Market Overview: Low-Carbon Cement, High-R-Value Materials, and Circular Construction Accelerate the Advanced Building Materials Market

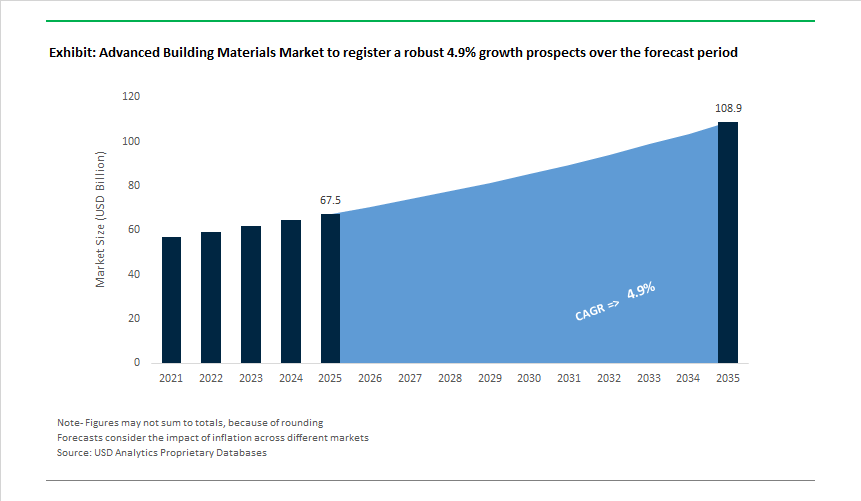

The Global Advanced Building Materials Market is valued at USD 67.5 billion in 2025 and is projected to reach USD 108.9 billion by 2035, growing at a 4.9% CAGR as construction shifts from cost-driven material selection to performance-, carbon-, and lifecycle-led decision-making. Today, advanced building materials are no longer niche innovations; they are becoming core inputs in how buildings are designed, approved, financed, and operated.

At the center of market momentum is decarbonisation pressure. Buildings account for a significant share of global CO₂ emissions, and regulators, investors, and asset owners are increasingly targeting embodied carbon alongside operational energy use. This has accelerated adoption of low-carbon cement alternatives (including blended cements, SCM-rich formulations, and novel binders), recycled aggregates, and engineered composites that materially reduce CO₂ intensity per square meter. For developers, these materials are increasingly required to unlock planning approvals, green financing, and tenant demand.

Energy efficiency represents the second structural growth engine. As energy costs remain volatile and building codes tighten, demand is shifting toward high-R-value insulation systems, advanced glazing, and thermally efficient façade materials that reduce lifetime operating costs. Advanced insulation materials-ranging from next-generation foams to thin-profile, high-performance systems-allow designers to meet energy targets without sacrificing usable floor space, a critical advantage in dense urban markets. As a result, insulation and envelope materials are moving from specification afterthoughts to early-stage design priorities.

The market is also being reshaped by circular construction principles. Developers and contractors are increasingly required to demonstrate recycled content, material recoverability, and waste reduction. This is driving demand for recycled-content composites, modular construction elements, and materials compatible with disassembly and reuse. In parallel, digital design tools and prefabrication are enabling tighter material optimization, reducing overdesign and construction waste-further reinforcing the value proposition of advanced materials that integrate well into industrialized construction workflows.

Technology-enabled construction methods add another layer of momentum. 3D-printed construction materials, advanced admixtures, and engineered mortars are enabling faster build times, lower labor dependency, and greater design flexibility. While still a smaller share of total market value, these technologies are attracting attention from governments and large developers seeking productivity gains in a sector historically constrained by low efficiency and labor shortages.

From a strategic perspective, the advanced building materials market is transitioning from product-led competition to system-level competition. Value is increasingly captured by manufacturers that can demonstrate measurable carbon and energy performance, integrate materials into complete building systems (structure, envelope, insulation), and align with regulatory frameworks, green certification schemes, and digital construction platforms.

Market Analysis: Circularity Investments, CCU Pilots, and Low-Carbon Policies Accelerate Global Adoption

In December 2025, Ambuja Cements (Adani Group) advanced its decarbonization trajectory by being selected for the first Indo-Swedish CCU Pilot, targeting the conversion of captured CO₂ into green fuels and materials-a milestone demonstrating the application readiness of CCU-driven cement manufacturing. The circular economy narrative strengthened further in April 2025, when Etex Group launched the industry’s first standard plasterboard made with 100% recycled gypsum, reinforcing Europe’s leadership in circular building material innovation. A month earlier, in March 2025, Etex opened a €200 million plasterboard facility in Bristol, marking its largest investment and cementing long-term confidence in lightweight construction materials for modular and off-site building markets.

The M&A landscape accelerated as well. In February 2025, Holcim’s acquisitions in the recycling sector underscored its strategy to dominate circular construction and reduce virgin-material dependencies. The same month, Home Depot’s acquisition of SRS Distribution strengthened its direct access to professional roofers and landscapers-key channels for high-performance roofing and exterior materials. In January 2025, the U.S. DOE launched a major initiative to fund bio-based building materials, reflecting federal procurement commitments toward carbon-sequestering materials.

Earlier developments between late 2024 and early 2025 further illustrate the market’s innovation cycle. In December 2024, a U.S.-based manufacturer introduced Structural Insulated Panels (SIPs) with 25% higher recycled content, supporting off-site construction demand. In October 2024, a German startup attracted significant investment to commercialize self-healing concrete, capable of autonomously repairing cracks to reduce maintenance cost and extend infrastructure life cycles. Together, these moves demonstrate the sector’s transition from experimental materials to large-scale, commercially viable advanced building systems.

Advanced Building Materials Market Trends and Opportunities

Trend 1: Corporate Decarbonization and Industrial-Scale Low-Carbon Cement Transitions

The advanced building materials market is being reshaped by an unprecedented wave of corporate decarbonization commitments, with cement and concrete producers executing capital-intensive transitions away from conventional Ordinary Portland Cement toward low-carbon binder systems. By 2025, leading multinationals had moved beyond pilot projects into full portfolio restructuring, embedding low-clinker and circular formulations as default offerings rather than premium alternatives. This shift is not incremental—it reflects a structural reallocation of capital toward materials that can deliver immediate embodied-carbon reductions while remaining compatible with existing construction standards. Large-scale deployment of clinker substitutes, including recycled concrete fines and industrial by-products, is now supported by measurable operational data. In 2024 alone, more than 10 million tons of construction and demolition materials were reintegrated into new binders, a year-on-year increase of roughly 20%, demonstrating that circular feedstocks are reaching industrial reliability. In parallel, carbon capture utilization and storage (CCUS) is moving from demonstration to commercial integration, with multiple EU-funded projects targeting cement with carbon footprints at least 30% below industry benchmarks. Together, clinker reduction and CCUS are transforming cement plants into hybrid material-and-carbon management assets, positioning advanced building materials as a core lever for corporate Scope 1 and Scope 3 emissions reduction strategies ahead of 2030 compliance milestones.

Trend 2: Policy-Led Acceleration of High-Performance Insulation and Retrofit Materials

Energy efficiency policy is translating directly into demand for advanced insulation, air-sealing, and envelope materials, particularly in mature housing stock. In the U.S., targeted provisions within the Inflation Reduction Act have created a predictable, incentive-backed pull for thermal performance upgrades, shifting insulation from a discretionary retrofit to a financially rational investment. Through 2025, homeowners can access tax credits covering up to 30% of qualifying insulation and sealing costs, generating sustained volume demand for spray foams, mineral wool, and advanced composite barriers. The effect is amplified in multifamily housing, where nearly $1 billion in federally backed funding has been earmarked for deep energy retrofits, explicitly prioritizing high-performance envelopes and climate-resilient materials. These programs are not only driving volume but also tightening performance expectations, favoring materials that combine thermal resistance, moisture control, and fire safety in a single system. At the community scale, the Greenhouse Gas Reduction Fund is mobilizing patient capital for building electrification and efficiency projects, reinforcing demand for advanced materials in underserved areas. Despite administrative resets in early 2025, the underlying policy architecture remains intact, anchoring a multi-year upgrade cycle for insulation and retrofit materials that deliver verifiable energy savings rather than nominal compliance.

Opportunity 1: Electrification-Ready Building Material Systems

As buildings transition away from gas toward all-electric operation, a new opportunity is emerging for “electrification-ready” material systems designed to manage higher electrical loads, tighter thermal tolerances, and more complex interfaces. Retrofitting legacy buildings for induction cooking and heat pumps often triggers costly electrical panel upgrades, creating a bottleneck for electrification programs. In response, manufacturers are developing integrated material solutions—fire-rated wall assemblies, advanced insulating backer boards, and smart conduits—that allow high-load appliances to be installed with minimal electrical rework. Public housing electrification initiatives announced in late 2025 are accelerating this trend, effectively acting as live testbeds for scalable retrofit kits. At the same time, packaged window heat pumps and modular HVAC systems are creating demand for specialized window-interface materials that combine airtightness, vibration control, and long-term durability. Beyond appliances, rising peak electricity demand from AI workloads and climate-driven cooling loads is opening space for phase-change materials and thermally conductive building components that act as passive load buffers. These materials help stabilize indoor temperatures and reduce stress on local grids, making them strategically valuable as electrification scales faster than grid reinforcement.

Opportunity 2: AI-Accelerated Discovery, Testing, and Code Qualification of Materials

One of the most transformative opportunities in advanced building materials lies in the application of artificial intelligence to compress the traditionally slow cycle of material discovery, validation, and regulatory approval. Historically, qualifying a new structural or envelope material for commercial use could take years due to iterative testing and conservative code pathways. By 2025, AI-driven pattern recognition and simulation tools are materially reducing this timeline. Academic and applied research has demonstrated that machine learning models can identify optimal ultra-high-performance concrete formulations using industrial waste streams in a fraction of the time required by trial-and-error methods, accelerating both sustainability and commercialization. More broadly, multi-agent AI systems are being deployed to screen candidate polymers, composites, and alloys against mechanical, fire, and durability constraints before physical prototyping begins, lowering R&D costs and failure rates. Investor sentiment reflects this shift: more than half of institutional investors surveyed in 2025 indicated plans to increase exposure to AI-enabled construction technologies. As regulatory bodies grow more comfortable with data-rich, simulation-backed submissions, AI-led design optioneering is becoming integral to how advanced materials move from lab-scale innovation to code-approved, deployable products in global construction markets.

Market Share Analysis: Advanced Building Materials Market

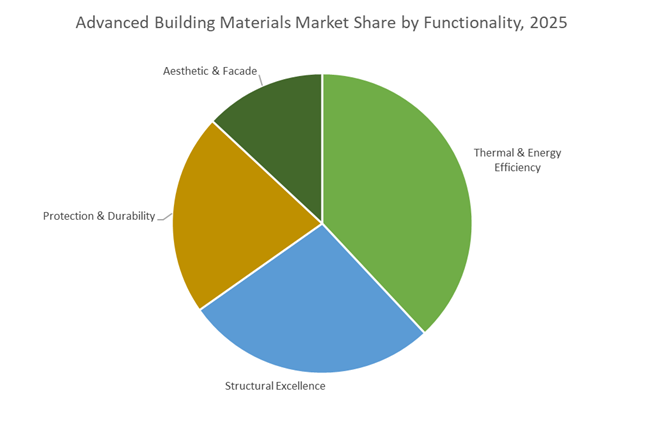

Market Share by Functional Segment: Thermal & Energy Efficiency as the Regulatory Core of Construction Spend

The Thermal & Energy Efficiency segment, accounting for approximately 35% of total market value in 2025, has emerged as the structural profit engine of the advanced building materials market as regulatory compliance overtakes aesthetics and cost minimization as the primary procurement driver. This shift is visible in the financial performance of market leaders such as Saint-Gobain, which reported operating margins exceeding 11% in 2025, largely anchored in its energy-efficient insulation, glazing, and envelope solutions. Unlike cyclical decorative materials, thermal-performance products are now embedded in building codes, with over 50% of global construction regulations mandating efficiency upgrades—creating a non-discretionary demand base. High-performance solutions from players like Kingspan and Owens Corning are gaining share because they deliver equivalent or superior R-values with up to 75% less material thickness, directly improving usable floor space in dense urban developments. Importantly, energy efficiency is no longer confined to insulation layers alone: Holcim’s low-carbon ECOPact and ECOPlanet concretes already represent over 30% of sales, demonstrating that thermal and energy performance is reshaping even core structural materials. This convergence of regulation, margin resilience, and space-efficiency economics explains why thermal and energy-efficient materials now define the functional center of gravity for advanced construction.

Market Share by Application: Residential Construction as the Volume Anchor for Energy-Efficient Materials

Residential construction, holding roughly 40% of total market demand, dominates advanced building materials consumption because energy efficiency directly translates into household-level economic and resilience benefits, making adoption less sensitive to short-term housing cycles. In 2025, manufacturers including Owens Corning and Saint-Gobain reported that nearly 60% of their energy-efficient material demand originated from residential projects, driven by retrofits rather than new builds. Even in cooling housing markets, advanced residential product lines delivered ~25% year-over-year revenue growth, indicating that material intensity per home is rising as homeowners prioritize lifetime energy savings over upfront costs. Technologies such as high-performance foams and airtight insulation systems from BASF now meet the emerging “zero-leak” thermal envelope standard, eliminating thermal bridges and enabling compliance with Net-Zero Home and Passive House certifications. Sustainability credentials further reinforce residential dominance: Kingspan’s milestone of recycling 1.1 billion PET bottles into insulation underscores how circular-economy metrics increasingly influence homeowner and developer purchasing decisions. As utility costs, climate resilience, and green financing converge at the household level, residential construction remains the most reliable and scalable demand base for advanced building materials in 2025.

Competitive Landscape: Decarbonization Leaders, Insulation Innovators and Circular Construction Champions

The competitive landscape spans global cement leaders pursuing carbon-neutrality, insulation technology specialists, and lightweight-construction companies scaling modularization. Differentiation is increasingly shaped by CCUS projects, high-performance insulation technologies, circular manufacturing capabilities, and integrated building-envelope solutions.

Holcim Group - Global Leader in Sustainable Cement and Circular Construction

Holcim’s portfolio includes ECOPact CO₂-reduced concrete and ECOPlanet green cement, reflecting its industry-leading position in decarbonized cement solutions. Its strategic focus on circularity has driven acquisitions in C&D waste recycling and partnerships accelerating CCUS deployment across Europe and North America. Holcim’s 2024-2025 agreements support capture and utilization of millions of tonnes of CO₂ annually, strengthening its global sustainability leadership. With unmatched production scale, Holcim supplies major infrastructure and commercial megaprojects requiring consistent delivery of advanced building materials.

Saint-Gobain - Specialist in High-Performance Insulation and Intelligent Building Envelopes

Saint-Gobain delivers mineral wool, PIR insulation, aerogel systems, and dynamic glazing for high-specification building envelopes. Its R&D strategy prioritizes thermal, acoustic, and occupant-health performance, with new materials engineered to exceed evolving regulatory standards. Recent innovations include materials that actively absorb VOCs, improving indoor air quality-an emerging differentiator in green buildings. Through integrated envelope solutions, Saint-Gobain enables optimized energy efficiency and system-level performance for energy-efficient buildings.

Kingspan Group - Market Leader in Insulated Panels and Advanced Thermal Efficiency Systems

Kingspan specializes in advanced insulated panels and rigid foam systems such as QuadCore, offering high R-values with reduced thickness. Its core strength is meeting the extreme performance needs of data centers and cold-storage facilities, where thermal reliability and fire resistance are critical. The company’s strategic roadmap includes achieving Net-Zero Carbon manufacturing and expanding renewable energy use across its facilities. Kingspan’s portfolio aligns with global demand for high-specification construction and ultra-efficient envelopes.

Etex Group - Lightweight Construction Pioneer With Major Investments in Circular Gypsum

Etex’s portfolio spans plasterboard, fiber cement and modular systems, enabling rapid, lightweight construction. Its €200M UK facility expansion (March 2025) significantly increases EU supply capacity. Etex also introduced standard plasterboard made from 100% recycled gypsum, increasing circular material availability for the broader construction sector. With strong positioning in modular and off-site construction, Etex supports the shift toward faster, lower-waste building methodologies.

CRH Plc - Integrated Building Materials Provider With A Focus On Durable Infrastructure

CRH supplies essential materials including aggregates, asphalt, cement, and specialty building products, serving large public and private infrastructure projects. The company continues to invest in digital construction technologies that optimize logistics and reduce waste across the supply chain. CRH is also developing sustainable cementitious binders and optimized mix designs to reduce carbon footprints in concrete products. Its strong infrastructure focus aligns with government-funded transportation, resilience, and urban-development programs.

The United States advanced building materials market in 2025 is being structurally reshaped by federal decarbonization funding and industrialized construction mandates under the Advanced Building Construction (ABC) Initiative and the Inflation Reduction Act (IRA). In January 2025, the U.S. Department of Energy (DOE) awarded USD 31.8 million across seven pilot projects focused on scalable, factory-based construction systems. A flagship example is Oak Ridge National Laboratory’s pressure-triggered sealant technology, designed for modular envelopes requiring airtightness, thermal resilience, and rapid onsite assembly—key requirements for semiconductor fabs and AI data centers.

Private-sector alignment is reinforcing this policy push. Epsilon Advanced Materials’ 2025 partnership with Phillips 66 highlights how advanced composites and low-toxicity coatings are now embedded into large-scale industrial facilities to meet ESG and safety compliance. Meanwhile, AECOM’s 10-year environmental BPA with NASA underscores how federal infrastructure is becoming a proving ground for advanced, low-emission structural and finishing materials.

China – Dual Carbon Mandates and High-Tech Industrial Parks

China’s advanced building materials market is expanding at scale, anchored in the “Dual Carbon” policy framework and the construction of 8-inch wafer fabs, AI clusters, and green urban districts. Government budgets for 2024–2025 included approximately USD 4 trillion in public infrastructure spending, with “New Infrastructure” projects prioritizing self-healing concrete, smart glass, and digitally monitored building envelopes in Tier-1 cities.

A pivotal regulatory shift occurred with the earmarking of USD 14 billion for green construction, mandating the adoption of LC³ cement, which cuts embodied carbon by up to 40% versus Ordinary Portland Cement. At the same time, China’s November 2025 export controls on graphite and battery materials have indirectly accelerated domestic innovation in graphene-enhanced concrete for high-load industrial flooring. As a result, China’s strategy blends mass deployment with materials substitution, ensuring domestic resilience while scaling advanced construction technologies nationwide.

United Kingdom – Mass Timber Codes and Carbon-Capturing Envelopes

The United Kingdom is positioning advanced building materials at the intersection of housing delivery, decarbonization, and modular construction. Government statistics released in February 2025 showed a 4.2% increase in block deliveries and a £2.1 billion export value for high-value construction materials, signaling strong momentum in engineered systems rather than traditional masonry alone.

A defining shift is the widespread adoption of hybrid structural frames combining CLT (Cross-Laminated Timber) and cold-formed steel, enabled by updated building codes. This approach balances long-span requirements with carbon reduction goals, supporting the 2.1% construction output growth forecast for 2025. Parallel innovation is visible in façade-integrated carbon capture, led by Nuada, whose MOF-based systems are now being embedded directly into industrial building envelopes—transforming structures into active decarbonization assets.

India – Semicon India and Green Building Scale-Up

India’s advanced building materials market is being propelled by the ₹1.6 lakh crore Semicon India investment wave, which is driving demand for high-durability, vibration-resistant, and thermally stable construction systems. A cornerstone initiative is the partnership between CREDAI and the Indian Green Building Council (IGBC), targeting 1,000 certified green projects by late 2025. This has sharply increased adoption of precast concrete, ready-mix concrete (RMC), and modular assemblies that compress project timelines.

On the supply side, Saint-Gobain completed a USD 320 million investment cycle in India, expanding capacity for advanced concrete formulations and 3D-printable building materials. Complementing this, new infrastructure announcements exceeding USD 740 million in April 2025 explicitly prioritized materials with enhanced seismic resistance and lifecycle durability, reflecting India’s shift toward performance-driven construction.

Germany – SuperLink Grids and Bio-Based Material Leadership

Germany remains Europe’s technical anchor for high-efficiency insulation and bio-based construction materials, tightly aligned with grid modernization and climate targets. The acquisition of the CALOSTAT insulation brand and Ondura roofing assets by Kingspan Group in 2024–2025 consolidated Germany’s position in ultra-thin, high-performance insulation systems.

A major deployment channel is the Federal Ministry for Economic Affairs and Climate Action (BMWK)’s SuperLink projects, which integrate aerogels and vacuum-insulated panels (VIPs) into underground high-voltage transmission corridors to minimize thermal losses. Concurrently, German chemical leaders are scaling bio-based coatings and finishes, with public-sector procurement increasingly favoring low-VOC, renewable-sourced materials by the end of 2025—embedding sustainability directly into national construction standards.

United Arab Emirates – Smart Cities, NABERS, and 3D-Printed Structures

The UAE advanced building materials market is defined by policy-driven adoption of smart, energy-responsive materials in one of the world’s most ambitious construction environments. The expansion of the NABERS framework into the Middle East has made dynamic glazing, smart façades, and Phase-Change Materials (PCMs) mandatory in new commercial towers across Dubai and Abu Dhabi.

Equally transformative is the UAE’s 2025 construction mandate requiring 25% of new buildings to utilize 3D printing technologies. This policy has created a surge in demand for specialized concrete–polymer hybrids optimized for robotic extrusion and rapid curing. Collectively, these initiatives position the UAE not just as a consumer but as a global reference market for next-generation smart building materials.

2025 Strategic Comparison: Advanced Building Materials National Matrix

Advanced Building Materials National Matrix

|

Country

|

Primary Strategic Driver

|

2025 Key Milestone

|

Primary Material Focus

|

|

United States

|

Federal R&D / ABC Initiative

|

USD 31.8M DOE ABC awards

|

Modular sealants, high-load composites

|

|

China

|

Dual Carbon / 8-Inch Fabs

|

USD 14B green construction allocation

|

LC³ cement, self-healing concrete

|

|

United Kingdom

|

Decarbonization / Housing

|

Hybrid mass-timber code adoption

|

CLT, GLT, MOF-based envelopes

|

|

India

|

Semiconductor Ecosystem

|

₹1.6 lakh crore Semicon India push

|

Precast concrete, 3D-printing mixes

|

|

Germany

|

Energy Efficiency / Insulation

|

CALOSTAT & aerogel integration

|

Aerogels, bio-based coatings

|

|

UAE

|

Smart Cities / Automation

|

25% 3D-printing mandate

|

Dynamic glazing, concrete hybrids

|

Advanced Building Materials Market Report Scope

Advanced Building Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$67.5 Billion

|

|

Market Size (2035)

|

$108.9 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material Type (Advanced Cement & Concrete, Advanced Wood & Timber, High-Performance Metals & Alloys, Advanced Glass & Glazing, Specialty Composites, Smart & Functional Materials), By Functionality (Structural Excellence, Thermal & Energy Efficiency, Acoustic Management, Aesthetic & Facade, Protection & Durability), By Application (Residential Construction, Commercial & Institutional, Industrial Infrastructure, Public Infrastructure), By Sales Channel (Direct B2B/OEM, Contractor & Professional Networks, Specialty Building Material Stores)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain S.A., BASF SE, Holcim Ltd., Cemex S.A.B. de C.V., Kingspan Group plc, Dow Inc., Sika AG, Heidelberg Materials AG, PPG Industries Inc., Larsen & Toubro Construction, Sherwin-Williams Company, Knauf Gips KG, Owens Corning, Arconic Corporation, Tata Steel Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Building Materials Market Segmentation

By Material Type

- Advanced Cement & Concrete

- Advanced Wood & Timber

- High-Performance Metals & Alloys

- Advanced Glass & Glazing

- Specialty Composites

- Smart & Functional Materials

By Functionality

- Structural Excellence

- Thermal & Energy Efficiency

- Acoustic Management

- Aesthetic & Facade

- Protection & Durability

By Application

- Residential Construction

- Commercial & Institutional

- Industrial Infrastructure

- Public Infrastructure

By Sales Channel

- Direct Sales (B2B/OEM)

- Contractor & Professional Networks

- Specialty Building Material Stores

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Advanced Building Materials Market

- Saint-Gobain S.A.

- BASF SE

- Holcim Ltd

- Cemex S.A.B. de C.V.

- Kingspan Group plc

- Dow Inc.

- Sika AG

- Heidelberg Materials AG

- PPG Industries, Inc.

- Larsen & Toubro (L&T) Construction

- Sherwin-Williams Company

- Knauf Gips KG

- Owens Corning

- Arconic Corporation

- Tata Steel Ltd.

*- List not Exhaustive