The Biocompatible Coatings Market, valued at USD 46.3 billion in 2025, is projected to reach USD 129.1 billion by 2035, registering a robust CAGR of 10.8%. Growth is fueled by escalating demand for infection-resistant coatings, hemocompatible surfaces, corrosion-proof implant coatings, and next-generation tribological solutions required by medical device OEMs operating in cardiovascular, orthopedic, dental, and neurovascular markets.

The Biocompatible Coatings Market is undergoing accelerated transformation, driven by strategic M&A consolidation, advanced surface engineering partnerships, and the increasing adoption of anti-thrombogenic and bioresorbable coatings across medical devices. In November 2025, Covalon Technologies reported a strong financial milestone with 82% revenue growth and paid its first special dividend (C$0.15/share), signaling renewed financial stability and reinforcing the rising global demand for infection-management coatings and antimicrobial grafting platforms. During the same month, two major coatings M&A events reshaped the supply landscape: an all-stock merger between AkzoNobel and Axalta valued at USD 25 billion, and a major EUR 8.7 billion acquisition of BASF’s surface treatment and automotive coatings business by Carlyle and QIA, both affecting availability of high-performance coating precursors used in precision medical components.

Momentum toward advanced biocompatibility continued with a major announcement in February 2025, when Silq Technologies and NuSil formed a partnership integrating zwitterionic surface treatments into implant-grade silicone elastomers. The innovation directly targets infection reduction and fibrosis prevention, two of the industry’s most challenging long-term implant complications. Similarly, Avient’s November 2024 launch of biocompatible Colorant Chromatics Transcend PEEK compounds at MEDICA highlighted the rising demand for high-heat, chemically stable polymer coatings in surgical robotics and dental scalers, driven by miniaturization and repeated sterilization cycles. Meanwhile, Medeologix expanded its catheter-focused hydrophilic coating capabilities through a strategic partnership with Biocoat (Nov 2024), cementing hydrophilic coatings as essential for low-friction access, precision navigation, and procedural safety in interventional cardiology and neurology.

The industry is simultaneously seeing disruptive innovation in regenerative coatings and anti-thrombogenic systems. In October 2024, UPM Biomedicals introduced FibGel, the world’s first injectable nanocellulose hydrogel, enabling biodegradable, animal-free coating options for tissue repair and reconstructive medicine. Soon after, Hydromer (June 2024) launched HydroThrombX, a next-generation thromboresistant coating engineered to reduce platelet adhesion and clot formation on vascular access devices—addressing the high unmet need for coating platforms that guarantee hemocompatibility and long-term vessel safety. As medical devices become more complex and regulatory frameworks increasingly emphasize durability, surface chemistry, and biocompatibility, these innovations collectively position the sector for sustained growth through 2035.

Industry professionals increasingly seek coating platforms that deliver measurable performance improvements, including extended implant lifespan, reduced infection risk, low debris generation, and enhanced osseointegration. Buyers also evaluate coatings by their compliance with ISO 10993 biocompatibility, long-term in vivo stability, and compatibility with advanced substrates like 316L steel, Ti-alloys, CoCr, and resorbable magnesium implants. Performance statistics present that biocompatible coatings are no longer considered optional—they are integral to device safety, regulatory compliance, and competitive differentiation.

- Orthopedic implant longevity is being redefined: Glass-Like Carbon (GLC) coatings at 2.5 μm thickness can extend hip joint life expectancy to 50 years, compared to 10 years for uncoated joints.

- Ultra-low friction tribological coatings are reshaping load-bearing applications: TiNbC coatings deliver a friction coefficient of 1.6 and wear rate of 0.99×10⁻⁵ mm³·N⁻¹·m⁻¹, reducing particulate debris and revision surgery probability.

- High-performance cardiovascular coatings demonstrate excellent blood compatibility: PTX–PEG coatings applied on magnesium cardiovascular stents record hemolysis rates of just 0.6%, far below the <5% clinical threshold.

- Advanced scaffold coatings support superior bone growth: Trabecular tantalum’s 99 wt% purity and high surface energy drive unmatched osseointegration and cell adhesion, key for orthopedic and dental reconstruction.

- Corrosion-resistant coatings ensure implant safety: TiNbC applied via Cathodic Arc Evaporation (CAE) outperforms TiC and ZrC, offering superior protection against metal ion release from stainless steel substrates.

Standardization of HA/Bioactive Glass, Drug-Eluting Polymer Innovation, Antimicrobial Neuromodulation Coatings, and Conductive Bioelectronic Interfaces Reshape the Biocompatible Coatings Market

Trend 1: Hydroxyapatite and Bioactive Glass Coatings Become Standardized for Cementless Orthopedic Implant Fixation

A decisive industry movement toward standardized Hydroxyapatite (HA) and bioactive glass coatings is redefining the performance benchmarks for cementless orthopedic implants, especially hip and knee replacements. Regulatory bodies-including the FDA and ISO-now mandate precise crystallinity, coating purity, and adhesion strength thresholds to ensure reproducible osseointegration outcomes.

Current standards require:

- ≥90% HA phase purity and >62% crystallinity (per ISO 13779-2) to avoid premature dissolution of amorphous phases

- Controlled thickness ranges-from 5–15 μm for thin-film applications to 20–40 μm for thicker plasma-sprayed layers optimized for mechanical anchoring

- Minimum tensile adhesion strength of 15–22 MPa (ASTM F1147-05), ensuring strong coating–substrate bonding under cyclic loading

- In vivo data confirming that HA-coated implants deliver 2× greater shear strength and 5× greater shear stiffness within four weeks compared to bare titanium

This standardization effort is pushing manufacturers toward more repeatable plasma-spray processes, optimized crystallinity profiles, and enhanced bioactive glass composites, fundamentally elevating implant performance and long-term stability.

Trend 2: Bioresorbable Polymer Drug-Eluting Coatings Gain Dominance in Coronary and Peripheral Vascular Devices

The shift from durable polymer DES (DP-DES) to bioresorbable polymer drug-eluting stents (BP-DES) is now accelerating as clinical data confirms lower inflammation, reduced late thrombosis risk, and improved arterial healing.

Key technical drivers include:

- Significantly reduced inflammation at 28 days compared to durable polymer coatings

- Highly engineered release profiles, exemplified by 4 μm ultrathin abluminal PDLLA coatings that elute everolimus over ~90 days before resorbing

- Randomized clinical trials validating non-inferiority of BP-DES for one-year TLF outcomes compared to top-performing DP-DES

- Ongoing preference for sirolimus and sirolimus analogs due to their wide therapeutic index and compatibility with hydrophobic polymer matrices

The move toward fully bioresorbable platforms is addressing long-standing concerns surrounding chronic polymer exposure and late-stage vascular reactions, positioning bioresorbable coatings as the new standard for modern stent platforms.

Opportunity 1: Antimicrobial, Anti-Biofilm Biocompatible Coatings for Neuromodulation and Deep Brain Stimulation Devices

Implantable neuromodulation technologies-including Deep Brain Stimulation (DBS) systems and spinal cord stimulators-face increasing clinical scrutiny due to the persistent challenge of device-associated infections. This creates a high-value opportunity for biocompatible antimicrobial coatings engineered to resist biofilm formation without relying on systemic drug release.

High-impact innovation areas include:

- Non-fouling polymeric coatings that prevent early protein adsorption and microbial anchoring

- Non-eluting antimicrobial strategies, incorporating immobilized silver nanoparticles or quaternary ammonium compounds to avoid antibiotic resistance escalation

- Biofilm-disruption mechanisms targeting the initial adhesion phase where bacteria transition into protective microcolonies

- Surface-modified polymers designed to retain electrical function and maintain neural signal fidelity, a prerequisite for neuromodulation devices

As neuromodulation expands into Parkinson’s disease, epilepsy, pain management, and closed-loop neurostimulation, the demand for infection-resistant biocompatible coatings will intensify, opening a premium growth segment.

Opportunity 2: Conductive Polymer Coatings (PEDOT:PSS) for High-Fidelity Bioelectronic Medicine Interfaces

Bioelectronic medicine-spanning neural interfaces, vagus nerve stimulators, retinal implants, and implantable biosensors-requires electrode surfaces that combine mechanical compliance with advanced electrical performance. PEDOT:PSS conducting polymer coatings are emerging as a transformative solution due to their ability to reduce impedance, increase charge transfer, and improve long-term biocompatibility.

Technical advantages include:

- >2× improvement in impedance and charge injection capacity using PEDOT:PSS eutectogels versus unmodified electrodes

- Substantial increases in CIC, enabling safer and more effective neural stimulation with reduced tissue damage

- Corrosion prevention, as PEDOT:PSS protects platinum and gold electrodes from dissolution under prolonged electrical load

- Superior mechanical compliance, reducing chronic foreign body response by better matching the softness of neural tissue

These properties allow PEDOT:PSS coatings to unlock new capabilities in recording precision, stimulation efficiency, and long-term device stability-critical for next-generation implantable bioelectronics.

Biocompatible Coatings Market Share Analysis

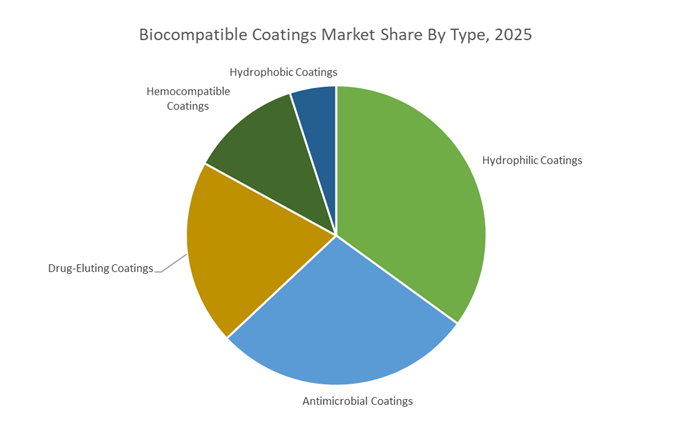

Market Share by Type/Function: Hydrophilic Coatings Lead Through Superior Lubricity, Safety Benefits, and Enabling Role in Minimally Invasive Procedures

Hydrophilic coatings command the leading 35% share of the Biocompatible Coatings Market, driven by their unrivaled ability to reduce friction and enhance device performance in minimally invasive medical procedures. When activated by moisture, these coatings form a hydrated hydrogel layer that dramatically lowers the coefficient of friction—often by up to 70% compared to uncoated catheters and guidewires—which is essential for navigating narrow, tortuous anatomical pathways with precision and minimal tissue trauma. Their dominance reflects a fundamental clinical requirement: to improve safety, maneuverability, and procedural efficiency in interventions where device–tissue interaction is constant and high-risk. Hydrophilic coatings are indispensable in angioplasty, neurovascular interventions, urology, and other catheter-based procedures, where reduced friction not only improves control but also minimizes complications such as vessel dissection or perforation. Furthermore, their ability to reduce irritation and trauma in applications like urinary catheterization directly supports better patient outcomes and lowers the incidence of Catheter-Associated Urinary Tract Infections (CAUTIs)—a major clinical and economic burden. As global healthcare systems expand their adoption of minimally invasive procedures, hydrophilic coatings remain the dominant functional coating class, supported by strong evidence of improved biocompatibility, reduced procedural risk, and enhanced clinician ergonomics.

Market Share by Application: Cardiovascular Devices Dominate Through High Procedure Volumes, Hemocompatibility Requirements, and Precision Navigation Needs

Cardiovascular devices represent the largest 40% share of the Biocompatible Coatings Market, driven by the enormous global volume of interventional cardiology and vascular procedures and the uncompromising performance demands placed on devices operating within the circulatory system. With cardiovascular disease remaining the leading cause of mortality worldwide, millions of PCI procedures and vascular interventions are performed each year, each requiring multiple coated devices—including guidewires, balloon catheters, drug-eluting stents, and delivery systems. This high procedural throughput alone creates sustained, large-scale demand for advanced biocompatible coatings. The segment’s leadership is further reinforced by the stringent hemocompatibility requirements in cardiovascular applications, where coatings must prevent platelet adhesion, protein deposition, and thrombogenic responses to reduce the risk of stent thrombosis and restenosis—two of the most critical complications in vascular interventions.

Moreover, the anatomical complexity of coronary and neurovascular pathways necessitates devices with exceptional “trackability” and “pushability,” characteristics that depend heavily on high-performance hydrophilic coatings. These coatings enable clinicians to steer devices through extremely narrow, curved, and diseased vessels with precision, reducing procedural time and improving therapeutic outcomes. As cardiovascular care continues to shift toward minimally invasive, catheter-based approaches—supported by rising rates of aging populations, chronic disease, and expanded access to interventional cardiology—the need for biocompatible, lubricious, and hemocompatible coatings ensures that cardiovascular devices remain the dominant application segment in this market.

Country Analysis: Global Biocompatible Coatings Development Hubs

United States – Leadership in Hydrophilic, Thromboresistant, and Parylene Biocompatible Coatings for Advanced Medical Devices

The United States remains the world’s most influential market for biocompatible coatings due to its concentration of major cardiovascular, neurovascular, and implantable device manufacturers. The country’s innovation trajectory is strongly shaped by high-performance hydrophilic coatings, thromboresistant polymer systems, and specialized parylene deposition technologies, all of which support the production of next-generation minimally invasive medical devices. In March 2024, SurModics, Inc. introduced a breakthrough polymer coating engineered to significantly reduce thrombosis risk, directly targeting critical needs in cardiovascular implants and vascular intervention systems. This milestone underscores the U.S. industry’s commitment to reducing adverse events and enhancing long-term implant safety.

SurModics further strengthened its leadership with the October 2023 commercial launch of Preside™, a next-generation hydrophilic coating designed for exceptional lubricity and ultra-low particulate generation, addressing safety mandates for catheter-based neurovascular and peripheral intervention devices. Complementing polymer innovation, Specialty Coating Systems (SCS) continues to dominate the global Parylene coating segment, offering pinhole-free, ultra-thin layers ideal for microelectronics, neuromodulation implants, and wearable biosensors. Regulatory alignment is also accelerating market maturity—most notably the FDA’s 2024 classification of hydrophilic re-coating solutions as Class II, mandating standardized performance testing and reinforcing U.S. leadership in biocompatible coating safety, compliance, and scalability.

Germany / European Union – MDR Compliance Driving Ceramic, Antimicrobial, and Orthopedic Coating Innovation

The European Union remains a powerhouse in biocompatible coating development, with demand largely governed by the stringent Medical Devices Regulation (MDR) fully enforced in 2024. The MDR dramatically strengthens requirements for biocompatibility testing, durability validation, long-term implantation safety, and clinical documentation, forcing manufacturers to adopt proven, high-quality coatings to maintain device certification and market access. This regulatory landscape is catalyzing rapid innovation across ceramic coatings (TiO₂, hydroxyapatite), antimicrobial coatings, and hydrogel-based biomaterials, especially for orthopedic and dental implants where long-term osseointegration and wear resistance are critical.

To meet rising regional demand, Biocoat expanded its European manufacturing footprint with a new hydrophilic coating facility in Copenhagen (September 2025), enhancing supply chain proximity for catheter, ophthalmic, and minimally invasive device manufacturers. Meanwhile, the EU is seeing significant diversification in materials science: UPM Biomedicals’ FibGel, launched in October 2024, introduces a sustainable nanocellulose hydrogel that offers biocompatibility, injectability, and animal-free formulation—ideal for regenerative medicine, soft tissue repair, and wound-care markets. Major German manufacturers continue to prioritize ceramic and antimicrobial coatings for orthopedic implants, coinciding with Europe’s growing aging population and expansion of reconstructive surgical procedures.

South Korea – National AMR Policy and High-Tech PECVD/PVD Advancements Fueling Antimicrobial Coating Adoption

South Korea is emerging as a key innovation cluster for antimicrobial, antiviral, and infection-control coatings, driven by national healthcare policies aimed at combating Antimicrobial Resistance (AMR). Government-led public health initiatives have intensified the need for protective coatings across reusable surgical instruments, hospital furniture, dental tools, and high-contact clinical environments. This regulatory pressure has accelerated the adoption of silver-nanoparticle-based antimicrobial coatings, copper-infused surfaces, and advanced hydrophilic antimicrobial films.

The country also benefits from its globally competitive high-tech manufacturing sector, with domestic firms investing heavily in plasma-enhanced chemical vapor deposition (PECVD) and physical vapor deposition (PVD) technologies. These processes enable ultra-uniform, durable thin films—such as Titanium Nitride (TiN)—that enhance wear resistance, sterilization durability, and surface safety for surgical tools and internal medical components. South Korea’s strong alignment between government policy, materials research institutes, and medical device manufacturers positions it as a rapidly expanding hub for clinical antimicrobial coatings with broad applicability across hospital, diagnostic, and surgical settings.

Canada – Dual-Functional Antimicrobial and Anti-Inflammatory Coatings Strengthening Wound Care and Surgical Applications

Canada is carving out a specialized niche in the Biocompatible Coatings Market through the development of dual-function therapeutic coatings that combine antimicrobial, anti-inflammatory, and wound-healing benefits. A leading example is Covalon Technologies Ltd., which introduced a novel coating formulation in early 2024 designed to enhance patient outcomes by providing both infection protection and inflammation control—an increasingly critical clinical requirement for wound dressings, chronic ulcer treatments, and post-surgical healing environments. This category of multifunctional coatings offers significant value to healthcare systems by reducing complications and improving recovery times.

Canadian companies also emphasize international commercialization strategies, often partnering with major global healthcare distributors to scale adoption across North America, Europe, and the Middle East. These partnerships reflect Canada’s strategic focus on intellectual property development, licensing platforms, and high-performance biomaterials, positioning the country as an important contributor to advanced wound care, catheter coatings, and surgical device coatings within the global biocompatible materials landscape.

Competitive Landscape: Global Leaders Driving Innovation in Biocompatible Coatings

The competitive environment in the Biocompatible Coatings Market is shaped by companies specializing in hydrophilic coatings, antimicrobial polymers, wear-resistant hard coatings, parylene deposition, bioresorbable materials, and advanced silicone surface treatments. Leadership is determined by proprietary chemistry, regulatory expertise, IP portfolios, and integration with medical device OEM workflows.

Covalon Technologies focuses heavily on photo-polymerized coating platforms that integrate antimicrobial agents and infection-management functionality into vascular access devices. With reported revenue growth of 82% to USD 33 million and its first special dividend in Nov 2025, the company demonstrates strong financial momentum. Covalon holds 88 granted patents, securing competitive advantage in antimicrobial chemistry, coating reactors, and polymer grafting technologies. Its strategic emphasis is on reducing Healthcare Associated Infections (HAIs), particularly through products like IV Clear and VALGuard, which combine transparent infection control and skin-friendly adhesive chemistry.

Surmodics is a global leader in surface modification technologies, offering hydrophilic, controlled-drug delivery, and anti-thrombogenic coatings widely used in cardiovascular, neurovascular, and ophthalmic devices. Its coatings enhance lubricity, reduce device insertion force, and minimize thrombogenic risk—critical for precision catheters and drug-coated balloons. The company maintains strong relationships with OEMs, including a distribution partnership with Cook Medical, and continues to expand its portfolio to support minimally invasive and next-generation device architectures, leveraging deep R&D capabilities in polymer chemistry and drug-eluting formulations.

Through the acquisition of DSM Biomedical, Covestro commands a powerful portfolio in bioresorbable materials, polyurethane coatings, silicone hybrids, and advanced biomaterials used in orthopedics, cardiovascular implants, and soft tissue repair. DSM Biomedical added approximately EUR 1 billion in revenue, broadening Covestro’s presence in medical OEM supply chains. The company is strongly focused on reducing device rejection, improving long-term biocompatibility, and creating wear-resistant polymers, while aligning with its corporate commitment to achieve Scope 1 and 2 climate neutrality by 2035, making sustainability a key competitive pillar.

SCS specializes in Parylene coatings (C, N, HT) applied through advanced CVD processes, producing uniform, pinhole-free barrier layers critical for implantables, microelectronics, wearables, and neurostimulation devices. Parylene’s exceptional moisture resistance and dielectric properties make it indispensable for precision medical systems requiring long-term stability inside the human body. With a global network of ISO- and FDA-compliant coating facilities, SCS maintains strong credibility among Class II and Class III medical device manufacturers, providing coatings that meet the most stringent performance and regulatory standards.

Hydromer is a specialized provider of hydrophilic, lubricious, and thromboresistant coatings for minimally invasive surgical tools, catheters, guidewires, and introducers. Its HydroThrombX product, launched in June 2024, introduces a breakthrough in platelet-adhesion reduction and clot prevention, optimized for vascular access applications. Hydromer’s coating systems rely on UV and thermal curing technologies to permanently bond polymer coatings to diverse substrates, enabling smooth insertion, lower friction, and more precise device control. The company collaborates closely with OEMs to deliver customized, substrate-specific coating solutions that meet evolving clinical and performance requirements.

Biocompatible Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$46.3 Billion

|

|

Market Size (2035)

|

$129.1 Billion

|

|

Market Growth Rate

|

10.8%

|

|

Segments

|

By Type/Function (Hydrophilic Coatings, Antimicrobial Coatings, Thromboresistant/Hemocompatible Coatings, Drug-Eluting Coatings, Hydrophobic Coatings), By Material Class (Polymers, Ceramics, Metals, Composites), By Application (Cardiovascular Devices, Orthopedic Implants, Neurology Devices, Ophthalmic Devices, Surgical & Diagnostic Tools), By Coating Technique (Dip Coating, Spray Coating, Chemical Vapor Deposition, Plasma Enhanced CVD, Sol-Gel Processing, UV Curing)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SurModics Inc., DSM Biomedical, Covalon Technologies Ltd., Specialty Coating Systems Inc., Biocoat Incorporated, Hydromer Inc., Evonik Industries AG, Hemoteq AG, AST Products Inc., AdvanSource Biomaterials Corporation, Materion Corporation, Medtronic Plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biocompatible Coatings Market Segmentation

By Type/Function

- Hydrophilic Coatings

- Antimicrobial Coatings

- Thromboresistant/Hemocompatible Coatings

- Drug-Eluting Coatings

- Hydrophobic Coatings

By Material Class

- Polymers

- Ceramics

- Metals

- Composites

By Application

- Cardiovascular Devices

- Orthopedic Implants

- Neurology Devices

- Ophthalmic Devices

- Surgical & Diagnostic Tools

By Coating Technique

- Dip Coating

- Spray Coating

- Chemical Vapor Deposition (CVD)

- Plasma Enhanced Chemical Vapor Deposition (PECVD)

- Sol-Gel Processing

- UV Curing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Biocompatible Coatings Manufacturers

- SurModics, Inc.

- DSM Biomedical (Royal DSM)

- Covalon Technologies Ltd.

- Specialty Coating Systems, Inc. (SCS)

- Biocoat Incorporated

- Hydromer, Inc.

- Evonik Industries AG

- Hemoteq AG

- AST Products, Inc.

- AdvanSource Biomaterials Corporation

- Materion Corporation

- Medtronic Plc

*- List not Exhaustive