Market Overview: Ultra-Low-K Insulation and Energy-Storage Surface Area Drive the Carbon Aerogels Market

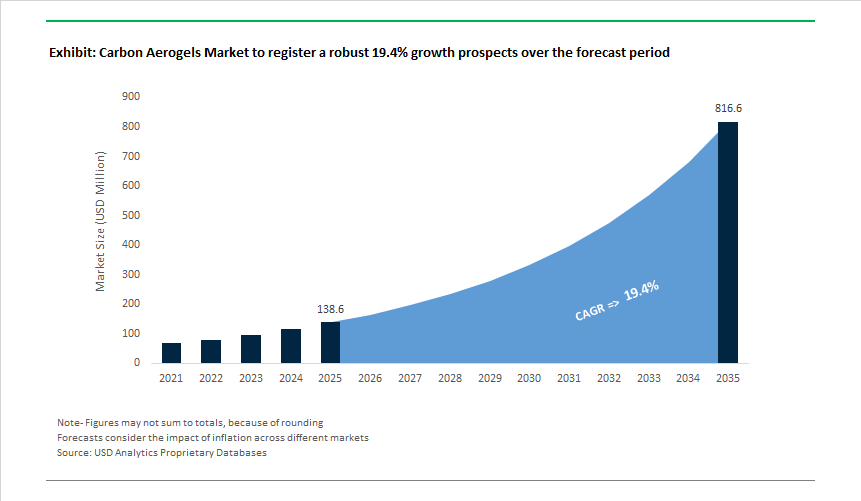

The Global Carbon Aerogels Market is valued at USD 138.6 million in 2025 and is projected to reach USD 816.2 million by 2035, expanding at a 19.4% CAGR as carbon aerogels transition from laboratory-scale materials into commercially relevant solutions for high-performance systems. Market momentum is not driven by volume substitution, but by use cases where conventional materials fail to meet tightening performance, space, and efficiency constraints.

At a strategic level, carbon aerogels are gaining traction because they address three converging pain points across advanced industries: the need to dramatically reduce heat loss in space- and weight-constrained systems, the push for higher power density and faster charge-discharge in energy storage, and growing demand for efficient adsorption materials in environmental and process industries. In these applications, buyers are less price-sensitive and more focused on system-level outcomes-energy efficiency, footprint reduction, safety margins, and lifetime performance-creating room for premium materials to scale.

Aerospace platforms, cryogenic infrastructure, and EV battery systems increasingly operate in environments where traditional insulation materials either occupy too much space or fail to deliver sufficient thermal resistance. Carbon aerogels enable thinner insulation layers with materially higher performance, allowing OEMs to redesign systems around reduced weight, lower boil-off losses, and improved thermal safety. As electrification and cryogenic hydrogen infrastructure expand, insulation performance is becoming a design constraint, not a specification detail-pulling carbon aerogels into earlier stages of system architecture decisions.

The second growth pillar is energy storage, where carbon aerogels are emerging as enabling materials rather than commodity carbons. In supercapacitors and advanced battery architectures, energy density and power delivery are increasingly limited by electrode structure and ion transport rather than chemistry alone. Carbon aerogels offer a pathway to step-change improvements in power handling and cycle life, positioning them as strategic inputs in applications where fast response and durability matter-such as grid stabilization, regenerative braking, and high-power electronics buffering. While still a smaller share of total demand, this segment carries outsized long-term value potential.

Further, opportunistic growth vector lies in adsorption and filtration, including oil spill remediation, gas separation, and catalyst support. These markets provide early commercialization pathways because they value performance-per-unit-mass and rapid deployment, allowing carbon aerogels to compete on effectiveness rather than upfront cost. For suppliers, these applications can serve as bridge markets that support scale-up while higher-value thermal and energy applications mature.

The market’s growth outlook is also improving due to manufacturing economics. Historically, carbon aerogels were constrained by high capital intensity and complex production routes. Recent progress in simplified, scalable manufacturing approaches has materially reduced cost barriers, shifting carbon aerogels from “technically superior but uneconomic” to commercially viable in targeted segments. This is a key inflection point: as costs fall, adoption expands beyond defense and research into industrial and mobility applications.

Market Analysis: Production Scale-Up, Sustainable Feedstocks and Application Breakthroughs

Commercial momentum accelerated through a stream of product launches, capacity expansions and public-sector funding. In November 2024, Aspen Aerogels announced a 30% expansion of North American production capacity to address surging EV thermal barrier demand. That expansion set the stage for 2025 activity: in February 2025 the U.S. Department of Energy published a policy roadmap prioritizing advanced materials for cryogenic insulation in space and LNG transport, increasing programmatic pull for high-performance carbon aerogels. April 2025 saw a German nanomaterials startup successfully pilot 3D-printed monolithic carbon aerogel catalyst supports for green hydrogen production, demonstrating customization and functional integration beyond blanket formats.

Public-private research and sustainability initiatives further broadened the addressable market. In June 2025, the European Commission awarded Horizon Europe funding to a consortium developing bio-based carbon aerogels from waste biomass, aligning aerogel innovation with circular economy mandates. Industry product introductions followed: May 2025 Cabot Corporation launched its ENTERA™ ultra-thin thermal barrier series for Li-ion battery packs, directly addressing battery thermal management and fire-protection needs. Research advances continued into the fall: August 2025 U.S. university teams published a graphene-based carbon aerogel composite for electromagnetic shielding-improving shielding effectiveness by >40 dB for 5G/6G devices-and in October 2025 a Chinese manufacturer added a new production line (initial ~5,000 m²/yr) aimed specifically at EV battery thermal barrier markets.

Carbon Aerogels Market Trends and Opportunities

Trend 1: Multifunctional Interlayers in High-Energy Li-S Batteries

Carbon aerogels are rapidly moving from laboratory additives to structurally critical components in lithium–sulfur (Li-S) battery architectures, particularly as multifunctional interlayers engineered to stabilize high-energy cathodes. The core commercial challenge for Li-S systems—the polysulfide shuttle effect that causes rapid capacity fade—is increasingly being addressed through ultralight, conductive aerogel membranes positioned between the cathode and separator. Recent 2024–2025 electrochemical studies demonstrate that carbon aerogel interlayers act simultaneously as secondary current collectors and physical confinement matrices, adsorbing soluble lithium polysulfides while maintaining electron and ion transport pathways. Cells incorporating these aerogels have achieved discharge capacities of ~807 mAh/g at aggressive 5C rates while sustaining stable performance beyond 500 cycles, a durability threshold that materially shifts Li-S closer to automotive qualification. At the pouch-cell level, aerogel-modified separators have enabled areal capacities compatible with 10 Ah formats, delivering gravimetric energy densities above 417 Wh/kg and ultralow capacity decay of ~0.025% per cycle over 1,000 cycles. This performance is tightly linked to the tunability of aerogel pore architectures: hierarchical micro-/mesoporous networks synthesized at high carbonization temperatures (~800°C) provide high sulfur utilization while preserving reversibility, with reported initial capacities exceeding 1,500 mAh/g and >70% retention after 500 cycles. From a market perspective, this trend positions carbon aerogels as a critical enabler for long-range EVs, aerospace power systems, and defense applications where lithium–sulfur’s theoretical energy advantage cannot be realized without structural polysulfide control.

Trend 2: Hydrophobic and Photothermal Aerogels for Atmospheric Water Harvesting

Carbon aerogels are emerging as a materials backbone for next-generation atmospheric water harvesting (AWH) systems, particularly in arid and off-grid environments where conventional desalination or condensation technologies are impractical. The market is shifting toward multifunctional aerogels that integrate hydrophobic frameworks with photothermal and hygroscopic functionalities, enabling passive, solar-driven water extraction without external power inputs. In 2025, photothermal carbon aerogels enhanced with carbon nanotubes or MXenes demonstrated solar-to-vapor conversion efficiencies approaching 70%, delivering water production rates of 1.8–2.8 L/kg/day even at relative humidity levels as low as 20%. These figures represent a step-change over polymer sorbents and silica gels, which struggle under low-humidity conditions. Parallel advances in “switchable” aerogel chemistries—such as lithium chloride-doped carbon networks—have further expanded applicability by enabling high water uptake (up to 3.52 g/g at 90% RH) followed by low-energy thermal release. When coupled with photovoltaic panels, these systems create synergistic value: waste heat drives desorption while simultaneously cooling PV modules, improving electrical output by ~2.9%. Importantly, durability benchmarks from 2024–2025 show less than 0.7% performance degradation after 20 adsorption–desorption cycles using biomass-derived carbon skeletons, reinforcing the suitability of aerogels for decentralized, long-life water infrastructure. This trend positions carbon aerogels at the intersection of climate adaptation, water security, and renewable energy integration.

Opportunity 1: Cryogenic Insulation for Liquid Hydrogen (LH₂) Infrastructure

The global scale-up of liquid hydrogen across maritime transport, aerospace, and heavy-duty mobility is opening a high-value opportunity for carbon aerogels as next-generation cryogenic insulation materials. Maintaining hydrogen at −253°C remains one of the most energy-intensive aspects of the hydrogen value chain, with boil-off losses directly impacting system efficiency and operating economics. Carbon aerogels, with their ultra-low thermal conductivity and extremely low density, are increasingly specified as internal liners and multilayer insulation components in LH₂ tanks. These materials are central to meeting 2025 U.S. DOE technical targets for hydrogen storage systems, which emphasize both gravimetric (1.8 kWh/kg) and volumetric (1.3 kWh/L) efficiency. Beyond insulation, ambient-pressure-dried carbon aerogels have demonstrated hydrogen physisorption capacities of 5.13–5.65 wt% at cryogenic temperatures, aligning closely with DOE benchmarks and enabling dual functionality as both thermal barriers and supplemental storage media. Regulatory alignment is accelerating adoption: as hydrogen storage and shipping codes converge globally, governments are introducing incentives for advanced composite insulation systems to improve safety and reduce lifecycle emissions. Industrial deployment is already underway, with aerogel-enhanced insulation increasingly incorporated into maritime LH₂ shipping concepts to minimize boil-off during long-distance transport, positioning carbon aerogels as a strategic material for the hydrogen economy’s physical infrastructure.

Opportunity 2: Compliant Substrates for Electronic Skin and Wearable Sensors

The rapid expansion of wearable electronics, digital health monitoring, and human–machine interfaces is creating a structurally distinct opportunity for flexible, conductive carbon aerogels engineered to replicate the mechanical compliance of human skin. Unlike traditional elastomers or metallic meshes, carbon aerogels combine low modulus, high resilience, and stable electrical conductivity, making them ideal substrates for electronic skin (“e-skin”) and soft sensor arrays. In 2025, flexible aerogels derived from sustainable bacterial cellulose demonstrated the ability to recover from repeated compressive strains up to 80% without permanent deformation, a critical requirement for long-term wearability under continuous motion. These materials also exhibit rapid electron transport and stable piezoresistive behavior, enabling high-sensitivity detection of physiological signals such as heart rate, respiration, joint movement, and sweat ion concentration. From a device integration standpoint, advances in laser-patterning and additive fabrication now allow carbon aerogels to be directly printed onto biocompatible substrates such as silicone elastomers and polyimide films, preserving breathability and minimizing skin irritation. This combination of mechanical conformity, sensing fidelity, and user comfort positions carbon aerogels as a foundational material for next-generation medical wearables, rehabilitation devices, and AR/VR haptic systems, where rigid electronics are structurally incompatible with prolonged human contact.

Market Share Analysis: Carbon Aerogels Market

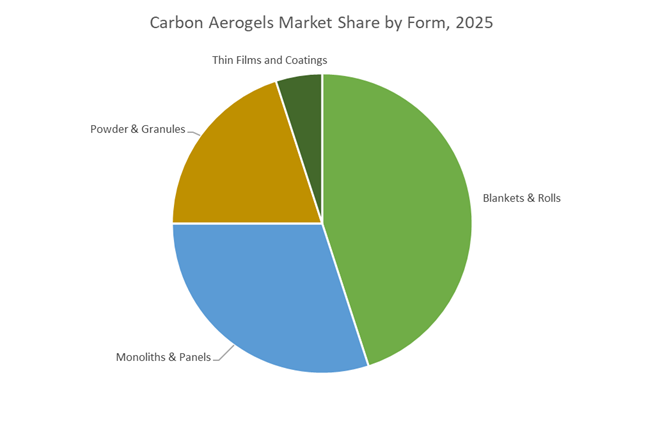

Market Share by Product Form: Blanket & Roll Aerogels as the Commercialization Breakthrough

Blankets and rolls, accounting for approximately 45% of the Carbon Aerogels Market, have emerged as the dominant form in 2025 because they fundamentally resolve the material’s historic fragility constraint while preserving its extreme performance advantages. By integrating carbon aerogels into fibrous reinforcement matrices, manufacturers have transformed what was once a laboratory material into an installation-ready, flexible thermal solution suited for curved, vibration-prone, and space-constrained environments. Production tracking across leading suppliers shows blanket formats approaching 48.7% of total aerogel consumption, reflecting rapid adoption in EV battery enclosures, subsea pipelines, and aerospace thermal shields where rigid panels are impractical. From a buyer economics standpoint, blanket aerogels materially reduce total system cost: next-generation products from Aspen Aerogels enable up to 40% faster installation through roll-to-fit assembly, directly lowering labor hours and production bottlenecks in high-throughput manufacturing lines. Performance remains a decisive driver—thermal conductivity levels as low as 0.013 W/m·K allow designers to cut insulation thickness by as much as 75% versus fiberglass, freeing critical volume for batteries, electronics, or payload. Equally important, ambient-pressure drying and continuous production lines introduced since 2020 have scaled annual output to roughly 5,000 m² per line, driving unit cost reductions of nearly 60%. This convergence of durability, manufacturability, and cost efficiency explains why blanket-form carbon aerogels now represent the commercial backbone of the market rather than a premium niche.

Market Share by Application: Energy Storage as the Primary Value Engine

The energy storage segment, representing roughly 40% of global carbon aerogel demand, has become the market’s principal growth engine as electrification, AI infrastructure, and grid resilience converge in 2025. Carbon aerogels are uniquely positioned because they are both electrically conductive and ultra-light, a combination unmatched by silica aerogels or conventional carbons. This has made them indispensable in EV battery thermal barriers, supercapacitors, and next-generation lithium-ion systems, where managing heat flux and power density directly determines safety and performance. Market evidence shows that battery-related aerogel orders have expanded nearly 20-fold between 2021 and 2025, signaling a structural transition from R&D adoption to mass-market integration. The commercial impact is visible in supplier financials: Aspen Aerogels reported 90% year-over-year revenue growth in its thermal barrier business, driven almost entirely by EV battery applications addressing thermal runaway risk in high-voltage architectures. On the electrochemical side, innovations from Cabot Corporation—including aerogel-derived conductive additives showcased at major international expos—have positioned carbon aerogels as a core material for energy storage systems supporting AI data centers. With demonstrated power densities approaching 895 mW/m³, compared with single-digit outputs for traditional carbon felts, carbon aerogels deliver a step-change in performance per unit volume, anchoring energy storage as the most lucrative and strategically critical application segment in the market.

Competitive Landscape: Flexible Blanket Producers, Specialty Carbon Innovators and Sustainable Start-Ups Compete on Performance and Scale

The competitive landscape is split between large producers scaling flexible aerogel blankets for industrial insulation and energy storage OEMs, specialty carbon firms developing electrode and additive chemistries, and nimble startups commercializing low-cost processes and bio-based feedstocks. Market leaders differentiate by production scale, hydrophobic processing, ultrathin product development for battery packs, and IP in sol-gel and drying technologies. Below are concise company profiles with strategic focus and relevance to the Carbon Aerogels market.

Aspen Aerogels - Market Leader in Flexible Aerogel Blankets Targeting EV Thermal Barriers

Aspen Aerogels supplies Pyrogel® and Cryogel® flexible aerogel blanket products engineered for high-temperature and cryogenic environments and has aggressively targeted the EV battery market with aerogel thermal barriers and fire-protection solutions. Its recent 30% capacity expansion (Nov 2024) underscores a strategy to serve automotive and energy storage OEMs at scale. Aspen’s core strength is large-scale, cost-efficient production of hydrophobic, flexible blankets that balance thermal performance with manufacturability for pack integration.

Cabot Corporation - Specialty Carbon and Ultra-Thin Thermal Barrier Innovator For Battery Systems

Cabot’s ENERMAX® and ENTERA™ product lines focus on carbon additives and aerogel-based thermal protection. The ENTERA™ ultra-thin series (May 2025) is specifically designed for direct integration into lithium-ion battery modules to enhance thermal management and fire protection. Cabot leverages a broad specialty carbon portfolio and ultrafine particle engineering capability to produce conductive, stable aerogel composites for energy storage and performance coatings.

Aerogel Technologies, LLC - Custom Monolithic Aerogels and Licensing Specialist For Advanced R&D

Aerogel Technologies leads in monolithic, custom-designed aerogel materials across carbon and other chemistries, supplying R&D and high-tech sectors including aerospace and nuclear physics. Its licensing model for proprietary sol-gel and drying processes accelerates industrial adoption of bespoke aerogel structures. The firm’s capability to produce tailored nanostructures makes it a prime partner for pilot deployments of catalytic supports and specialized insulation modules.

Svenska Aerogel Holding AB - Particle-Based Aerogel Powders Enabling Mass-Market Coatings and Green Construction

Svenska Aerogel’s Quartzene® platform focuses on non-carbon, high-porosity aerogel powders optimized for integration into plasters, paints and composites. The company is pursuing scale into Sustainable Building Materials, offering easy-to-blend particle formats that improve thermal performance of conventional building products-facilitating mass-market energy-efficient coatings without extensive process change.

Green Earth Aerogel Technologies (GEAT) - Sustainable Aerogel Developer Pushing Ambient-Pressure Drying Commercialization

GEAT specializes in bio-based and organic precursor aerogels, with a strong R&D emphasis on ambient-pressure drying (APD) to dramatically lower production costs and simplify scale-up. The company targets niche high-value applications in defense, space and renewable energy where tailored surface chemistry and porosity (for catalysis and sorption) offer premium value. Continuous APD improvements position GEAT as a cost-effective challenger for commercial viability.

The United States has emerged as the global commercialization nucleus for carbon aerogels, underpinned by defense procurement, EV battery safety mandates, and federally backed climate programs. A defining 2025 milestone was Aspen Aerogels completing a 30% capacity expansion, aligning output with long-term supply agreements from North American automotive OEMs. These contracts prioritize carbon-reinforced aerogel blankets engineered to suppress thermal propagation in high-energy-density battery packs—positioning carbon aerogels as a non-negotiable safety layer in next-generation EV platforms.

Parallel momentum is coming from climate-tech funding. The U.S. Department of Energy updated its Carbon Dioxide Removal (CDR) plan in early 2025 to prioritize high-surface-area carbon aerogels as sorbent scaffolds for Direct Air Capture (DAC). At the same time, Aerogel Technologies introduced mechanically robust carbon aerogels using ambient-pressure drying, targeting a ~25% cost reduction versus supercritical processes—an inflection point for domestic scale economics and supply-chain resilience.

China – Dual-Carbon Policy, Grid Storage, and Environmental Remediation

China’s carbon aerogel strategy is anchored in industrial modernization under the Dual-Carbon framework, where scale and application breadth outweigh bespoke performance. Under Made in China 2025, the Ministry of Industry and Information Technology (MIIT) classified carbon aerogels as a strategic new material, catalyzing capacity additions for oleophilic aerogels used in oil-spill response and wastewater treatment. Domestic suppliers, including Guangdong Alison Hi-Tech, have expanded output to serve municipal and industrial remediation programs.

Energy storage is the second pillar. Provincial hubs in Jiangsu and Shaanxi are piloting carbon aerogel electrodes in utility-scale supercapacitors for grid stabilization, supported by state subsidies in 2025. Defense spillovers are also visible, with national media citing adoption of carbon-aerogel EMI-shielding composites for naval platforms—leveraging the material’s exceptional absorption-to-weight ratio.

Germany – 5G Thermal Management and Green Chemistry Integration

Germany is positioning carbon aerogels at the intersection of telecom infrastructure and circular chemistry. In 2025, Nanolit launched a graphene-integrated carbon aerogel for 5G/6G base stations, delivering ~18% reductions in cooling energy for high-power electronics—an immediate OPEX lever for network operators. This aligns with federal support from the Federal Ministry for Economic Affairs and Climate Action (BMWK), which extended funding for aerogel-based insulation in urban Super Grid projects to stabilize thermal loads in underground HV cables.

On the feedstock side, BASF signaled a strategic pivot toward bio-derived carbon aerogels from lignin, embedding aerogels within Europe’s Green Deal supply chains. This approach strengthens ESG credentials while creating a circular pathway for construction and automotive insulation markets.

South Korea – Battery Safety, Supercapacitors, and Quantum Hardware

South Korea’s carbon aerogel roadmap is tightly coupled with EV battery safety and advanced electronics. In 2025, JIOS Aerogel partnered with a Tier-1 battery manufacturer to deploy carbon-silica hybrid aerogels rated up to 1100 °C as thermal-runaway barriers for high-nickel chemistries—addressing a top OEM risk vector.

Beyond mobility, national labs—working alongside Samsung Electronics initiatives—are evaluating carbon aerogels as cryogenic supports for quantum processors, where low thermal mass and dimensional stability are decisive. Government backing via the K-Battery R&D Fund (active through 2030) has elevated carbon-aerogel electrodes to a priority for ultra-fast-charging supercapacitors, reinforcing South Korea’s end-to-end electronics leadership.

United Kingdom – Aerospace Decarbonization and University Spin-Outs

The UK is carving out a differentiated niche in ultra-lightweight carbon aerogels for aerospace decarbonization. A standout 2025 development was Aerogel Core, a University of Bath spin-out backed by Innovate UK, advancing graphene-based carbon aerogels for aircraft engine soundproofing. Independent testing indicates 50% weight reductions versus conventional materials, translating into 30–90 tonnes of CO₂ savings per year for a 280-aircraft fleet—clear ROI for airlines under tightening emissions regimes.

UK-funded research also targets SAF catalysis, where carbon aerogels act as high-porosity catalyst supports to improve biomass-to-fuel conversion efficiency. Domestically, the Future Homes Standard (2025) is accelerating demand for thin, high-R-value insulation, pulling carbon-treated aerogel blankets into dense urban retrofit projects.

India – CCUS Enablement and Indigenous Aerospace Materials

India’s 2025 strategy elevates carbon aerogels as enabling materials for CCUS and industrial decarbonization. A policy paper from NITI Aayog identifies advanced porous carbons—including aerogels—as critical for abating emissions in steel and cement, with incentives to localize production and reduce import exposure. The rollout of the Carbon Credit Trading Scheme (CCTS) has further stimulated aerogel-based energy-efficiency retrofits to generate tradable credits.

In aerospace, the Indian Space Research Organisation (ISRO) continues to validate carbon aerogel thermal protection systems for reusable launch vehicles, citing successful high-velocity re-entry tests. Together, CCUS policy pull and sovereign aerospace programs are anchoring a domestic demand floor for high-performance carbon aerogels.

2025 Strategic Comparison: Carbon Aerogels National Matrix

Carbon Aerogels National Matrix

|

Country

|

Primary Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

United States

|

Defense & Energy Security

|

Aspen Aerogels +30% capacity

|

EV battery safety, DAC

|

|

China

|

Industrial Modernization

|

Subsidized grid supercapacitors

|

Environmental remediation, storage

|

|

Germany

|

Green Telecom / 5G

|

Graphene-aerogel base station launch

|

Thermal management

|

|

South Korea

|

Battery Safety & Electronics

|

1100 °C thermal barrier rollout

|

EV safety, quantum

|

|

United Kingdom

|

Aerospace Innovation

|

Graphene aerogel spin-out scale-up

|

Acoustic insulation, SAF

|

|

India

|

CCUS & Decarbonization

|

NITI Aayog CCUS material mandate

|

Heavy industry, space

|

Carbon Aerogels Market Report Scope

Carbon Aerogels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$138.6 Million

|

|

Market Size (2035)

|

$816.2 Million

|

|

Market Growth Rate

|

19.4%

|

|

Segments

|

By Raw Material (Polymeric/Synthetic, Cellulosic/Bio-based, Graphene/CNT Composites, Inorganic–Organic Hybrids), By Form (Blankets & Rolls, Monoliths & Panels, Powder & Granules, Sputtered Thin Films & Coatings), By Processing Technology (Supercritical Drying, Ambient Pressure Drying, Freeze Drying), By Application (Energy Storage, Thermal Management, Environmental Remediation, Electronics & Defense, Sensing & Catalysis)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Aspen Aerogels Inc., Cabot Corporation, Aerogel Technologies LLC, Armacell International S.A., BASF SE, Shanghai Aerogelzone Technology Co. Ltd., Guangdong Alison Hi-Tech Co. Ltd., Green Earth Aerogel Technologies, American Elements, Svenska Aerogel Holding AB, Nanolit, Enersens, Active Aerogels, Aerogel-it GmbH, JIOS Aerogel Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Carbon Aerogels Market Segmentation

By Raw Material

- Polymeric/Synthetic

- Cellulosic/Bio-based

- Graphene/Carbon Nanotube (CNT) Composites

- Inorganic-Organic Hybrids

By Form

- Blankets & Rolls

- Monoliths & Panels

- Powder & Granules

- Sputtered Thin Films and Coatings

By Processing Technology

- Supercritical Drying

- Ambient Pressure Drying

- Freeze Drying

By Application

- Energy Storage

- Thermal Management

- Environmental Remediation

- Electronics & Defense

- Sensing & Catalysis

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Carbon Aerogels Market

- Aspen Aerogels, Inc.

- Cabot Corporation

- Aerogel Technologies, LLC

- Armacell International S.A

- BASF SE

- Shanghai Aerogelzone Technology Co., Ltd.

- Guangdong Alison Hi-Tech Co., Ltd.

- Green Earth Aerogel Technologies

- American Elements

- Svenska Aerogel Holding AB

- Nanolit

- Enersens

- Active Aerogels

- Aerogel-it GmbH

- JIOS Aerogel Corporation

*- List not Exhaustive