Market Overview: Advanced Materials Market Value, Growth Outlook & Strategic Insights to 2035

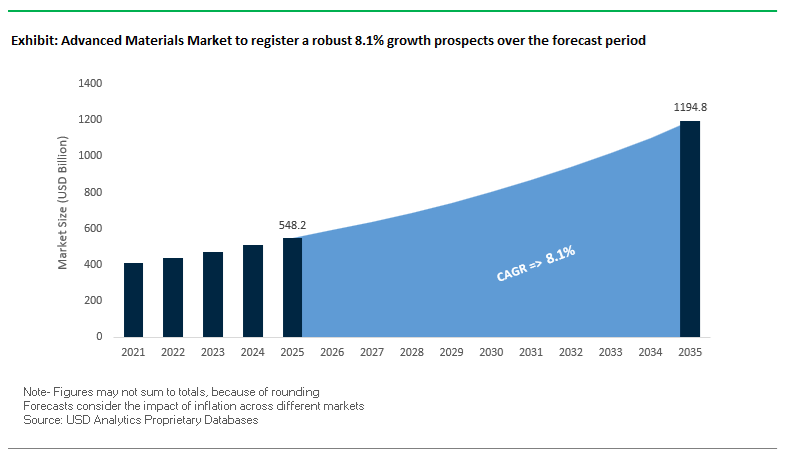

The Global Advanced Materials Industry, valued at USD 548.2 Billion in 2025, is projected to reach USD 1,194.5 Billion by 2035, expanding at a robust CAGR of 8.1% (2025–2035). This strong growth trajectory is driven by transformative shifts across aerospace, semiconductors, electric mobility, nanotechnology, and sustainability-centric manufacturing. Industry professionals increasingly seek advanced polymers, composites, and high-performance materials that enable AI infrastructure, next-gen electronics, lighter aircraft, and high-density EV batteries. The market is evolving beyond conventional materials, pivoting toward R&D-intensive, high-value categories where performance, cost efficiency, and regulatory alignment determine competitive advantage.

Key Consumer Insights for Advanced Materials Vendors

- Global R&D Investment Surge: Leading corporations invested €1.3 trillion in 2022, with a meaningful share dedicated to advanced materials enabling AI computing and next-gen semiconductor ecosystems.

- Aerospace & Defense Remains a High-Value Buyer: Sustained demand for carbon fiber composites, titanium alloys, and advanced ceramics drives premium margins.

- Cost Barrier in Nanomaterials: Prices exceeding $1,000 per gram restrict mass-market adoption but accelerate innovation in high-performance segments.

- EV Revolution Reshaping Materials Demand: Strong reliance on silicon carbide (SiC), advanced battery chemistries, and lightweight structural materials.

- EU’s Advanced Materials Act to Reshape Innovation: Aiming to streamline commercialization from “lab to fab”, enhancing domestic competitiveness and supply chain resilience.

Market Analysis: Recent Strategic Shifts, M&A Activities & Innovation Trends in the Global Advanced Materials Industry

The Advanced Materials Industry experienced a series of high-impact strategic developments across policy, mergers, financing, and R&D acceleration. In November 2025, Teck Resources announced the filing of materials for a Merger of Equals with Anglo American, creating the proposed “Anglo Teck.” With over 70% copper exposure and expanded access to critical minerals, this entity significantly influences supply chains for high-performance copper alloys, semiconductor wiring solutions, and conductive materials, tightening global competition for electronic-grade copper resources. During the same month, the European Union progressed its Advanced Materials Act, signaling a major legislative push to expedite commercialization cycles, support domestic innovators, and fortify strategic sectors-from renewable energy and defense to EV manufacturing.

Also in November 2025, Rayonier Advanced Materials showcased resilience in challenging economic conditions, reporting $353 million in Q3 2025 net sales, reaffirming strong demand for high-purity cellulose, a critical feedstock for specialty chemicals, filtration systems, and advanced engineered materials. In the consumer materials segment, Kimberly-Clark announced a landmark acquisition agreement to purchase Kenvue for $48.7 billion, creating a combined consumer-health giant with extensive exposure to specialty polymers, absorbent materials, and chemical solutions used in personal wellness products. This move indirectly influences raw-material consumption patterns, procurement cycles, and product innovation requirements for advanced polymer suppliers.

In September 2025, AMSilk GmbH secured €52 million in financing, accelerating the commercialization of silk-based biopolymers, an increasingly vital category for sustainable advanced materials used in medical implants, performance textiles, and biocompatible coatings. This financing wave highlights investor appetite for bio-derived, recyclable, and low-carbon materials capable of replacing petroleum-based counterparts. Earlier in June 2025, EY reported that global corporate R&D spending increased 6% in 2024, despite slower revenue growth, underlining how advanced materials remain a strategic priority for tech and chemical conglomerates. Finally, March 2025 marked a pivotal acceleration in AI-driven materials discovery, with machine learning models increasingly used to simulate molecular structures, optimize nanomaterials, and reduce prototype cycles for high-temperature alloys and semiconductors.

Key Trends Transforming the Advanced Materials Market

Trend 1: Nationalization of Critical Material Supply Chains Reshapes Global Sourcing Strategies

One of the strongest forces reshaping the advanced materials ecosystem is the global shift toward supply chain sovereignty. Governments are deploying unprecedented capital, regulatory enforcement, and security-led industrial mandates to secure domestic capabilities. In the U.S., the CHIPS and Science Act has become a catalyst for demand in ultra-high-purity SiC and GaN substrates as $39 billion in semiconductor manufacturing subsidies and $13 billion in R&D funding incentivize fabs to diversify away from Asia and prioritize domestic material procurement. This nationalization trend is mirrored by Europe’s Critical Raw Materials Act, which imposes measurable targets—40% domestic processing and 25% recycling of strategic raw materials by 2030—creating predictable long-term demand for European refining and processing materials.

Defense agencies are also directly shaping the materials landscape. In July 2025, the U.S. Department of War mobilized the Defense Production Act to provide a $400 million equity injection and a $150 million loan to MP Materials to build domestic heavy rare earth separation capacity. These interventions signal that rare earth magnets, high-temperature alloys, and specialized coatings are no longer only economic assets; they are defense-critical resources. The EU’s rule capping single-country reliance at 65% for any strategic material further compels OEMs to diversify suppliers, creating new investment corridors for processing hubs in regions such as North America, Africa, and Southeast Asia. Collectively, these policy shifts establish long-term anchors for advanced material demand tied directly to national security and energy transition priorities.

Trend 2: ESG Enforcement Accelerates Innovation in Low-Carbon and Non-Toxic Advanced Materials

Material science innovation is increasingly driven by quantifiable ESG requirements rather than voluntary sustainability initiatives. Automotive suppliers such as Valeo now operate under validated mandates to reduce upstream Scope 3 emissions by 15% by 2030, pushing the industry toward recycled aluminum (which offers up to 95% energy savings compared to primary production), bio-sourced polymers, and lightweighting materials with verified low-carbon footprints. These procurement pressures are influencing alloy design, composite formulation, and surface treatment innovation across the entire mobility value chain.

A similar transformation is underway in the steel sector. Green steel, previously cost-prohibitive, is expected to see its premium drop from approximately $210 per tonne to just $7 per tonne by 2030 as GH2-DRI plants scale commercially. This shift will fundamentally alter procurement strategies for high-volume industries where steel remains irreplaceable. At the same time, tightening regulations such as REACH are eliminating legacy materials like hexavalent chromium, forcing rapid adoption of sustainable yet high-performance alternatives. Coatings such as CVD tungsten carbide, which can extend component life by up to 250 times in abrasive environments, are emerging as frontrunners in sectors that require durability aligned with environmental compliance. ESG, therefore, is no longer an external driver but a foundational determinant of material innovation cycles.

Major Opportunities in the Advanced Materials Market

Opportunity 1: Commercialization of Drop-In Sustainable Materials with Performance Parity

Industries are prioritizing advanced materials that meet stringent carbon targets without requiring extensive re-engineering of existing systems. This creates a significant opportunity for suppliers capable of delivering drop-in materials with identical or superior mechanical, thermal, and environmental performance. Europe’s lithium processing expansion under the CRMA is a case in point: if all 19 proposed facilities move forward, the region could meet up to 80% of its lithium processing needs by 2030. Building this capacity demands corrosion-resistant alloys, high-integrity membranes, and specialized reactor materials, opening a multi-year supply runway for producers of advanced industrial materials.

Simultaneously, companies like Constellium are proving the commercial viability of guaranteed low-carbon aluminum solutions for automotive body structures. These materials retain conventional performance characteristics while offering substantially reduced embedded emissions and high recycled content. For OEMs pursuing Scope 3 alignment, such materials present a low-risk, high-impact route to meeting decarbonization commitments, making this segment one of the most commercially attractive in the near term.

Opportunity 2: Advanced Materials as Enablers of Next-Generation Hydrogen and Carbon Capture Systems

Hydrogen production, seawater electrolysis, and carbon capture innovation are constrained primarily by material limitations, creating a high-value opportunity for breakthrough coatings, membranes, and catalysts. Recent research demonstrated a triple-protected electrocatalyst capable of sustaining 3,000 hours of real seawater electrolysis at high current density—an important validation that advanced surface engineering, including LDH-based coatings and multi-layer defense electrodes, can significantly accelerate the viability of coastal hydrogen generation.

Current PEM systems rely heavily on expensive Nafion™ membranes and platinum-group catalysts. Advancements in Anion Exchange Membranes (AEMs) hold the potential to dramatically reduce system costs by enabling cheaper transition metal catalysts, but they still face durability and current density challenges. Addressing these gaps represents one of the largest material science opportunities of the coming decade, particularly as governments scale gigawatt-level hydrogen hubs and industrial decarbonization projects.

Advanced Materials Market Share Analysis

Market Share by Product Type: Composites Maintain Market Leadership with 28.4% Share

Composites dominate the Advanced Materials Market with a 28.4% share in 2025, firmly positioned as the largest product category due to their unmatched combination of lightweighting, high strength, corrosion resistance, and energy-efficiency performance. Their leadership is directly tied to escalating demand from aerospace, next-generation automotive platforms, EV battery enclosures, and large-format wind turbine blades, where material substitution toward low-weight, high-performance structures is accelerating. Their ability to enhance fuel efficiency, extend EV driving range, and meet demanding structural integrity requirements solidifies composites as the preferred engineering solution across multiple industries. Surrounding segments reinforce this trend: polymers continue to expand on the back of recyclable and bio-based materials for sustainable manufacturing; ceramics gain relevance in high-temperature and high-wear environments; metals & alloys retain indispensable roles in turbines, engines, and defense systems where thermal stability is critical; nanomaterials emerge as the fastest-scaling category driven by electronics, batteries, and nano-enhanced composites; while functional materials grow in importance as clean-energy systems demand advanced battery, photovoltaic, and fuel-cell materials.

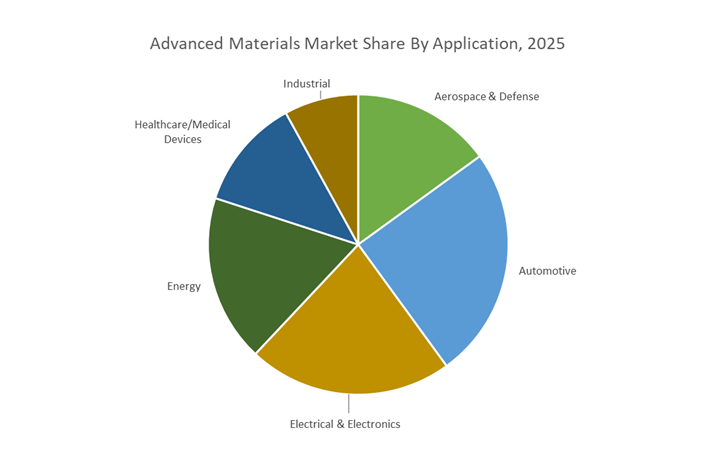

Market Share by Application: Aerospace & Defense Leads with 15.8% Share

Aerospace & Defense holds a 15.8% share of the Advanced Materials Market in 2025, underpinned by its inherent need for high-strength, lightweight, thermally stable materials that can withstand extreme operating environments. The segment’s share is reinforced by rising global aircraft production, modernization of defense fleets, and the rapid adoption of additive manufacturing (3D-printed alloys and composites) to improve performance and reduce component weight. Advanced ceramics, superalloys, and high-modulus composites remain essential to improving durability, fuel efficiency, and mission-readiness across air, space, and defense systems. Meanwhile, the broader application landscape showcases strong momentum: the automotive sector remains the dominant volume driver, propelled by the EV revolution and its demand for battery materials, lightweight composites, and high-efficiency magnets; electrical & electronics continue to scale with the adoption of SiC and GaN materials for power devices; the energy sector accelerates advanced material use for batteries, photovoltaics, and hydrogen systems; healthcare steadily rises with growth in implants and drug-delivery devices; and industrial applications rely on high-performance coatings and catalysts to enhance process reliability.

Market Share by Form: Sheets & Films Lead with 24.3% Share

Sheets & Films account for 24.3% of the Advanced Materials Market in 2025, supported by massive demand from flexible electronics, solar energy films, high-performance packaging, touch sensors, and display technologies. Their production scalability, uniformity, and suitability for next-generation device architectures make them a cornerstone of advanced manufacturing. The segment’s dominance is reinforced by the rapid rise of printed electronics, thin-film photovoltaics, and flexible consumer devices, all of which rely heavily on engineered film materials for conductivity, transparency, and mechanical behavior. Supporting segments further shape the market: resins & polymers remain essential feedstocks for composite and additive manufacturing systems; powders & particles continue to be the fastest-growing form factor due to exploding demand from additive manufacturing in aerospace, medical, and automotive industries; coatings sustain high-margin adoption for corrosion protection, optical enhancement, and surface functionality; and fibers & fabrics, particularly carbon and glass fibers, scale in alignment with composite material expansion.

Competitive Landscape - Strategic Positioning & Innovation Leadership in the Advanced Materials Industry

The competitive environment in the Global Advanced Materials Industry is defined by high R&D intensity, aggressive portfolio optimization, scale-driven production capabilities, and deep integration with high-growth end-use industries such as aerospace, electronics, EV batteries, and semiconductors. Each leading player is doubling down on specialized materials-from high-purity polymers to carbon composites and advanced ceramics-to secure long-term contracts with strategic industries. Sustainability, circularity, and high-performance engineering remain the core differentiators shaping global leadership.

BASF SE - Global Leadership in Advanced Polymers and Circular Materials

BASF SE leverages the world’s largest chemical production footprint to deliver a comprehensive portfolio of advanced polymers, catalysts, performance chemicals, and next-gen coating materials. The company’s increasing emphasis on bio-based coatings, “self-healing” material innovations, and circular economy frameworks reflects its strategy to lead high-performance and sustainable materials markets. With operations in 90+ countries, BASF invests heavily in R&D to maintain its technological edge in chemical intermediates, polymer additives, and specialty materials used across automotive, aerospace, electronics, and industrial infrastructure.

3M Company - Multifunctional Advanced Materials with Deep IP Strength

3M’s competitive advantage is rooted in its diverse technology platforms and strong pipeline of advanced materials-from thermal management films and conductive adhesives to precision abrasives critical for electronics and semiconductor manufacturing. The company is strategically shifting toward high-growth segments such as semiconductor materials and advanced healthcare solutions, leveraging approximately 3,000 patents annually. This scale of innovation reinforces 3M’s dominance in high-value applications that require material reliability, form factor optimization, and long-term durability.

DuPont de Nemours, Inc. - High-Performance Materials for Critical Infrastructure & Electronics

DuPont remains a global leader in advanced materials for semiconductors, protective applications, and water systems through products such as Teflon fluoropolymers, Kevlar aramid fibers, and specialty electronic materials. The company continues optimizing its portfolio through divestments and an intensified focus on electronics and infrastructure protection materials, supporting high-reliability applications in 5G networks, advanced manufacturing, and wearable technologies. Its leadership in engineered polymers and high-strength fibers sustains strong demand across defense, industrial safety, and semiconductor fabrication.

Hexcel Corporation - Aerospace-Centric Advanced Composites Powerhouse

Hexcel Corporation specializes in carbon fibers, prepregs, honeycomb structures, and resin systems, making it a critical supplier to major global aircraft programs. With aerospace platforms increasingly prioritizing lightweighting for fuel efficiency, Hexcel’s materials remain essential for commercial aviation, defense aircraft, and space systems. The company maintains a global manufacturing footprint across the Americas, Europe, and Asia, allowing it to serve OEMs with consistency, quality, and rapid delivery cycles in a sector where materials performance directly impacts operational safety and energy efficiency.

Samsung Electronics Co., Ltd. - Advanced Semiconductor and Battery Materials Innovator

Samsung is both a major consumer and developer of advanced materials, with deep focus areas spanning semiconductor-grade chemicals, OLED display materials, and next-generation battery chemistries through Samsung SDI. Its R&D investment, projected at $25.2 billion in 2024, underscores the company’s commitment to pioneering material informatics, solid-state battery innovation, and ultra-pure semiconductor materials. Samsung’s scale and technological leadership position it at the center of global materials innovation for electronics, EVs, and AI computing.

LG Chem - Global Leader in Advanced Battery Materials & Electronic Chemicals

With core strengths in petrochemicals, IT materials, and lithium-ion battery components, LG Chem plays a central role in global EV supply chains. The company is expanding EV battery material production across North America and Asia, supported by its portfolio of over 25,000 battery-related patents. LG Chem’s innovations in solid-state batteries, cathode materials, and polymer electrolytes establish it as a dominant force in next-generation energy storage and materials for large-scale ESS and automotive applications.

Country Analysis: Global Advanced Materials Market Innovation Hubs

United States: Leadership in Semiconductor Materials, Clean Energy Innovation, and Defense-Grade Advanced Materials

The United States remains the world’s most influential innovation hub in the advanced materials market, driven by strategic federal investments, semiconductor leadership, and accelerated clean energy initiatives. A core priority for the US is the creation of a resilient and self-sufficient domestic advanced materials supply chain, strengthened significantly by the 2024 CHIPS for America Act. The Biden–Harris Administration’s announcement of $100 million in AI-driven semiconductor materials R&D highlights a national agenda to boost sustainable next-generation microelectronics. This complements the country’s aggressive push toward clean energy materials, as federal agencies collectively propose over $11.3 billion in RD&D funding for high-efficiency energy materials, quantum-led fusion materials research, and climate-aligned industrial technologies.

The US also maintains its competitive edge in defense-grade materials through the DARPA FY2024 $4.4 billion budget request, which accelerates breakthroughs in nanomaterials, aerospace composites, high-temperature alloys, and next-gen structural materials for military modernization. Emerging industrial hotspots like Northern Virginia’s “Data Center Alley” are driving the adoption of AI-optimized sustainable concrete, supplied by Titan America, illustrating how advanced construction materials are scaling with hyperscale digital infrastructure expansion. Meanwhile, companies like Hexcel Corporation continue to solidify the nation’s dominance in carbon fiber composites for aerospace and defense, reinforcing the US as a global epicenter for high-performance engineered materials.

China: Rapid Scaling of New Materials, Semiconductor Self-Sufficiency, and Green Manufacturing Leadership

China’s advanced materials market is defined by an assertive state-backed strategy under Made in China 2025, which sets strict targets for achieving 70% domestic content in core materials by 2025. This policy direction has catalyzed massive state funding into high-tech materials, nanomaterials, and specialty chemicals. A central driver is the commitment of $20.2 billion to the National Integrated Circuit Industry Investment Fund, aimed at attaining semiconductor materials independence across wafers, photoresists, and advanced packaging substrates. China is also accelerating its R&D infrastructure expansion, with plans to establish 40 advanced research centers dedicated to materials science, nanotechnology, and industrial innovation by 2025.

The country is simultaneously strengthening its leadership in green manufacturing, promoting new materials that reduce industrial emissions and enhance resource efficiency across petrochemicals, steel, and construction sectors. China’s vast NEV (New Energy Vehicle) ecosystem continues to stimulate demand for advanced polymers, lightweight composites, and high-performance EV materials. However, oversupply, price competition, and fluctuating technology preferences are reshaping investment momentum in EV materials. Even with these challenges, China remains the fastest-scaling advanced materials ecosystem in the world.

Germany (Europe): Innovation in High-Performance Polymers, Specialty Chemicals, and Advanced Ceramics

Germany plays a central role in shaping Europe’s advanced materials market, driven by world-class engineering, specialty chemical leadership, and sustainability-oriented innovation. As part of Europe’s push toward decarbonization and supply-chain resilience, German industry remains at the forefront of bio-based and circular-material technologies. Companies such as BASF SE are pioneering sustainable high-performance polymers, including the launch of a bio-based 3D printing filament in 2023, which enhances mechanical strength and supports eco-efficient manufacturing.

Germany's automotive, aerospace, and machinery sectors continue to invest in fiber-reinforced composites (FRCs) to achieve lightweighting goals and reduce CO₂ emissions in accordance with EU climate frameworks. At the same time, the region's economic-security strategy emphasizes reducing reliance on non-EU suppliers for specialty materials—unlocking new funding for R&D in engineered chemicals and critical raw materials. Germany also stands out in advanced ceramics R&D, where universities, Fraunhofer institutes, and industrial leaders are developing next-generation ceramic components for high-temperature processing, industrial furnaces, and semiconductor substrates. These innovations position Germany as Europe’s strongest hub for high-performance materials manufacturing.

Japan: Global Hub for Functional Materials, Battery Innovations, and Quantum-Ready Materials

Japan continues to be a global leader in functional materials, supported by decades of manufacturing excellence in electronics, automotive, and precision engineering. Japanese companies dominate critical semiconductor materials segments, including photoresists, CMP slurries, and high-purity specialty gases—making Japan an irreplaceable part of the global microelectronics value chain. The nation is also deeply invested in advanced battery materials, particularly for next-generation lithium-ion and all-solid-state batteries, which are essential for EV expansion and energy storage modernization.

Japan’s expertise in high-tech carbon fiber composites remains unmatched, supplying aerospace, high-speed rail, and industrial markets with some of the world’s strongest and lightest structural materials. The country is further accelerating investments in quantum materials, superconductors, and ultralow-defect crystals to strengthen its role in the emerging quantum computing ecosystem. This combination of functional materials excellence, battery technology leadership, and advanced R&D positions Japan as a strategic innovation center in the global advanced materials market.

South Korea: Advanced Displays, Semiconductor Specialty Materials, and Bio-Materials Expansion

South Korea’s advanced materials ecosystem is strongly aligned with its global leadership in semiconductors and premium display technologies. The country continues to invest heavily in next-generation OLED materials, flexible substrates, and high-barrier encapsulation films to maintain dominance in the high-end consumer electronics and automotive display sectors. In response to geopolitical supply-chain vulnerabilities, South Korean conglomerates are expanding capacity for domestic high-purity process chemicals and photoresists, strengthening national self-reliance in core semiconductor materials.

Beyond electronics, South Korea is scaling investments in bio-materials, tapping into opportunities in medical implants, biocompatible polymers, and advanced drug delivery systems. A notable trend is the integration of AI and materials informatics, where companies increasingly use machine learning to accelerate material discovery and optimization. This digital-materials strategy is enabling faster time-to-market for novel materials and creating a new competitive differentiator for South Korean manufacturers.

India: Rising Demand for Automotive, Defense, and Infrastructure-Ready Advanced Materials

India is witnessing rapid growth in advanced materials adoption, driven by automotive lightweighting needs, infrastructure modernization, and the expansion of domestic defense manufacturing. Under the Make in India initiative, the automotive sector is increasing the use of high-strength steels, aluminum alloys, and composites to meet stricter emissions and safety regulations. The country is also strengthening its domestic capability for aerospace-grade composites and specialty alloys, supported by public-private partnerships that are accelerating the development of indigenous defense platforms.

Infrastructure and urban development are fueling significant adoption of advanced construction materials, including high-performance cement formulations, flame-retardant chemicals, and specialty coatings for large-scale smart city projects. India is also making strategic investments in nanotechnology, with companies like Solar Industries expanding R&D into advanced nanomaterials and energetic materials for defense, mining, and commercial applications. This evolving ecosystem positions India as a fast-advancing participant in the global advanced materials market.

Advanced Materials Market Report Scope

Advanced Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$548.2 Billion

|

|

Market Size (2035)

|

$1194.5 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Product Type (Composites, Polymers, Ceramics, Metals & Alloys, Nanomaterials, Functional Materials), By Application (Aerospace & Defense, Automotive, Electrical & Electronics, Energy, Healthcare/Medical Devices, Industrial), By Form (Fibers & Fabrics, Powders & Particles, Resins & Polymers, Sheets & Films, Coatings, Preforms, Monomers), By Technology (Additive Manufacturing, Materials Informatics, Surface Engineering, Process Technologies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, DuPont de Nemours Inc., 3M Company, Hexcel Corporation, Covestro AG, Toray Industries Inc., Kyocera Corporation, Solvay SA, Materion Corporation, Evonik Industries AG, Morgan Advanced Materials plc, Teijin Limited, Arkema S.A., Corning Inc., Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Materials Market Segmentation

By Product Type

- Composites (Carbon Fiber, Glass Fiber, Aramid, Metal Matrix, Ceramic Matrix)

- Polymers (High-Performance Plastics, Engineering Plastics, Bio-based Polymers, Elastomers)

- Ceramics (Technical Ceramics, Structural Ceramics, Electronic Ceramics)

- Metals & Alloys (Titanium Alloys, Nickel-based Superalloys, High-Strength Steel)

- Nanomaterials (Graphene, Carbon Nanotubes (CNTs), Quantum Dots, Nanoparticles)

- Functional Materials (Smart Materials, Energy Materials, Coatings & Films, Electronic Chemicals)

By Application

- Aerospace & Defense

- Automotive

- Electrical & Electronics

- Energy

- Healthcare/Medical Devices

- Industrial

By Form

- Fibers & Fabrics

- Powders & Particles

- Resins & Polymers

- Sheets & Films

- Coatings

- Preforms

- Monomers

By Technology

- Additive Manufacturing

- Materials Informatics

- Surface Engineering

- Process Technologies

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Advanced Materials Industry

- BASF SE

- DuPont de Nemours, Inc.

- 3M Company

- Hexcel Corporation

- Covestro AG

- Toray Industries, Inc.

- Kyocera Corporation

- Solvay SA

- Materion Corporation

- Evonik Industries AG

- Morgan Advanced Materials plc

- Teijin Limited

- Arkema S.A.

- Corning Inc

- Huntsman Corporation

*- List not Exhaustive

Research Coverage – Advanced Materials Market

This report by USDAnalytics investigates the Global Advanced Materials Market through a deeply analytical, decision-oriented lens, examining how breakthroughs in materials science, policy frameworks, supply-chain restructuring, and capital allocation are reshaping high-performance materials ecosystems worldwide. The analysis reviews critical innovation pathways across composites, polymers, ceramics, metals, nanomaterials, and functional materials, while highlighting how AI-driven materials discovery, ESG enforcement, and nationalization of strategic supply chains are redefining competitive advantage. This report highlights recent strategic developments, investment flows, regulatory inflection points, and technology transitions that directly influence procurement strategies, manufacturing economics, and long-term growth positioning. Designed for industry executives, investors, R&D leaders, and procurement heads, this report is an essential resource for understanding where value is being created, which material categories are scaling fastest, and how advanced materials are enabling next-generation aerospace, semiconductor, EV, clean energy, and defense systems through 2035. Scope Includes-

- By Product Type: Composites (Carbon Fiber, Glass Fiber, Aramid, Metal Matrix, Ceramic Matrix); Polymers (High-Performance Plastics, Engineering Plastics, Bio-based Polymers, Elastomers); Ceramics (Technical, Structural, Electronic); Metals & Alloys (Titanium Alloys, Nickel-based Superalloys, High-Strength Steel); Nanomaterials (Graphene, CNTs, Quantum Dots, Nanoparticles); Functional Materials (Smart Materials, Energy Materials, Coatings & Films, Electronic Chemicals)

- By Application: Aerospace & Defense, Automotive, Electrical & Electronics, Energy, Healthcare/Medical Devices, Industrial

- By Form: Fibers & Fabrics, Powders & Particles, Resins & Polymers, Sheets & Films, Coatings, Preforms, Monomers

- By Technology: Additive Manufacturing, Materials Informatics, Surface Engineering, Process Technologies

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021–2024 with forecasts from 2025–2035.

- Company Coverage: Competitive analysis and profiles of 15+ leading global advanced materials companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.