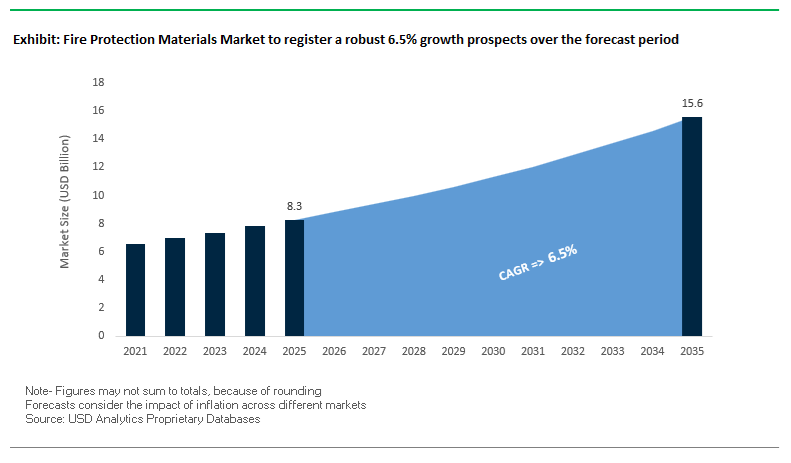

The Fire Protection Materials Market, valued at USD 8.3 billion in 2025, is expected to grow to USD 15.6 billion by 2035, expanding at a strong CAGR of 6.5%. The market is experiencing accelerated momentum as global building codes tighten, passive fire protection (PFP) requirements intensify, and new infrastructure projects demand certified firestop, fire-resistant coatings, and high-performance insulation. Industry professionals are particularly focused on identifying materials that ensure compartment integrity, comply with evolving code standards, support sustainable building certifications, and enable seamless documentation within digital construction workflows.

The global Fire Protection Materials Market is undergoing notable advancements in material science, digital jobsite integration, and regulatory alignment. In January 2026, 3M introduced a new generation of Fire Barrier Electrical Box Inserts using Hyper-GS intumescent technology capable of expanding up to 100× in volume during fire conditions. The innovation supports retrofits and complex electrical penetrations, addressing a persistent safety concern in existing buildings. Months earlier, in December 2025, Sherwin-Williams launched FIRETEX® FX6010 across Europe—a fast-drying, single-leg spray-applied intumescent coating designed to simplify cellulosic fire protection applications and increase project throughput.

The market is also influenced by consolidation and geographic expansion. In November 2025, Sika AG strengthened its Asia-Pacific footprint by acquiring a regional specialist in gypsum-based spray materials and fire-resistant mortars, enabling deeper penetration into high-volume construction markets where fire protection codes are tightening quickly. Regulatory bodies are equally shaping demand; in October 2025, the UK Government initiated a comprehensive review of Approved Document B, with a focus on international property protection standards and potential increases in required fire-resistance durations. The reevaluation signals a strong policy push toward higher fire performance thresholds across the built environment.

Digital transformation is further reshaping firestop workflows. Hilti’s updated Firestop Selector software, released in September 2025, integrates BIM-linked installation documentation and cloud-based compliance tools, helping contractors reduce approval timelines by up to 30%. Meanwhile, research and sustainability trends are accelerating. In July 2025, a German academic consortium presented promising results for next-generation geopolymer foams—recyclable, non-toxic fireproofing insulations offering superior thermal resistance. Regionally, regulatory tightening is also evident: Vietnam’s new Fire Prevention, Fighting, and Rescue Law became effective in May 2025, expanding design-stage fire safety requirements and increasing demand for certified PFP systems. Additionally, in April 2025, a major global data center developer mandated low-smoke, halogen-free firestop materials—underscoring the rising importance of clean-agent PFP products that protect sensitive electronic environments.

As commercial high-rises, industrial plants, data centers, and modular buildings expand worldwide, fire protection materials increasingly must demonstrate higher fire-resistance ratings, superior thermal stability, low toxicity, and regulatory-aligned VOC profiles.

Key performance indicators present significant shifts in compliance expectations and application complexity. Regulatory updates commonly require minimum 3-hour fire-resistance ratings for joints and through-penetrations in major commercial structures. Low-VOC formulations (<250 g/L) are becoming standard for intumescent coatings aligned with LEED and green building criteria. Digitalization is integral to PFP, with BIM-based firestop documentation covering over 90% of life safety elements in new construction projects. Industrial safety requirements are also intensifying, as high-hazard sectors mandate coatings capable of withstanding hydrocarbon and jet fire conditions up to 1,000°C for 4 hours. Meanwhile, modular construction growth—rising over 7% annually—continues to shift demand toward prefabricated fire-resistant panels and integrated fire barrier systems.

- 3-hour fire-resistance ratings are mandated for key through-penetrations in commercial high-rise buildings, accelerating demand for intumescent sealants, firestop mortars, and certified PFP assemblies.

- Low-VOC intumescent coatings (<250 g/L) are becoming essential as green building and LEED-aligned construction expands globally.

- Digital firestop documentation covers 90%+ of critical elements, improving inspection readiness and long-term compliance tracking.

- Hydrocarbon and jet fire coatings must withstand up to 1,000°C for 4 hours, particularly in petrochemical, LNG, and offshore applications.

- Prefabrication growth at 7%+ annually is boosting demand for fire-resistant panels, pre-installed barriers, and modular PFP components.

Regulatory-Driven Material Upgrades and Sustainability-Led Innovation Accelerating Growth in the Fire Protection Materials Market

Trend 1 - Mandatory Upgrades to Intumescent Coatings for Structural Steel in Tall Timber Construction

Mass timber adoption in mid- and high-rise construction is reshaping fire protection requirements for hybrid steel–timber structures. The 2021 International Building Code (IBC) introduced new categories-Types IV-A, IV-B, and IV-C-that impose stringent fire-resistance standards on all load-bearing structural elements. Type IV-A in particular mandates a three-hour fire-resistance rating and requires all mass timber components to be fully encapsulated by non-combustible materials. This radical shift elevates the role of intumescent coatings as essential protective systems for exposed and embedded structural steel.

The protection requirement extends to steel connectors, which anchor primary mass timber elements. To comply with ASTM E119, the average temperature rise on the unexposed side must stay within 250°F above ambient, necessitating intumescent coatings engineered for prolonged insulation performance and precise char expansion behavior. This regulation reshapes specification patterns for architects, engineers, and fire protection consultants in the mass timber construction ecosystem.

Thin-film intumescent coatings are gaining market share due to their aesthetic superiority. For Architecturally Exposed Structural Steel (AESS), these coatings deliver a smooth, uniform finish that seamlessly supports modern architectural design without compromising fire resistance. Their rise coincides with the global movement toward visually expressive timber–steel hybrid frames.

Innovation in this segment is accelerating. Next-generation water-borne intumescent coatings incorporating microencapsulated Ammonium Polyphosphate aim to overcome the moisture sensitivity of legacy formulations. Enhanced durability, lower VOCs, and improved long-term performance in humid environments represent core R&D priorities as market leaders race to meet expanding code-driven demand.

Trend 2 - Fire-Resistant Barriers and Encapsulation Systems Become Essential for Lithium-Ion BESS Safety Compliance

As grid-scale and commercial Battery Energy Storage Systems (BESS) proliferate, high-profile thermal runaway incidents have triggered global regulatory tightening. Passive fire protection materials are now indispensable components of BESS design, enclosure engineering, and installation planning.

NFPA 855, the cornerstone standard in North America, mandates strict spacing and grouping requirements for ESS installations-three feet of clear separation for every 50 kWh grouping, unless equivalent engineered mitigation systems are deployed. Fire-rated barriers with one- or two-hour protection enable operators to reduce spacing and increase energy density, making fire-resistant wall systems, encapsulation materials, and inter-module shields essential to BESS project economics.

Fire behavior evaluation is governed by UL 9540A, which assesses thermal runaway propagation at the cell, module, and unit level. This test methodology directly drives demand for high-performance passive mitigation materials that can demonstrably limit heat transfer and flame spread. Manufacturers are prioritizing materials that retain structural integrity, maintain insulation capacity at peak thermal loads, and resist decomposition under rapid temperature rise.

A unique hazard with Li-ion fires is the release of extremely toxic and flammable gases, requiring materials that both contain fire and safely vent or neutralize off-gases. Encapsulation systems must integrate specialized seals, venting geometries, and non-reactive barrier layers to prevent secondary ignition events and safeguard personnel. The convergence of safety regulations and grid-storage deployment growth ensures sustained demand for advanced fire-resistant BESS materials.

Opportunity 1 - High-Transparency Fire-Rated Glazing Solutions for Open-Plan Architecture and Egress Compliance

The architectural preference for open, transparent layouts-spanning atriums, corridors, and transition zones-creates a high-value commercial opportunity for fire-rated glazing systems that combine life-safety performance with aesthetic freedom. Modern fire-rated glass technologies, including glass-ceramics, borosilicate laminates, and multi-layer intumescent laminates, deliver both architectural clarity and stringent fire compartmentation.

Leading systems achieve integrity ratings ranging from E30 to E120 minutes, enabling compliance for egress routes, exit doors, and atrium boundaries. These expanded fire durations align with global requirements such as India’s NBC 2016, which mandates up to 120 minutes of fire protection for designated exit doors. Crucially, these glazing systems remain transparent during fire exposure-allowing emergency responders to assess interior conditions, identify occupants, and plan rescue operations.

The drive toward seamless architectural integration is intensifying demand for glazing with zero coefficient of thermal expansion, minimal visual distortion, and availability in large sheet dimensions (e.g., 2100 mm × 3200 mm). Such characteristics enable the construction of large fire-rated glass façades, expansive partition walls, and frameless door systems without compromising structural or visual performance.

As urban development trends emphasize space efficiency, natural light, and visual connectivity, fire-rated glazing stands out as a high-growth segment with strong specification pull from architects and code authorities alike.

Opportunity 2 - Non-Toxic, Sustainable Flame Retardant Systems for Textiles and Plastics in Consumer and Contract Furnishings

Growing regulatory scrutiny of halogenated flame retardants (HFRs)-long associated with human health risks-has accelerated global demand for sustainable non-halogenated flame retardant (NHFR) chemistries. This shift is particularly pronounced in the consumer furnishings, contract interiors, and textile manufacturing sectors.

Research from the U.S. National Institute of Environmental Health Sciences (NIEHS) links exposure to legacy HFRs such as PBDEs with endocrine disruption, developmental disorders, and neurological impacts. These scientific findings underpin increasingly restrictive regulations by the EPA and ECHA, pushing manufacturers toward safer alternatives.

The industry’s material science transition is anchored in new fire-retardant mechanisms:

- Endothermic Cooling via magnesium and aluminum hydroxides, which absorb heat and reduce substrate temperature.

- Char Formation Mechanisms driven by phosphorus-based compounds that generate a protective insulating layer on the polymer surface, suppressing flame spread without toxic byproducts.

Global compliance pressure is intensifying. Europe and North America have introduced stringent rules regulating products containing halogenated FRs, compelling exporters-including major producers in Asia-Pacific-to adopt NHFR formulations to retain market access. This geopolitical regulatory dynamic is accelerating adoption of bio-based, inorganic, and hybrid NHFR systems across textile, upholstery, mattress, and commercial furnishing supply chains.

The push toward low-toxicity, environmentally compliant flame retardants constitutes one of the fastest-evolving innovation streams in the fire protection materials market, creating long-term opportunities for chemical innovators and specialty polymer manufacturers.

Fire Protection Materials Market Share Analysis

Market Share by Type of Protection: Passive Fire Protection Leads Through Mandatory Structural Safety and Lifetime Reliability

Passive Fire Protection (PFP) secures the highest 62% market share in the Fire Protection Materials Market, underscoring its critical role as the first and most dependable barrier against fire progression in built environments. Unlike active systems, PFP does not rely on sensors, activation mechanisms, or external power sources—making it essential for ensuring structural integrity from the very first moments of a fire event. Regulatory requirements drive its dominance: building codes mandate that core load-bearing components such as steel columns, beams, and reinforced concrete must maintain fire resistance for 60, 90, or 120 minutes, depending on the structure’s classification and risk profile. This requirement directly fuels demand for intumescent coatings, cementitious sprays, and fire-rated boards, all engineered to delay structural collapse and provide adequate evacuation time.

PFP’s market leadership is further reinforced by its role in compartmentation, where fire-rated walls, floors, and penetration seals restrict the Rate of Fire Spread (ROFS), contain smoke movement, and prevent flashover across large buildings. This compartmental strategy is indispensable in high-density construction—hospitals, airports, office towers—where fire spread must be restricted to protect both life and critical assets. Additionally, PFP offers compelling lifecycle cost advantages, requiring little to no maintenance over a building’s 50+ year lifespan, in stark contrast to Active Fire Protection (AFP) systems that require periodic inspection, testing, and replacement. These performance, regulatory, and economic factors combine to elevate PFP as the largest and most indispensable category within the fire protection materials landscape.

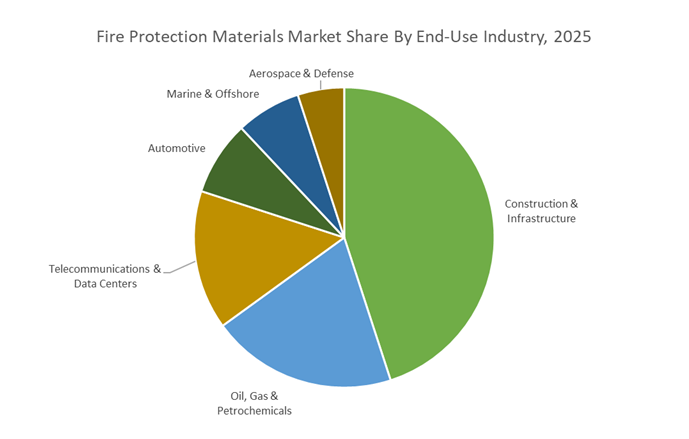

Market Share by End-Use Industry: Construction & Infrastructure Dominates Through Code-Driven Adoption and High-Volume Global Demand

Construction & Infrastructure leads the market with a 45% share, anchored by its comprehensive and legally binding requirements for Passive Fire Protection across virtually all building types. Global building codes—including the International Building Code (IBC) and national fire safety regulations—mandate the use of PFP solutions to achieve specified fire resistance ratings for structural systems, partitions, and egress pathways. High-rise structures, tunnels, public facilities, and institutional buildings frequently require up to 3-hour fire-resistance ratings, driving significant consumption of intumescent coatings, fire-rated drywall, cementitious sprays, and high-performance firestop systems. As construction volumes continue to expand globally—particularly in urban megaprojects and emerging markets—the scale of PFP material demand rises proportionally.

Beyond regulatory mandates, the Construction & Infrastructure segment commands its leading share due to the sheer volume of components requiring fire protection. Every fire-rated wall, barrier penetration, door assembly, service duct, and structural column within residential, commercial, and institutional buildings contributes to cumulative material consumption, making this segment by far the largest user of PFP materials. Additionally, the protection of Means of Egress—including stairwells, corridors, lobbies, and exit routes—forms a non-negotiable safety requirement, as these elements must maintain fire integrity long enough to ensure occupant evacuation. The growing prioritization of resilient building design, safe urban density, and compliance with evolving performance-based fire engineering standards further solidifies Construction & Infrastructure as the dominant end-use sector for fire protection materials.

Country Analysis: Global Fire Protection Materials Development Hubs

China: Regulatory Crackdowns and High-Rise Urbanization Driving Explosive Passive Fire Protection (PFP) Demand

China is experiencing one of the world’s most aggressive expansions in Passive Fire Protection (PFP) materials due to intensified regulatory enforcement, dense high-rise urbanization, and mandatory upgrades to national fire safety codes. Following several high-rise fire incidents—including notable cases in Hong Kong—the Ministry of Emergency Management and State Council Work Safety Committee launched a nationwide rectification campaign in late 2025, demanding immediate inspections of fire hazards in residential and commercial towers. This campaign imposes strict oversight on external wall insulation systems, particularly targeting flammable insulation materials and enforcing compliance with bans on non-rated exterior systems. As a result, demand for non-combustible rock wool, fireproof composites, certified insulation boards, and up-rated exterior cladding materials has surged across major provinces.

China’s mandatory national code, GB 50016 (updated 2023), is driving some of the largest-volume procurements of firestop systems, fire-rated boards, penetration sealing materials, and structural fire protection products in the global market. With over one million high-rise buildings taller than 27 meters, city-scale retrofits are underway to reinforce fire cutoffs, upgrade smoke barriers, and ensure the performance integrity of fire-rated door seals. Manufacturing capacity is expanding rapidly to meet demand, especially in intumescent coatings, fire-resistant sealants, and fireproof mortars, reflecting China’s unmatched scale in construction materials production. Beyond construction, fire safety in electric vehicles is becoming a top priority; domestic automakers are increasing integration of ceramic and mica-based fire barriers within EV battery packs to comply with tightening national standards designed to arrest thermal runaway propagation, a major risk factor in high-voltage EV systems.

United States: NFPA-Driven Compliance and Federal Investment Accelerating Next-Generation Fire Protection Materials

The United States remains a global leader in fire protection materials through its continual advancement of NFPA and ICC model codes, stringent testing requirements, and strong federal support for safer energy infrastructure and EV fire mitigation technologies. Model codes such as the International Building Code (IBC) and NFPA 1 are frequently updated to incorporate new data from structural fire science and high-hazard building use cases. Their adoption by states and municipalities drives sustained demand for fire-resistant coatings, listed firestop systems, fire-rated partitions, and compliant joint systems across commercial, industrial, and high-density residential projects. Federal support is playing an increasingly central role: in October 2024, the U.S. Department of Energy issued a $670.6 million loan to Aspen Aerogels, accelerating domestic production of advanced fire-safe battery materials, underscoring the government’s push to strengthen EV battery fire resilience.

Product innovation continues to shape the U.S. market, with 3M’s 2025 enhancement of Fire Barrier Tuck-In Wrap Strips—featuring Hyper-GS Intumescent Technology capable of expanding up to 100x its volume—marking a major leap in sealing performance for complex through-penetrations. The regulatory environment for high-hazard sectors is also evolving, with NFPA 2 (Hydrogen Technologies) and NFPA 4 (Integrated Systems Testing) driving the need for specialized fire-rated enclosures, detection systems, and multi-system integration in hydrogen facilities and next-generation energy installations. Leading providers such as Hilti continue to invest heavily in UL- and ASTM-certified systems, including solutions tested to ASTM E1966 (UL 2079) for fire-rated construction joints. The U.S. market therefore remains at the forefront of innovation in fire protection materials, code compliance technologies, and advanced fire-stopping solutions across high-risk environments.

European Union / Germany: Sustainability-Driven Fire Protection and Clean Agent Innovation Under Green Deal Mandates

The European Union, supported by Germany’s engineering and materials leadership, is pursuing one of the most sustainability-driven fire protection frameworks globally. Regulations under the European Green Deal are reshaping the landscape for fire protection materials by tightly linking environmental performance with fire safety compliance. A major development occurred in November 2023, when the EU adopted Delegated Regulation (C(2023)7486) mandating that all treated or modified wood products achieve a minimum D-s2, d0 classification under EN fire standards. This requirement ensures that mass timber and hybrid wood construction employ certified fire-retardant treatments (FRTs), driving rising demand for fire-retardant coatings, impregnated treatments, and certified pyrolysis-resistant systems.

The region continues to phase out environmentally harmful fire suppression systems such as Halon 1301, sustaining demand for clean agents (e.g., Inergen), water mist systems, and fluorine-free suppression technologies aligned with circular economy mandates. European materials companies are pioneering advanced fire safety solutions for electric vehicles, with Arkema’s Foranext Gaseous Thermal Barrier (GTB) launched in January 2024. This breakthrough material creates a protective thermal barrier around overheating cells, helping prevent thermal runaway propagation in EV battery packs. Continental regulations under the Construction Products Regulation (CPR) harmonize fire performance standards for structural materials, sealants, mortars, and protective claddings, further solidifying Europe’s position as a global leader in sustainable, certified fire protection solutions.

Japan: High-Reliability Fire Protection Materials for Dense Infrastructure and Miniaturized Electronics

Japan’s fire protection materials market is shaped by its need for extremely reliable fire protection systems across high-density public transport structures, advanced infrastructure, and miniaturized electronics ecosystems. Significant ongoing investment in fire-resistant coatings for high-speed rail tunnels, metro systems, and urban infrastructure hubs reflects Japan’s priority on ensuring uninterrupted operation in environments where structural fire safety is critical. The demands of public transportation networks—especially during refurbishment of aging infrastructure—are accelerating adoption of ultra-durable intumescent coatings, fire-resistant concrete additives, and advanced smoke control systems tailored to confined environments.

Japan’s leadership in electronics and semiconductor miniaturization is generating demand for ultra-thin intumescent films, fire-retardant encapsulation resins, and micro-scale flame barriers. These materials are essential for protecting increasingly compact electronic assemblies where spacing between components is minimal, amplifying the risk of arc faults and overheating. In the automotive sector, Japanese firms continue to lead the development of ceramic and mica-based insulating materials engineered for internal EV battery cell isolation. These materials meet stringent domestic automotive fire safety standards, ensuring enhanced protection against short circuits and thermal runaway within battery modules. Collectively, Japan’s focus on reliability, durability, and advanced materials science anchors its position as a global leader in next-generation fire protection materials.

Competitive Landscape: Global Leaders Advancing Intumescent Chemistry, Digital Firestop Systems, and High-Temperature Industrial Insulation

The competitive landscape of the Fire Protection Materials Market is characterized by major players expanding their firestop portfolios, introducing next-generation intumescent technologies, acquiring regional specialists, and integrating digital tools to streamline life safety compliance. Companies are prioritizing solutions that address regulatory tightening, energy-sector complexity, modular construction growth, and the need for long-term durability across commercial, industrial, and infrastructure environments.

Hilti maintains a dominant position in engineered firestop systems, offering sealants, foams, blocks, collars, and modular devices designed to simplify firestop installation in penetrations and joints. A major milestone came in September 2025, with the launch of its enhanced Firestop Selector tool, integrating BIM capabilities and cloud-based compliance documentation to reduce project complexity and improve inspection readiness. Hilti’s core strengths include deep engineering expertise, robust installer training programs, and its ability to integrate fire protection into digital construction environments, making it a preferred partner for high-rise, industrial, and healthcare projects.

3M is a central innovator in intumescent technology and fire barrier solutions, offering wraps, sheets, sealants, and intumescent devices known for reliability and ease of installation. In January 2026, the company launched its Fire Barrier Electrical Box Inserts featuring 100× expansion Hyper-GS technology, targeting back-to-back electrical boxes and challenging retrofit applications. With strong capabilities in polymer chemistry and fireproofing science, 3M continues to deliver products that meet stringent UL, ASTM, and global building code requirements while simplifying field installation.

Sherwin-Williams continues to grow its leadership in protective and marine coatings through its FIRETEX® product range, which includes solutions for both cellulosic and hydrocarbon fire risks. The December 2025 launch of FIRETEX® FX6010 demonstrates its commitment to improving application efficiency with faster-drying, single-leg spray intumescent coatings suitable for large structural steel installations. Sherwin-Williams remains a key supplier for commercial infrastructure, industrial facilities, and petrochemical assets requiring high-performance PFP solutions.

Sika’s core offerings in sealing, bonding, and building envelope solutions extend strongly into passive fire protection, particularly fire-resistant mortars, sealants, and coatings used across commercial and infrastructure projects. Its November 2025 acquisition of a regional fire-resistant materials producer in APAC expands its production capabilities, allowing the company to meet increasing demand in fast-growing construction markets. Sika’s longstanding expertise in durable, flexible fire-rated sealants and jointing materials strengthens its competitiveness in high-volume, code-driven environments.

Morgan Advanced Materials specializes in high-performance thermal insulation and fire-resistant ceramic fiber systems, including Microtherm and Superwool solutions. These materials deliver superior heat resistance and low weight, making them essential for fire protection in industrial furnaces, marine systems, and aerospace applications. The company continues to innovate with low bio-persistence ceramic fibers, enhancing both environmental and worker safety performance.

AkzoNobel’s International Protective Coatings division offers recognized brands including Chartek and Interchar, widely used in oil & gas, petrochemical, and offshore industries where hydrocarbon and jet fire protection is mission-critical. The company strategically integrates its PFP coatings with anticorrosion systems to deliver combined CUI (corrosion under insulation) and passive fire protection performance. Its legacy of reliability in extreme industrial environments makes it a key supplier for energy, marine, and heavy infrastructure sectors.

Fire Protection Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.3 Billion

|

|

Market Size (2035)

|

$15.6 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Type of Protection (Passive Fire Protection, Active Fire Protection), By Passive Material Type (Firestop Products, Intumescent Coatings, Fire-Rated Boards & Sheets, Fire-Resistant Structural Materials, Flame Retardant Chemicals), By Active Suppression Agent (Clean Agents, Water-Based Systems, Foam-Based Systems, Dry Chemical Powders, CO₂ Systems), By End-Use Industry (Construction & Infrastructure, Oil Gas & Petrochemicals, Automotive, Marine & Offshore, Aerospace & Defense, Telecommunications & Data Centers), By Application Area (Compartmentalization, Penetration Sealing, Structural Steel Protection, Cable Protection, Ductwork Insulation)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hilti Corporation, 3M Company, Hempel A/S, Sherwin-Williams Company, International Fire Protection, Minilec Group (Spectris plc), Axon Interconex (Isolatek International), Promat International NV (Etex Group), Knauf Insulation, Aspen Aerogels Inc., United Technologies, Tyco Fire Protection Products, Rotary Fire Protection

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fire Protection Materials Market Segmentation

By Type of Protection

- Passive Fire Protection (PFP)

- Active Fire Protection (AFP)

By Passive Material Type

- Firestop Products

- Intumescent Coatings

- Fire-Rated Boards & Sheets

- Fire-Resistant Structural Materials

- Flame Retardant Chemicals

By Active Suppression Agent

- Clean Agents

- Water-Based Systems

- Foam-Based Systems

- Dry Chemical Powders

- CO₂ Systems

By End-Use Industry

- Construction & Infrastructure

- Oil, Gas & Petrochemicals

- Automotive

- Marine & Offshore

- Aerospace & Defense

- Telecommunications & Data Centers

By Application Area

- Compartmentalization

- Penetration Sealing

- Structural Steel Protection

- Cable Protection

- Ductwork Insulation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Fire Protection Materials Suppliers

- Hilti Corporation

- 3M Company

- Hempel A/S

- Sherwin-Williams Company

- International Fire Protection (IFP)

- Minilec Group (Spectris plc)

- Axon Interconex (Isolatek International)

- Promat International NV (Etex Group)

- KNAUF Insulation

- Aspen Aerogels, Inc.

- United Technologies

- Tyco Fire Protection Products

- Rotary Fire Protection (RFP)

- Advanced Material Science Companies

*- List not Exhaustive