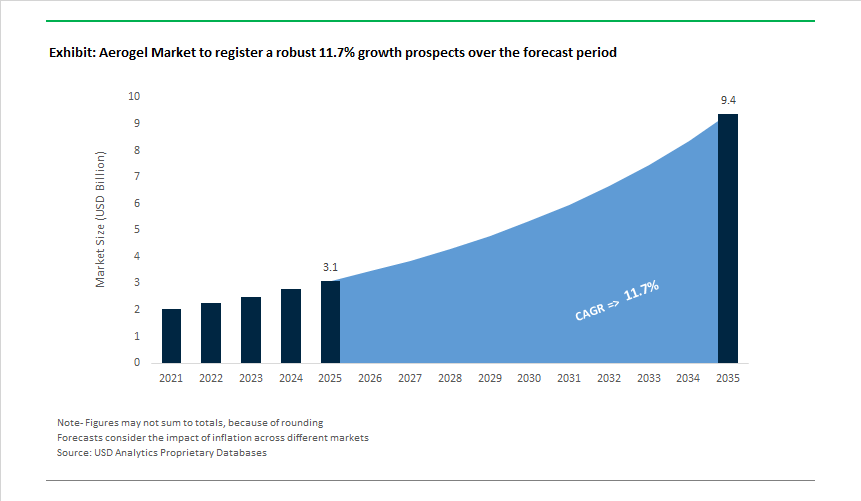

Market Overview: Ultra-Low Insulation and High-Porosity Aerogels Driving 11.7% CAGR To 2035

The Aerogel Market (USD 3.1 billion in 2025; projected to reach USD 9.4 billion by 2035 at an 11.7% CAGR) is transitioning from niche insulation to commercially scaled deployment across energy, mobility, and industrial safety applications. This inflection is driven by aerogel’s ability to deliver ultra-low thermal conductivity (λ ≈ 0.018-0.024 W/m·K) and extreme porosity (95-99.8% air by volume), enabling insulation performance levels that conventional materials cannot match within constrained envelopes. For asset owners and OEMs facing space limitations, retrofit constraints, and rising safety standards, aerogel blankets and panels unlock 50-80% insulation thickness reduction while achieving higher R-values - a decisive advantage in building façades, subsea pipelines, cryogenic LNG systems, and EV battery pack architectures.

At the system level, aerogel adoption is being driven by risk mitigation and lifecycle economics. In industrial processing, energy infrastructure, and offshore environments, aerogel’s inherent hydrophobicity materially reduces corrosion under insulation (CUI) - a failure mode that drives unplanned downtime and costly asset replacement. Leading manufacturers position aerogel blankets as a solution that simultaneously improves thermal performance, minimizes moisture ingress, and extends inspection intervals compared with mineral wool or calcium silicate. In parallel, aerogel’s high continuous-use temperature capability (≈650°C, with blanket systems rated up to ≈1200°C) supports growing deployment in passive fire protection (PFP), battery thermal runaway mitigation, and high-temperature process insulation, where traditional polymer foams and fibrous materials fail to meet safety thresholds.

Over the forecast period, market expansion will be shaped by manufacturing scalability and cost-down trajectories rather than performance differentiation alone. Advances in ambient pressure drying (APD), roll-to-roll blanket production, and composite aerogel formulations are enabling higher throughput and improved mechanical robustness, supporting broader adoption beyond premium projects. Suppliers capable of delivering compression-resistant thermal barriers for EV battery swelling, flexible hydrophobic blankets for retrofits, and standardized panel systems for industrial OEMs are best positioned to displace incumbent insulation materials in high-value segments.

Market Analysis: Recent Commercial Wins, Technology Shifts, and Supply-Chain Actions

The aerogel sector’s commercial and technological momentum intensified, anchored by both OEM adoption in automotive and large industrial insulation projects. In March 2025, Cabot Corporation launched a new silica aerogel line focused on ultra-thin building insulation systems, signaling supplier strategies to target commercial façade retrofits and high-value energy-efficiency upgrades. By July 2025, a major energy industrial firm began a North Sea subsea insulation project deploying aerogel blankets exclusively for LNG and subsea pipeline thermal management - a demonstration of aerogel’s advantage in extreme cold flow-assurance environments.

Through August 2025, academic-industry R&D reported a notable breakthrough in Ambient Pressure Drying (APD) methods that cut energy use by ~40% versus traditional supercritical drying, materially improving the economics of aerogel manufacture and lowering barriers to scale. The EV value chain continued to validate aerogel use: in September 2025, a Korean battery maker filed a patent for a fiber-dispersed aerogel composite designed to retain insulation performance under pack pressurization, underscoring aerogel’s role in battery thermal runaway mitigation. In November 2025, Aspen Aerogels secured a PyroThin® thermal barrier contract with a major European EV OEM for production slated to begin in 2027 - and simultaneously announced internal cost-control measures to shore up profitability amid North American EV market volatility. Also in November 2025, Cabot expanded its sustainability aim by incorporating aerogel products into an EVOLVE™ platform, indicating a supplier shift toward lower-GHG precursor chemistries and circularity goals.

Aerogel Market Trends and Opportunities

Trend 1: Silica Aerogel Adoption in Deep Energy Building Retrofits

Global energy-efficiency mandates and tightening urban planning constraints are accelerating the shift toward ultra-thin, high-performance insulation—positioning silica aerogels as a core material for deep retrofits and heritage preservation. In 2025, developers increasingly specify aerogel blankets and panels where wall thickness is the binding constraint: replacing 50 mm of mineral wool with ~10 mm of silica aerogel routinely frees 3–5 inches of envelope depth. In a 10,000 sq ft commercial retrofit, this translates into 80–120 sq ft of incremental leasable area—an immediate, quantifiable uplift to asset yield that materially improves retrofit ROI. Performance benchmarks reinforce the economics: silica aerogels deliver thermal conductivity in the 0.013–0.018 W/(m·K) range, providing 2×–4× higher R-value per inch than foams or mineral wool and enabling Net-Zero targets without façade alteration or invasive demolition. Fire safety and durability further de-risk adoption. Class-A, non-combustible aerogels maintain hydrophobicity and resist sagging or settlement across 20-year lifecycles, mitigating mold risk and meeting the stricter 2025 green-building certification criteria now common in dense urban cores. Collectively, space efficiency, thermal superiority, and lifecycle reliability are shifting aerogels from “premium option” to “default solution” in constrained retrofit scenarios.

Trend 2: Graphene and Carbon Aerogel Monoliths for Energy Storage

Energy-storage design is pivoting from powder additives toward free-standing, 3D monolithic aerogels that unlock step-changes in power density, cycle life, and manufacturability. In 2025, carbon and graphene-modified aerogel monoliths are demonstrating electrode-level gains that conventional activated carbons struggle to match. Recent electrochemical studies report mass-specific capacitance exceeding 200 F/g with ~94% retention after 5,000 cycles, attributed to continuous, hierarchical pore networks that shorten ion diffusion paths and stabilize redox sites. The implications are material at the system level: monolithic aerogels integrated into compact supercapacitor form factors have sustained >80,000 charge–discharge cycles without degradation—an operational profile aligned to industrial backup, grid buffering, and regenerative braking where maintenance-free longevity is decisive. Hybridization is amplifying value. Graphene-oxide-modified aerogels incorporated into lithium-air and zinc-cobalt chemistries are lifting energy density beyond 500 Wh/kg while preserving flat discharge plateaus, pointing to credible pathways for long-duration, high-capacity storage without the thermal penalties of dense powder compaction. As manufacturing scales, monoliths also simplify electrode assembly and quality control—key to translating lab performance into bankable, repeatable production.

Opportunity 1: EV Battery Fire Safety and Thermal Management

The enforcement of UL 9540A:2025 is catalyzing a structural shift toward aerogel-based thermal barriers as the benchmark solution for preventing cascading thermal runaway in EV battery packs. Aerogel composites combine extreme temperature tolerance (>1,000 °C) with UL94 V-0 flame retardancy, enabling 50–80% reductions in insulation thickness versus mica or ceramic fibers and freeing pack volume for higher energy density. Material innovation is extending beyond insulation into load-bearing functionality: 2025 patents from LG Chem describe aerogel composites with >90% compression recovery, allowing barriers to act as structural spacers that accommodate cell swelling during fast charging while maintaining thermal isolation. Chemical robustness is equally critical. Dual hydrophobic–oleophobic surface treatments now protect aerogels from electrolyte exposure, ensuring barrier integrity during leak or failure events. As OEMs standardize pack designs to pass abuse testing with margin, aerogels are becoming a design enabler—simultaneously improving safety, volumetric efficiency, and manufacturability.

Opportunity 2: Aerogel Composites for Aerospace Cryogenic Insulation

The transition toward liquid hydrogen (LH₂) propulsion is creating a high-stakes demand for ultra-light, ultra-efficient cryogenic insulation—an application where aerogels deliver disproportionate value. Comparative aerospace studies in 2025 show aerogel-insulated LH₂ tanks cutting total system mass by more than 50% relative to fiberglass, preserving payload while enabling zero-emission architectures. Thermal performance is decisive: late-2025 analyses demonstrate boil-off reductions from ~2,019 g/h (fiberglass) to ~3.6 g/h with aerogel configurations—~99.8% fuel-loss mitigation that underwrites long-duration flight safety and economics. Programmatic validation is advancing in parallel. In May 2025, NASA reported progress toward Multi-Layer Aerogel Insulation (MLAI) systems for cryogenic stages, targeting superior durability over conventional MLI and a 3:1 reduction in nitrogen mass uptake during cooldown. As aviation and space platforms converge on LH₂, aerogel composites are emerging as a cornerstone material—unlocking mass efficiency, boil-off control, and operational resilience at scale.

Market Share Analysis: Aerogel Market

Market Share by Material Type: Silica Aerogel Consolidates Dominance Through System-Level Performance

Silica aerogel accounts for approximately 85% of the global aerogel market, a position reinforced not by novelty but by its unmatched system-level performance across insulation, durability, and form-factor adaptability. Its dominance is anchored in an ultra-low thermal conductivity that approaches near-vacuum insulation behavior, allowing engineers to meet aggressive thermal targets with a fraction of the thickness required by mineral wool, fiberglass, or cellular glass. This thickness reduction is not a cosmetic benefit—it directly enables retrofit feasibility, weight reduction, and access to constrained geometries in industrial plants, ships, and buildings where traditional insulation simply cannot fit. Market share is further locked in by silica aerogel’s engineered hydrophobicity, which addresses one of insulation’s most expensive failure modes: moisture ingress and long-term performance decay. Unlike polymer foams or fibrous insulation, silica aerogel maintains thermal stability and mechanical integrity across extreme operating envelopes, surviving continuous temperatures up to 650°C without melting, sagging, or off-gassing. Beyond insulation, its exceptionally high internal surface area has opened adjacent value pools in performance coatings and fire-retardant formulations, reinforcing demand diversity without fragmenting manufacturing scale. The result is a material platform that delivers superior lifecycle economics, regulatory acceptance, and cross-sector applicability—explaining why silica aerogel remains the structural backbone of the global aerogel market.

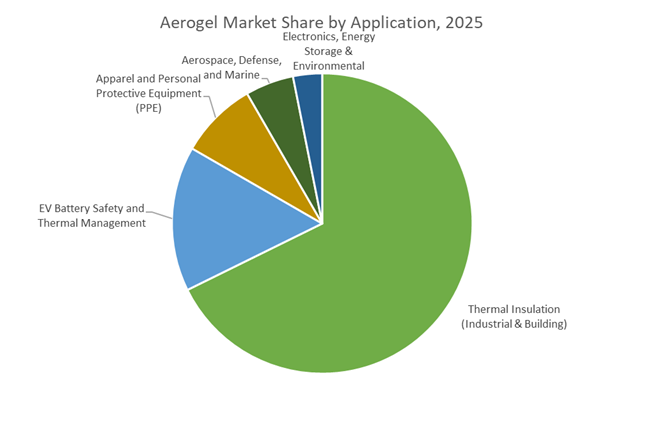

Market Share by End-Use Industry: Oil, Gas, and Petrochemicals Anchor Volume Demand

The oil, gas, and petrochemicals sector represents roughly 30% of total aerogel demand, positioning it as the market’s most consistent volume engine despite growing visibility in consumer and construction applications. This leadership is driven by the industry’s acute exposure to thermal losses, space constraints, and corrosion under insulation (CUI)—a combination of risks that conventional insulation systems struggle to mitigate simultaneously. Silica aerogel blankets deliver decisive advantages in this environment by enabling significantly thinner insulation layers, which reduces topside weight on offshore platforms and frees up space for process equipment in dense refinery layouts. Installation speed is another critical driver: faster wrap-and-seal deployment directly shortens shutdown windows and LNG project timelines, where delays translate into multi-million-dollar penalties. Most importantly, aerogel’s breathable yet hydrophobic structure materially reduces trapped moisture, cutting corrosion rates under insulation by more than half and extending asset life without costly inspection cycles. The segment’s dominance is further reinforced by cryogenic performance requirements, as LNG infrastructure demands insulation that can operate reliably from ambient conditions down to −196°C with minimal boil-off losses. As global energy investments continue to prioritize efficiency, uptime, and corrosion risk reduction, oil and gas applications remain the economic anchor sustaining large-scale aerogel adoption.

Competitive Landscape: Global Suppliers Focusing On EV Safety, Thin-Profile Building Insulation, and Scalable APD Production

The competitive field in aerogels is defined by firms specializing in flexible silica blankets, powder/granule aerogels, and manufacturing innovations (APD/SCD) aimed at driving down cost and expanding applications. Leading suppliers are differentiating via OEM integrations (battery and energy sectors), product form factors (blanket, panel, granule, powder), and moves toward sustainable precursor chemistry and lower-energy drying routes.

Aspen Aerogels: Leader in EV Thermal Barriers and Industrial Flexible Blankets

Aspen Aerogels is the market reference for high-performance PyroThin® thermal barriers and flexible Pyrogel®/Cryogel® industrial blankets, with proven integration into major EV battery programs (e.g., PyroThin® as a core thermal runaway solution) and large cryogenic applications. The company’s product architecture focuses on compression-resilient cell-to-cell thermal barriers and hydrophobic blankets specified for LNG and cryogenic equipment. Aspen’s 2024 DOE loan and its recent Nov 2025 contract with a European EV OEM confirm its strategic position in both automotive safety and industrial insulation, while near-term cost management actions indicate an emphasis on scaling profitability alongside growth.

Cabot Corporation: Silica Aerogel Particles For Thin-Profile Building Systems and Sustainable Platforms

Cabot is a principal global producer of silica aerogel particles (Nanogel®) used to boost the thermal performance of coatings, panels, and glazing systems, enabling double-glazed units with markedly lower U-values and building energy savings. Cabot’s March 2025 product line expansion for ultra-thin insulation and its inclusion of aerogels in the EVOLVE™ Sustainable Solutions program highlight a supplier pivot to sustainable precursors and high-value building efficiency markets. Cabot’s global manufacturing footprint supports scale applications across industrial insulation and specialty catalysis.

Nano-Tech (HK) Limited: APAC Blanket and Panel Supplier Optimizing APD For Cost-Sensitive Volumes

Nano-Tech (HK) is a leading APAC manufacturer of flexible aerogel blankets and panels targeting China’s building-efficiency and industrial infrastructure projects. By focusing on Ambient Pressure Drying (APD) to lower capital and energy costs, Nano-Tech is positioned to provide hydrophobic aerogel felt and boards with high-temperature stability (~550°C) at more competitive price points - a key factor for widescale retrofit adoption in APAC markets. The firm is also advancing carbon aerogel lines for energy-storage and supercapacitor applications.

Jios Aerogel Corporation: Supercritical-Drying Specialist For Powder/Granule Aerogels and Automotive Applications

Jios specializes in supercritical drying (SCD) processes to produce aerogel powders and granules with exceptionally low λ and high surface area purity, serving automotive acoustic and thermal use-cases in engine bays and catalytic shields. Its powder products reduce component surface temperatures substantially and the company is investing in polymer aerogels and fiber-reinforced composites to improve mechanical robustness for dynamic transport environments. Jios’ expansion into European partnerships for daylighting and window systems aligns with regional energy-efficiency directives.

Nichias Corporation: Pyrogel™ Distributor and Industrial Converter Focused On CUI Mitigation

Nichias is a critical Japanese converter/distributor of Pyrogel™ XTE blankets, targeting the power generation, petrochemical, and LNG sectors where CUI mitigation and thin thermal profiles are essential. By marketing Pyrogel™ XTE’s half-to-one-third-the-λ performance of conventional rock wool, Nichias enables thinner insulation and reduced heat loss, with product ratings usable up to ~650°C. Its regional integration capabilities and service to heavy industry make it a go-to partner for retrofits and high-temperature industrial insulation projects.

Aerogel Market Report Scope

Aerogel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2035)

|

$9.4 Billion

|

|

Market Growth Rate

|

11.7%

|

|

Segments

|

By Material Type (Silica Aerogel, Carbon Aerogel, Polymer Aerogel, Others), By Form (Blankets, Monoliths, Particles/Granules, Powders, Others), By Processing Method (Supercritical Drying, Ambient Pressure Drying, Freeze Drying), By Application (Thermal Insulation, EV Battery Safety, Aerospace & Defense, Environmental & Water Treatment, Electronics & Energy Storage, Apparel & PPE), By End-User Industry (Oil & Gas, Construction & Infrastructure, Automotive & Transportation, Aerospace & Marine, Industrial & Chemicals, Healthcare & Research)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Aspen Aerogels Inc., Cabot Corporation, Armacell International S.A., Aerogel Technologies LLC, Guangdong Alison Hi-Tech Co., Ltd., Sino-Aerogel Co., Ltd., JIOS Aerogel, Nano Technology Co., Ltd., Active Aerogels, Enersens, Green Earth Aerogel Technologies, Aerogel-it, Thermablok Aerogels Ltd., Keey Aerogel, Svenska Aerogel Holding AB

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aerogel Market Segmentation

By Material Type

- Silica Aerogel

- Carbon Aerogel

- Polymer Aerogel

- Others

By Form

- Blankets

- Monoliths

- Particles/Granules

- Powders

- Others

By Processing Method

- Supercritical Drying

- Ambient Pressure Drying (APD)

- Freeze Drying

By Application

- Thermal Insulation

- EV Battery Safety

- Aerospace and Defense

- Environmental and Water Treatment

- Electronics and Energy Storage

- Apparel and Personal Protective Equipment

By End-User Industry

- Oil and Gas

- Construction and Infrastructure

- Automotive and Transportation

- Aerospace and Marine

- Industrial and Chemicals

- Healthcare and Research

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aerogel Market

- Aspen Aerogels, Inc.

- Cabot Corporation

- Armacell International S.A.

- Aerogel Technologies, LLC

- Guangdong Alison Hi-Tech Co., Ltd.

- Sino-Aerogel Co., Ltd.

- JIOS Aerogel

- Nano Technology Co., Ltd.

- Active Aerogels

- Enersens

- Green Earth Aerogel Technologies

- Aerogel-it

- Thermablok Aerogels Ltd.

- Keey Aerogel

- Svenska Aerogel Holding AB

*- List not Exhaustive

Table of Contents: Aerogel Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Aerogel Market Landscape & Outlook (2025–2034)

2.1. Introduction to the Aerogel Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Thermal Performance Benchmarking vs Conventional Insulation Materials

2.4. Manufacturing Technologies, Cost Curves, and Scalability Outlook

2.5. Regulatory Landscape, Fire Safety Standards, and Sustainability Drivers

3. Innovations Reshaping the Aerogel Market

3.1. Trend: Ultra-Thin Silica Aerogels for Deep Energy Building Retrofits

3.2. Trend: Carbon and Graphene Aerogel Monoliths for Energy Storage Systems

3.3. Opportunity: Aerogel-Based Thermal Barriers for EV Battery Fire Safety

3.4. Opportunity: Aerogel Composites for Cryogenic Aerospace and Hydrogen Systems

4. Competitive Landscape and Strategic Initiatives

4.1. Capacity Expansion, APD Scale-Up, and Manufacturing Localization

4.2. R&D in Compression-Resilient and Fiber-Reinforced Aerogel Composites

4.3. Sustainability Initiatives, Low-GHG Precursors, and Circular Materials

4.4. OEM Partnerships, Long-Term Supply Agreements, and Vertical Integration

5. Market Share and Segmentation Insights: Aerogel Market

5.1. By Material Type

5.1.1. Silica Aerogel

5.1.2. Carbon Aerogel

5.1.3. Polymer Aerogel

5.1.4. Other Aerogel Materials

5.2. By Form

5.2.1. Blankets

5.2.2. Monoliths

5.2.3. Particles and Granules

5.2.4. Powders

5.2.5. Other Forms

5.3. By Processing Method

5.3.1. Supercritical Drying

5.3.2. Ambient Pressure Drying (APD)

5.3.3. Freeze Drying

5.4. By Application

5.4.1. Thermal Insulation

5.4.2. EV Battery Safety and Thermal Management

5.4.3. Aerospace and Defense

5.4.4. Environmental and Water Treatment

5.4.5. Electronics and Energy Storage

5.4.6. Apparel and Personal Protective Equipment

5.5. By End-User Industry

5.5.1. Oil and Gas

5.5.2. Construction and Infrastructure

5.5.3. Automotive and Transportation

5.5.4. Aerospace and Marine

5.5.5. Industrial and Chemicals

5.5.6. Healthcare and Research

6. Country Analysis and Outlook of Aerogel Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. United Kingdom

6.7. Spain

6.8. Italy

6.9. China

6.10. India

6.11. Japan

6.12. South Korea

6.13. Australia

6.14. South East Asia

6.15. Brazil

6.16. Argentina

6.17. Middle East

6.18. Africa

7. Aerogel Market Size Outlook by Region (2025–2034)

7.1. North America Aerogel Market Size Outlook to 2034

7.1.1. By Material Type

7.1.2. By Form

7.1.3. By Application

7.1.4. By End-User Industry

7.2. Europe Aerogel Market Size Outlook to 2034

7.2.1. By Material Type

7.2.2. By Form

7.2.3. By Application

7.2.4. By End-User Industry

7.3. Asia Pacific Aerogel Market Size Outlook to 2034

7.3.1. By Material Type

7.3.2. By Form

7.3.3. By Application

7.3.4. By End-User Industry

7.4. South and Central America Aerogel Market Size Outlook to 2034

7.4.1. By Material Type

7.4.2. By Form

7.4.3. By Application

7.4.4. By End-User Industry

7.5. Middle East and Africa Aerogel Market Size Outlook to 2034

7.5.1. By Material Type

7.5.2. By Form

7.5.3. By Application

7.5.4. By End-User Industry

8. Company Profiles: Leading Players in the Aerogel Market

8.1. Aspen Aerogels, Inc.

8.2. Cabot Corporation

8.3. Armacell International S.A.

8.4. Aerogel Technologies, LLC

8.5. Guangdong Alison Hi-Tech Co., Ltd.

8.6. Sino-Aerogel Co., Ltd.

8.7. JIOS Aerogel

8.8. Nano Technology Co., Ltd.

8.9. Active Aerogels

8.10. Enersens

8.11. Green Earth Aerogel Technologies

8.12. Aerogel-it

8.13. Thermablok Aerogels Ltd.

8.14. Keey Aerogel

8.15. Svenska Aerogel Holding AB

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures