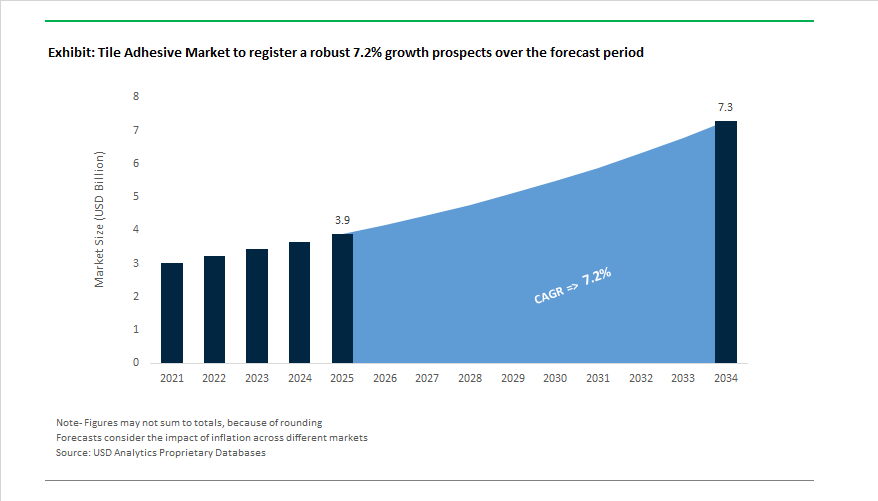

The Global Tile Adhesive Market is projected to grow from USD 3.9 billion in 2025 to USD 7.3 billion by 2034, expanding at a CAGR of 7.2%, as tile installation shifts from a craft-driven trade to a performance-specified construction system. Market growth is being shaped less by tile volumes and more by substrate complexity, labor productivity pressures, and regulatory-driven formulation upgrades, particularly in fast-urbanizing regions.

Cementitious tile adhesives (CTAs) continue to anchor market volume, especially across Asia-Pacific, where rapid residential construction, affordable housing programs, and large-format ceramic adoption sustain demand. However, within this dominant category, manufacturers are upgrading formulations with polymer modification, extended open time, and improved slip resistance to meet modern installation requirements for large-format tiles, thin porcelain slabs, and mixed substrates. Producers such as MAPEI, Sika, Ardex, Saint-Gobain Weber, and Henkel have systematically repositioned cementitious products from commodity mortars to graded performance classes aligned with EN 12004 and ISO 13007, enabling clearer differentiation on-site.

At the premium end, reaction resin adhesives (epoxy and polyurethane) are gaining momentum well beyond niche industrial use. These systems are increasingly specified for high-load commercial floors, chemical exposure zones, swimming pools, façades, and exterior insulation systems, where cement-based solutions face durability limits. Their growth is being accelerated by tighter waterproofing, hygiene, and chemical resistance requirements, particularly in healthcare, food processing, and transport infrastructure. While reaction resins account for a smaller share by volume, they deliver disproportionately higher value per installation, reshaping revenue mix for leading suppliers.

The industry is witnessing a mix of sustainable product introductions, portfolio expansion, marketing repositioning, and price actions that reset expectations for spec performance and total installed cost. In May 2023, Sika closed the MBCC Group acquisition, materially broadening its construction chemicals footprint and cross-selling potential for tile adhesive systems across regions. Through 2023–2024, Bostik (Arkema) pursued targeted capacity and portfolio moves: March 2023 a USD 27 million investment in Middleton (MA) to reinforce polyester supply for high-performance adhesive lines; December 2023 a planned acquisition of Arc Building Products to secure an Ireland footprint; and February 2024 an investment in UV acrylic HMPSA, signalling sustained focus on advanced adhesive technologies.

By 2024, pricing and sustainability took center stage. Bostik announced a 5–7% global price increase (March 2024) to offset persistent raw material and energy pressures, while July 2024 saw Magicrete launch a campaign promoting specialized tile adhesives over site-mixed cement, highlighting strength, durability, and speed—a narrative resonating in developing markets. On the innovation front, September 2024, Bostik unveiled Fast Glue Ultra+ with 60% bio-based content, reinforcing the low-VOC/eco trajectory. November 2024, Nuvoco introduced ‘Zero M Tile Adhesive T5’ for both stone and tiles, widening high-performance choices at retail and project sites. December 2024, Arkema finalized the acquisition of Dow’s flexible packaging laminating adhesives business, not tile-specific but strategically accretive to adhesives know-how and global reach.

Momentum carried into 2025 with portfolio and sustainability governance themes. The APAC growth engine remained intact, with major brands sharpening direct-to-contractor routes and specification support for large-format porcelain, tile-on-tile renovations, submerged applications, and deformable substrates. The net effect: broader premium options (epoxy/resin systems), tighter EHS profiles, stronger local footprints, and smarter price/value architectures that protect margins while meeting jobsite performance KPIs.

Market Trend 1: Rapid Shift Toward Polymer-Modified, Single-Component Tile Adhesives for Large-Format Installation

The rise of large-format and low-porosity tiles, such as porcelain slabs and engineered stones, is fundamentally redefining adhesive performance standards. Polymer-modified, single-component tile adhesives are emerging as the global benchmark for high-bond strength, superior flexibility, and efficient installation.

Industry data indicates that flexible adhesives have seen a 29% surge in adoption across major urban construction markets like Dubai, Seoul, and New York over the past two years, driven by their ability to absorb stresses caused by thermal expansion, vibration, and building movement. The resilience makes them indispensable for securing oversized tiles on walls and floors in high-rise and commercial structures.

Further, global commercial installations exceed 120 million square feet annually using polymer-based adhesives, a statistic that drives the dominance of the segment in retail and corporate flooring applications where high-traffic durability is essential. The market is also witnessing rapid adoption of ready-mix single-component tile adhesives, which allow for light foot traffic within 24 hours, compared to the 72-hour curing cycle required by cement-sand mortars.

The efficiency, coupled with compliance with international standards such as ANSI A118.15 and ISO 13007, is propelling the transition from traditional mortar systems toward high-performance polymer-modified products that deliver time savings, consistency, and superior adhesion performance for both residential and commercial flooring applications.

Market Trend 2: Expansion of Low-Dust, Rapid-Setting Tile Adhesives for Commercial Renovation Projects

The global construction and renovation sectors are increasingly adopting low-dust and rapid-setting tile adhesives that improve job site safety and drastically shorten project timelines. These advanced formulations are essential for health-sensitive renovation environments such as airports, hospitals, and shopping centers, where continuous operations demand minimal downtime and reduced air contamination.

Stringent occupational safety regulations across Europe, North America, and Asia-Pacific are accelerating the shift. Low-dust adhesive technologies—developed through specialized polymer encapsulation—are reducing airborne particulate emissions by more than 90%, in full compliance with health and environmental risk assessment standards such as OSHA’s Respirable Dust Regulation and the EU’s Workplace Exposure Directive.

Rapid-setting adhesives have also become the material of choice for “fast-track” renovation projects, enabling grouting within 3–4 hours and supporting heavy load-bearing use within 24–48 hours. The capability allows contractors to re-open critical facilities—such as retail stores and airport concourses—within a single day, providing unmatched economic value.

A major trend boosting demand is the “tile-on-tile” renovation technique, made possible by advanced polymer-modified adhesives that bond securely to existing substrates. The eliminates the dust-intensive demolition phase, reduces waste, and ensures lower environmental impact while maintaining long-term adhesion integrity.

Market Opportunity 1: Development of Crack-Isolation and Uncoupling Systems for Challenging Substrates

The complexity of modern flooring systems—ranging from radiant heated floors to structurally dynamic concrete slabs—is creating high-value opportunities for crack-isolation and uncoupling membrane systems. These integrated installation solutions are engineered to absorb horizontal stress and prevent tile cracking, ensuring the longevity of high-value flooring installations.

Horizontal substrate movement, caused by thermal cycles and concrete shrinkage, remains the leading cause of tile delamination. To counteract the, manufacturers are commercializing multi-layered uncoupling systems that combine vapor equalization channels, waterproof membranes, and specialized polymer adhesives to maintain tile stability. Leading brands offer up to ten distinct crack-isolation systems, each tailored for substrates such as concrete, gypsum, or heated screeds.

The introduction of tile adhesives compatible with non-traditional surfaces—including existing vinyl, metal, and moisture-compromised concrete—has significantly expanded market applicability. Additionally, major suppliers across North America and Europe are providing lifetime warranties for installations that use a complete system (membrane, adhesive, and grout), underscoring the technical reliability and maturity of modern crack-bridging solutions.

Market Opportunity 2: Advancement of Photocatalytic Tile Adhesives with Self-Cleaning and Air-Purifying Properties

The next major frontier in tile adhesives lies in functional, photocatalytic formulations designed for self-cleaning, air-purifying, and antimicrobial applications. With rising demand for sustainable, low-maintenance infrastructure—particularly in healthcare, hospitality, and public facilities—the integration of titanium dioxide (TiO₂) and similar photocatalytic nanoparticles into adhesives and grouts is becoming a disruptive innovation trend.

Scientific research has validated that TiO₂-based photocatalytic materials actively degrade VOCs, NOx, and SOx under light exposure, transforming pollutants into harmless compounds like CO₂ and water. The dual-function technology not only enhances indoor air quality but also keeps tiled surfaces visibly clean by oxidizing organic deposits, significantly cutting long-term maintenance costs.

Commercial adoption is well-documented—Japan’s construction sector achieved up to 60% market penetration of photocatalytic coatings and adhesives in select segments as early as 2003, demonstrating proven consumer and institutional acceptance. The economic advantage is equally compelling: reductions in facade cleaning frequency and associated costs make photocatalytic adhesives particularly attractive for large commercial and public structures, such as hospitals, schools, and airports.

With green building certifications such as LEED and BREEAM emphasizing life-cycle sustainability, self-cleaning tile adhesives represent an emerging market segment poised to align with both environmental policy and cost-efficiency trends in construction.

Tile Adhesive Market Share Insights, 2025-2034

Market Share by Application Method

The thin-set installation method overwhelmingly dominates the global tile adhesive industry, accounting for an estimated 71.6% of the projected 2025 market share. This dominance reflects the widespread transition toward modern tiling systems, particularly for porcelain, vitrified, and large-format tiles, where thin-set adhesives provide superior adhesion, faster setting times, and efficient material utilization. The method’s advantages—such as reduced thickness, lower weight, and compatibility with high-performance substrates—make it the preferred installation choice across residential, commercial, and institutional projects. The trend toward lightweight construction and modular building designs further enhances its adoption, as contractors seek adhesives that ensure uniform bonding strength, durability, and minimal shrinkage. Additionally, thin-set adhesives are increasingly formulated with polymer modifications, improving flexibility, water retention, and crack resistance—qualities essential for high-traffic or moisture-prone areas.

On the other hand, the thick-bed installation method retains a smaller yet essential market niche. It remains critical for projects involving uneven substrates, stone tile installations, or industrial flooring systems that demand a thicker mortar bed to achieve level surfaces and improved load-bearing capability. While its use is gradually declining in modern construction, it continues to play a vital role in renovation projects, particularly in older buildings and restoration works where floor irregularities are common. Furthermore, the rise in heritage restoration and luxury stone flooring segments is sustaining the demand for thick-bed adhesives, as they provide both structural stability and superior mechanical anchorage for heavy tile applications.

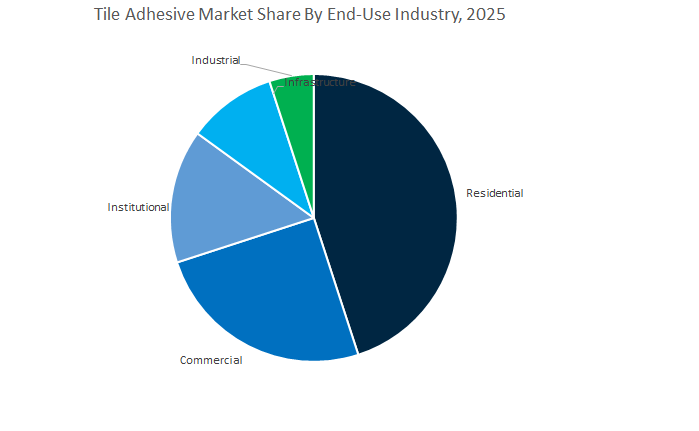

Market Share by End-Use Sector

The residential sector leads the global tile adhesive market, accounting for roughly 44.6% of the projected 2025 market share, and serves as the primary driver of adhesive demand worldwide. Rapid urbanization, rising disposable incomes, and the growing popularity of aesthetic interior designs have significantly boosted the consumption of tile adhesives across new housing developments and home renovation projects. In particular, post-pandemic trends have accelerated spending on home improvement, remodeling, and DIY applications, where consumers prefer durable and visually appealing flooring and wall finishes. Adhesive manufacturers are responding with ready-mix, eco-friendly, and fast-setting formulations, catering to both professionals and homeowners. The growing use of ceramic, porcelain, and decorative tiles in bathrooms, kitchens, and living spaces continues to strengthen the residential demand base.

Meanwhile, the commercial and institutional sectors represent a stable and lucrative segment of the market, driven by office complexes, hospitality projects, healthcare facilities, and educational institutions. These settings demand premium adhesives engineered for high-traffic resistance, slip prevention, and long-term durability under continuous mechanical and chemical stress. Additionally, the infrastructure and industrial segments, though smaller in volume, are high-value niches that require specialized tile adhesive formulations designed for extreme conditions. Applications in swimming pools, tunnels, facades, food processing plants, and chemical facilities necessitate adhesives with superior bonding strength, water impermeability, and chemical and thermal resistance. These industrial-grade adhesives often employ epoxy or polymer-modified cement bases to deliver enhanced performance in structurally demanding environments.

A handful of global and regional champions compete on system breadth (adhesives, grouts, membranes), sustainability certifications (EC1 Plus/low VOC), technical support, and project logistics. The winners pair chemistry leadership with contractor enablement—from substrate prep to grout sealing—to deliver predictable, defect-free installations at scale.

Overview (4–5 lines).

Global leaders are consolidating share through full installation systems, site training, and specification selling. Cementitious remains the volume anchor, but reaction resin growth, APAC scale, and direct sales dominance recalibrate strategies. Across the board, vendors emphasize eco labels, quick-setting technologies, deformability classes (S1/S2), and compatibility for large-format and low-porosity tiles. Expect continued bolt-on M&A, plant upgrades, and sustainability-led innovation as brands compete on lifecycle performance and installed cost per m².

Mapei S.p.A. fields a deep lineup: Keraflex (high-performance cementitious), Kerapoxy (two-component epoxy for chemical resistance), and Ultralite (lightweight technology) to cover standard to specialty installs. Recent focus on very low VOC (EC1 Plus) solutions aligns with green building requirements and indoor air quality goals. With dedicated plants (including India) and strong ceramics & stone specialization, Mapei couples R&D with on-site technical service, enabling contractor productivity and spec-backed risk reduction on large commercial projects.

Sika AG’s SikaCeram portfolio—e.g., SikaCeram®-288 Flex S1 for large-format/deformable substrates—anchors its tile offer, complemented by polyurethane resin options like SikaCeram®-428 Super Bond T for natural stone/marble on challenging bases. The MBCC acquisition (May 2023) amplifies technology breadth and channel access. Sika’s differentiation is complete systems—primers, waterproofing membranes, grouts—plus application engineering, supporting complex builds with predictable cycle times.

Saint-Gobain Weber delivers polymer-modified cementitious grades such as weberset classic (vitrified/tile-on-tile) and weberset flex for substrate movement/large formats. Specialty SKUs like weberset glass mosaic target submerged environments (pools), while low-VOC profiles align with healthy home trends. Continuous improvements—e.g., self-curing properties—aim to cut labor steps and reduce callbacks, a key value driver for professional tilers and builders.

Henkel AG & Co. KGaA leverages its Adhesive Technologies scale to bring cross-industry innovation (from electronics/automotive/packaging) into construction and craftsmen segments. With a strong R&D and open innovation stance, Henkel addresses urbanization megatrends, offering integrated sealing, bonding, and flooring systems around tilework. The strategy: system compatibility, professional productivity, and sustainability, supporting both new build and renovation specifications.

Bostik (Arkema Group) pursues a bolt-on acquisition path (e.g., Arc Building Products—Dec 2023) to enhance local manufacturing and time-to-market. Product innovation highlights include Bostik Fast Glue Ultra+ (Sept 2024) with 60% bio-based content, reflecting Arkema’s specialty materials strategy. With a comprehensive Wall & Floor portfolio—from Conflex to Evoflex—Bostik targets large-format, rapid-drying, and flexible installs across new builds and remodeling, aligning performance with eco design expectations.

Pidilite Industries (Roff brand) offers high-performance tile adhesives for ceramic, porcelain, and natural stone, widely adopted by professional tilers in developing markets. Backed by Pidilite’s brand equity and deep distribution in India, Roff and Dr. Fixit cover water-resistant and outdoor applications with a focus on ease of use and consistent bonding. The strategic play is high-volume residential with reliable performance and readily available technical support.

Country Analysis: Expanding Global Footprint of the Tile Adhesive Industry

China – Asia-Pacific’s Engine for Sustainable and High-Performance Tile Adhesive Manufacturing

China remains the largest manufacturing and R&D hub for cementitious and dispersion-based tile adhesives, supported by its booming urbanization and government-driven sustainability agenda. Under the 14th Five-Year Plan, the Chinese government has mandated that over 70% of new urban buildings must meet Green Building Standards by 2025, driving a surge in demand for low-VOC, polymer-modified tile adhesives. The sustainability focus is pushing local manufacturers to develop eco-friendly, flexible, and highly durable thin-set adhesive systems, optimized for modern high-rise construction and energy-efficient designs.

The shift toward large-format tiles and porcelain slabs in residential and commercial buildings has significantly influenced the market’s evolution. The trend necessitates high-deformability adhesives (C2 S1/S2 classified) capable of bonding heavy tiles with minimal shrinkage or cracking. Major multinational companies and domestic leaders have established localized R&D facilities in China to develop rapid-setting and frost-resistant tile adhesives suitable for extreme climate variations and accelerated construction cycles. With a combination of regulatory pressure, infrastructure growth, and technical innovation, China’s tile adhesive industry continues to be the benchmark for high-volume, high-performance manufacturing in the Asia-Pacific region.

India – Fastest-Growing Market Fueled by Smart City Infrastructure and Housing Demand

India’s tile adhesive industry is undergoing a significant transformation, driven by rapid urbanization, government infrastructure investments, and changing consumer preferences toward durable, pre-mixed adhesives. Major initiatives such as the Smart Cities Mission and Pradhan Mantri Awas Yojana (PMAY) have accelerated adoption of ready-mix polymer-modified tile adhesives, replacing conventional sand-cement mortars that are labor-intensive and less durable. The rise of vitrified and large-format ceramic tiles in modern residential and commercial projects further amplifies the demand for high-bond-strength polymeric adhesives with greater flexibility and water resistance.

Sika AG’s 2024 launch of a 40-kilotons-per-year facility in Andhra Pradesh underscores the market’s industrial maturity, focusing on high-performance tile adhesives that meet the needs of India’s fast-paced construction environment. Additionally, domestic brands like Pidilite Industries (Roff) are aggressively expanding their market share through strong marketing campaigns promoting superior strength, ease of use, and moisture tolerance. The developments indicate a strategic shift toward professional-grade, high-performance products, supported by increased technical awareness among contractors and builders. As India modernizes its infrastructure and real estate, the demand for cementitious and polymer-modified adhesives is expected to grow exponentially, establishing the country as a global growth leader in the tile adhesive sector.

United States – Pioneering High-Performance and Sustainable Tile Adhesion Technologies

The United States tile adhesive market is characterized by innovation in low-VOC, high-flexibility, and premium-grade adhesives, especially across the renovation and remodeling sectors. Home improvement trends, particularly in kitchen and bathroom remodels, have driven sustained demand for dispersion-based tile adhesives with low odor and easy application, appealing to both DIY consumers and professional installers. The Inflation Reduction Act (IRA) of 2022 has further accelerated the adoption of energy-efficient building practices, indirectly supporting the use of adhesive systems compatible with underfloor heating, radiant cooling, and moisture management in modern buildings.

From a technical standpoint, ANSI A118.15 and A118.11 standards have reshaped the U.S. commercial construction landscape, pushing manufacturers toward deformable, polymer-rich cementitious adhesives with superior curing speed and tensile strength. Major market players, including 3M Company, LATICRETE, and MAPEI, are introducing advanced formulations tailored for high-moisture environments and fast-track installations. The U.S. tile adhesive sector thus represents a high-value, innovation-driven market—where eco-certified, rapid-bond, and heat-tolerant adhesive systems are becoming the new industry benchmark.

Germany – European Leader in Low-Emission and Smart Building Tile Adhesives

Germany continues to be a technology and sustainability powerhouse in the global tile adhesive industry, driven by its strict environmental regulations and precision engineering in construction materials. The EMICODE EC1 and EC1 Plus certifications have set the standard for low-emission and solvent-free tile adhesives, prompting leading companies like Henkel, BASF, and Ardex to focus on sustainable, polymer-modified cementitious and epoxy-based formulations. The aligns with the EU’s broader decarbonization and Circular Economy Action Plan, emphasizing sustainable raw materials and recyclable packaging.

High-demand sectors such as industrial flooring, cleanrooms, and chemical processing plants are driving adoption of reaction resin adhesives (epoxy and polyurethane-based), prized for their chemical resistance and long-term durability. Furthermore, German manufacturers are pioneering adhesives optimized for heated flooring systems and energy-efficient buildings, offering enhanced flexibility under thermal expansion cycles. The emphasis on formulation purity, structural strength, and eco-performance solidifies Germany’s position as a core innovation hub for advanced and sustainable tile adhesive technologies in Europe.

Brazil – Rapid Construction Growth Driving High-Volume Tile Adhesive Demand

Brazil represents one of the most dynamic markets for tile adhesives in Latin America, fueled by a combination of residential housing expansion, commercial construction, and modernization of installation practices. With widespread use of Vinyl Acetate Ethylene (VAE)-based dispersion adhesives, the market favors affordable, easy-to-apply, and quick-setting solutions for interior applications in large-scale residential developments. Public and private housing programs have further accelerated the adoption of packaged, ready-mix adhesives that improve installation speed and consistency over conventional mortars.

Local construction chemical producers are increasingly investing in technologies that enhance non-slip performance, longer open time, and improved adhesion consistency, catering to Brazil’s humid and variable climatic conditions. As infrastructure and real estate investment continue to expand, particularly in urban centers such as São Paulo and Rio de Janeiro, the demand for cost-efficient, high-bond-strength tile adhesives is expected to rise sharply. Brazil’s strong focus on installation efficiency and product affordability positions it as a volume-driven yet evolving market for modern tile adhesive solutions.

Saudi Arabia – Giga-Projects Driving Demand for High-Performance Tile Adhesives

Saudi Arabia has emerged as a strategic high-specification market for tile adhesives and sealants, propelled by the Vision 2030 development agenda and major giga-projects such as NEOM, The Line, and Red Sea Global. The projects demand high-durability waterproof, heat-resistant, and frost-resistant adhesives engineered for extreme climatic conditions. Specialized products such as C2 S2-classified polymer-modified cementitious adhesives and epoxy-based tile bonding materials are widely used for exterior cladding, water features, and high-traffic commercial spaces requiring thermal and mechanical stability.

Regulatory bodies in Saudi Arabia are enforcing stringent quality and sustainability standards for all public and commercial construction materials. The has led to the increasing certification of third-party-tested, high-bond-strength adhesives that ensure long service life and superior performance under desert temperature variations. The rapid progression of The mega-infrastructure projects, combined with government mandates favoring eco-certified, high-performance materials, cements Saudi Arabia’s role as the Middle East’s fastest-growing market for premium tile adhesive systems.

Tile Adhesive Market Report Scope

Tile Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$7.3 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Chemistry (Cementitious, Dispersion, Reaction Resin), By Polymer Chemistry (VAE, SB, Acrylic, Epoxy, Polyurethane), By Application Method (Thin-Set, Thick-Bed), By Tile Type (Ceramic, Vitrified, Natural Stone, Glass, Large-Format), By End-User (Residential, Commercial, Institutional, Industrial, Infrastructure), By Usage Area (Internal, External, Dry, Wet

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mapei S.p.A., Sika AG, Bostik, Saint-Gobain Weber, Henkel AG & Co. KGaA, Laticrete International, Inc., ARDEX Group, Pidilite Industries Ltd., BASF SE, H.B. Fuller Company, Fosroc International Limited, MYK LATICRETE India Pvt. Ltd., Ultratech Cement Ltd., Terraco Group, Sherwin-Williams

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Cementitious

- Dispersion

- Reaction Resin

By Polymer Chemistry

- VAE

- SB

- Acrylic

- Epoxy

- Polyurethane

By Application Method

By Tile Type

- Ceramic

- Vitrified

- Natural Stone

- Glass

- Large-Format

By End-Use Sector

- Residential

- Commercial

- Institutional

- Industrial

- Infrastructure

By Usage Area

- Internal

- External

- Dry

- Wet

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Tile Adhesive Market-

- Mapei S.p.A.

- Sika AG

- Bostik

- Saint-Gobain Weber

- Henkel AG & Co. KGaA

- Laticrete International, Inc.

- ARDEX Group

- Pidilite Industries Ltd.

- BASF SE

- H.B. Fuller Company

- Fosroc International Limited

- MYK LATICRETE India Pvt. Ltd.

- Ultratech Cement Ltd.

- Terraco Group

- Sherwin-Williams

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the evolving Tile Adhesive Market through the lens of material chemistry, installation productivity, and channel economics; it curates recent breakthroughs in polymer-modified cementitious systems, reaction resin upgrades for large-format and submerged applications, and low-VOC dispersion technologies, while our analysis reviews specification drivers, contractor workflows, price/value architecture, and sustainability compliance across priority end-uses. It also highlights demand pivots across renovation vs. new build, APAC’s scale advantages, and the accelerating shift to crack-bridging, rapid-set, and tile-on-tile solutions that compress downtime and elevate lifecycle performance. Built for specifiers, procurement leaders, and project owners, this report is an essential resource for benchmarking adhesive selection against substrate conditions, traffic and moisture loads, and ESG targets—translating market signals into practical playbooks for bids, sourcing, and installation quality, etc……

Scope Highlights

Segmentation:

- By Chemistry: Cementitious; Dispersion; Reaction Resin

- By Polymer Chemistry: VAE; SB; Acrylic; Epoxy; Polyurethane

- By Application Method: Thin-Set; Thick-Bed

- By Tile Type: Ceramic; Vitrified; Natural Stone; Glass; Large-Format

- By End-Use Sector: Residential; Commercial; Institutional; Industrial; Infrastructure

- By Usage Area: Internal; External; Dry; Wet

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis/profiles of 15+ companies, including Mapei S.p.A., Sika AG, Bostik, Saint-Gobain Weber, Henkel, Laticrete International, ARDEX Group, Pidilite Industries, BASF, H.B. Fuller, Fosroc, MYK LATICRETE India, Ultratech Cement, Terraco Group, and Sherwin-Williams.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.