Biomaterials Market Overview: Rapid Scale-Up in Orthopedics, Dental and Regenerative Therapies

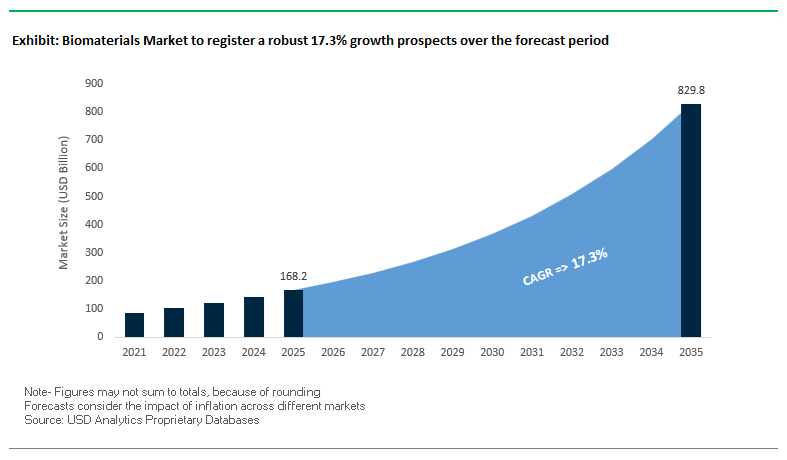

The global biomaterials market is projected to grow from USD 168.2 billion in 2025 to around USD 829.5 billion by 2035, registering a powerful CAGR of 17.3% (2025–2035). This expansion is underpinned by surging demand for orthopedic implants, dental implants, polymeric biomaterials, regenerative hydrogels, and tissue engineering scaffolds. For manufacturers and vendors, the market is increasingly driven by stringent mechanical performance, cytocompatibility, and controlled degradation requirements, particularly in load-bearing implants and long-term contact devices.

Advanced titanium alloys (e.g., Ti–6Al–4V) used in total hip replacement stems must now demonstrate fatigue life beyond 10 million cycles under ISO 7206 physiological loading conditions, pushing metal producers toward tighter process control and defect-free microstructures. On the dental side, the shift to sand-blasted and acid-etched (SLA) titanium surfaces delivering an Sa of 1–3 µm is becoming a benchmark for fast and reliable osseointegration. In parallel, polymeric biomaterials such as PEEK and medical-grade polyethylene must meet Grade 2 (mild reactivity) or better cytocompatibility, while bioresorbable hydrogels and 3D porous scaffolds are engineered for defined resorption windows (months to years) and pore sizes ≥100 μm to support vascularization and tissue regeneration.

Key market insights for biomaterials manufacturers and vendors

- Orthopedic and joint reconstruction OEMs are demanding titanium and cobalt-chrome biomaterials with fatigue life >10 million cycles for long-term, load-bearing hip and knee implants.

- Dental implant manufacturers increasingly specify SLA-treated titanium surfaces (Sa ~1–3 µm) to accelerate osseointegration and reduce early failure rates in premium implant lines.

- Polymer suppliers must deliver PEEK and medical-grade PE with cytocompatibility of Grade 2 or better, supporting long-term direct contact with human cells and tissues.

- Hydrogel and cartilage repair players design bioresorbable systems that maintain mechanical support for 3–6 months, followed by complete resorption within 1–2 years, aligning with clinical regeneration timelines.

- Tissue engineering scaffold providers are optimizing interconnected pore structures ≥100 μm, enabling robust vascularization and effective nutrient/waste transport in bone and soft-tissue regeneration.

Biomaterials Market Analysis: Capital Markets, Clinical Trials and Smart Materials Momentum

The global biomaterials industry is being reshaped by strong capital markets activity and late-stage clinical milestones, especially in regenerative medicine and cartilage repair. In December 2025, Regentis Biomaterials Ltd. began trading on the NYSE American (RGNT), signaling investor confidence in its GelrinC◦ hydrogel resorbable implant for knee cartilage repair and the broader regenerative biomaterials space. In the same month (December 2025), Thermo Fisher Scientific announced the acquisition of Clario Holdings Inc., expanding its capabilities in digitally driven clinical development—an ecosystem increasingly critical for streamlining regulatory approval of innovative biomaterials, tissue-engineered products, and implantable devices. Earlier in April 2025, Northern Illinois University (NIU) launched a state-of-the-art Biomaterials and Tissue Engineering Laboratory, highlighting the growing academic and R&D focus on functional biomaterials and advanced tissue engineering platforms.

Strategic partnerships and technology collaborations are further accelerating innovation in biobased and smart biomaterials. In mid-2025, Corbion N.V. expanded its partnership with a 3D bioprinting firm to optimize PLA-based bio-inks for customized tissue scaffolds, supporting the industrialization of 3D-printed regenerative solutions. In May 2025, PetVivo Holdings, Inc. and PiezoBioMembrane, Inc. entered a Master Services Agreement to co-develop piezoelectric nanofibers integrated into biocompatible biomaterials, targeting “smart” implants that couple mechanical stimuli with bioelectric responses. Meanwhile, Temple OrthoBiologics, launched in September 2024 as a spin-out from Temple Therapeutics, is focusing on orthopedic sports medicine biomaterials that prevent scar tissue formation, illustrating the trend toward highly targeted, indication-specific biomaterial platforms.

Commercialization of sustainable, bio-based materials is also gaining traction, extending biomaterials from strictly medical into consumer applications. In August 2025, Origin Materials announced the first commercial use of its bio-based PET bottle cap, demonstrating the scalability of carbon-negative biomaterials derived from wood chips into high-volume consumer goods. At the same time, Regentis Biomaterials reported in December 2025 that its pivotal FDA trial for GelrinC◦ had surpassed 50% enrollment, marking a critical step toward U.S. regulatory approval. Collectively, these developments underline a biomaterials market where regenerative hydrogels, degradable polymers, smart nanofiber systems, and biobased plastics are converging with digital clinical platforms and advanced manufacturing to drive double-digit growth through 2035.

Next-Generation Regenerative and Antimicrobial Strategies Driving High-Performance Biomaterials Adoption

Market Trend 1: Rapid Clinical Adoption of Immunomodulatory Biomaterials Enabling Pro-Healing Tissue Regeneration

A defining trend in the Biomaterials Market is the transition from inert structural implants toward immunomodulatory biomaterials engineered to actively shape the host immune response. Advanced scaffold chemistries—including surface-tethered IL-4, anisotropic micro-topographies, and bioactive hydrogel matrices—are being shown in vivo to increase the M2/M1 macrophage ratio by 3× to 5×, a critical prerequisite for orchestrating regenerative healing rather than chronic inflammation. These materials also demonstrate ≥50% reductions in pro-inflammatory cytokines (TNF-α, IL-6) while upregulating anti-inflammatory mediators such as IL-10 and TGF-β, reinforcing their role in controlled immunomodulation during early healing.

This immune-centered design approach has delivered unprecedented biological outcomes: in critical-sized bone defect models, optimized immunomodulatory hydrogels achieve ≈93% bone restoration, far outperforming passive biomaterial controls. Moreover, implants fostering M2 polarization show ≥40% reduction in fibrous capsule thickness, which directly improves long-term integration and reduces foreign body reaction risks. With tissue engineering, orthopedics, neurology, and soft-tissue reconstruction increasingly requiring regenerative cues, immunomodulatory biomaterials are becoming core assets in next-generation clinical implant design.

Market Trend 2: Convergence of Biomaterials with Digital Health Platforms for Continuous, Data-Driven Patient Monitoring

Another high-impact trend reshaping the Biomaterials Market is the integration of biomaterial-based sensing systems with digital health platforms, enabling real-time physiological monitoring and automated therapeutic response. Modern implantable and wearable biosensors use advanced hydrogel membranes and selective polymer coatings to achieve MARD ≤9%, matching the accuracy required for clinical continuous glucose monitoring (CGM). Beyond glucose, biomaterial-infused sensors enable ≤1-minute response time to analyte changes, supporting rapid intervention in hypoxia, infection, ischemia, and metabolic instability.

These intelligent systems also power pH-sensitive, stimulus-responsive drug delivery, where polymer matrices release therapeutic payloads in response to acidity typical of inflamed or tumor microenvironments, achieving precise burst-release profiles that align with pathological triggers. In parallel, flexible biomaterial-based wearables—such as smart patches and textile-integrated sensors—transmit biomarkers including lactate, cortisol, and antibodies via Bluetooth over ≥10 meters, enabling continuous telemedicine workflows. This biomaterial–IoT convergence is accelerating adoption in chronic disease management, oncology, wound monitoring, rehabilitation, and personalized medicine ecosystems.

Market Opportunity 1: Engineering Phage- and Enzyme-Functionalized Biomaterials to Combat Implant-Associated Infections

The rise in antibiotic-resistant pathogens is creating a high-value opportunity for phage-functionalized and enzyme-functionalized biomaterials designed to eradicate biofilms on implants. In early clinical datasets for prosthetic joint infections (PJIs), phage therapy has achieved 78%–83% infection remission at ≥12-month follow-up—an unprecedented outcome for multidrug-resistant infections. Biofilm-protected bacteria typically show up to 1,000× higher MIC, but phage-functionalized surfaces disrupt biofilm matrices, drastically lowering the effective MIC and enabling therapeutic penetration.

Lytic phages and lysins covalently immobilized on implant surfaces can deliver ≥99.9% (3-log) bacterial reduction within hours of contact, demonstrating highly selective antimicrobial potency. Their mechanism of action bypasses traditional antibiotic pathways, meaning no observed cross-resistance in strains already resistant to standard drugs. This positions phage-functionalized biomaterials as a transformative opportunity for orthopedics, cardiovascular implants, catheters, dental implants, and surgical meshes—markets where infection prevention directly improves outcomes and reduces hospital readmission costs.

Market Opportunity 2: Scaling Plant-Derived and Recombinant Protein Biomaterials for Sustainable, High-Purity Medical Manufacturing

A major emerging opportunity in the Biomaterials Market lies in the industrial-scale production of plant-derived and recombinant protein biomaterials, which offer unmatched purity, sustainability, and biofunction customization. Recombinant human collagen, engineered elastin, and spider silk analogs achieve ≥99% purity, eliminating risks associated with mammalian pathogens and immunogenic contaminants inherent in animal-derived sources. Unlike natural extraction processes that exhibit variability in hormonal and biochemical composition, recombinant systems show <1% batch-to-batch variation, ensuring consistent biomechanical and bioactive performance in regulated medical devices.

Sequence-level programmability allows insertion of cell-binding motifs (e.g., RGD), enzyme-cleavable domains, and mechanical-tuning segments, enabling tailored materials for wound care, ophthalmology, cardiovascular grafts, and aesthetic injectables. Meanwhile, microbial fermentation and plant-expression platforms can scale production volumes 10× to 100× faster than animal sourcing, dramatically improving supply reliability. As healthcare systems prioritize sustainability and ethical sourcing, recombinant and plant-derived biomaterials are positioned to become a dominant supply chain for next-generation medical implants, scaffolds, hydrogels, and drug-delivery systems.

Biomaterials Market Share Analysis

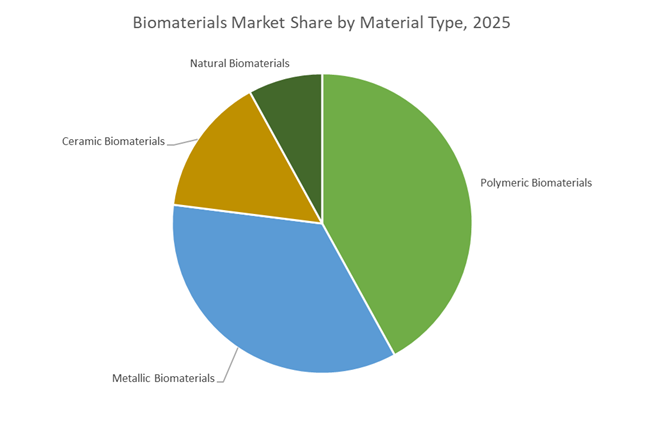

Market Share by Material Type: Polymeric Biomaterials Lead Due to Versatility, Biocompatibility, and High-Volume Clinical Adoption

Polymeric biomaterials hold the largest share of the global biomaterials market—approximately 42% in 2025—because they offer unmatched flexibility in design, tunable degradation profiles, and broad applicability across both implantable and disposable medical devices. Their ability to be engineered with precise mechanical, chemical, and biological properties enables polymers such as UHMWPE, PEEK, PLA, PLGA, silicone, and polyurethane to fulfill roles ranging from load-bearing orthopedic implants to soft, flexible cardiovascular components and high-volume surgical consumables. Bioresorbable polymers continue to expand adoption through applications in sutures, fixation devices, wound dressings, and controlled-release drug delivery systems, where tailored degradation kinetics eliminate secondary surgical procedures. Meanwhile, high-strength engineering polymers like PEEK increasingly replace metals in spinal and trauma implants due to their radiolucency, corrosion resistance, and bone-mimicking modulus. Polymers are also foundational to emerging regenerative medicine and tissue engineering applications, where they enable 3D-printed scaffolds with complex architectures and biologically compatible surfaces. This breadth of functionality—not matched by metallic, ceramic, or natural biomaterials—ensures polymeric biomaterials remain the dominant material type across high-growth medical markets.

Market Share by End-Product Application: Orthopedic Devices & Orthobiologics Dominate Due to Rising Surgical Volumes and Material-Intensive Procedures

The Orthopedic Devices & Orthobiologics sector accounts for nearly 30% of the global biomaterials market, reflecting the substantial and growing clinical burden of musculoskeletal disorders and the material-intensive nature of orthopedic implant systems. Joint replacements, spinal fusion procedures, and trauma fixation surgeries require large volumes of advanced biomaterials—ranging from UHMWPE articulating surfaces and PEEK cages to titanium alloy screws, cobalt-chrome femoral components, and PMMA bone cement—making orthopedics the most resource-intensive medical application. The steady rise in osteoarthritis incidence, sports-related injuries, obesity-linked joint degeneration, and global population aging creates sustained demand for hip, knee, shoulder, and spine implants. Simultaneously, orthobiologics—including collagen scaffolds, bioactive ceramics, demineralized bone matrices, and PLA-based resorbable graft substitutes—are transforming surgical outcomes by promoting natural bone regeneration. With over 1.7 billion people worldwide affected by musculoskeletal conditions, orthopedic care remains a clinical and economic priority. This large patient base, combined with continuous innovations in implant materials, surface coatings, and regenerative technologies, ensures orthopedics maintains its position as the largest and most influential application segment in the biomaterials market.

Country Analysis: Global Drivers in Biomaterials Development

United States: Acceleration of Regenerative Medicine, Nanofiber Platforms, and 3D Bioprinting-Enabled Personalized Implants

The United States remains the global epicenter of high-value biomaterials innovation, supported by strong venture capital inflows, advanced FDA regulatory pathways, and a dense ecosystem of academic research centers and medical device manufacturers. A major milestone in 2025 was the launch of Northern Illinois University’s Biomaterials and Tissue Engineering Laboratory, which strengthens national capabilities in mammalian cell culture, extracellular matrix (ECM) modeling, and regenerative biomaterial prototyping. These developments directly support the next generation of stem-cell compatible scaffolds, peptide-enhanced hydrogel biomaterials, and immune-modulatory implant coatings. Complementing this academic progress, the launch of Temple OrthoBiologics (September 2024) marks a new commercial focus on preventing scar tissue formation in orthopedic joints—an emerging indication where advanced bioactive polymer composites, growth-factor-loaded matrices, and anti-fibrotic biomaterials represent key therapeutic differentiators.

The U.S. is also at the forefront of functional biomaterial systems incorporating nanofibers, piezoelectric materials, and bioresorbable composites. The 2025 Master Services Agreement between PetVivo Holdings and PiezoBioMembrane Inc. underscores rising demand for ECM-mimicking biomaterials that can stimulate tissue repair through mechano-electrical signaling. The orthopedic market continues consolidating, with Zimmer Biomet’s acquisition of Paragon 28 (April 2025) strengthening leadership in custom foot-and-ankle implants. Meanwhile, 3D-printed biomaterial implants grew 28% in 2025, driven by U.S. manufacturers adopting porous Titanium lattice structures and advanced polymeric filaments to deliver personalized implants with superior osteointegration. Collectively, these advancements reinforce the United States’ position as a global powerhouse in biomaterials research, commercialization, and implant innovation.

European Union (Germany, UK, France): Breakthroughs in Drug Delivery, Circular Biomaterials, and Bioresorbable Cardiovascular Technologies

Europe’s biomaterials ecosystem is heavily shaped by its strong academic research networks, sustainability mandates, and leadership in drug-delivery technologies. The 12th Galenus International Workshop (Portugal, March 2025) highlighted Europe’s rapidly advancing capabilities in nanomedicine-enabled targeted drug delivery, emphasizing engineered polymer nanoparticles, lipid-polymer hybrids, and biomaterial vectors designed for cell, gene, and nucleic acid therapies. These innovations help position Europe at the forefront of precision therapeutic delivery, where biomaterial-based encapsulation, controlled-release platforms, and bioresponsive polymers are essential.

EU-wide initiatives are also accelerating the adoption of sustainable, naturally derived biomaterials as part of the region’s circular bio-economy strategy. Research groups across Germany, France, the UK, and the Nordics are exploiting unconventional protein and polysaccharide sources—such as fish-waste collagen, fungal chitosan, and insect-derived biopolymers—to replace traditional synthetic polymers in wound care, tissue scaffolds, and surgical meshes. On the commercial front, Teleflex’s acquisition of BIOTRONIK’s vascular intervention unit (February 2025) reinforces the EU’s strategic shift toward bioresorbable polymer scaffolds and drug-eluting cardiovascular implants, responding to demand for minimally invasive, long-life interventions. Supporting the next generation of biomaterial breakthroughs, the European Society for Biomaterials (ESB) continues advancing research, including award-winning work on AI-enhanced biomaterial design, strengthening Europe’s position as a leader in computational biomaterials science and clinical translation.

China: Regulatory Reforms, High-End Medical Device Prioritization, and Advanced Implant Development

China is rapidly advancing its biomaterials market through aggressive regulatory modernization and increased emphasis on high-end medical device innovation. The National Medical Products Administration (NMPA) released an Announcement on Optimizing Full Lifecycle Regulation (July 2025) specifically aimed at accelerating approval pathways for novel biomaterial-based medical devices. These reforms prioritize next-generation implants utilizing flexible neural electrodes, bioengineered tissues, and gene-modified biomaterial platforms, signaling a national shift toward cutting-edge applications in neurology, orthopedics, cardiovascular therapy, and reconstructive surgery.

To support domestic manufacturing security, the NMPA also issued revised Good Manufacturing Practice (GMP) standards (November 2025; effective 2026), mandating higher quality control for both synthetic and natural biomaterials, aligning China’s regulatory framework with international Quality Management Systems (QMS). Chinese policy initiatives explicitly highlight biomaterials as a strategic domain for achieving self-sufficiency, especially in complex implant categories such as brain–computer interface substrates, degradable vascular implants, and soft-tissue regenerative matrices. As China increasingly integrates advanced biomaterials into its high-end medtech portfolio, the country is emerging as a major innovation hub with growing global influence.

South Korea: Commercial Expansion in Dental Biomaterials and Orthopedic Regenerative Solutions

South Korea’s biomaterials market is expanding rapidly due to its strong medical manufacturing capabilities and high procedural volumes in dentistry and orthopedics. The country is a recognized leader in Dental Bone Graft Substitutes (DBGSs), with substantial demand for synthetic hydroxyapatite, β-TCP bioceramics, collagen membranes, and bioresorbable polymer barriers driven by the nation’s high rate of dental implant procedures. Companies such as Genoss, through products like the OSTEON™ line, are driving innovation in synthetic bone materials designed for enhanced biocompatibility, osseointegration, and structural stability in oral surgery.

South Korea’s strategic partnerships further reinforce its biomaterials leadership. In February 2025, J&J MedTech signed an exclusive agreement with CG Bio to distribute NOVOSIS, a next-generation bone graft solution marketed for spinal and trauma care across key Asian markets. This collaboration demonstrates global confidence in Korean biomaterial manufacturing standards and regenerative technology expertise. Additionally, South Korea’s fast-growing orthopedic implants sector is increasingly adopting 3D printing and robotic-assisted surgery, which requires precise, high-strength, and bioresorbable materials for patient-specific implant geometries. These advancements position South Korea as a crucial commercial hub for high-performance dental and orthopedic biomaterials across the Asia-Pacific region.

Competitive Landscape of the Global Biomaterials Market

The global biomaterials market is characterized by a mix of orthopedic and spine device OEMs, specialty polymer suppliers, advanced metals producers, and biobased polymer innovators. Major players such as Zimmer Biomet and Stryker dominate the implantable device value chain, specifying stringent performance requirements for metallic and polymeric biomaterials. In parallel, Evonik Industries, Carpenter Technology, and Corbion provide critical upstream inputs—from high-purity metallic alloys and resorbable polymers to PLA and PLGA systems for sutures, scaffolds and drug delivery. This combination of clinical OEMs and material specialists is driving innovation in fatigue-resistant metals, porous and 3D-printed structures, resorbable polymers, and bio-based biomaterials, anchoring long-term market growth.

Zimmer Biomet: Advanced Metallic and Polymeric Biomaterials for Joint Reconstruction

Zimmer Biomet is a global leader in musculoskeletal health, leveraging both metallic and polymeric biomaterials across its extensive joint reconstruction portfolio. The company manufactures total hip, knee and shoulder replacement systems that rely heavily on titanium and cobalt-chrome alloys combined with ultra-high molecular weight polyethylene (UHMWPE) as bearing surfaces. Zimmer Biomet has been a pioneer in highly cross-linked UHMWPE (HXLPE) liners, which can reduce wear particle generation by more than 90% versus conventional polyethylene, thereby extending implant survivorship in demanding orthopedic applications. Strategically, the company is expanding its orthobiologics offerings, incorporating natural biomaterials such as demineralized bone matrix (DBM) and growth-factor carriers to enhance bone healing and fusion. It is also at the forefront of additive manufacturing, using 3D printing to produce porous titanium biomaterials with tailored pore structures that improve osseointegration and reduce stress shielding.

Stryker: Porous Titanium and PEEK Biomaterials for Spine and Trauma

Stryker Corporation is a key multinational medical technology company with a strong focus on orthopedic implants, spine systems, and surgical technologies. Its product portfolio spans trauma, spine, and joint replacement devices, where materials such as titanium and PEEK (polyetheretherketone) are widely used for spinal cages and fixation plates. Stryker is particularly known for its Tritanium◦ porous titanium biomaterial, produced via additive manufacturing to create an interconnected pore architecture that closely mimics cancellous bone, enhancing biological fixation. In spine, Stryker is a dominant player by leveraging PEEK’s radiolucency and bone-like modulus, which reduces stress shielding and imaging artifacts compared with metallic implants. The company is also expanding its range of bioabsorbable fixation devices based on polymers like PLGA, engineered to provide temporary mechanical support and fully degrade over time, eliminating the need for secondary removal surgeries.

Evonik Industries: Resorbable Polymers and PEEK for Next-Generation Implants

Evonik Industries AG plays a pivotal role as a specialty chemicals provider to the medical device and pharmaceutical biomaterials value chain. Its portfolio includes high-performance polymeric biomaterials such as VESTAKEEP® PEEK for orthopedic implants and RESOMER◦ degradable polymers (PLGA, PCL, and related copolymers) used in sutures, drug delivery systems, and tissue engineering scaffolds. Evonik’s core strength lies in resorbable copolymers with customizable degradation profiles, enabling OEMs to tune implant life from weeks to several years, particularly in drug-eluting stents and resorbable fixation devices. The company is also a key enabler of 3D-printed medical devices, developing high-purity polymer powders for laser sintering and extrusion-based printing to create patient-specific porous implants. Recently, Evonik has partnered with biotech companies to optimize lipid nanoparticles (LNPs) as drug delivery vehicles, leveraging its polymer and formulation expertise to improve the stability and targeting of advanced RNA therapeutics—a fast-growing biomaterials-enabled segment.

Carpenter Technology: High-Strength Metallic Biomaterials for Implants

Carpenter Technology Corporation is a leading producer of high-performance specialty alloys that form the backbone of many orthopedic and cardiovascular implants. Its biomaterials portfolio covers medical-grade stainless steel (316L), titanium alloys, and cobalt-chrome alloys, all engineered for high strength and corrosion resistance in long-term implantable devices. Carpenter is also a major supplier of atomized metal powders with tight particle size distributions and high purity, optimized for metal 3D printing (powder bed fusion) of patient-specific implants and complex geometries. By providing vacuum-melted and electroslag-remelted (ESR) alloys, the company minimizes inclusions and maximizes fatigue strength, meeting the rigorous reliability requirements of permanent implants. Strategically, Carpenter is investing in next-generation biodegradable metals, such as magnesium-based alloys, which are designed to provide temporary fixation and gradually dissolve after bone healing, aligning with the trend toward bioresorbable metallic biomaterials.

Corbion: PLA-Based Bioresorbable Polymers for Sutures, Stents and Scaffolds

Corbion N.V. is a global specialist in biobased products, with a leading position in lactic acid and PLA (polylactide) biomaterials for bioresorbable medical applications. The company is a primary source of lactic acid monomers and high-purity PLLA, PDLA, and PLGA copolymers, which are widely used in bioresorbable sutures, vascular stents, and orthopedic fixation screws. Corbion’s vertically integrated production enables tight control over chiral purity, which directly influences the crystalline structure and degradation rate of its polymers, a critical factor for predictable implant performance. In tissue engineering, Corbion is a major supplier of materials for 3D bioprinting bio-inks and electrospun scaffolds, supporting regenerative medicine R&D worldwide. Strategically, the company is expanding the use of its bio-based and biodegradable polymers beyond traditional medical devices into sustainable packaging and high-value technical fibers, leveraging the growing demand for low-carbon, circular biomaterials solutions.

Biomaterials Market Report Scope

Biomaterials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$168.2 Billion

|

|

Market Size (2035)

|

$829.5 Billion

|

|

Market Growth Rate

|

17.3%

|

|

Segments

|

By Material Type (Metallic Biomaterials, Polymeric Biomaterials, Ceramic Biomaterials, Natural Biomaterials), By Origin (Synthetic Biomaterials, Natural Biomaterials), By Application (Orthopedic Devices & Orthobiologics, Cardiovascular Implants & Devices, Dental Implants & Regenerative Materials, Wound Healing & Surgical Biomaterials, Tissue Engineering & Regenerative Medicine, Plastic & Reconstructive Surgery)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Johnson & Johnson, Medtronic, Stryker, Zimmer Biomet, Royal DSM, Carpenter Technology, Evonik Industries, Becton Dickinson, Boston Scientific, Tegra Medical (TE Connectivity), Celanese Corporation, Nobel Biocare (Envista), Corbion, Geistlich Pharma, Heraeus Holding

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biomaterials Market Segmentation

By Material Type

- Metallic Biomaterials

- Polymeric Biomaterials

- Ceramic Biomaterials

- Natural Biomaterials

By Origin

- Synthetic Biomaterials

- Natural Biomaterials

By Application

- Orthopedic Devices & Orthobiologics

- Cardiovascular Implants & Devices

- Dental Implants & Regenerative Materials

- Wound Healing & Surgical Biomaterials

- Tissue Engineering & Regenerative Medicine

- Plastic & Reconstructive Surgery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Biomaterials Market

- Johnson & Johnson

- Medtronic

- Stryker

- Zimmer Biomet

- Royal DSM

- Carpenter Technology

- Evonik Industries

- Becton Dickinson

- Boston Scientific

- Tegra Medical (TE Connectivity)

- Celanese Corporation

- Nobel Biocare (Envista)

- Corbion

- Geistlich Pharma

- Heraeus Holding.

*- List not Exhaustive

Research Coverage: Global Biomaterials Market

The latest USDAnalytics biomaterials study provides an in-depth strategic view of how next-generation metals, polymers, ceramics, and natural biomaterials are transforming orthopedics, dental implants, cardiovascular devices, wound care, and tissue engineering platforms. Drawing on late-stage clinical pipelines, regulatory developments, and M&A activity, this report investigates how fatigue-resistant alloys, bioresorbable polymers, hydrogels, scaffolds, and smart immunomodulatory materials are reshaping device design and long-term patient outcomes. It highlights the rapid rise of polymeric biomaterials, regenerative hydrogels, and recombinant protein systems, while analysis reviews capital flows, technology platforms, and regional adoption patterns across mature and emerging healthcare systems. Breakthroughs in 3D-printed implants, nanofiber scaffolds, antimicrobial and phage-functionalized coatings, and plant- or fermentation-derived biopolymers are mapped against evolving clinical needs in joint reconstruction, spine, dental regeneration, cardiovascular repair, and chronic wound management. With detailed benchmarking of leading manufacturers, supply-chain shifts, and the growing convergence of biomaterials with digital health and personalized medicine, this report is an essential resource for C-suite leaders, product strategists, R&D teams, investors, and policy stakeholders evaluating opportunities in the global biomaterials market through 2035.

Scope Highlights

- Segmentation (By Material Type): Metallic Biomaterials, Polymeric Biomaterials, Ceramic Biomaterials, Natural Biomaterials

- Segmentation (By Origin): Synthetic Biomaterials, Natural Biomaterials

- Segmentation (By Application): Orthopedic Devices & Orthobiologics, Cardiovascular Implants & Devices, Dental Implants & Regenerative Materials, Wound Healing & Surgical Biomaterials, Tissue Engineering & Regenerative Medicine, Plastic & Reconstructive Surgery

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2025 and detailed market forecasts from 2026 to 2034.

- Companies Covered: Analysis and profiles of 15+ leading and emerging biomaterials players across device OEMs, specialty materials suppliers, and biobased innovators.