, and R&D leaders, the USDAnalytics study on the Hygiene Adhesives Market integrates performance engineering with sustainability and skin science—this report investigates how modern chemistries deliver low-odor, creep-resistant bonding at low add-on weights in high-speed nonwoven lines; tracks breakthroughs in bio-based formulations, moisture-vapor-permeable designs, and ultra-gentle skin-friendly systems; analysis reviews decarbonization moves, regulatory scrutiny around NIAS/odor, and line-efficiency levers from melt stability to downtime reduction; and highlights elastic attachment integrity, core stabilization efficacy, and comfort-driven positioning technologies that elevate wearer experience and compliance. Built to support specification, sourcing, and innovation roadmaps, this report is an essential resource for category managers, process engineers, and technical marketers seeking defensible decisions across diapers, adult incontinence, feminine care, medical disposables, and wipes, etc……

Scope Highlights

Segmentation

- By Product Type / Resin Base: Hot Melt Adhesives; Water-Based Adhesives; Solvent-Based Adhesives; Bio-Based/Renewable Adhesives

- By Application / Function: Construction Adhesives; Elastic Attachment Adhesives; Positioning Adhesives; Core Stabilization Adhesives; Wetness Indicator Adhesives

- By End-Use Product: Baby Diapers; Adult Incontinence Products; Feminine Hygiene Products; Medical Disposables; Wipes

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analytical coverage and profiles of 15+ companies (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.