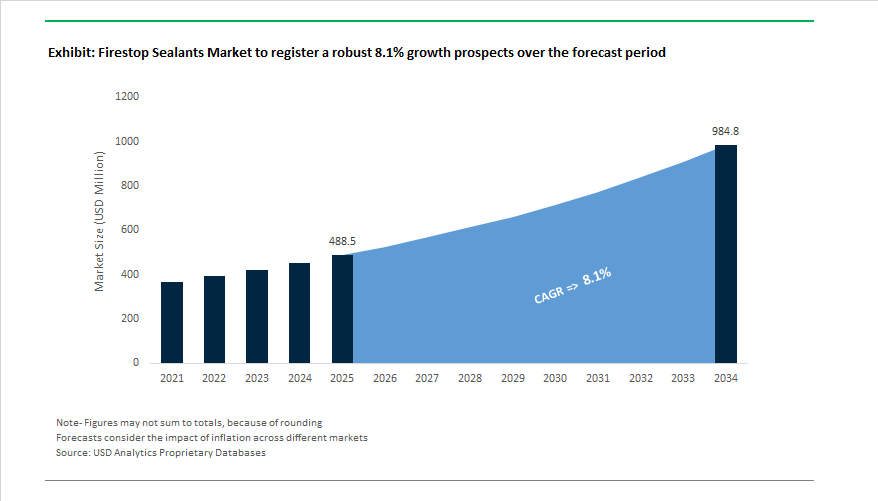

The Global Firestop Sealants Market is expected to expand from USD 488.5 million in 2025 to USD 984.7 million by 2034, advancing at a CAGR of 8.1%, as passive fire protection becomes a non-negotiable design and compliance requirement across modern buildings. Growth is structurally tied to the acceleration of high-rise construction, healthcare facilities, transportation hubs, and data centers—asset classes where compartmentation failure directly translates into life-safety risk, operational downtime, and regulatory exposure. The tightening enforcement of international fire test standards, including UL 1479, ASTM E814, and EN 1366-4, is shifting procurement away from generic sealants toward tested, listed, and system-specific firestop solutions that can reliably deliver multi-hour fire resistance while remaining compatible with complex MEP penetrations and mixed-material assemblies.

From a performance and specification standpoint, firestop sealants are increasingly engineered as multi-functional materials, not single-purpose fillers. Graphite-based intumescent systems designed for service penetrations are achieving free expansion ratios exceeding 30:1, enabling effective closure of annular gaps around combustible pipes such as PVC during fire exposure. In parallel, silicone firestop sealants with ±50% movement capability, qualified under ASTM E1966 and UL 2079, are being specified in high-rise and seismic-active regions to maintain fire integrity under joint movement, vibration, and building drift. Acoustic performance is also influencing material selection, with water-based acrylic firestop sealants delivering Sound Transmission Class (STC) ratings up to 54, allowing designers to address fire and sound attenuation simultaneously in hospitals, schools, and multi-tenant commercial buildings.

Regulatory alignment and construction methodology are reinforcing these adoption trends. Firestop systems are routinely required to achieve 2- to 4-hour F- and T-ratings under IBC and NFPA codes, elevating material choice from a contractor preference to a design-critical decision governed by tested assemblies. At the same time, the shift toward modular construction, prefabricated MEP racks, and offsite fabrication is increasing demand for pre-formed and fast-curing firestop sealants that can be installed with high repeatability and minimal rework. Overlaying these technical drivers is a clear sustainability mandate: manufacturers are transitioning toward low-VOC, halogen-free firestop formulations to meet evolving indoor air quality and worker safety requirements under LEED v5 and REACH.

The Firestop Sealants Market is witnessing a wave of significant product launches, M&A integration, and regulatory tightening that are reshaping both competitive positioning and technological direction.

In August 2025, Specified Technologies Inc. (STI) launched its SpecSeal Cast-In Firestop Device (CID) — a pre-engineered, three-in-one solution combining sleeve, firestop, and waterproofing functions. The innovation directly targets new concrete deck construction, significantly reducing on-site labor and simplifying UL-listed installation compliance. Shortly prior, in July 2025, Sika AG completed the successful integration of MBCC Group, reinforcing its position as a global leader in passive fire protection and expanding its footprint in both construction sealants and waterproofing systems. The integration is expected to boost synergy realization across distribution and product development, strengthening Sika’s leadership in silicone, polyurethane, and acrylic fire barrier technologies.

In June 2025, Hilti Corporation expanded its Firestop Selector digital tool, fully integrated with BIM/CAD platforms, allowing engineers to match tested firestop systems to specific penetrations within seconds. This digitalization move underlines a wider trend — the integration of firestop planning into digital construction ecosystems. Meanwhile, H.B. Fuller (January 2025) highlighted its growing commitment to offsite and modular construction, offering fast-curing, flexible sealants designed for factory pre-assembly and on-site installation efficiency.

From a regulatory standpoint, March 2025 marked a pivotal point as Promat International (Etex Group) introduced low-VOC, environmentally compliant intumescent sealants, directly addressing global Green Building and IAQ standards. The trend toward low-toxicity, installer-safe fire barrier materials was further reinforced by FSi Promat’s October 2024 reformulation of its PyroPro HPE product line — ensuring compliance with occupational exposure guidelines without compromising thermal performance or expansion capacity.

The industry also saw technological breakthroughs led by 3M Company (December 2024) with the enhancement of its Hyper-GS Intumescent Technology, capable of 100× volume expansion, improving retrofit flexibility for cable tray and electrical box penetrations. Additionally, global code reviews initiated in October 2024 are expected to drive the standardization of higher F-Rating requirements, particularly in data centers, hospitals, and critical infrastructure, thereby increasing demand for silicone and graphite-enhanced sealants with high elasticity and endurance.

The Firestopping Sealants Market is prioritizing innovation in intumescent and low-smoke toxicity sealants that enhance life safety beyond fire resistance, addressing one of the most critical aspects of fire emergencies — toxic gas emissions. As smoke inhalation accounts for over 60% of fire-related fatalities, firestop sealant manufacturers are refocusing on halogen-free and low-emission formulations to meet the latest ASTM E814 (UL 1479) and L-Rating smoke leakage compliance standards. These standards ensure that modern firestopping systems function as both flame barriers and smoke containment mechanisms, a necessity in high-occupancy commercial, healthcare, and residential buildings.

Globally, leading manufacturers like 3M, Hilti, and Tenmat are developing advanced halogen-free intumescent compounds that exhibit zero halogen content and achieve “low smoke” emission ratings during testing. These innovations mitigate the release of corrosive and toxic gases, significantly improving evacuation survivability and minimizing post-fire contamination of structural components. Beyond commercial buildings, the advancement has become vital in critical transport sectors, particularly rail. Compliance with BS EN 45545-2 (Railway Fire Safety Standard) requires materials that meet strict benchmarks for smoke density and toxicity, driving cross-sector adoption of premium-grade, low-smoke firestop sealants. The convergence of building and transport fire safety standards highlights a growing market segment that prioritizes both human safety and sustainability, positioning low-smoke, halogen-free intumescent sealants as the cornerstone of next-generation passive fire protection systems.

The expansion of seismic and high-rise construction is reshaping material performance benchmarks, creating strong demand for flexible, dynamic firestop sealants that retain their fire resistance while absorbing structural movement. Unlike traditional rigid formulations, new-generation high-movement firestop sealants are designed to perform under extreme joint stress and thermal expansion conditions, with ±50% movement capability validated through ASTM E1966 (UL 2079) standards. The performance is vital in skyscrapers, airports, hospitals, and bridges, where wind sway, vibration, or seismic activity can compromise traditional firestop integrity.

Recent research and testing from advanced facilities such as Holmes Solutions in New Zealand demonstrate that multi-axial (X-Y-Z) stress conditions can be successfully mitigated using next-generation firestop materials. These systems effectively maintain integrity during up to 50mm of out-of-plane displacement, confirming the viability of flexible intumescent and silicone-based sealants for complex penetration and joint configurations. The market’s focus has expanded beyond fire containment to also ensure structural continuity and post-event serviceability, especially in seismic zones of Japan, California, and Chile, where fire-rated expansion joint systems are integral to performance-based design. Manufacturers are combining elastomeric movement capability with fireproofing and acoustic insulation properties, enabling firestopping materials to serve multiple performance functions within modern resilient construction frameworks.

The retrofit and remediation market for firestop sealants represents one of the most rapidly expanding segments in passive fire protection, fueled by aging infrastructure and stricter post-incident building code enforcement. A significant proportion of high-rise and commercial buildings erected between the 1970s and 1990s suffer from non-compliant, deteriorating, or undocumented firestop systems, which have failed to keep pace with modern fire performance standards. Following catastrophic fire events in global urban centers, government authorities have intensified compliance requirements through routine fire safety audits and building re-certification programs.

Studies estimate that retrofit and replacement projects account for 12%–15% of total global firestop material expenditure, underscoring a lucrative opportunity for manufacturers offering certified, easy-to-apply, and re-entrant sealant systems designed for remedial installation. The market is also benefiting from the digitalization of compliance workflows, where Building Information Modeling (BIM)-enabled firestop mapping allows contractors to document, verify, and replace thousands of fire penetrations per project with precision. The rise of performance-based building safety frameworks across regions like the EU, Middle East, and North America is further reinforcing the demand. Consequently, the industry is witnessing increasing collaboration between firestop manufacturers, construction management firms, and digital compliance platforms, targeting modernization of older structures while ensuring adherence to international standards such as EN 1366-3 and UL 1479.

The global rise of mass timber construction—especially Cross-Laminated Timber (CLT) and glulam hybrid structures—is generating a specialized demand for firestop sealants compatible with timber substrates and hygroscopic materials. As wood buildings reach unprecedented heights (up to 18 stories in Type IV construction, under the 2021 International Building Code (IBC)), fire safety solutions must evolve to accommodate the unique behavior of wood under fire exposure. Unlike concrete or steel, CLT chars predictably at approximately 0.6–0.7 mm per minute, maintaining load-bearing capacity but presenting challenges in penetration sealing and joint detailing.

Specialized intumescent acrylic sealants and fire-protective fillers are being tested under DIN EN 1366-3 for CLT-specific applications, ensuring compatibility with charring layers and preventing premature crack propagation. Certification agencies such as UL Solutions and Warringtonfire have updated their testing protocols (e.g., UL XHEZ guide) to explicitly address firestopping in mass timber assemblies, reflecting the material’s growing adoption in sustainable mid- and high-rise projects. Manufacturers investing in CLT-compatible firestop solutions are well-positioned to capture the expanding niche, as timber buildings proliferate across North America, Northern Europe, and the Asia-Pacific.

In addition, the broader hybrid construction movement, combining steel, concrete, and engineered timber, is driving demand for multi-substrate firestop systems that can adhere to diverse materials under fluctuating moisture and temperature conditions. As global sustainability frameworks such as LEED v4 and BREEAM increasingly favor renewable construction materials, firestopping sealants tailored to sustainable and bio-based substrates are expected to form a critical component of green-certified building envelopes.

Firestop Sealants Market Share Insights, 2025-2034

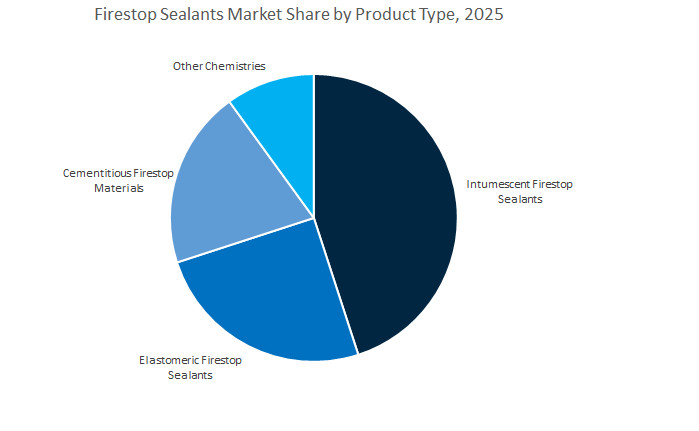

Intumescent firestopping sealants hold a commanding 48% share of the global firestopping sealants industry, underscoring their critical role in fire protection systems across commercial, industrial, and residential buildings. These sealants expand many times their original volume when exposed to high temperatures, forming a carbonaceous char layer that blocks flames, smoke, and toxic gases from penetrating fire-rated barriers. This property makes them indispensable in through-penetration firestopping—the largest application area—and in complex infrastructure where multiple utilities intersect walls and floors. Their versatility across substrates such as concrete, gypsum, and steel, combined with their low smoke emission, excellent adhesion, and compliance with international fire resistance standards (ASTM E814, UL 1479, EN 1366-3), positions them as the industry standard. The rise in green building certifications (LEED, BREEAM) and stringent fire safety regulations in North America, Europe, and Asia-Pacific continues to drive demand.

While intumescent sealants dominate, non-intumescent and ablative firestopping systems maintain significant market relevance. These products, often endothermic or elastomeric in nature, rely on chemical heat absorption or self-extinguishing mechanisms rather than expansion, making them ideal for industrial plants, mechanical rooms, and utility corridors where continuous exposure to heat or chemicals occurs. Firestop foams are gaining rapid traction for their ease of installation and ability to seal irregular or oversized openings—a trend particularly strong in commercial retrofits, cable management systems, and prefabricated buildings. Their expanding polyurethane or acrylic foam matrices enable quick application and strong adhesion to multiple substrates. Firestop putties and gaskets occupy a smaller yet vital segment, offering moldable, re-penetrable, and preformed fire protection solutions for data centers, telecom infrastructure, and electrical junction boxes.

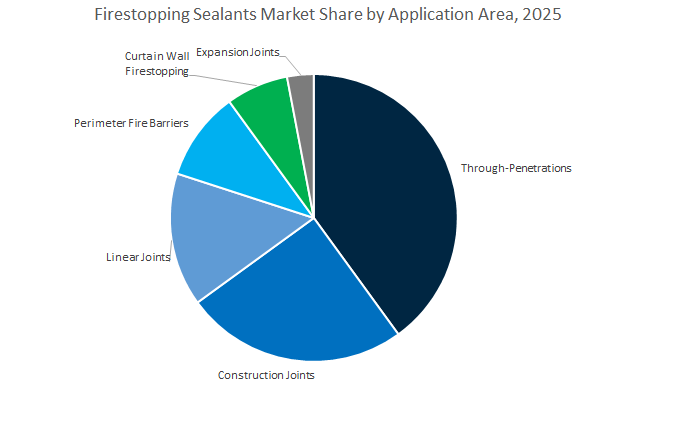

Through-penetrations dominate the global firestopping sealants market, with a 40.2% share in 2025, as modern buildings incorporate extensive mechanical, electrical, and plumbing (MEP) infrastructure. Every penetration—pipes, conduits, or cable bundles—represents a potential breach in a building’s fire barrier system. Intumescent and foam-based sealants are the preferred solutions due to their ability to expand under fire exposure, sealing voids and maintaining fire integrity ratings up to 4 hours. This segment’s growth is heavily influenced by urban high-rise construction, data centers, healthcare facilities, and commercial complexes, where compartmentalization is mandatory for life safety compliance. Furthermore, the proliferation of multi-service penetrations and mixed-material interfaces (plastic pipes, metal ducts, fiber cables) necessitates versatile, high-performance sealant systems. Firestop manufacturers are responding with multi-certified, low-VOC, and paintable formulations that meet both fire and acoustic performance requirements, ensuring safe and aesthetically integrated installations.

Construction joints represent a rapidly growing segment as dynamic movement and thermal expansion become key design considerations in modern architecture. Firestopping sealants in this area must deliver flexibility, adhesion durability, and tested fire resistance, making silicone, polyurethane, and hybrid intumescent systems the preferred materials. These products are vital at head-of-wall, floor-to-wall, and slab-edge joints, particularly in seismic zones and high-rise buildings. Similarly, linear joints and perimeter fire barriers are increasingly critical in facade and curtain wall assemblies, ensuring fire compartmentation between floors and limiting vertical flame spread. The integration of curtain wall firestopping systems—combining sealants with insulation and mineral wool barriers—is expanding rapidly, driven by the global focus on fire-safe building envelopes post high-profile fire incidents. Expansion joints and specialized perimeter systems in infrastructure projects and large-span structures further rely on high-mobility, weather-resistant firestop sealants to accommodate building movement while preserving fire resistance.

The firestop sealants industry is moderately consolidated, with leading players such as Hilti Corporation, 3M, Sika AG, and H.B. Fuller driving innovation through material science advancements, sustainability leadership, and digital engineering tools.

Hilti remains a global leader through its direct sales and technical service model, offering full integration from product specification to installation. Its Firestop Selector platform, integrated with BIM tools, enables instant system verification for MEP contractors, significantly reducing field approval time and compliance risk. The company’s acrylic, silicone, and foam-based firestop sealants deliver multi-hour ratings with enhanced elasticity for dynamic structures. Hilti’s focus on low-VOC formulations (introduced January 2024) demonstrates its alignment with sustainable construction standards and worker safety regulations.

3M is an undisputed innovator in intumescent and elastomeric sealant technologies, offering over 100 UL-tested systems that provide up to 4-hour fire resistance ratings. Its Hyper-GS expansion technology enables 100× volume increase, ensuring superior gap sealing for cables, conduits, and composite penetrations. Flagship products such as 3M™ Fire Barrier Sealant IC 15WB+ and 3M™ Fire Barrier Wrap Strips are globally recognized benchmarks for intumescent acrylic performance. The company’s strategic focus on re-penetrable and flexible fire barrier systems makes it a trusted partner for data centers and smart buildings, where frequent cable retrofits demand resilient firestopping.

Sika AG combines fireproofing, waterproofing, and sealant technologies under a unified “Build Protect Finish Repair” framework. Following its MBCC Group integration (July 2025), Sika expanded its reach in construction and passive fire protection markets, strengthening its position in EN and ASTM-compliant systems. Its Sikasil® and Sikaflex® sealants provide fire resistance up to 4 hours, with the flexibility to handle joint movements and thermal cycling. The company’s global expansion strategy focuses on offering one-source envelope solutions, enabling specifiers to streamline procurement and improve compliance across complex building projects.

H.B. Fuller has positioned itself as a specialist in adhesive and firestop sealant solutions for industrial, modular, and offsite construction. Its solvent-free, single-component elastomeric sealants exhibit strong adhesion to diverse substrates, including concrete, metal, and plastic. The company’s focus on fast-curing and pre-fabrication-friendly products enables modular builders to apply sealants in controlled environments, enhancing productivity and installation accuracy. H.B. Fuller’s move to expand contractor-focused retail distribution channels (2025) demonstrates its commitment to democratizing access to professional-grade sealants for smaller projects and specialized retrofit work.

The United States firestop sealants market continues to evolve through innovation, sustainability initiatives, and regulatory compliance, making it a global benchmark in passive fire protection technologies. In May 2025, Tremco CPG Inc. expanded its firestop sealant product line with advanced intumescent technologies engineered for enhanced reliability in commercial and industrial construction. The aligns with the tightening NFPA and IBC fire safety standards that prioritize comprehensive compartmentation in multi-use structures. Similarly, Hilti Corporation launched a new high-adhesion, fast-curing firestop sealant series in April 2025, aimed at reducing installation time and improving bond strength for fire-rated assemblies — crucial for both new constructions and retrofits.

Environmental sustainability is also transforming the U.S. market landscape. RectorSeal’s introduction of eco-friendly, low-VOC firestop sealants in March 2025 underscores a growing preference for environmentally compliant fire protection products that meet LEED and WELL certification standards. Meanwhile, 3M’s breakthrough technology, featuring enhanced thermal expansion and superior smoke-sealing properties, provides multi-layered fire containment in high-rise and mixed-use buildings, combining safety with energy efficiency. Specified Technologies Inc. (STI Firestop) has also reinforced its leadership by launching next-generation firestop systems capable of preventing the spread of fire, smoke, and toxic gases through complex building penetrations.

China’s firestop sealants industry is expanding rapidly, supported by government policies emphasizing industrial fire safety, green construction, and urban infrastructure modernization. The Ministry of Housing and Urban-Rural Development (MOHURD) has prioritized fire protection in its national construction guidelines, boosting adoption of certified passive fire protection (PFP) materials, including intumescent and acrylic firestop sealants. With continued investment in manufacturing, public infrastructure, and commercial real estate, China’s industrial and construction sectors represent one of the largest application bases for fire-rated sealants globally.

Major domestic players, such as China National Chemical Corporation (ChemChina), are expanding their role in the chemical fire protection value chain, including the development of heat-resistant and flame-retardant additives for sealants and coatings. The market is also benefitting from the government’s push for eco-friendly formulations under its dual-carbon policy, encouraging the use of low-VOC, halogen-free firestop sealants. As urbanization accelerates and industrial safety oversight intensifies, China is poised to become a dominant force in cost-efficient yet high-performance firestopping solutions across construction, infrastructure, and industrial manufacturing sectors.

Germany remains at the forefront of the European firestop sealants market, with a distinct emphasis on sustainable product innovation, industrial compliance, and building certification standards. The nation’s industrial manufacturing and automotive facilities are heavily regulated under DIN and EN standards, creating strong demand for high-performance firestop sealants in mechanical joints, HVAC systems, and logistics infrastructure. The market is simultaneously driven by Germany’s leadership in green construction, where low-VOC and BREEAM/LEED-compliant firestop sealants are integral to achieving energy efficiency and environmental performance goals.

Recent investment trends underline The technological evolution. Dow’s minority equity investment expansion in SAS Chemicals GmbH (May 2024) highlights a strategic move to strengthen the European façade and structural adhesives market, integrating structural silicone and firestop chemistries for curtain wall and façade systems. German chemical leaders are also investing in R&D of hybrid firestop systems, combining intumescent materials with flexible elastomeric polymers to enhance mechanical stability while maintaining fire resistance. As EU environmental regulations tighten, Germany continues to act as the epicenter for innovation in sustainable and REACH-compliant fire protection materials.

The United Kingdom’s firestop sealants industry is undergoing a period of regulatory transformation driven by enhanced building safety requirements following the Grenfell Tower incident. Effective March 2025, the UK is phasing out the BS 476 standard in favor of the European classification BS EN 13501, compelling manufacturers to retest and recertify firestop products to meet new compliance thresholds. The major shift is expected to significantly raise product quality and certification transparency across the fire protection materials market.

The updated BS 9991:2024 Fire Safety Standard emphasizes compartmentation and enhanced fire management in multi-occupancy and residential structures, accelerating demand for certified firestop sealants used in linear joints and service penetrations. In parallel, the Department of Finance’s updated Technical Booklet E (Fire Safety) (May 2025) enforces stricter documentation and quality assurance for firestop installations. Additionally, ROCKWOOL Limited’s new Centre of Excellence for Firestopping (June 2025) in Birmingham provides a state-of-the-art training and production facility focused on coated batts and firestop sealant technologies, bridging the gap between regulatory compliance and practical application. The UK is thus emerging as a regulatory and educational leader in modern firestopping and building compartmentation systems, reinforcing safety, sustainability, and accountability in the construction supply chain.

South Korea’s firestop sealants market is being shaped by the convergence of automotive electrification, high-tech manufacturing, and data infrastructure development. Hyundai Mobis, a subsidiary of Hyundai Motor Group, announced a revolutionary EV battery fire safety technology integrating heat-resistant materials and in-built fire suppression systems to prevent thermal runaway propagation — a breakthrough that highlights the need for flexible, thermally stable firestop sealants in battery modules. Similarly, the 2024 partnership between U.S.-based PACT® and Korea’s BS Technics introduced TR Sleeve™ technology, a thermal containment wrap for battery cells, supported by fire-retardant sealant barriers and coatings that improve vehicle safety performance.

Beyond automotive applications, the rising number of hyperscale data centers in South Korea has amplified demand for intumescent putties and firestop sealants to protect electrical cable penetrations and network infrastructure. The trend is reinforced by government efforts to enhance data infrastructure fire safety standards following recent fire-related outages. South Korea’s integration of next-generation thermal barrier materials, flame-retardant sealants, and intelligent safety systems is positioning it as an innovation-driven hub for high-performance firestop technologies catering to the EV, electronics, and digital infrastructure industries.

Firestop Sealants Market Report Scope

Firestop Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$488.5 Million

|

|

Market Size (2034)

|

$984.7 Million

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Product Type (Intumescent Firestop Sealants, Elastomeric Firestop Sealants, Silicone Firestop Sealants, Hybrid Polymer Sealants, Cementitious Firestop Materials, Other Chemistries), By Application (Cable and Wire Penetrations, Piping Penetrations, Linear Joint Seals, Mixed Penetrations, Structural and Non-Structural Penetrations), By End-User (Commercial Construction, Residential Construction, Industrial, Infrastructure & Transportation, Institutional

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Hilti Group, Sika AG, BASF SE, Dow Inc., Tremco Incorporated, H.B. Fuller Company, Specified Technologies Inc., RectorSeal, Fosroc International Ltd., Pecora Corporation, Promat International NV, Nelson Firestop, Bostik, Rockwool International A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Intumescent Firestop Sealants

- Elastomeric Firestop Sealants

- Silicone Firestop Sealants

- Hybrid Polymer Sealants

- Cementitious Firestop Materials

- Other Chemistries

By Application

- Cable and Wire Penetrations

- Piping Penetrations

- Linear Joint Seals

- Mixed Penetrations

- Structural and Non-Structural Penetrations

By End-Use Sector

- Commercial Construction

- Residential Construction

- Industrial

- Infrastructure & Transportation

- Institutional

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- 3M Company

- Hilti Group

- Sika AG

- BASF SE

- Dow Inc.

- Tremco Incorporated

- H.B. Fuller Company

- Specified Technologies Inc.

- RectorSeal

- Fosroc International Ltd.

- Pecora Corporation

- Promat International NV

- Nelson Firestop

- Bostik

- Rockwool International A/S

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Firestop Sealants Market with a decision-focused lens on code compliance, life-safety performance, and sustainability, delivering analysis reviews that connect chemistry, tested systems, and install productivity to real-world outcomes across high-rise, healthcare, transportation, data centers, and modular/offsite builds. It highlights breakthroughs in halogen-free, low-smoke intumescents; high-movement silicone systems for seismic joints; and digital/BIM-enabled specification that de-risks approvals while accelerating commissioning. Combining verified test listings with cost-in-use benchmarking and risk scenarios under evolving IBC/NFPA and EN standards, this report is an essential resource for specifiers, fire engineers, QS/procurement teams, and owners seeking reliable F-/T-ratings, acoustic and smoke containment, and low-VOC pathways aligned to LEED/BREEAM targets.

Scope Highlights

Segmentation:

- By Product Type: Intumescent Firestop Sealants; Elastomeric Firestop Sealants; Silicone Firestop Sealants; Hybrid Polymer Sealants; Cementitious Firestop Materials; Other Chemistries.

- By Application: Cable & Wire Penetrations; Piping Penetrations; Linear Joint Seals; Mixed Penetrations; Structural & Non-Structural Penetrations.

- By End-Use Sector: Commercial Construction; Residential Construction; Industrial; Infrastructure & Transportation; Institutional.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: 15+ company analyses/profiles including strategies, certifications, and recent developments.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.