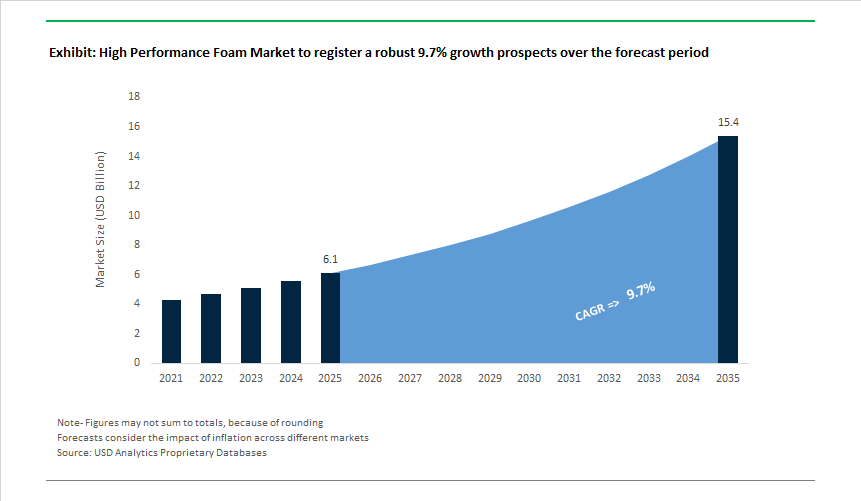

Market Overview: Silicone Foams, Structural PU and Aerogel Insulation Power the USD 6.1B Market At 9.7% CAGR To 2035

The High-Performance Foam (HPF) Market is scaling into a USD 6.1 billion industry in 2025 and is projected to reach USD 15.4 billion by 2035, expanding at a 9.7% CAGR as foam materials transition from passive fillers to engineered, multi-functional system components. Across aerospace, automotive, electronics, and industrial insulation, OEMs are increasingly specifying foams for their ability to simultaneously deliver thermal stability, flame-smoke-toxicity (FST) compliance, weight reduction, chemical resistance, and space efficiency. This convergence of requirements is reshaping material selection logic and elevating high-performance foams into procurement-critical categories.

Material-level demand is being shaped by application-specific risk and performance thresholds. Silicone foams are recording the fastest adoption rates due to their ability to maintain mechanical integrity and elastic recovery at elevated temperatures, alongside inherent chemical inertness and low outgassing. These attributes make them indispensable in electronics thermal management, aerospace interiors, and under-hood automotive environments where conventional organic foams degrade or emit unacceptable smoke and toxicity. In parallel, structural polyurethane and specialty engineered foams are increasingly designed into vehicle architectures, delivering weight reductions of up to ~20 kg per vehicle in certain EV platforms-directly translating into improved driving range, energy efficiency, and modular component integration.

Safety, regulatory compliance, and asset protection are becoming decisive demand drivers. In aerospace, rail, offshore energy, and industrial facilities, HPF grades meeting stringent FST and OSU 65/65 requirements are no longer optional, particularly for interior panels, insulation layers, and equipment housings. At the same time, low leachable chloride content and moisture resistance are elevating the role of high-performance foams in corrosion under insulation (CUI) mitigation, especially in oil & gas and chemical processing environments. These specifications are increasingly embedded directly into procurement documents, favoring suppliers with validated test data and certification-ready product portfolios.

Looking ahead, differentiation within the HPF market will be driven by space efficiency and regulatory alignment. Vacuum-insulated and aerogel-based foam cores are displacing thicker conventional insulation materials in space-constrained aerospace, battery, and industrial retrofit applications, while HFO-blown spray foams are gaining traction as regulators and customers push to reduce global warming potential without compromising thermal performance.

Market Analysis: Product Launches, Capacity Expansions and Sustainability Breakthroughs Driving HPF Adoption

The HPF sector registered a sustained wave of product innovation and strategic investment as manufacturers target electrification, aerospace safety and low-carbon materials. In March 2024, Boeing announced a major investment in an aerospace development centre, signalling industry commitment to advanced materials including specialized foams for lightweight structures and interior systems. Building on vehicle and battery protection needs, May 2024 saw Huntsman launch SHOKLESS, a polyurethane foam family engineered to protect EV battery packs from impact and thermal shock-directly addressing OEM safety and module packaging requirements. The same period produced new spray-foam insulation systems (Icynene series) optimized for energy efficiency in commercial and residential construction.

Strategic collaborations and low-carbon feedstock work accelerated in September 2024, when BASF partnered with Future Foam on biomass-balance certified flexible foams, demonstrating early commercial steps toward renewable feedstocks in flexible foam manufacturing. Aerospace-focused foam technology also expanded in September 2024 with L&L Products’ InsituCore launch for lightweight composite manufacturing. Through 2025 the growth story broadened: April 2025 Huntsman introduced high-performance spray polyurethane insulation variants, and October 2025 Armacell inaugurated a new Pune facility to produce ArmaGel® XG aerogel insulation for high-temperature service, strengthening regional supply to APAC energy and industrial markets. Financial and commercial signals reinforced demand-October 2025 Rogers Corporation reported sequential EMS segment growth driven by portable electronics and A&D demand, and September 2025 Fullstride/Vale/Borealis introduced a CO₂-derived feedstock foam (carboncup™), marking a step toward captured-carbon polymer feedstocks.

High-Performance Foam (HPF) Market Trends and Opportunities

Trend 1: Ultra-Low-Flammability Foams as a Structural Layer in EV Battery Safety

Global EV fire-safety regulation is no longer focused solely on detection and suppression; it is now reshaping battery pack architecture itself. The publication of ANSI/CAN/UL 9540A:2025 in March 2025 materially raised the bar by introducing mandatory hydrogen measurement at the unit level and emphasizing the prevention of deflagration and re-ignition. As a result, high-performance silicone, polyimide, and hybrid ceramic foams are being specified as functional thermal barriers rather than passive fillers. These foams are engineered to withstand extreme off-gassing temperatures and pressures while maintaining dimensional stability under compression, a requirement highlighted in 2025 technical guidance from UL Research Institutes. From a system perspective, advanced foams are now deployed as compression pads that simultaneously manage cell swelling and act as thermal isolators, ensuring adjacent cells remain below the critical 150–200 °C threshold associated with cascading thermal runaway. This role becomes even more pronounced in Asia-Pacific markets, where China’s GB38031-2025 standard (effective January 2025) requires stable battery operation under extreme environmental and fast-charging conditions. Consequently, demand is accelerating for thermally conductive yet electrically insulating foams that dissipate heat during normal operation while forming an ultra-low-flammability barrier during internal short-circuit events, embedding HPF directly into EV safety architectures.

Trend 2: Strategic Shift Toward Bio-Based and Recyclable Polyolefin Foams

Sustainability pressures are pushing high-performance foam producers beyond incremental efficiency gains toward fundamental feedstock transformation. Corporate Scope-3 targets and consumer scrutiny are accelerating the transition from fossil-derived monomers to bio-based and chemically recycled polyolefins, particularly in automotive interiors and protective packaging. By 2025, bio-based polypropylene commercialization is scaling rapidly, supported by producers such as Neste and LyondellBasell, which are converting waste oils and residues into drop-in PP suitable for expanded foam applications. Automotive OEMs are reinforcing this shift through closed-loop partnerships: in late 2024, Jaguar Land Rover, working with Dow and Adient, demonstrated chemically recycled polyurethane seat foams that retain premium rebound and durability characteristics. At the infrastructure level, recycling systems are also maturing. Germany’s EPP Loop program, launched in early 2025, targets recovery of 75% of domestic expanded polypropylene waste by 2030, stabilizing feedstock availability for molders and reducing exposure to the 15–20% raw-material price volatility observed during 2024–2025. Together, these developments are repositioning HPF as a cornerstone material for circular automotive and packaging systems rather than a linear, disposable input.

Opportunity 1: High-Performance Insulation Foams for Cryogenic Liquid Hydrogen Storage

The rapid emergence of liquid hydrogen (LH₂) in aviation and maritime propulsion is creating a structurally new demand pocket for high-performance foams capable of managing extreme cryogenic gradients. At −253 °C, LH₂ storage tanks face unprecedented boil-off challenges, making insulation efficiency a mission-critical design variable rather than a secondary consideration. Research published in mid-2025 demonstrates that optimized closed-cell HPF networks can dramatically reduce heat ingress between the 20 K cold boundary and ambient external temperatures, directly extending fuel retention times for long-duration transport. Aerospace validation is reinforcing confidence in these materials: updated 2025 technical findings from NASA confirm that selected unreinforced polyurethane foams can withstand more than 4,200 thermal cycles—equivalent to roughly 15 years of airline service—without mechanical degradation. From a system-weight perspective, this performance is decisive. As LH₂ tanks rely on thinner composite shells than gaseous systems, insulation mass becomes the dominant contributor to tank weight. Modern HPF solutions delivering 70–85% thermal-protection efficiency enable lighter tanks while preserving payload capacity, positioning advanced foams as a key enabler of hydrogen-powered aircraft and zero-emission shipping.

Opportunity 2: High-Damping Foams for Next-Generation Aerospace Cabin Acoustics

The aerospace industry’s shift toward composite fuselages and ultra-high-bypass engines has altered cabin noise profiles in ways traditional fiberglass insulation cannot effectively address. Composite-rich airframes such as the A350 and B787 exhibit stronger low-frequency vibration transmission due to reduced inherent damping, elevating passenger noise and fatigue levels. In response, high-damping polyurethane and hybrid foams are being engineered to target these low-frequency bands while meeting stringent Fire, Smoke, and Toxicity (FST) requirements. During 2025, Lufthansa Technik and Safran Interiors initiated flight tests of recyclable acoustic foams designed specifically for retrofit and line-fit applications, demonstrating measurable reductions in cabin noise without adding mass penalties. Defense demand is amplifying this opportunity: with NATO defense spending rising by 13% in 2025, procurement of advanced aircraft platforms is driving requirements for “defense-grade” foams that combine acoustic absorption with full FAA and EASA compliance. Sustainability is now layered onto performance—Safran’s early-2025 trials of compostable foam seat cushions integrating acoustic layers illustrate how HPF can deliver a 15% noise reduction while aligning with EU Green Deal objectives for circular aviation.

Market Share Analysis: High-Performance Foam Market

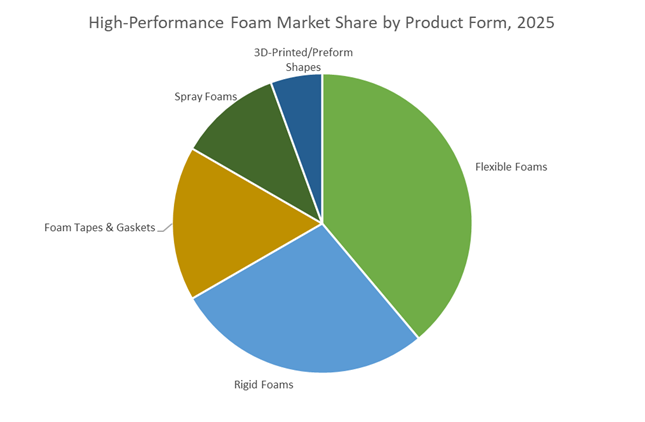

Market Share by Product Form: Flexible High-Resilience and Elastomeric Foams Anchor Lifecycle Performance

Flexible foams—particularly high-resilience (HR) polyurethane and advanced elastomeric foams—account for the largest share of the High-Performance Foam Market because they solve a multi-variable performance equation that rigid foams structurally cannot address. Their dominance is rooted in long-term compression recovery, vibration damping, sealing integrity, and moisture control, all of which directly impact product lifespan. In automotive, electronics, and industrial systems, foams are no longer treated as passive fillers; they are engineered components expected to perform reliably for 10–30 years under cyclic load, temperature variation, and chemical exposure. Flexible microcellular foams that maintain over 90% shape recovery after sustained compression significantly reduce failure rates in gaskets, seating systems, and electronic cushioning, lowering warranty and recall risk for OEMs. At the same time, closed-cell flexible foams with thermal conductivity near 0.034 W/m·K have become indispensable for energy efficiency and condensation control, particularly in electrified systems where thermal stability directly affects battery performance and safety. Procurement decisions in 2025 increasingly prioritize VOC-free, nitrogen-expanded foams, especially in medical devices and EV interiors, where indoor air quality and regulatory compliance are non-negotiable. These combined drivers—fatigue resistance, thermal efficiency, sealing reliability, and regulatory alignment—explain why flexible high-performance foams dominate market share at the material-form level.

Market Share by Application: Automotive and Transportation Drive Volume Through NVH and Thermal Safety Demands

Automotive and transportation represent approximately 30% of total demand, making this segment the largest application market for high-performance foams due to its unique convergence of lightweighting, acoustic management, and thermal safety requirements. As powertrains electrify and combustion noise disappears, previously masked NVH issues—road noise, inverter whine, and aerodynamic vibration—have become critical differentiators in vehicle quality. High-performance acoustic foams engineered to target specific frequency bands now deliver measurable cabin noise reductions, directly influencing consumer perception in premium and mass-market EVs alike. Simultaneously, the push toward aggressive efficiency targets has accelerated substitution of metal and dense rubber components with lightweight foam-based solutions across seating, sealing, and thermal insulation systems. A defining 2025 inflection point is battery safety, where aerogel-reinforced silicone and elastomeric foams act as thermal barriers during cell-to-cell failure events, buying crucial evacuation time and enabling compliance with evolving EV fire regulations. Beyond automotive, rail and aerospace applications reinforce this dominance through long service-life requirements, where UV-stable, flame-retardant foams are specified to last the entire operational life of the platform without degradation. Collectively, electrification-driven NVH sensitivity, thermal runaway mitigation, and lifecycle durability make transportation the most structurally entrenched demand engine for high-performance foams.

Competitive Landscape: Global Specialists Scaling Aerogel, Silicone, PU and Fluoropolymer Foams For Safety, Lightweighting and Low-Carbon Performance

The competitive field consists of diversified materials groups and specialty foam manufacturers that differentiate by material science (silicone, fluoropolymer, aerogel, PU), certifications (FST/OSU), regional manufacturing footprint, and sustainability of feedstocks (HFO, biomass balance, CO₂-derived monomers). Leading players combine R&D in low-GWP blowing agents, in-house compounding/foaming know-how, and targeted facility builds to capture aerospace, EV and industrial insulation contracts.

Armacell International S.A.: Aerogel and Elastomeric Foam Leader Scaling APAC Production For Cryogenic and High-Temperature Insulation

Armacell is a global leader in engineered insulation foams, renowned for ArmaFlex® elastomeric products and the ArmaGel® aerogel line that minimizes thermal loss and mitigates CUI in high-temperature service. The company’s 2025 Pune plant launch expands regional capacity for ArmaGel XG, supporting cryogenic and dual-temperature industrial applications. Armacell’s sustainability moves include ArmaPET® Eco50, a recycled-PET based core material, positioning the firm for circular-economy demands in composite cores and insulated panels.

Rogers Corporation: Elastomeric Materials Specialist Growing EMS Sales Across A&D and Portable Electronics

Rogers’ Elastomeric Material Solutions segment supplies high-performance silicone, urethane and polyolefin foams used in sealing, thermal management and battery firewall applications (ProCell™ EV Firewall). The company reported an 8.7% sequential EMS sales increase (Q3 2025), evidencing strong demand from portable electronics and aerospace & defense customers. Rogers focuses on foams for thermal and acoustic control in advanced mobility and high-reliability electronics.

Sekisui Chemical Co., Ltd.: Ultra-Thin Crosslinked Polyolefin Foams For Electronics, EMC Shielding and Mobility NVH Solutions

Sekisui’s proprietary crosslinked polyolefin foams (SOFTLON, THERMOBREAK) enable ultra-thin constructions (down to 40 μm) for electronic device tapes, thermal management and EMC shielding in 5G and ADAS sensor housings. With flame-retardant series meeting FMVSS and UL standards, Sekisui targets mobility and rail safety markets requiring weight reduction and NVH control.

Zotefoams Plc: Nitrogen-Expanded Closed-Cell Foams and Fluoropolymer FST Solutions For Aerospace Interiors and High-Voltage Batteries

Zotefoams’ unique three-stage nitrogen expansion process produces consistent, low-VOC crosslinked block foams. Its ZOTEK® F fluoropolymer foam range addresses FST and dielectric needs in aerospace interiors and high-voltage battery housings. Zotefoams’ Ecozote initiatives (recycled LDPE content) support sustainability while maintaining the performance demanded by defense and high-impact sports applications.

Huntsman International LLC: PU Systems Specialist With EV Battery Protection and Spray-Foam Insulation Portfolios

Huntsman supplies tailored polyurethane systems for rigid and flexible foam markets and has strategically expanded its insulation and EV protection capabilities via product launches (SHOKLESS, Icynene series) and acquisitions. SHOKLESS targets mechanical and thermal protection for high-voltage battery packs, while prior M&A (Icynene-Lapolla) broadened Huntsman’s SPF footprint for commercial and residential energy-efficiency projects.

The United States high-performance foam market has consolidated its global leadership around aerogel-based thermal barriers and micro-cellular polymer foams, driven by federal reshoring and safety mandates. In October 2024, the U.S. Department of Energy (DOE) issued a USD 670.6 million conditional loan to Aspen Aerogels to expand domestic production of PyroThin® aerogel foams, now treated as a safety-critical component for cell-to-cell thermal runaway prevention in EV battery packs. This capital infusion positions aerogel foams as strategic infrastructure materials rather than niche insulation solutions.

Innovation breadth widened in 2025 as AeroShield Materials, an MIT spin-out, secured additional funding to scale ultra-insulating transparent aerogel foams for high-performance windows—linking foam innovation to Net Zero building envelopes. Simultaneously, CHIPS Act–aligned R&D grants accelerated development of polyimide-based micro-cellular foams with ultra-low dielectric constants, enabling thermal and signal management in AI-accelerator server clusters. Collectively, U.S. policy now integrates EV safety, AI infrastructure, and building decarbonization through advanced foam substrates.

China: Whole-Chain Governance, Export Controls & Industrial-Scale Aerogel Foams

China’s high-performance foam strategy combines capacity scale with regulatory leverage, reinforcing material sovereignty under Made in China 2025. Export controls effective November 8, 2025, issued by the Ministry of Commerce (MOFCOM), tightened global access to lithium battery equipment and select superhard materials—directly affecting high-performance battery insulation foams used in high-voltage EV systems.

Domestically, the Ministry of Industry and Information Technology (MIIT) reported a sharp rise in closed-cell silica aerogel foam production by December 2025, aligned with the goal of 70% domestic content in core materials. Industrial execution is visible in capacity expansions by Guangdong Alison Hi-Tech, which scaled high-temperature aerogel blankets across 2024–2025, securing multi-year contracts for deep-sea pipeline insulation in APAC. China’s approach integrates export leverage with industrial volume, reshaping global foam supply dynamics.

Japan: 6G Electronics, Chemical Recycling & Bio-Attributed Foams

Japan’s high-performance foam market is defined by the intersection of 6G telecommunications, circularity, and low-carbon materials. In December 2025, PS Japan Corporation launched a mass-balanced, bio-attributed polystyrene foam using biomass naphtha—cutting lifecycle emissions while maintaining electronics-grade performance for device housings.

Circularity advanced further in November 2025 when Toyo Styrene began commercial operations at Japan’s first chemical recycling plant for polystyrene foams in Chiba, employing microwave depolymerization to recover reusable monomers. On the technology front, Japanese electronics OEMs are piloting silicone-based high-performance foams with integrated EMI shielding for 6G signal reflectors, where thermal dissipation and signal stability are critical. Japan thus positions foam materials at the core of next-generation connectivity.

Germany: Clean Industrial Deal Accelerates Carbon-Aware and Circular Foams

Despite elevated energy costs, Germany leads Europe’s pivot toward carbon-aware high-performance foams under the Clean Industrial Deal and Zero-Emission Building (ZEB) mandates. In August 2025, BASF introduced a next-generation carbon aerogel foam for hydrogen storage and aerospace, compliant with stringent Fire, Smoke, Toxicity (FST) standards—expanding foam applications into hydrogen aviation.

Regulatory pull intensified after EPBD updates (July 2025), pushing German manufacturers toward Vacuum Insulation Panels (VIPs) and high-R-value phenolic foams to meet net-zero envelope requirements. At K 2025, BASF also showcased Infinergy®, a bio-based expanded TPU (E-TPU) foam, signaling a strategic shift to renewable, high-elasticity foams for automotive interiors and performance footwear—embedding circularity into premium foam markets.

South Korea: HBM4 Packaging, Hydrogen Valleys & Recycled-Content Mandates

South Korea’s high-performance foam market is tightly coupled with its dominance in AI memory packaging and hydrogen energy systems. In 2025, SK hynix and Samsung Electronics integrated high-temperature polyimide foams into HBM4 production lines, enabling materials to withstand 260 °C reflow without warpage—an essential requirement for stacked memory architectures.

Government investment in Ulsan and Changwon Hydrogen Valleys has driven demand for cryogenic-grade foams used in liquid hydrogen storage and fuel-cell plates. Regulatory pressure adds momentum: the Revised Resource Recycling Act (2025) mandates 10% recycled content in engineering plastics and foams, forcing manufacturers to adopt advanced sorting and de-inking technologies—embedding sustainability into Korea’s high-tech foam supply chain.

India: Component PLI and Infrastructure-Led Foam Demand Expansion

India is rapidly emerging as a China+1 manufacturing base for high-performance foams, supported by incentives and infrastructure growth. The ₹25,000 crore (USD 3 billion) Component PLI announced in Budget 2025 is attracting investment into EPP (Expanded Polypropylene) and specialty polyurethane foams for electronics packaging—strengthening domestic protection for smartphones, servers, and telecom equipment.

Demand is amplified by public spending. Late-2025 allocations of ₹260 billion for highways and ₹192 billion for commercial real estate are accelerating adoption of energy-efficient insulation foams in green buildings. In healthcare, rising medical device exports have led Sheela Foam to expand antimicrobial specialty foams for surgical pads and orthopedic supports—diversifying India’s high-performance foam applications beyond construction and electronics.

2025 Strategic Matrix: High-Performance Foam Developments

High-Performance Foam Developments Matrix

|

Country

|

Primary Technical Focus

|

Key 2025 Policy / Event

|

Material Leadership

|

|

United States

|

EV safety & AI servers

|

USD 670.6M DOE loan; CHIPS R&D

|

Aerogel & polyimide foams

|

|

China

|

Resource sovereignty

|

MOFCOM export controls

|

Battery & aerogel foams

|

|

Japan

|

6G & circularity

|

Chemical recycling scale-up

|

Bio-attributed PS & silicone foams

|

|

Germany

|

Hydrogen & ZEBs

|

EPBD updates; Clean Industrial Deal

|

Carbon aerogels & VIPs

|

|

South Korea

|

HBM4 & hydrogen

|

K-Semiconductor Belt Phase II

|

High-temp polyimide foams

|

|

India

|

Electronics reshoring

|

₹25k Cr Component PLI

|

EPP & specialty PU foams

|

High Performance Foam Market Report Scope

High Performance Foam Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.1 Billion

|

|

Market Size (2035)

|

$15.4 Billion

|

|

Market Growth Rate

|

9.7%

|

|

Segments

|

By Material Type (Polyurethane Foam, Polyolefin Foam, Silicone Foam, Fluoropolymer Foam, High-Performance Polymers, Syntactic Foams), By Product Form (Flexible Foams, Rigid Foams, Spray Foams, Foam Tapes & Gaskets, 3D-Printed/Preform Shapes), By Processing Technology (Supercritical Fluid Expansion, Chemical Blowing, Physical Blowing, Injection Molding & Extrusion), By Application (Thermal Insulation, Acoustic Management, EV Battery Safety, Structural Cores, Protection & Packaging), By End-User Industry (Automotive & Transportation, Aerospace & Defense, Building & Construction, Electrical & Electronics, Medical & Healthcare, Sports & Leisure)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Rogers Corporation, Armacell International S.A., Zotefoams plc, Evonik Industries AG, Dow Inc., SABIC, Sekisui Chemical Co. Ltd., Saint-Gobain, Toray Industries Inc., 3M Company, JSP Corporation, Sealed Air Corporation, Kaneka Corporation, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High-Performance Foam Market Segmentation

By Material Type

- Polyurethane (PU) Foam

- Polyolefin (PO) Foam

- Silicone Foam

- Fluoropolymer Foam

- High-Performance Polymers

- Syntactic Foams

By Product Form

- Flexible Foams

- Rigid Foams

- Spray Foams

- Foam Tapes & Gaskets

- 3D-Printed/Preform Shapes

By Processing Technology

- Supercritical Fluid Expansion

- Chemical Blowing

- Physical Blowing

- Injection Molding & Extrusion

By Application

- Thermal Insulation

- Acoustic Management

- EV Battery Safety

- Structural Cores

- Protection & Packaging

By End-User Industry

- Automotive & Transportation

- Aerospace & Defense

- Building & Construction

- Electrical & Electronics

- Medical & Healthcare

- Sports & Leisure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High-Performance Foam Market

- BASF SE

- Rogers Corporation

- Armacell International S.A.

- Zotefoams plc

- Evonik Industries AG

- Dow Inc.

- SABIC

- Sekisui Chemical Co., Ltd.

- Saint-Gobain

- Toray Industries, Inc.

- 3M Company

- JSP Corporation

- Sealed Air Corporation

- Kaneka Corporation

- Huntsman Corporation

*- List not Exhaustive