Market Overview: Vacuum Insulation Panels Transition From Niche Efficiency Upgrade To Core Thermal-Architecture Material

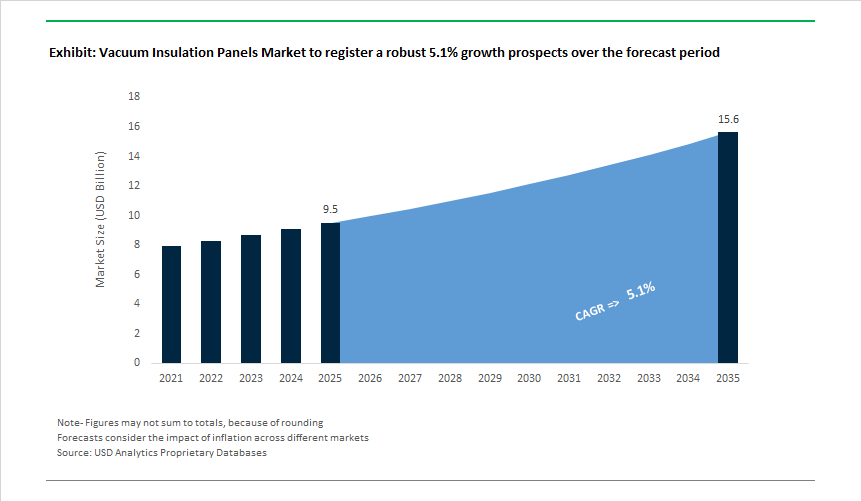

The Global Vacuum Insulation Panels (VIP) Market, valued at USD 9.5 billion in 2025, is projected to reach USD 15.6 billion by 2035, expanding at a 5.1% CAGR, as VIPs move decisively from premium insulation add-ons to system-critical components in buildings, refrigeration, cold-chain logistics, and emerging electrified platforms. Growth is not being driven by volume substitution alone, but by structural constraints-space scarcity, tightening energy codes, and thermal-performance ceilings that conventional foams and mineral insulation can no longer meet.

At a material level, VIPs deliver step-change performance rather than incremental gains. With effective thermal conductivities typically in the 0.0018-0.004 W/m·K range, VIPs provide up to 10-13× the insulation efficiency of polyurethane foam or mineral wool at a fraction of the thickness. This capability is increasingly decisive in applications where envelope thickness directly limits usable volume or energy rating compliance-such as A+++ refrigerators, ultra-low-energy buildings, pharmaceutical cold boxes, and compact thermal zones in mobility platforms.

Manufacturer roadmaps highlight how the category is maturing industrially. Panasonic’s U-Vacua® panels, widely adopted in high-efficiency refrigeration, are engineered to outperform conventional PU insulation by ~13×, enabling OEMs to expand internal storage volume while exceeding regional energy-label thresholds. Evonik and Knauf Insulation continue to advance fumed silica and microporous core technologies optimized for long-term vacuum retention, mechanical robustness, and consistent lambda values under cyclic thermal loading. Dow and OCI are focusing on multi-layer barrier films with improved gas impermeability and seal integrity-addressing one of the industry’s historical failure points: gradual vacuum degradation over service life.

In addition, buying criteria are shifting from nominal R-value to lifetime thermal stability and integration risk. Specifiers are increasingly evaluating VIPs based on barrier durability, edge-loss mitigation, puncture resistance, and certified performance under real-world thermal cycling, rather than laboratory-only metrics. This is particularly evident in building retrofits and cold-chain logistics, where panel replacement is impractical and failure carries high economic or compliance risk.

The demand profile is also broadening geographically and sectorally. In buildings, VIP adoption is accelerating in dense urban markets where façade thickness is regulated or space constrained, supporting compliance with near-zero-energy building (nZEB) and passive-house standards without structural redesign. In refrigeration and cold storage, VIPs are becoming integral to energy-label strategy, not optional upgrades. On the other hand, early-stage use in EV battery thermal protection and specialty transport containers reflects growing interest in ultra-thin, lightweight insulation solutions that decouple thermal performance from package size.

Across segments, suppliers are prioritizing scalable manufacturing, geometry customization, and standardized certification, signaling a transition from bespoke solutions toward repeatable industrial platforms. As energy efficiency thresholds tighten globally and system designers exhaust the performance headroom of conventional insulation, Vacuum Insulation Panels are increasingly positioned not as premium alternatives, but as enabling materials for next-generation thermal architectures-where space efficiency, energy performance, and long-term stability must be solved simultaneously.

Market Analysis: Recent Product Launches, Partnerships and Policy Signals

The VIP market saw important product and policy developments that are reshaping adoption pathways. In Jan 2025, ClearVue and LuxWall announced a collaboration to develop a vacuum-insulated window combining solar PV coatings and VIP technology - a notable extension of VIPs into active façade elements for net-zero buildings. Mar 2023 marked the Hutchinson-va-Q-tec partnership to develop scalable, shaped VIPs for eMobility, and in Jun 2025 regulatory guidance from the UK Environment Agency warned against VIP use in large public housing projects unless manufacturers provide robust end-of-life recycling roadmaps; this has increased pressure on suppliers to demonstrate circularity and recyclability.

Product commercialization accelerated in 2023-2025: Kingspan launched upgraded high-durability VIPs targeted at European retrofits (Nov 2025 product line extension), and Panasonic continued to push VIP adoption in consumer appliances-reducing refrigerator wall thickness by up to 30% and delivering significant energy savings. Most recently, Dec 2025 Va-Q-tec announced a partnership with BASF to co-develop a hybrid VIP + PCM solution for EV battery packs, combining ultra-low conduction with phase-change buffering to improve crash and thermal-runaway resilience. These collaborations and launches reflect a market moving beyond niche appliance and cold-chain use into building envelopes, transport electrification, and integrated thermal systems - but adoption pathways are contingent on addressing edge losses, mechanical robustness, and regulatory end-of-life requirements.

Regionally, Asia Pacific investments since Jul 2023 have increased local VIP production capacity to meet cold-chain and construction demand in China and India, while major appliance OEMs and construction envelope firms in Europe and North America continue to drive specification upgrades and certified installation practices. The near-term competitive advantage will therefore belong to manufacturers that can scale automated, high-yield VIP production, validate long-term barrier film performance, offer hybrid thermal system design services, and demonstrate credible recycling or take-back programs in regulated markets.

Vacuum Insulation Panels Market: Trends and Opportunities

Ultra-Thin, Flexible VIPs Redefine Payload Economics in Cold Chain Logistics

The rapid expansion of biologics, cell & gene therapies, and GLP-1 drugs is fundamentally changing cold chain design priorities—from box-level insulation thickness to payload efficiency per shipment. This has accelerated the development of ultra-thin, flexible vacuum insulation panels (VIPs) using multilayer, high-barrier polymer envelopes that conform to curved and irregular container geometries. Unlike rigid legacy VIPs, these next-generation panels maximize usable internal volume while maintaining ultra-low thermal conductivity.

By 2025, logistics validation data shows that VIP-integrated shipping containers deliver ~30% higher internal storage efficiency versus polyurethane or EPS foam systems. This improvement is economically material, as temperature-sensitive pharmaceuticals now represent over 56% of global drug shipments, where freight cost is driven by volumetric constraints rather than weight. More critically, operational data from 2025 pilots indicate a 33% reduction in product spoilage and a 45% improvement in temperature retention, enabling “zero-excursion” performance across long, intermodal routes.

Smart integration is becoming standard. In April 2024, Kingspan expanded its Inokor platform to combine VIPs with embedded IoT temperature and shock sensors—reflecting a broader shift where ~34% of logistics providers now pair high-performance insulation with real-time monitoring to meet tightening pharma compliance thresholds. VIPs are therefore evolving from passive insulation into active risk-mitigation assets in pharmaceutical logistics.

Fumed Silica and Composite Cores Extend VIP Service Life in Buildings

As VIPs move deeper into construction and infrastructure, long-term performance—not initial thermal conductivity alone—has become the decisive metric. The market is pivoting away from glass fiber cores toward fumed silica (SiOₓ) and fiber-reinforced composite cores, which exhibit superior resistance to vacuum aging caused by gas ingress and moisture diffusion over decades.

Independent technical studies finalized in 2025 show that fumed silica VIPs experience thermal conductivity drift of 0.01–0.1 mW/m·K per year, retaining ~60% of original performance after 30 years—a level aligned with the 25–50 year service-life expectations of modern buildings. Initial conductivities as low as 0.004 W/m·K allow ultra-thin wall assemblies, while even in the event of full vacuum loss, silica cores maintain ~0.020 W/m·K, roughly 2× better than conventional insulation.

Fire performance is reinforcing adoption. With building codes tightening—such as the UK’s Future Homes Standard—non-combustible fumed silica VIPs enable A-grade fire classifications while achieving wall U-values near 0.18 W/m²K. This combination of fire safety, longevity, and space efficiency positions silica-core VIPs as a code-compliant solution for dense urban construction where thickness constraints dominate design decisions.

Deep Energy Retrofits Create Structural Demand Under EU EPBD

The recast Energy Performance of Buildings Directive (EPBD) has transformed VIPs from niche materials into policy-driven retrofit enablers. Finalized across 2024–2025, the directive mandates zero-emission standards for new buildings by 2030 and imposes binding renovation targets on existing stock—particularly the worst-performing non-residential buildings.

EU Member States are required to renovate 16% of non-residential floor area by 2030 and 26% by 2033, a challenge that is structurally difficult in historic city centers where façade preservation is non-negotiable. VIPs offer a unique advantage here: high thermal resistance at millimeter-scale thickness, enabling internal insulation upgrades without altering exterior architecture.

The rollout of Renovation Passports and mandatory Global Warming Potential (GWP) accounting by 2025 further favors VIPs, as they deliver large energy performance gains in stepwise retrofit pathways. With the European Commission estimating €275 billion per year in additional building-sector investment to meet 2030 targets, deep retrofits are becoming a primary allocation channel—one where VIPs are increasingly specified to meet Zero-Emission Building (ZEB) thresholds in constrained structures.

VIP Integration Emerges as a Passive Efficiency Lever in BEV Platforms

Automotive OEMs are beginning to evaluate VIPs as a passive thermal efficiency layer to address one of the most persistent EV challenges: winter range loss. In extreme cold, HVAC loads can consume up to 40% of battery capacity, directly impacting vehicle usability. Ultra-thin VIPs integrated into cabins and battery enclosures reduce heat loss without adding active system complexity.

Experimental verification in 2025 showed that EV cabins using VIP-insulated headliners maintained temperatures ~7.7°C higher than vehicles with conventional insulation under identical heating input—translating into measurable range preservation during cold-weather operation. Beyond comfort, VIPs are gaining attention for battery protection, where they act as thermal barriers that slow heat transfer during abnormal events.

Strategic partnerships are accelerating industrialization. Between 2023 and 2024, Hutchinson partnered with va-Q-tec to develop automotive-grade VIPs for door panels, battery lids, and pack enclosures. As OEMs move toward higher energy-density cells and ultra-fast charging, VIPs are increasingly viewed not as insulation add-ons, but as safety and efficiency enablers that complement active thermal management while adding zero parasitic energy load.

Market Share Analysis: Vacuum Insulation Panels Market

Market Share by Product Type: Flat Vacuum Insulation Panels Define the Industry’s Integration Standard

Flat vacuum insulation panels account for approximately 85% of the global Vacuum Insulation Panels Market, reflecting their position as the most manufacturable, scalable, and performance-efficient VIP format. This dominance is rooted in flat panels’ ability to deliver exceptionally low thermal conductivity in a slim, standardized geometry that aligns seamlessly with appliance assembly lines and building envelope systems. By applying the thermos-flask principle in a low-profile form, flat VIPs achieve insulation performance levels that conventional materials cannot match without significant thickness penalties, making them indispensable in space-constrained designs. Market share is further reinforced by space-saving R-value economics, where thin flat panels unlock higher usable internal volume in appliances and preserve valuable floor area in buildings—benefits that directly translate into customer value and premium product differentiation. Longevity also plays a decisive role, as advanced barrier films and internal getters enable flat VIPs to maintain vacuum integrity over multi-decade lifespans, aligning with long asset replacement cycles in construction and durable goods. From an operational standpoint, flat panels offer installation efficiency advantages, integrating with standard adhesives and workflows while avoiding the complexity and cost of custom-shaped insulation solutions. Together, these performance, integration, and lifecycle advantages position flat VIPs as the default product architecture for the market, securing their overwhelming share.

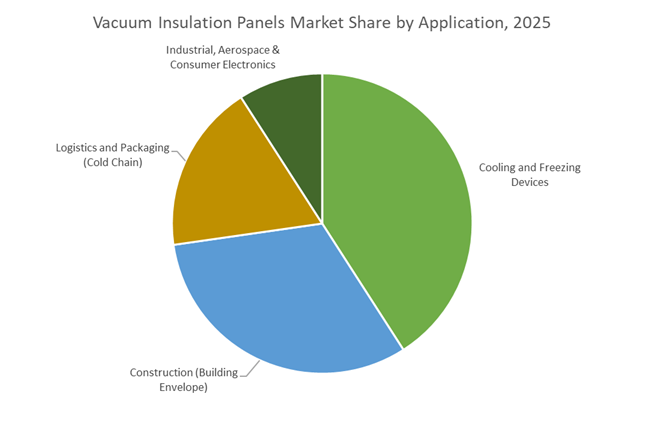

Market Share by Application: Cooling and Freezing Equipment Anchor Commercial Demand

Cooling and freezing devices represent approximately 45% of total demand in the Vacuum Insulation Panels Market, making refrigeration the largest and most commercially influential application segment. This leadership is driven by tightening global energy efficiency regulations and rising consumer expectations for lower operating costs and higher storage capacity. VIPs enable refrigerator and freezer manufacturers to reduce energy consumption materially while simultaneously increasing internal volume—a dual benefit that conventional insulation materials cannot deliver. Market share is further strengthened by the role of VIPs in cold chain resilience, where extended temperature hold times during power interruptions are critical for pharmaceuticals, vaccines, and high-value food logistics. For commercial and industrial buyers, VIP adoption is increasingly justified through clear return-on-investment economics, as energy savings offset higher upfront costs within a relatively short payback period. As appliance manufacturers and cold chain operators prioritize efficiency ratings, lifecycle cost reduction, and regulatory compliance, cooling and freezing applications remain the primary demand engine for vacuum insulation panels, sustaining their leading share in the global market.

Competitive Landscape: Technology IP, Core Material Supply and Application Leadership

Market leaders in VIPs differentiate on three vectors: core purity & engineering (fumed silica, microporous foams), barrier film and vacuum integrity technology, and application systems integration (appliances, façades, cold chain, eMobility). The following company profiles summarize competitive strengths, product focus, and strategic moves relevant to procurement teams and OEM specifiers.

Va-Q-Tec AG - IP-Backed Specialist With The Broadest VIP Product Range and Quality Systems

va-Q-tec holds an extensive IP portfolio (50+ rights) and a proprietary va-Q-check QA system, enabling consistent vacuum integrity and traceable panel performance. The company offers the broadest product range - from flat panels to complex shaped VIPs - and targets high-value refrigerated logistics, appliances, and automotive thermal management. Certifications (TÜV SÜD, ISO 9001/50001/14001) support institutional procurement, and its solutions can sustain multi-day temperature control in cold-chain containers without external power, positioning va-Q-tec as a leader in temperature-sensitive logistics.

Kingspan Group Plc - Vertical Integration Of Vips Into Building Envelope Systems For Passive-House and Retrofit Markets

Kingspan integrates VIP technology into its building-envelope portfolio and has launched a new generation of high-durability VIPs for façade retrofits and floor/wall applications (Nov 2025). The company emphasizes barrier film robustness and installation simplicity to reduce risk in retrofit projects. Its Optimer® line uses advanced fumed silica cores to maximize thermal resistance in minimal thickness assemblies, targeting Passive House and net-zero building specifications across Europe and globally. Kingspan’s distribution and façade system expertise accelerate VIP specification by architects and retrofit contractors.

Panasonic Holdings Corporation - Appliance OEM Driving VIP Scale and Miniaturization For Refrigeration Efficiency

Panasonic leverages in-house VIP manufacturing and automated lines to reduce refrigerator/freezer wall thickness by up to 30%, increasing usable interior volume and cutting energy consumption-delivering compelling value to OEMs and consumers. The company’s scale enables cost competitiveness in high-volume appliance markets while its R&D focuses on next-generation barrier films that preserve vacuum integrity over 15-20 year appliance lifetimes. Panasonic’s appliance adoption case is a key commercial reference for long-life, high-volume VIP deployment.

Evonik Industries AG - Fumed Silica Supplier and R&D Partner Enabling High-Performance VIP Cores

Evonik supplies high-purity AEROSIL® fumed silica, a foundational raw material enabling centre-of-panel λCOP values near industry bests and consistent core processing. The company collaborates on R&D into microporous polymer foams and improved processability to reduce VIP density and enable special-shape panels. Evonik’s material control and global supply capability are strategic for VIP producers seeking consistent thermal and mechanical performance at scale.

Microtherm - Specialist in Ultra-Thin, Niche VIP Products For Aerospace, Transformers and Medical Equipment

Microtherm focuses on ultra-thin VIPs (as thin as 3 mm) and extremely low λCOP (<0.004 W/m·K), servicing space-constrained, high-reliability sectors such as aerospace, high-voltage transformers, and medical devices. The company combines high-precision manufacturing with engineering support for integration, addressing edge-protection and mechanical handling in complex assemblies. Microtherm’s niche approach targets applications where every millimetre and gram matter and where premium performance justifies higher unit cost.

The United States vacuum insulation panels (VIP) market is being structurally accelerated by federal decarbonization funding and the economics of space-constrained retrofits. In 2025, DOE-backed R&D-anchored by national laboratories-has advanced self-healing barrier coatings that materially extend VIP service life, addressing one of the category’s historical adoption barriers. This innovation is particularly relevant for public buildings, hospitals, and federal retrofits where whole-life performance and maintenance cycles determine procurement outcomes. On the commercial side, the expansion of VIP portfolios by manufacturers such as Kingspan is targeting high-R-value performance without wall thickening, a decisive advantage under tightening state and municipal energy codes.

Parallel momentum is visible in packaging and logistics. The reshoring of pharmaceutical and defense cold chains is elevating demand for customized, high-durability VIP solutions that can maintain thermal integrity across long dwell times. As domestic production scales, VIPs are transitioning from a premium niche to a code-driven specification for retrofits, industrial envelopes, and temperature-critical logistics-creating a multi-year demand floor.

China - “Dual Carbon” Targets, Data-Center PUE Limits, and Appliance Efficiency

China’s VIP demand is policy-driven and scale-oriented, tied directly to national energy efficiency mandates. The requirement for new data centers to achieve Power Usage Effectiveness (PUE) below 1.5 by end-2025 has catalyzed VIP adoption in server enclosures, modular shells, and edge-computing hubs, where ultra-thin insulation reduces cooling loads without footprint expansion. Concurrently, domestic manufacturing capacity for silica- and fiberglass-based VIPs has expanded rapidly to support Zero-Emission Building pilots in Tier-1 cities.

The appliance sector provides an additional demand pillar. Refrigerator OEMs are adopting VIP-urethane hybrid insulation to comply with 2025 efficiency thresholds, driving high-volume, standardized VIP formats. This convergence of data-center efficiency, urban building policy, and appliance standards positions China as the largest scale market for VIPs, with cost-down trajectories improving year-over-year.

Germany & the European Union - EPBD Recast and Whole-Life Carbon Compliance

Europe is the primary regulatory engine of the global VIP market, with Germany at the implementation forefront. The 2025 EPBD recast introduces mandatory whole-life carbon (WLC) reporting, structurally favoring VIPs due to their superior operational emission reductions versus conventional insulation. Horizon Europe allocations for “innovative building skins” are accelerating circular VIP development-leveraging recycled glass wool and bio-based fumed silica-to align with Safe-and-Sustainable-by-Design (SSbD) principles.

Industrial supply-side readiness is strengthening as materials leaders expand upstream inputs for VIP cores. Capacity additions by firms such as Evonik Industries AG ensure secure availability of high-purity fumed silica, de-risking project execution for zero-emission buildings and deep retrofits across the EU.

Japan - Expo-Led Demonstration, Residential Retrofits, and Precision VIPs

Japan is leveraging high-visibility demonstrations and materials DX to mainstream VIPs. At Expo 2025 Osaka, stainless-steel-sealed VIPs showcased non-flammability and long-life performance for carbon-neutral cold transport, signaling a shift toward premium, safety-first formats. Policy initiatives from MLIT are simultaneously promoting VIP use in residential retrofits to cut household energy demand, aligning with national CO₂ reduction targets.

Technology leadership remains a differentiator. Precision panels from Panasonic enable ultra-thin insulation for housing and consumer electronics, reinforcing Japan’s role in high-performance niches where thickness, safety, and durability are decisive.

South Korea - Passive House Codes, Heatwave Mitigation, and Battery Safety

South Korea’s VIP market is being pulled by stringent U-value requirements (0.15–0.18 W/m²K) that make VIPs a standard specification in dense, high-rise residential projects. Public health imperatives-mitigating heat stress during extreme summers-are reinforcing adoption in housing and public buildings. Government support programs are lowering entry barriers for domestic producers through R&D credits and preferential financing.

Beyond buildings, VIPs are increasingly integrated into EV battery housings and grid-scale energy storage systems to manage thermal runaway risks. This dual building-plus-battery demand profile creates diversified, resilient growth for VIP suppliers.

India - Cold-Chain Modernization, PLI 2.0, and High-Ambient Performance

India’s VIP adoption is demand-led by pharmaceutical cold chains and energy-efficient appliances. The 2025 expansion of the PLI for White Goods to include high-performance insulation is catalyzing local VIP manufacturing for air conditioners and commercial refrigeration. Health-sector guidance favoring vacuum-insulated shippers for biologics is translating into immediate logistics investments, particularly for last-mile delivery in high-ambient conditions.

Regulatory tailwinds are strengthening as the Energy Conservation Building Code (ECBC) evolves to prioritize high-R-value materials in commercial retrofits. Together, PLI incentives, pharma logistics, and code updates position India as a fast-ramping market where localized VIP supply can scale rapidly.

Strategic Drivers Comparison (2025): Vacuum Insulation Panels Market

Vacuum Insulation Panels Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

Key Regulatory / Policy Event

|

Targeted VIP Core Material

|

|

United States

|

Retrofit efficiency & reshoring

|

DOE self-healing barrier R&D

|

Fumed silica

|

|

China

|

Data-center cooling

|

PUE < 1.5 mandate (2025)

|

Fiberglass / silica

|

|

Germany & EU

|

EPBD compliance

|

Mandatory whole-life carbon reporting

|

Recycled glass wool

|

|

Japan

|

Net-zero logistics & safety

|

Expo 2025 demonstrations; retrofit incentives

|

Stainless-steel sealed

|

|

South Korea

|

Passive house standards

|

Tightened U-value codes; materials support

|

Fiberglass

|

|

India

|

Pharma cold chain & appliances

|

PLI for energy-efficient white goods; ECBC update

|

Bio-based / silica

|

Vacuum Insulation Panels Market Report Scope

Vacuum Insulation Panels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.5 Billion

|

|

Market Size (2035)

|

$15.6 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Core Material (Silica-Based, Fiberglass-Based, Others), By Envelope Material (Plastics, Metals, Hybrid Envelopes), By Product Type (Flat Panels, Special Shape Panels), By Application (Construction, Cooling & Freezing Devices, Logistics & Packaging, Industrial & Aerospace, Consumer Electronics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Panasonic Holdings Corporation, Kingspan Group plc, Evonik Industries AG, va-Q-tec AG, LG Hausys Ltd., Fujian SuperTech Advanced Material Co., Ltd., Morgan Advanced Materials plc, BASF SE, Recticel SA, ThermoCor Inc., Cold Chain Technologies LLC, OCI Company Ltd., Porextherm Dämmstoffe GmbH, Kevothermal LLC, Sofrigam SA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Vacuum Insulation Panels Market Segmentation

By Core Material

- Silica-Based

- Fiberglass-Based

- Others

By Envelope Material

- Plastics

- Metals

- Hybrid Envelopes

By Product Type

- Flat Panels

- Special Shape Panels

By Application

- Construction

- Cooling and Freezing Devices

- Logistics and Packaging

- Industrial and Aerospace

- Consumer Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Vacuum Insulation Panels Market

- Panasonic Holdings Corporation

- Kingspan Group plc

- Evonik Industries AG

- va-Q-tec AG

- LG Hausys, Ltd.

- Fujian SuperTech Advanced Material Co., Ltd.

- Morgan Advanced Materials plc

- BASF SE

- Recticel SA

- ThermoCor, Inc.

- Cold Chain Technologies, LLC

- OCI Company Ltd.

- Porextherm Dämmstoffe GmbH

- Kevothermal, LLC

- Sofrigam SA

*- List not Exhaustive