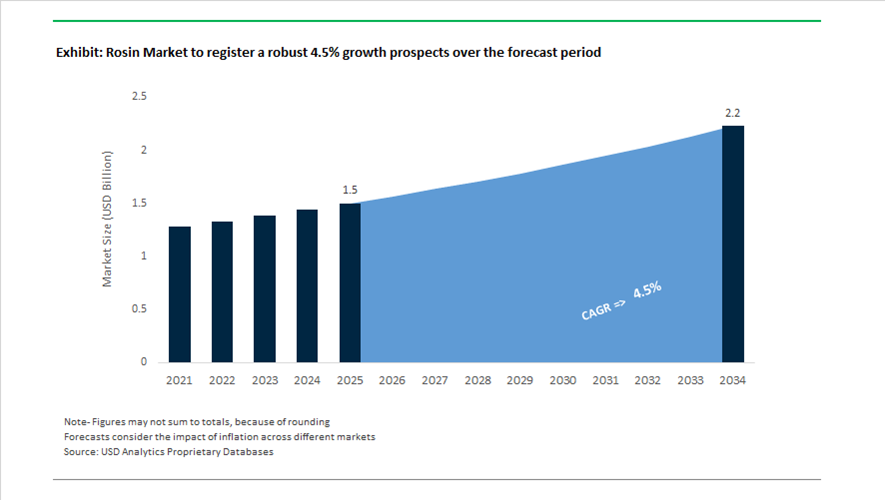

Rosin Market Valued at $1.5 Billion in 2025, Projected to Reach $2.2 Billion by 2034 at 4.5% CAGR

The global rosin market is valued at $1.5 billion in 2025 and is projected to reach $2.2 billion by 2034, expanding at a CAGR of 4.5%. Growth is supported by rising demand for gum rosin, tall oil rosin (TOR), rosin esters, hydrogenated rosin derivatives, bio-based tackifiers, pine chemicals, and pressure-sensitive adhesive (PSA) resins used in packaging adhesives, road markings, rubber compounding, inks, coatings, and automotive sealants. Sustainability mandates and the shift toward renewable feedstocks are strengthening the position of pine-derived resins as alternatives to petroleum-based tackifiers. Supply chain consolidation and ISCC PLUS-certified mass balance production are emerging as competitive differentiators.

Industry restructuring accelerated in 2024. In February 2024, Arakawa Chemical Industries launched upgraded rosin ester series engineered for improved thermal stability and enhanced adhesion performance in automotive adhesives and high-performance industrial coatings. In March 2024, Henkel entered a multi-year strategic partnership with Kraton to source high-performance bio-based tackifiers utilizing Kraton’s patented REvolution™ rosin ester technology, targeting carbon footprint reduction in consumer packaging adhesives. In March 2024, Grupo Resinas Brasil acquired Pinopine, consolidating its global footprint in gum rosin and turpentine derivatives and strengthening Brazil’s leadership in pine oleoresin supply. In May 2024, Foreverest Resources enhanced its global supply chain operations to address surging international demand for natural tackifiers, followed by the November 2024 introduction of customized gum rosin grades tailored for the PSA market. In September 2024, Kraton formally launched its REvolution™ rosin ester platform, delivering superior color stability, low odor, and improved oxidative resistance for hot-melt adhesive formulations.

Strategic recalibration intensified in 2025 and 2026. In August 2025, Kraton executed a service continuity agreement with International Paper to secure uninterrupted operations at its Savannah, Georgia facility, reinforcing stability in tall oil rosin and derivative production. In December 2025, Ingevity provided a strategic portfolio update indicating evaluation of alternatives for its Road Markings and Advanced Polymer Technologies units to streamline operations. In January 2026, Ingevity completed the sale of its North Charleston crude tall oil refinery and most of its Industrial Specialties line, signaling a pivot away from lower-margin pine chemical assets. In the same month, Kraton’s Panama City facility achieved ISCC PLUS certification, enabling mass-balance certified bio-based rosin derivatives to meet verified sustainable sourcing requirements. In February 2026, Kraton appointed Sangwoo Ryu as CEO to accelerate its bio-based innovation roadmap and advance sustainable pine chemical strategies.

The rosin market is increasingly characterized by bio-based tackifier development, hydrogenated and polymerized rosin esters for hot-melt adhesives, PSA-grade customized gum rosin formulations, ISCC PLUS-certified sustainable sourcing, tall oil refinery consolidation, and leadership-driven strategic realignment in pine chemical portfolios. As packaging, automotive, and infrastructure sectors seek renewable resin alternatives with enhanced thermal and oxidative stability, rosin derivatives continue to secure a durable position within the global specialty chemicals value chain.

Key Trends and Emerging Growth Opportunities in the Rosin Market

Strategic Pivot to Renewable Feedstocks for High-Performance Adhesives

The global rosin market is undergoing a strategic repositioning as adhesive and elastomer manufacturers accelerate their exit from fossil-derived C5 and C9 petroleum resins. Rising carbon costs, tightening ESG disclosure norms, and long-term supply volatility in petrochemical feedstocks are elevating rosin, particularly gum rosin and tall oil rosin, as core renewable platform chemicals for next-generation tackifiers. Unlike petroleum resins, rosin-based systems offer inherent bio-content, strong adhesion polarity, and compatibility with modern polymer architectures, making them increasingly attractive for pressure-sensitive adhesives, hot-melt adhesives, and elastomer modification.

This transition is being reinforced by capacity investments aimed at securing pine-based supply chains. In late 2024, Kraton Corporation announced a major expansion of its bio-based specialty materials capacity at its Belpre, Ohio site, with full ramp-up expected by late 2025. The investment is designed to increase the availability of pine-derived polymers and rosin-based derivatives for SBS block copolymers used in packaging, hygiene, and medical adhesives. North America has emerged as a focal point for this shift as brand owners demand traceable, renewable inputs with lower lifecycle emissions.

Market data from the U.S. Department of Agriculture and industry sources indicate that bio-based chemical adoption in adhesives and coatings rose by 14% year over year in 2024. The automotive tire sector stands out as a key demand driver, with pine-based tackifier usage expanding by approximately 11% as tire manufacturers optimize rolling resistance and durability for electric vehicles. In this context, rosin is no longer viewed as a commodity resin but as a strategic enabler of low-carbon, high-performance adhesive systems.

Premiumization of Ultra-Refined and Specialty Rosins

Alongside volume-driven renewable substitution, the rosin market is also experiencing pronounced premiumization in specialty and professional applications. Manufacturers are investing in advanced refining, filtration, and hydrogenation technologies to produce ultra-clarified rosins with tightly controlled color, softening point, and impurity profiles. These high-purity grades are increasingly targeted at segments where performance consistency outweighs cost sensitivity.

The professional musical instrument segment illustrates this trend clearly. As of 2024, professional users accounted for the highest revenue share within the music rosin category, driven by orchestral musicians and conservatories demanding consistent friction behavior across varying humidity and temperature conditions. Engineered and heritage rosins in this niche command price premiums ranging from 300 to 500% over standard industrial grades, and demand has proven resilient even during broader economic slowdowns.

A similar shift is visible in specialty sports and footwear applications, including gymnastics, ballet, and climbing. Industry developments in 2025 highlight a growing emphasis on temperature-stable rosin formulations that maintain grip performance under high humidity and thermal stress. This has accelerated the development of hybrid natural-synthetic rosin systems that mitigate caking and brittleness, further reinforcing premium pricing dynamics and insulating suppliers from commodity market volatility.

Rosin-Based Microencapsulation for Controlled-Release Agrochemicals

One of the most structurally attractive growth opportunities for the rosin market lies in agricultural microencapsulation and controlled-release fertilizer systems. As global farming shifts toward precision agriculture and nutrient efficiency, rosin’s hydrophobicity, biodegradability, and film-forming properties position it as a viable alternative to petrochemical polymer coatings used in controlled-release fertilizers.

Peer-reviewed research published in November 2024 demonstrated that resin-coated fertilizers can extend nutrient release durations by 20 to 30 times compared to uncoated formulations. Field trials on maize and sunflower crops showed substantial improvements in nitrogen-use efficiency, with certain binary nitrogen-phosphorus systems delivering yield increases exceeding 91% relative to unfertilized controls. These performance gains directly address regulatory and environmental pressures to reduce fertilizer runoff and nitrogen losses.

A parallel structural driver is the growing competition for crude tall oil feedstock from renewable diesel and sustainable aviation fuel production under the EU RED III framework. As crude tall oil is increasingly diverted toward energy applications, gum rosin is re-emerging as a strategically important alternative for agricultural encapsulation. Unlike tall oil, gum rosin does not compete directly with biofuel mandates, creating a stable supply and pricing window for agrochemical formulators seeking scalable, bio-based coating materials.

High-Purity Rosin Derivatives for Semiconductor Packaging and Underfill

Advanced electronics packaging represents a non-traditional but rapidly emerging frontier for rosin-based materials. In semiconductor manufacturing, ultra-purified rosin esters and hydrogenated derivatives are being evaluated for use in underfill and molding compounds, particularly in fan-out wafer-level packaging and high-density interconnect applications. These materials offer strong adhesion to silicon and organic substrates while maintaining low ionic contamination levels, a critical requirement for device reliability.

The expansion of 5G infrastructure and AI-enabled computing is intensifying demand for advanced packaging solutions. With global 5G connections projected to reach 1.8 billion by the end of 2025, semiconductor manufacturers are prioritizing materials that support thermal stability, mechanical stress resistance, and miniaturization. Rosin-based underfill components are gaining attention due to their balance of adhesion performance and dielectric stability in densely packed chip architectures.

Geopolitical realignment is further strengthening this opportunity. Trade measures introduced in 2025, including tariffs of up to 50% on certain rosin ester imports, are reshaping global supply chains. As semiconductor fabrication benefits from more than 200 billion dollars in global subsidies, domestic producers in the United States and Europe are well positioned to supply specialty-grade, hydrogenated rosin derivatives to chip packaging ecosystems seeking secure, compliant, and regionally diversified inputs.

Rosin Market Share and Segmentation Insights

Gum Rosin Dominates Global Rosin Supply Due to High Purity and Versatile Industrial Applications

Gum rosin accounted for 48.60% of the rosin market in 2025, making it the most widely used rosin source across industrial applications. Extracted through tapping living pine trees, gum rosin offers superior purity, light color, and consistent quality, which makes it highly suitable for adhesives, printing inks, paper sizing, personal care formulations, and coatings. Major production hubs such as China and Brazil support strong supply for downstream rosin derivative industries including rosin esters and modified rosins. A significant 2025 industry focus is the expansion of sustainable pine tapping practices, where certified forest management programs and improved tapping techniques help maintain tree health and long-term productivity. These initiatives support stable raw material supply while meeting rising sustainability and traceability requirements from global chemical and consumer product manufacturers.

Adhesives & Sealants Lead Rosin Consumption as Demand for High-Performance Tackifiers Expands

Adhesives and sealants represent the largest application segment in the rosin market, accounting for 42.80% of global demand in 2025 due to the extensive use of rosin derivatives as tackifiers in pressure-sensitive and hot-melt adhesive systems. Rosin esters and modified rosin products improve adhesion strength, tack performance, and compatibility with polymer systems, enabling bonding across diverse substrates such as paper, plastics, and metals. Demand is particularly strong in packaging tapes, labels, construction adhesives, and bookbinding adhesives. A major 2025 formulation trend is the growing adoption of hybrid adhesive systems, where rosin-based tackifiers are combined with hydrocarbon resins and performance modifiers. These hybrid systems allow manufacturers to tailor adhesion profiles, thermal stability, and substrate compatibility for demanding applications in automotive assembly, electronics, and high-performance packaging.

Rosin Market Competitive Landscape

The 2026 rosin market is driven by Tall Oil Rosin (TOR), hydrogenated rosin esters, and ISCC PLUS-certified supply chains. Growth is supported by low-VOC adhesive demand, supply volatility mitigation, and increasing adoption of bio-based resins in pressure-sensitive adhesives, coatings, and sustainable infrastructure.

Kraton strengthens tall oil rosin leadership with ISCC PLUS certification and circular paving innovations

Kraton Corporation is reinforcing its dominance in the rosin market through large-scale crude tall oil fractionation and bio-based binder development. ISCC PLUS certification at its Panama City facility enables mass-balance production of sustainable rosin esters and fatty acids. A 10%+ price increase in TOFA across EMEA reflects rising feedstock costs and supply constraints. Leadership transition in 2026 supports acceleration of high-margin specialty polymer and pine chemical integration strategies. CirKular+™ paving solutions utilize rosin chemistry to enhance recycled asphalt performance and circularity. Focus on tall oil derivatives supports consistent supply for adhesives, tires, and infrastructure applications.

Ingevity reshapes pine chemicals portfolio with divestitures and EV-focused advanced materials integration

Ingevity Corporation is restructuring its rosin and pine chemicals business to focus on high-value performance materials and advanced technologies. Divestiture of its crude tall oil refinery and industrial specialties segment streamlines operations toward specialty applications. The company reported $1.17 billion in 2025 revenue and targets long-term growth toward $1.5 billion through portfolio optimization. Integration of carbon nanotube technology through CHASM partnership supports entry into EV battery materials using pine-derived chemistry. Leadership transition in 2026 aligns with its specialty-first strategy. Focus on high-performance rosin derivatives enhances positioning in advanced materials and energy storage applications.

Harima expands rosin resin integration with global sourcing and semiconductor materials growth

Harima Chemicals Group is strengthening its rosin market position through vertical integration and expansion into high-growth electronic materials. Internal sourcing of 60% of rosin requirements provides resilience against global supply volatility. Lawter subsidiary enhances capabilities in rosin-modified resins for adhesives and graphic arts applications. Expansion into semiconductor resists and solder materials supports demand from 5G and automotive electrification sectors. Development of bio-based lycopene production reflects broader carbon recycling initiatives. Global footprint across Asia-Pacific, the U.S., and Europe supports supply chain proximity and market responsiveness.

Eastman advances hydrogenated rosin resins with medical-grade performance and circular resin development

Eastman Chemical Company is positioning itself as a leader in hydrogenated rosin resins for high-purity applications. Foral™ and Staybelite™ products meet stringent requirements for medical adhesives and food-grade applications, offering superior oxidative stability and color retention. Cost optimization initiatives targeting up to $250 million support competitive pricing against synthetic alternatives. Integration of molecular recycling technology enables development of hybrid circular resins combining bio-based rosin with recycled feedstocks. Strategic focus on pressure-sensitive adhesives supports growth in e-commerce and packaging sectors. Emphasis on low-odor, high-clarity resins aligns with hygiene and healthcare standards.

DRT expands terpene and rosin derivatives portfolio with fragrance integration and low-odor ester innovation

DRT (Dérivés Résiniques et Terpéniques) is strengthening its position in the rosin market through integration with dsm-firmenich and expansion of terpene-based intermediates. Production of alpha and beta-pinene supports both fragrance and industrial rosin applications. Balanced portfolio across gum rosin and tall oil rosin enables flexibility amid regional supply fluctuations. Viester® rosin esters are engineered for low-color and low-odor performance in clean beauty and hygiene markets. Capacity expansion in France and the U.S. supports rising demand for bio-based specialty chemicals. Focus on high-purity derivatives aligns with premium consumer and industrial applications.

United States: Crude Tall Oil Integration Driving High-Value Rosin Derivatives

The United States rosin industry is increasingly anchored in crude tall oil valorization and long-term feedstock security, positioning the country as a leader in bio-based rosin derivatives rather than commodity gum rosin. In 2025, Mainstream Pine Products advanced construction of its $90 million crude tall oil biorefinery in Berkeley County, South Carolina. The facility is engineered to process 110,000 tons per year of pulp-mill byproducts into tall oil rosin and fatty acids, materially expanding domestic availability of high-purity rosin inputs for adhesives, inks, and elastomer modifiers. Supply chain stability has been reinforced through the August 2025 strategic continuity agreement between Kraton Corporation and International Paper, ensuring long-term access to pine pulping co-products amid fluctuating pulp mill operating rates.

Downstream demand is being reshaped by electrification and infrastructure policy. Kraton’s SYLVATRAX™ rosin ester additives are seeing record adoption in 2025–2026 for electric vehicle tires, where rosin-based tackifiers are critical to managing higher torque and vehicle mass. At the same time, Ingevity Corporation announced the September 2025 divestiture of its North Charleston crude tall oil refinery, signaling an industry-wide pivot away from lower-margin industrial grades toward performance-driven rosin chemistry. Innovation is extending into infrastructure materials, with the April 2025 launch of CirKular+™ paving systems that use rosin-based binders to enable full reuse of reclaimed asphalt. Sustainability commitments further differentiate the U.S. market, as leading producers set 2032 targets to cut solvent consumption in rosin esterification processes by 70%.

China: High-Purity and Medical-Grade Rosin Reshaping Product Mix

China’s rosin industry is undergoing a structural upgrade, shifting from volume-led gum rosin production toward high-purity and specialty derivatives for electronics, medical, and advanced coatings applications. At the ASE CHINA 2025 exhibition, Guangdong Komo Group introduced a water-white hydrogenated rosin series designed for electronic chemicals and UV-curable resins, emphasizing thermal stability, low odor, and consistent color values. Parallel innovation is evident in the medical segment, where Chinese producers launched bio-compatible rosin resins in late 2025 with 97% bio-based content, engineered to eliminate cytotoxicity and allergenicity in medical adhesives and depilatory waxes.

Policy and automation trends are also shaping supply. Throughout 2025, the Ministry of Commerce of China expanded export controls on selected dual-use chemicals and processing equipment, tightening availability of catalyst-grade rosin derivatives for global high-tech manufacturing. On the upstream side, gum rosin producers in Yunnan and Guangxi provinces accelerated adoption of automated resin tapping systems during 2024–2025, improving tree yield by an estimated 15% while reducing labor intensity. Together, these developments signal China’s transition from a bulk exporter to a strategically controlled supplier of specialty and high-purity rosin materials.

Brazil: Forestry Certification and Supply Resilience Reinforcing Export Leadership

Brazil remains one of the world’s most important gum rosin producers, with competitiveness increasingly tied to forestry management and supply resilience rather than pure output scale. After wildfires in 2024 reduced gum rosin yields by nearly 12%, Brazilian producers invested heavily in satellite-monitored fire prevention and early-warning systems to secure the 2025–2026 harvest seasons. These measures have stabilized supply expectations and reinforced Brazil’s reputation as a reliable long-term exporter.

Pricing and sustainability dynamics have further strengthened Brazil’s position. In September 2024, gum rosin export offers were revised upward as market conditions normalized, with Brazil maintaining annual output of approximately 130,000 metric tons. In 2025, the country recorded a 20% increase in FSC-certified pine plantations, specifically aligned with the sourcing requirements of European tire manufacturers that mandate traceability and certified bio-based inputs. This certification-driven strategy is positioning Brazilian rosin as a preferred feedstock for premium elastomers and adhesive systems in regulated export markets.

France: Low-Solvent Processing and Premium Resin Orientation

France plays a strategic role in the European rosin value chain, particularly in low-solvent processing and premium end-use applications. The expansion of Kraton Corporation’s Niort facility, completed in recent cycles, achieved a 70% reduction in solvent consumption, setting a new benchmark for environmental performance in pine chemical processing across Europe. This has strengthened France’s position as a reference point for low-footprint rosin ester manufacturing.

Product focus in France is also shifting decisively toward premium markets. By early 2026, French chemical hubs have increasingly prioritized alpha methyl styrene resins and hydrogenated rosin grades for high-end cosmetics, fragrances, and specialty adhesives. This transition reflects broader European demand for odor-neutral, color-stable, and fully hydrogenated rosin derivatives that comply with stringent regulatory and consumer safety expectations.

Rosin Industry: Country-Level Strategic Summary

Rosin Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Key Implication for Rosin Industry

|

|

United States

|

CTO biorefineries and EV tire additives

|

Shift toward high-value tall oil rosin and performance esters

|

|

China

|

High-purity and medical-grade rosin

|

Transition from volume exports to specialty-controlled supply

|

|

Brazil

|

Forestry certification and supply resilience

|

Strengthened export reliability for regulated markets

|

|

France

|

Low-solvent processing and premium applications

|

Leadership in sustainable, high-end rosin derivatives

|

Rosin Market Report Scope

Rosin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.2 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Source Type (Gum Rosin, Tall Oil Rosin, Wood Rosin), By Derivative Product (Rosin Esters, Hydrogenated Rosin, Modified Rosins, Rosin Soaps & Salts), By Application (Adhesives & Sealants, Printing Inks, Rubber & Tires, Paints & Coatings, Paper Sizing, Electronics, Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kraton Corporation, Ingevity Corporation, Eastman Chemical Company, Lawter Inc., Guangdong Komo Group Co. Ltd., Forchem Oyj, Respol, Wuzhou Sun Shine Forestry & Chemicals, Arakawa Chemical Industries Ltd., Foreverest Resources Ltd., Pine Chemical Group, DRT, Guangxi Foreverest Pine Chemicals, G C Rutile, SOCER

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rosin Market Segmentation

By Source Type

- Gum Rosin

- Tall Oil Rosin

- Wood Rosin

By Derivative Product

- Rosin Esters

- Hydrogenated Rosin

- Modified Rosins

- Rosin Soaps & Salts

By Application

- Adhesives & Sealants

- Printing Inks

- Rubber & Tires

- Paints & Coatings

- Paper Sizing

- Electronics

- Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Rosin Industry

- Kraton Corporation

- Ingevity Corporation

- Eastman Chemical Company

- Lawter Inc.

- Guangdong Komo Group Co. Ltd.

- Forchem Oyj

- Respol

- Wuzhou Sun Shine Forestry & Chemicals

- Arakawa Chemical Industries Ltd.

- Foreverest Resources Ltd.

- Pine Chemical Group

- DRT

- Guangxi Foreverest Pine Chemicals

- G C Rutile

- SOCER

*- List not Exhaustive