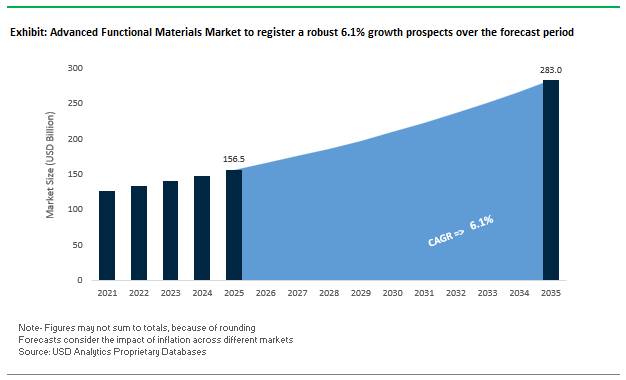

The Advanced Functional Materials Market, valued at USD 156.5 billion in 2025, is projected to reach USD 282.9 billion by 2035, expanding at a CAGR of 6.1%. This market is accelerating due to rapid advancements in nanomaterials, high-performance polymers, functional ceramics, and advanced composites, all driven by transformative demand from electric vehicles (EVs), aerospace, semiconductors, and biomedical engineering. The industry is experiencing a steady R&D shift with over 45% of recent nanomaterial patents tied to energy storage and flexible electronics, reflecting the dominance of next-generation battery research and wearable technologies.

Market Analysis: Strategic Acquisitions, Capacity Scaling, and AI Infrastructure Spend Driving Advanced Functional Materials Growth

The Advanced Functional Materials Market is undergoing significant transformation as global M&A activity, material innovations, and capital inflows reshape the competitive and technological landscape. In December 2025, AkzoNobel acquired Axalta Coating Systems in a USD 9.2 billion deal, strengthening its specialty coatings portfolio and enhancing capabilities in high-performance materials required for aerospace, EVs, and industrial manufacturing. During the same month, Ahlstrom expanded its North American footprint by extending production for advanced synthetic filtration materials-addressing surging demand in automotive and heavy industrial sectors. Earlier, in November 2025, Eaton Corporation’s USD 9.5 billion acquisition of Boyd Corporation marked a major shift in the thermal management space, equipping Eaton with enhanced solutions for EV power electronics, data center cooling, and environmental sealing technologies. In the semiconductor domain, Skyworks Solutions’ partial acquisition of Qorvo in November 2025 contributed to consolidation across the RF and mixed-signal ecosystem, supporting next-generation wireless and AI systems.

On the other hand, large-scale technology firms continue influencing upstream material demand. In October 2025, Meta, Amazon, Alphabet, and Microsoft jointly announced plans to invest more than USD 320 billion into AI infrastructure and data center development, driving unprecedented requirements for high-purity gases, thermal interface materials, and advanced composites. This expanding digital infrastructure also underscores the importance of power semiconductors, highlighted by Onsemi’s acquisition of United Silicon Carbide (Qorvo Subsidiary) in August 2025, aimed at strengthening supply for EV traction inverters and AI computing hardware. Ahlstrom further reinforced its leadership in specialty materials by completing a new molecular filtration media unit in Turin in June 2025, addressing demand from pharmaceutical, industrial, and high-purity process environments. Earlier, in March 2025, the company launched an advanced Absorbent Glass Mat (AGM) battery separator platform, strengthening its relevance in the lead-acid and energy storage ecosystem.

Advanced Functional Materials Market Overview- Performance-Led Demand, Cross-Industry Convergence, and Supply-Chain Resilience

The Advanced Functional Materials Market is increasingly defined by performance-led procurement and cross-industry convergence, rather than by material categories alone. Today, buyers across semiconductors, aerospace, healthcare, energy, and digital infrastructure are evaluating suppliers on quantifiable functional outcomes-including thermal conductivity, electrical performance, biocompatibility, weight reduction, and sustainability credentials. As a result, competitive advantage is shifting toward manufacturers that can deliver application-specific performance at scale, supported by rapid innovation cycles and resilient supply chains.

Demand momentum is being amplified by AI compute expansion, defense modernization, and healthcare innovation, all of which place exceptional stress on material purity, reliability, and lifecycle performance. High-purity consistency has become a gating factor for adoption in semiconductor fabrication and medical devices, while lightweighting and cost-to-performance optimization are increasingly decisive in aerospace, EVs, and advanced mobility platforms. At the same time, geopolitical uncertainty and capacity concentration are pushing OEMs to prioritize supplier diversification, regional manufacturing, and long-term material security, elevating materials from a procurement input to a strategic planning variable.

A defining characteristic of the market is cross-industry technology transfer. Materials initially developed for aerospace or defense-such as high-performance composites, advanced ceramics, and nano-engineered coatings-are now being redeployed into healthcare devices, data centers, and clean energy systems. This convergence is accelerating commercialization timelines and expanding addressable markets for suppliers that can bridge regulatory, performance, and volume requirements across sectors.

From the growth perspective, value creation is increasingly tied to functional integration rather than raw material innovation alone. Customers are favoring partners that can co-develop solutions, integrate materials into systems (thermal management, filtration, structural components), and support qualification across demanding regulatory environments. As capital investment intensifies in AI infrastructure, EV batteries, and next-generation healthcare, advanced functional materials are becoming enabling technologies rather than optional upgrades.

Advanced Functional Materials Market: Trends and Opportunities

Accelerated Corporate R&D in Solid-State Battery Electrolytes Reshaping EV and Aerospace Power Systems

Corporate investment in solid-state battery (SSB) materials has decisively shifted from exploratory lab programs to application-driven validation, signaling that advanced functional materials are now being developed with clear commercialization timelines. Large OEMs and chemical majors are prioritizing sulfide-based solid electrolytes, largely because their ionic conductivity approaches that of liquid electrolytes while enabling higher energy density and improved thermal safety—two non-negotiables for next-generation electric vehicles and aerospace platforms. A defining moment came in October 2025, when BMW Group, Samsung SDI, and Solid Power entered a trilateral validation agreement focused on demonstration-vehicle integration. This collaboration underscores how advanced materials suppliers are now being embedded directly into OEM development cycles rather than remaining upstream component vendors.

Material-level performance gains are reinforcing this momentum. In November 2025, LG Chem disclosed particle-engineering advances that delivered a reported 15% improvement in baseline capacity and up to 50% better high-rate discharge performance versus conventional liquid electrolyte systems, highlighting how microstructural control is becoming a competitive differentiator in advanced functional materials. Parallel to performance breakthroughs, infrastructure investment is accelerating: Samsung SDI has moved beyond bench-scale work with a dedicated solid-state pilot line in Suwon, progressing to large-format sample testing with global OEMs. Notably, commercial entry points are emerging outside passenger EVs first—December 2025 shipments of solid-state cells by Factorial to Avidrone Aerospace demonstrate that heavy-payload drones and aerospace platforms may act as early adopters, de-risking the technology before mass automotive rollout.

Regulatory-Driven Shift Toward Sustainable High-Barrier Coatings Without PFAS

Advanced functional materials innovation is increasingly being dictated by regulation rather than pure performance metrics, particularly in packaging and surface coatings. The European Packaging and Packaging Waste Regulation (PPWR), enacted in February 2025, has forced material suppliers to rethink barrier technologies under the principle of “functional circularity”—delivering moisture, oxygen, and grease resistance without undermining recyclability or relying on persistent chemicals. The scheduled EU-wide PFAS ban for food-contact packaging in August 2026 has been a catalytic trigger, sharply increasing demand for aqueous dispersions, bio-polymers, and functionalized paper-based coatings that can meet barrier requirements while remaining compliant.

Equally disruptive are PPWR recyclability mandates requiring all packaging to be recyclable or reusable by 2030. This is accelerating the transition away from complex multi-material laminates toward mono-material solutions such as MDO-PE, mono-PP films, and high-performance coated paperboards. Late 2025 compliance milestones illustrate the commercial readiness of these materials: Delipac’s PFAS-free “Smart-Safe” barrier paperboard successfully cleared EU 2026 audits, demonstrating that biodegradable and carbon-balanced coatings can meet industrial-scale performance expectations. Importantly, regulatory pressure is now extending into strategic foresight. The European Commission’s planned 2028 assessment of bio-based plastics as formal alternatives to recycled-content quotas is already redirecting R&D budgets toward PHA, cellulose-based films, and bio-derived functional coatings, positioning sustainable barrier materials as one of the most structurally attractive growth vectors within advanced functional materials.

Domestic Specialty Polymer Production Emerging as a Strategic Semiconductor Opportunity

Geopolitical realignment and semiconductor supply-chain securitization are creating a structural opportunity for advanced functional materials producers, particularly in specialty polymers, photoresists, and high-k dielectric materials required for sub-2 nm semiconductor nodes. Governments are no longer treating materials as interchangeable inputs but as strategic assets critical to national competitiveness. In the U.S., implementation of the CHIPS framework has already translated into over $72 million in late-2024 grants from the NSF and Department of Commerce, explicitly aimed at closing the “lab-to-fab” gap for domestic advanced materials suppliers.

Japan has taken a similarly interventionist approach. Under the Economic Security Promotion Act, METI approved roughly ¥100 billion in subsidies in November 2024, prioritizing Silicon Carbide materials and advanced electronic components essential for EV power modules and next-generation telecom infrastructure. India’s strategy is equally material-centric: the Electronics Component Manufacturing Scheme is incentivizing advanced substrates and specialty components to lift domestic value addition from low single digits toward 20% by the end of the decade. Beyond national programs, cross-border R&D is intensifying. METI-backed collaborations involving NTT, Intel, and SK Hynix are targeting photoelectric fusion materials that replace electrical interconnects with photonic communication on-chip, underscoring how advanced functional materials are becoming foundational to future semiconductor architectures.

High-Temperature Composite Materials Redefining Aerospace Propulsion Efficiency

In aerospace and defense, advanced functional materials are breaking through long-standing thermal and weight constraints that have limited propulsion efficiency. Ceramic Matrix Composites (CMCs) are increasingly replacing metallic superalloys in hot-section components, enabling engines to operate at substantially higher temperatures without complex cooling architectures. A critical validation milestone was achieved in 2025 under NASA’s HyTEC program, where NASA Glenn Research Center and GE Aerospace completed TRL-5 testing of advanced Environmental Barrier Coatings capable of surviving 1,000 thermal cycles at temperatures approaching 3,000°F.

The implications extend well beyond durability. CMC turbine components used in adaptive cycle engines such as GE’s XA100 are roughly one-third the weight of metal equivalents, allowing smaller rotating assemblies and contributing to materially lower fuel consumption in next-generation aircraft. Advanced functional materials are also becoming indispensable in hypersonic systems, where Silicon Carbide fiber-reinforced CMCs maintain structural integrity above 1,300°C at speeds exceeding Mach 5. Complementing material innovation is a shift in manufacturing methodology: the integration of Directed Energy Deposition and AI-driven microstructure modeling is compressing development cycles by an estimated 30–40% compared to traditional chemical vapor infiltration. Together, these advances position high-temperature composites as a cornerstone opportunity within the advanced functional materials market, directly linking materials science innovation to propulsion efficiency, range, and mission capability.

Competitive Landscape: Strategic Positioning Across Polymers, Ceramics, Nanomaterials, and Aerospace Composites

The competitive environment in the Advanced Functional Materials Market is defined by rapid innovation cycles, cross-industry integration, and aggressive portfolio expansion. Companies are focusing heavily on high-performance polymers, nanomaterial engineering, semiconductor fabrication materials, functional ceramics, and aerospace composites to maintain leadership positions. Sustainability, recyclability of composites, semiconductor-grade purity, and advanced battery material development remain core differentiators. The top players including BASF SE, 3M Company, DuPont, Hexcel Corporation, and KYOCERA Corporation are strengthening strategic capabilities through M&A, specialized material advancements, and global manufacturing expansion.

BASF SE continues to dominate through its strategic focus on advanced cathode materials tailored for electric vehicle (EV) batteries, positioning itself as a critical supplier for global automotive electrification. Its extensive portfolio includes nanomaterials, carbon nanotubes (CNTs), and functional additives designed to enhance conductivity and structural durability across electronics and industrial applications. BASF is also innovating aggressively in sustainable polyurethane and bio-based plastics, supporting global mandates for reduced environmental impact and greener supply chains. The company delivers specialty amines, resins, and engineering plastics that enhance thermal stability and long-term reliability in semiconductor, construction, and automotive components.

3M Company - Leadership in Thermal Management and High-Performance Ceramics

3M stands out for its advanced materials including boron nitride thermal fillers and high-purity ceramic microspheres, essential for modern thermal management systems in high-power electronics. Leveraging decades of expertise in material science, 3M produces highly customized film and coating solutions for automotive interiors, digital displays, and healthcare device manufacturing. Recent initiatives include expanding its fluoropolymer and high-performance adhesive portfolios aimed at extreme aerospace and industrial applications. The company’s integrated material stacks for semiconductor production support next-generation chip miniaturization and improved insulating performance.

Dupont De Nemours Inc. - Innovating Semiconductor Fabrication Materials

DuPont remains at the forefront of semiconductor manufacturing, especially through its material innovations for Extreme Ultraviolet (EUV) lithography, enabling smaller and faster ICs. Its acquisition-driven integration of Laird Performance Materials significantly boosted DuPont’s electromagnetic shielding and thermal interface materials portfolio, strengthening its role in EV, telecom, and computing industries. Key offerings include chemically amplified photoresists, advanced polyimides (Kapton), and sustainable non-fluorinated photoacid generators. The company continues expanding its engineered films and adhesive solutions to improve EV battery safety, thermal control, and system efficiency.

Hexcel Corporation - Global Leader in Aerospace Composites

Hexcel Corporation dominates the aerospace composites market with flagship products such as HexTow® carbon fiber and HexPly® prepregs, essential for lightweight, high-strength structural components. With over 80% of its materials used in commercial aerospace and defense, Hexcel plays a critical role in reducing aircraft weight and improving fuel performance. The company is actively pursuing sustainable composite manufacturing, including carbon fiber recycling from production scrap and end-of-life aircraft materials. Its innovation pipeline includes materials built for extreme temperature and pressure environments used in next-gen jet engine blades and offshore energy infrastructure.

KYOCERA Corporation - Excellence in Fine Ceramics For High-Reliability Applications

KYOCERA is internationally recognized for its premium fine ceramics and advanced materials, providing components with superior wear resistance, heat tolerance, and electrical insulation. Its product range spans alumina, zirconia, and silicon carbide, widely used in semiconductor fabrication equipment, industrial cutting tools, and medical implants. The company is expanding capacity for MLCCs and ceramic substrates, aligning with the surging demand for 5G and high-frequency electronic systems. KYOCERA is also intensifying R&D for ceramic components in EV power modules and automotive sensors that require high reliability under extreme thermal cycling.

United States Advanced Functional Materials Market Driven by CHIPS and Science Act Industrialization

The United States advanced functional materials market in 2025 is structurally aligned with semiconductor sovereignty and nanomaterials leadership, anchored by large-scale federal funding under the CHIPS and Science Act. In January 2025, the U.S. Department of Commerce awarded USD 285 million to the Semiconductor Research Corporation to establish a CHIPS Manufacturing USA institute focused on digital twins, advanced materials modeling, and next-generation processing techniques. This initiative directly targets a 40% reduction in chip development costs, positioning functional substrates, dielectric materials, and nanostructured coatings as core enablers of domestic semiconductor competitiveness.

Infrastructure expansion further reinforces this trajectory. In early 2025, Arizona State University was designated as a flagship CHIPS R&D hub, specializing in advanced packaging materials, heterogeneous integration substrates, and functional interconnect materials. Collectively, these developments are accelerating commercialization timelines for U.S.-based advanced functional materials across AI processors, high-frequency RF devices, and defense-grade electronics.

China Advanced Functional Materials Market Under 14th Five-Year Plan Sovereignty Push

China remains the fastest-scaling advanced functional materials market globally, driven by its strategic objective to achieve 70% self-sufficiency in core materials by 2025. Under Made in China 2025 and the concluding 14th Five-Year Plan, the government has established 40+ dedicated R&D centers focused on functional composites, energy storage materials, and smart coatings. These centers are tightly integrated with downstream manufacturing clusters, enabling rapid transition from lab-scale innovation to industrial deployment.

A defining feature of China’s strategy is capital intensity. Through 2026, China has committed a USD 1.4 trillion investment framework to embed functional materials into nationwide 5G networks, industrial IoT systems, and smart infrastructure. Advanced sensing materials, conductive polymers, and multifunctional coatings are being deployed at scale, reinforcing China’s position as both the largest producer and consumer of advanced functional materials for digital infrastructure.

Germany Advanced Functional Materials Market Anchored in EU Green Deal and Cluster 4

Germany functions as the European epicenter for sustainable advanced functional materials, leveraging the EU Green Deal and Horizon Europe’s Cluster 4 initiatives. Under the 2025 Horizon Europe Work Programme, Germany is leading multiple projects within the IAM4EU (Innovative Advanced Materials for Europe) framework, supported by a €1.4 billion allocation for 2025. These programs prioritize self-healing coatings, lightweight multifunctional materials, and circular-economy-driven upcycling technologies for automotive and industrial applications.

Industrial collaboration is a defining strength of the German market. Chemical leaders such as BASF and Covestro are actively partnering with public research clusters to develop bio-based conductive plastics and low-carbon functional polymers. This ecosystem positions Germany as the EU’s reference market for green electronics, sustainable mobility materials, and circular functional material systems.

South Korea Advanced Functional Materials Market Fueled by 3D-DRAM and AI Hardware

South Korea’s advanced functional materials market in 2025 is increasingly shaped by the race for AI-centric memory architectures and next-generation semiconductors. In May 2025, the Ministry of Science and ICT expanded its basic research budget to KRW 1.91 trillion, with significant allocations toward 3D-DRAM materials, hybrid bonding substrates, and vertical channel transistor materials. These functional materials are critical for scaling memory density and reducing power consumption in AI workloads.

South Korea’s strategic positioning is further strengthened by international collaboration. By joining Horizon Europe as an associate member in 2025, South Korea unlocked joint R&D pathways with EU partners in quantum materials, functional displays, and nanoelectronics. This cross-border integration enhances technology transfer while reinforcing South Korea’s role as a global supplier of advanced functional materials for memory, displays, and AI hardware platforms.

Japan Advanced Functional Materials Market Accelerated by Materials DX and Data Science

Japan continues to defend its leadership in electronic ceramics, specialty polymers, and nanomaterials through data-driven innovation. In January 2025, the Ministry of Education (MEXT) formalized the Materials DX Platform, unveiled at the Materials Innovation Strategy Symposium. This initiative integrates AI, big data, and simulation tools to dramatically shorten discovery cycles for functional nanomaterials used in healthcare devices, energy systems, and semiconductor manufacturing.

Complementing this digital push, the Advanced Research Infrastructure for Materials and Nanotechnology (ARIM) provides open access to world-class fabrication and characterization facilities. This infrastructure enables Japanese SMEs to rapidly prototype functional materials, reinforcing Japan’s competitive edge in high-reliability applications such as medical diagnostics, solid-state batteries, and precision electronics.

India Advanced Functional Materials Market Driven by National Manufacturing Mission

India is emerging as a high-growth destination for advanced functional materials manufacturing, supported by new fiscal frameworks introduced in 2025. The National Manufacturing Mission (2025–26) prioritizes materials ecosystems for EV batteries, solar PV cells, power electronics, and high-voltage transmission, directly linking functional materials to India’s clean-energy and electrification goals.

A defining catalyst is the approval of a ₹1.0 lakh crore (≈USD 12 billion) R&D incentive scheme in July 2025. This program offers long-tenure, low-interest financing for private-sector investment in deep-tech materials, nanotechnology, and biomanufacturing. As a result, India’s advanced functional materials market is transitioning from import-dependence to domestic capability creation, particularly in energy storage, electronic materials, and sustainable manufacturing inputs.

Sweden Advanced Functional Materials Market Centered on Organic and Bio-Based Electronics

Sweden occupies a unique niche in the advanced functional materials market, pioneering organic semiconductors and wood-derived functional materials. In late 2025, researchers at Linköping University announced breakthroughs in recyclable perovskite solar cells and plastic nerve cells, reinforcing Sweden’s leadership in sustainable electronics and bio-integrated systems.

A landmark December 2025 breakthrough demonstrated conductive plastic electrodes produced using visible light, eliminating hazardous solvents traditionally used in flexible electronics manufacturing. This innovation positions Sweden as a global reference point for low-toxicity, circular functional materials, particularly relevant for wearable electronics, biomedical devices, and next-generation flexible circuits.

Strategic Summary – Advanced Functional Materials Market (2025)

Advanced Functional Materials Market Development Matrix by Country

|

Country

|

Strategic Focus Area

|

Key 2025 Development

|

Market Positioning Impact

|

|

United States

|

Semiconductor & Nanomaterials

|

$285M CHIPS Manufacturing USA Institute

|

Domestic supply chain resilience

|

|

China

|

Functional Composites & IoT

|

$1.4T Smart Infrastructure Framework

|

High-volume industrial dominance

|

|

Germany

|

Sustainable Materials

|

€1.4B Horizon Europe Cluster 4

|

EU green materials leadership

|

|

South Korea

|

AI Memory Materials

|

KRW 1.91T 3D-DRAM Research Push

|

Advanced memory specialization

|

|

Japan

|

Materials DX & AI

|

Materials DX Platform Launch

|

Faster functional material discovery

|

|

India

|

Clean-Tech Manufacturing

|

₹1.0 Lakh Cr R&D Incentives

|

Rapid capacity build-up

|

|

Sweden

|

Organic Electronics

|

Solvent-Free Conductive Plastics

|

Sustainable electronics innovation

|

Advanced Functional Materials Market Report Scope

Advanced Functional Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$156.5 Billion

|

|

Market Size (2035)

|

$282.9 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Material Type (Ceramics, Composites, Polymers, Metals, Nanomaterials, Energy Materials, Glasses, Others), By Technology (Nanomaterials, Smart Materials, Conductive Polymers, Biomaterials, Photonic Materials, Other Technologies), By Form Factor (Bulk Solid, Coatings, Fibers, Films & Sheets, Powders), By Application (Electrical & Electronics, Automotive & Transportation, Aerospace & Defense, Energy Storage & Generation, Healthcare, Environmental, Industrial, Construction)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, BASF SE, Dow Inc., DuPont de Nemours Inc., Arkema S.A., Kyocera Corporation, LG Chem Ltd., Huntsman International LLC, Evonik Industries AG, Hexcel Corporation, Morgan Advanced Materials, SGL Carbon, Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, Toray Industries Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Functional Materials Market Segmentation

By Material Type

- Ceramics

- Composites

- Polymers

- Metals

- Nanomaterials

- Energy Materials

- Glasses

- Others

By Technology

- Nanomaterials

- Carbon Nanotubes

- Graphene

- Quantum Dots

- Smart Materials

- Piezoelectric Materials

- Shape Memory Alloys

- Thermochromic Materials

- Conductive Polymers

- Polyaniline

- Polythiophene

- Biomaterials

- Photonic Materials

- Other Technologies

By Form Factor

- Bulk Solid

- Coatings

- Fibers

- Films and Sheets

- Powders

- Electrical and Electronics

- Automotive and Transportation

- Aerospace and Defense

- Energy Storage and Generation

- Healthcare

- Environmental

- Industrial

- Construction

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Advanced Functional Materials Market

- 3M Company

- BASF SE

- Dow Inc.

- DuPont de Nemours, Inc.

- Arkema S.A.

- Kyocera Corporation

- LG Chem Ltd.

- Huntsman International LLC

- Evonik Industries AG

- Hexcel Corporation

- Morgan Advanced Materials

- SGL Carbon

- Sumitomo Chemical Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Toray Industries, Inc.

*- List not Exhaustive