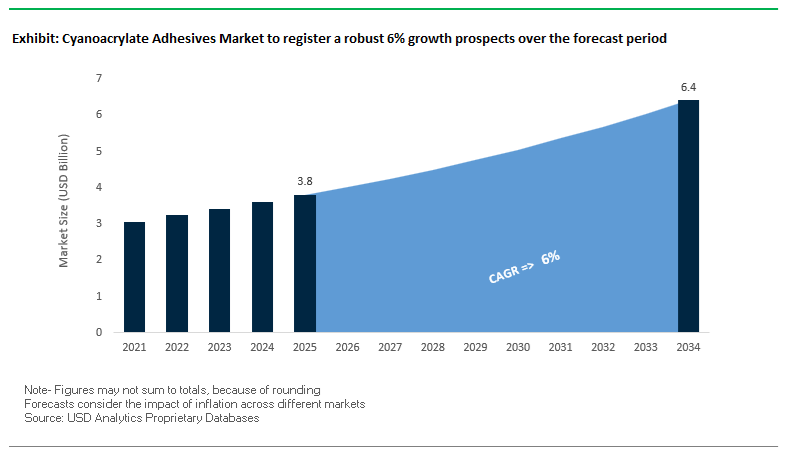

The cyanoacrylate adhesives market is gainig rapid demand growth driven by OEMs redesigning assembly architectures around speed, part miniaturization, and reduced mechanical complexity. The market is projected to expand from USD 3.8 billion in 2025 to USD 6.4 billion by 2034, at a CAGR of 6.0%, reflecting sustained qualification of cyanoacrylate systems in automotive sub-assemblies, consumer electronics, medical devices, and high-precision industrial manufacturing. In these environments, the value proposition is not adhesion in general, but deterministic curing behavior, rapid handling strength, and repeatable bonding of small, high-tolerance components. Cyanoacrylates are increasingly specified at the process-planning stage where seconds of cycle time, clean bond lines, and elimination of secondary fastening steps directly affect throughput, yield, and labor efficiency.

Demand is being structurally reshaped by OEM shifts toward automated, high-speed assembly and compact, multi-material designs that are poorly served by screws, clips, or slower-curing chemistries. Modern cyanoacrylate formulations are engineered for controlled viscosity, capillary flow, and substrate-specific adhesion across metals, engineered plastics, elastomers, and composite surfaces. This enables rapid fixation of precision parts without thermal input, mechanical stress, or fixturing dwell, which is critical in electronics housings, sensor assemblies, and micro-mechanical components. In medical device manufacturing, cyanoacrylates have progressed beyond temporary bonding, with application-specific grades designed to meet biocompatibility expectations and consistent cure performance in controlled production environments, supporting both functional assembly and surface sealing roles.

Material substitution is driven by measurable operational outcomes rather than material novelty. Cyanoacrylates are replacing micro-fasteners and solvent-based adhesives because instant cure at ambient conditions reduces fixture stations, lowers work-in-process inventory, and improves line uptime. High initial bond strength minimizes handling delays and rework, while visually clean bond lines eliminate post-assembly finishing in appearance-critical products. These attributes translate directly into lower per-unit assembly cost and higher effective equipment utilization. Looking forward, the market trajectory will be shaped by manufacturers’ ability to deliver tightly controlled, automation-compatible formulations that align with OEM validation protocols, moisture-managed production environments, and regulatory compliance requirements, anchoring cyanoacrylates as a production-grade bonding material rather than a discretionary adhesive choice.

The cyanoacrylate adhesives industry has entered a high-growth, innovation-driven phase as leading manufacturers invest heavily in bio-compatible, high-temperature, and low-odor formulations while expanding regional manufacturing capacity to meet the accelerating demand in Asia-Pacific and North America.

In November 2025, a major global adhesive manufacturer launched a new line of toughened black cyanoacrylates engineered for EV battery module assembly, offering enhanced peel strength and long-term resistance to vibration and impact. This reflects a broader market trend—transitioning from simple bonding to structural reliability in electric mobility components. The same month, Ahlstrom expanded into specialty materials for instant adhesives, aligning its substrate business with the Pressure-Sensitive and Contact Adhesives segment, which increasingly overlaps with cyanoacrylate formulations.

The regional production landscape is also shifting rapidly. In October 2025, an Asia-Pacific adhesives manufacturer completed a large-scale solvent-free production expansion in Vietnam, strategically targeting consumer electronics OEMs in the region’s growing manufacturing hubs. Similarly, September 2025 marked a significant acquisition by a European chemical group, which bought a US-based biocompatible cyanoacrylate specialist, signaling deeper integration between medical-grade chemistry and industrial manufacturing.

Innovation continues to reshape the performance envelope. In August 2025, university and industry researchers announced a breakthrough in light-cure cyanoacrylate systems, enabling complete polymerization within seconds—even in shadowed zones—by leveraging a secondary moisture-activated cure. This hybrid mechanism bridges the gap between UV adhesives and moisture-cure systems, unlocking potential in multi-layer electronics and transparent assemblies.

June 2025 also saw the introduction of a gap-filling cyanoacrylate capable of bonding 5 mm joints—traditionally dominated by epoxies—demonstrating the material’s progression into structural and large-area applications. February 2025 was notable for Henkel’s Loctite 4011S and 4061S launches, expanding its medical-grade adhesive range for bonding rubber, plastics, and metals under strict biocompatibility and sterilization standards.

The market’s regulatory direction is equally impactful. January 2025 EU guidelines emphasized the transition toward low-monomer cyanoacrylate formulations, pushing global producers to adopt VOC-safe chemistries. This aligns with Japan’s December 2024 initiative, which redirected R&D toward high-resilience cyanoacrylates capable of retaining >75% strength after 1,000 hours of hot-humid aging, confirming the industry's focus on long-term reliability under environmental stress.

The new generation of toughened cyanoacrylate adhesives (CAs) is transforming structural bonding by overcoming one of the core limitations of traditional cyanoacrylates—brittleness. Manufacturers are incorporating elastomeric and toughening components to achieve improved impact resistance, peel strength, and temperature durability, enabling CAs to compete directly with epoxies and structural acrylics in demanding engineering environments.

Recent studies and industrial innovations demonstrate remarkable performance enhancement. Laboratory evaluations report that elastomer-toughened CA systems can exhibit peel strength values up to 22 times higher than standard epoxy resins under identical conditions. The performance leap positions CAs as credible alternatives for high-stress bonding in sectors such as automotive structural components, aerospace repair, and defense hardware, where lightweight, rapid-curing bonds are essential.

Temperature endurance has also advanced dramatically. Major adhesive manufacturers market heat-resistant cyanoacrylates capable of continuous operation up to 200°C (390°F) without secondary heat curing. The characteristic is particularly advantageous in under-the-hood automotive assemblies, high-vibration engines, and industrial machinery where adhesives must perform reliably in thermally challenging environments. These developments signal a decisive shift toward engineering-grade CAs that merge fast curing with structural reliability, offering an unmatched combination of speed, toughness, and durability.

The industry’s pivot to low-bloom and odorless cyanoacrylate adhesives reflects both regulatory and aesthetic imperatives, particularly in precision markets like consumer electronics, optics, and medical devices. The characteristic white “bloom” residue and sharp odor of traditional formulations have long been barriers to use in high-precision or consumer-facing applications.

Modern Methoxyethyl and Alkoxyethyl cyanoacrylates eliminate these drawbacks, enabling clean, non-staining bonds ideal for sensitive assemblies such as smartphone screens, camera lenses, or wearable medical devices. These specialized adhesives provide fixture times under five seconds while maintaining superior shear strength and cosmetic quality. For high-value electronics manufacturing, where residue contamination could impair sensor or lens function, such low-bloom formulations are the industry standard.

Additionally, the occupational safety and health benefits of low-odor CAs are accelerating their adoption in high-volume assembly lines. By reducing the need for advanced ventilation systems, these adhesives not only improve workplace air quality but also lower operational costs in industrial environments. The transition toward odorless, clean-room compatible cyanoacrylates aligns with global manufacturing trends emphasizing environmental compliance and enhanced worker well-being.

The surge in electric vehicle (EV) production presents a high-growth opportunity for fast-curing cyanoacrylate adhesives, which offer superior precision, thermal stability, and bonding reliability for battery module and electronic subassembly applications. The adhesives’ ability to form rapid, strong bonds without heat or complex curing infrastructure aligns perfectly with EV assembly automation and throughput requirements.

In EV battery pack construction, CAs are increasingly being used alongside structural adhesives for busbar bonding, temperature sensor attachment, and module reinforcement. Suppliers are promoting dual-use formulations that provide high handling strength within one minute and full structural integrity within five minutes, allowing high-speed, continuous production of battery modules. The instant bonding advantage shortens manufacturing cycles and minimizes fixture time in robotic assembly lines.

Thermal resistance is another decisive factor. Advanced CA formulations developed for EV applications withstand continuous service temperatures up to 200°C (390°F), ensuring reliable performance near heat-generating cells and electronic modules. These high-thermal-stability adhesives not only enhance battery safety and durability but also expand their use into powertrain and electronic control unit (ECU) assemblies, where vibration resistance and temperature endurance are mission-critical.

The convergence of biocompatibility, instant curing, and regulatory acceptance is propelling cyanoacrylate adhesives into next-generation medical and wearable device markets. With the rise of minimally invasive procedures, wound closure alternatives, and wearable health monitoring technologies, CAs are emerging as high-value medical-grade adhesives that deliver strong, flexible, and sterile bonding in sensitive applications.

In wearable medical devices such as ECG monitors, insulin pumps, and continuous glucose monitors (CGMs), long-term skin adhesion is a critical performance metric. Manufacturers are developing specialized CA formulations capable of secure, irritation-free bonding for up to seven days of continuous wear while allowing clean removal without residue. These adhesives must exhibit balanced tack, breathability, and moisture resistance to withstand real-world use across varying skin conditions and patient activity levels.

In clinical settings, long-chain cyanoacrylates—specifically butyl and hexyl variants—are FDA-approved for tissue adhesion and wound closure, offering an effective, non-invasive alternative to sutures. These medical-grade adhesives achieve rapid polymerization upon contact with biological moisture, sealing incisions while minimizing infection risks and patient recovery time. With ISO 10993 biocompatibility certification and FDA acceptance, cyanoacrylates are becoming indispensable in biosensor attachment, transdermal patch assembly, and emergency surgical adhesives.

Cyanoacrylate Adhesives Market Share Insights, 2025-2034

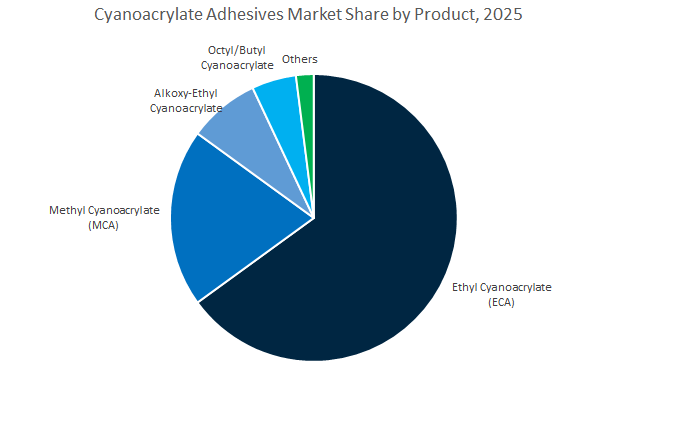

Ethyl cyanoacrylate (ECA) remains the cornerstone of the global cyanoacrylate adhesives industry, commanding a dominant share of 66.9% in 2025 due to its unmatched balance of performance, cost, and versatility. ECA’s ability to rapidly bond a wide variety of substrates—including plastics, metals, elastomers, ceramics, and composites—has cemented its role as the universal “instant adhesive” across industrial, medical, and consumer applications. Its fast-curing nature, coupled with high tensile and shear strength, makes it indispensable for precision assembly, repair, and small component bonding. In electronics manufacturing, ECA is widely used for wire tacking, PCB component bonding, and fixing ferrite cores. In the medical field, ECA-based formulations are used for quick, non-invasive device assembly and some topical applications (non-contact closure). The ongoing shift toward low-blooming and low-odor ECA variants also supports its growing demand in high-precision, cleanroom environments such as optical assembly and consumer electronics. Its superior adhesion to diverse materials, combined with process simplicity and a favorable cost-performance ratio, ensures that ECA remains the backbone of both industrial and retail-grade cyanoacrylate adhesives.

Methyl cyanoacrylate (MCA) retains a significant 20.4% market share, driven by its extremely fast cure speed and high surface energy compatibility. It is particularly effective for bonding acidic or porous substrates such as wood, paper, and leather, where other formulations may fail. Its fast polymerization reaction makes it suitable for rapid assembly lines and instant repair applications across manufacturing, footwear, and woodworking industries. However, MCA’s brittleness, limited temperature resistance, and strong odor restrict its use in sensitive or high-stress environments. To address this, hybrid and stabilized MCA variants are being developed, enhancing flexibility and reducing odor without compromising speed. In DIY and small-scale repair applications, MCA remains the go-to adhesive for its instantaneous grip and ease of use. Despite being less dominant than ECA, it plays a crucial role in high-speed production, rapid fixturing, and emergency repairs—markets that rely on immediate curing and high bond strength over aesthetic or long-term durability.

Manual or handheld application methods account for 66.1% of the global cyanoacrylate adhesives market, underscoring the product’s hallmark attribute—ease of use and instant performance. From small consumer tubes to precision needle-tip applicators and brush-on bottles, manual application remains the preferred method for maintenance, repair, and assembly (MRO) tasks across industries. It allows users to apply adhesive exactly where needed without specialized equipment, supporting a vast ecosystem of industrial workshops, household repair, and crafts. In professional use, it is common in furniture manufacturing, footwear assembly, electronics repair, and small-scale automotive work, where versatility and speed outweigh automation benefits. The simplicity of manual dispensing aligns perfectly with the DIY market boom, especially in Asia-Pacific and Latin America, where accessibility and affordability are key purchase drivers. Additionally, the low equipment requirement and minimal training needed for manual application contribute to its continued dominance in low- to mid-volume production environments, ensuring strong market retention through 2025.

Automated dispensing systems represent a rapidly expanding share of the cyanoacrylate adhesives market, driven by the global transition toward high-precision, automated manufacturing in sectors such as electronics, automotive, and medical devices. Automated systems ensure consistent dot size, precise placement, and repeatable performance, critical for small or delicate assemblies where manual application risks over-application or contamination. In electronics, automated dispensing is vital for attaching microcomponents, securing connectors, and fixing sensors under controlled conditions. Similarly, automotive manufacturers employ robotic application systems for interior trim bonding, sensor installation, and electronic control unit (ECU) assembly to maintain accuracy and reduce cycle times. The medical device sector also depends heavily on automation to meet stringent cleanliness, regulatory, and quality requirements during adhesive application. The shift toward closed-system automated dispensing units, which prevent premature curing and minimize operator exposure, is enhancing adoption.

The global cyanoacrylate adhesives market is led by a group of diversified specialty chemical giants and niche precision adhesive experts that drive innovation in instant bonding, biocompatibility, and high-performance assembly applications. Companies such as Henkel, H.B. Fuller, Bostik (Arkema), Permabond, ThreeBond, and 3M dominate the competitive field with integrated R&D, specialized product lines, and global production footprints.

Henkel’s Loctite® brand continues to dominate the cyanoacrylate adhesives market with the industry’s broadest portfolio, covering medical-grade, low-odor, light-cure, and impact-toughened instant adhesives. The company’s latest innovations—Loctite 4011S and 4061S (February 2025)—were developed for precision bonding in medical device manufacturing, emphasizing compliance with ISO 10993 and USP Class VI standards. Henkel’s Loctite line remains the benchmark for high-speed assembly, electronic bonding, and maintenance repair operations (MRO) across global industries.

H.B. Fuller has built strong market differentiation through its Full-Care series, which integrates cyanoacrylate and hot-melt bonding for hygiene construction and consumer packaging. The company’s innovations focus on low-add-on adhesive solutions that enhance productivity and sustainability in disposable hygiene markets such as baby care and feminine care. Fuller’s continued R&D push in biocompatible and flexible adhesives underlines its leadership in nonwoven construction adhesives.

Bostik, under the Arkema Group, leverages its Born2Bond™ line to serve medical device, electronics, and industrial micro-assembly markets. The Born2Bond™ Ultra and Light Lock ranges combine instant bonding with solvent-free and low-odor formulations, offering rapid cure and superior aesthetic finish. Bostik’s strategy emphasizes the integration of high-performance polymer science from Arkema, ensuring adhesives meet biocompatibility, sterilization, and optical clarity standards for medical and consumer electronics assembly.

Permabond focuses on performance-driven markets that demand durability and precision. Its 940 series non-blooming cyanoacrylates deliver aesthetic excellence in electronics and cosmetic-grade applications, while high-temperature variants withstand continuous exposure up to 250°C after post-curing. Permabond’s impact-resistant, low-odor cyanoacrylates are widely used in automotive, aerospace, and consumer electronics, where clean assembly and consistent strength are critical.

ThreeBond is a key Japanese manufacturer specializing in solvent-less, single-component instant adhesives tailored for automotive, electronics, and precision assembly. Its TB1700 and TB7700 series are recognized for superior heat and vibration resistance, essential for EV battery bonding. The latest Gold Label series (TB7737/7738) introduces elastomer-toughened formulations offering exceptional peel strength and impact durability, positioning ThreeBond as a preferred supplier for high-performance mechanical assemblies.

3M Company continues to leverage its multi-material expertise to deliver cyanoacrylate adhesives for industrial assembly, electronics, and personal safety products. Its advanced adhesives integrate seamlessly with 3M’s broader tape and structural bonding portfolio. In May 2025, the company confirmed a $67 million expansion in Nebraska, scaling production for high-demand industrial adhesives, including instant-bonding cyanoacrylate systems used in automotive and safety equipment manufacturing.

The United States cyanoacrylate adhesives market is at the forefront of innovation, with significant advances in medical-grade formulations, aerospace-grade instant adhesives, and defense-oriented bonding technologies. Henkel’s February 2025 launch of Loctite 4011S and 4061S, free from carcinogenic and mutagenic substances (CMR), demonstrates the U.S. focus on biocompatible adhesives for surgical equipment and catheter assembly.

Meanwhile, tariffs on imported specialty polymers from Asia have driven domestic adhesive producers to diversify supply chains and invest in local production of cyanoacrylate monomers. 3M Company’s 2024 expansion in Nebraska enhances capacity for industrial adhesives, while H.B. Fuller’s acquisition of ND Industries (Nov 2024) strengthens its presence in UV-curable and instant-bonding technologies for precision assembly. Aerospace programs, including unmanned aerial vehicles (UAVs) and lightweight composites, are fueling demand for rubber-toughened, heat-resistant cyanoacrylates, ensuring structural integrity under dynamic stress conditions.

The U.S. market also remains a defense and MRO (Maintenance, Repair & Overhaul) hub, with continued procurement of rapid curing adhesives for field repairs in extreme conditions. The trends underscore the U.S.’s leadership in advanced, sustainable, and high-performance instant adhesives across automotive, aerospace, and healthcare industries.

Germany stands as the European innovation center for industrial cyanoacrylate adhesives, with major demand from automotive lightweighting, precision electronics, and medical device sectors. The nation’s engineering ecosystem, led by DELO Industrial Adhesives and Henkel AG & Co. KGaA, is driving the transition toward low-odor, solvent-free cyanoacrylate formulations that meet EU VOC emission standards and the European Green Deal objectives.

German automotive OEMs are heavily integrating fast-curing instant adhesives into electric vehicle (EV) production — particularly for bonding interior panels, sensors, and lightweight structural parts. DELO’s development of automated micro-dispensing systems is optimizing precision assembly in electronics, enabling sub-second curing in fully robotic manufacturing environments. The regulatory environment, especially EU-MDR compliance, mandates continuous testing of biocompatible cyanoacrylates for medical device use.

Germany’s focus on thermal resistance, moisture stability, and automation-driven adhesive systems is redefining industrial bonding efficiency. Combined with its strong R&D investment in isocyanate-free, alkoxy-ethyl cyanoacrylates, Germany remains a European hub for sustainable and high-performance instant adhesives.

China dominates the Asia-Pacific cyanoacrylate adhesives market, driven by unparalleled demand from electronics assembly, 5G infrastructure, and large-scale construction projects. The nation’s rapid industrialization and digital transformation have positioned it as a global manufacturing powerhouse for both commodity-grade and specialty instant adhesives.

China’s consumer electronics and PCB sectors are expanding rapidly, creating high-volume demand for low-bloom, low-odor, and light-curing cyanoacrylate adhesives for precision component bonding. Government-backed programs under Made in China 2025 are incentivizing vertical integration of cyanoacrylate monomer production, reducing dependence on imports and boosting domestic supply chain resilience. Local champions like Hubei Huitian New Materials are scaling operations and innovating to compete directly with global adhesive giants.

Beyond electronics, the construction, footwear, and general manufacturing sectors contribute heavily to market growth, favoring cost-effective, high-tack instant adhesives for everyday industrial assembly. China’s increasing R&D focus on temperature-resistant, impact-toughened cyanoacrylates also aligns with its broader strategy to lead in high-value industrial materials and green chemical manufacturing.

Japan’s cyanoacrylate adhesives market continues to set global benchmarks for high-precision and reliability, particularly in electronics, semiconductors, and optical component manufacturing. Companies such as Toagosei Co. Ltd. and ThreeBond dominate the domestic landscape, focusing on ultra-low viscosity, high-flexural-strength cyanoacrylates for micro-assembly, camera modules, and display bonding applications.

The market’s emphasis on rapid curing with high mechanical stability reflects Japan’s expertise in combining speed and structural integrity. Japanese firms are also integrating robotic dispensing and automation technologies into their adhesive systems to improve application consistency and efficiency in production environments. In addition, significant research into photo-curable and hybrid instant adhesives is shaping the next wave of materials designed for flexible electronics and precision robotics.

With continued leadership in cleanroom-grade cyanoacrylates and semiconductor-compatible adhesives, Japan maintains its edge in miniaturization, innovation, and manufacturing precision, catering to global tech and automotive OEMs.

South Korea’s cyanoacrylate adhesives industry is expanding rapidly, supported by its robust EV battery, display, and shipbuilding sectors. The country’s global leadership in battery technology and flexible display manufacturing has spurred demand for specialized low-outgassing cyanoacrylate formulations compatible with OLED, micro-LED, and advanced electronic modules.

In the automotive and EV industries, high thermal resistance and dielectric stability are essential, prompting manufacturers to use non-structural cyanoacrylates for secondary sealing within EV battery packs. Shipbuilding and heavy machinery manufacturers continue to rely on fast-curing industrial adhesives to shorten maintenance and assembly timelines.

Ongoing R&D efforts target thermal stability, improved adhesion to composites, and precision application for high-volume manufacturing. South Korea’s combination of technological infrastructure and chemical innovation positions it as a regional leader in performance-driven instant adhesives for high-tech and heavy industries alike.

India’s cyanoacrylate adhesives market is expanding at an accelerated rate, fueled by industrialization, infrastructure development, and the Make in India initiative. The country’s booming construction and automotive component sectors are major consumers of general-purpose and high-performance instant adhesives used in flooring, paneling, and component assembly.

Domestic manufacturers like Pidilite Industries Ltd. are increasing production capacity and distribution networks to serve India’s large and price-sensitive market. Additionally, the e-commerce and DIY adhesive segment is witnessing rapid growth, supported by improved product accessibility and growing consumer awareness. In the automotive industry, cyanoacrylates are being adopted for bonding sub-assemblies and trim components, ensuring both durability and precision for exports and domestic use.

India’s industrial diversification and focus on eco-friendly, solvent-free adhesive technologies are aligning with international sustainability standards, making it a pivotal market for future growth in low-VOC, quick-bonding solutions.

Cyanoacrylate Adhesives Market Report Scope

Cyanoacrylate Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.8 Billion

|

|

Market Size (2034)

|

$6.4 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Product Type (Ethyl Cyanoacrylate, Methyl Cyanoacrylate, Alkoxy-Ethyl Cyanoacrylate, Octyl/Butyl Cyanoacrylate, Others), By Technology (Reactive, UV/Light Curable, Toughened/Reinforced, Gel/Thickened), By Application (Manual/Handheld, Automated Dispensing), By End-User (Transportation, Medical & Healthcare, Electronics, Industrial, Consumer Goods, Woodworking & Furniture, Footwear & Leather

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Arkema Group, Toagosei Co., Ltd., DELO Industrie Klebstoffe GmbH & Co. KGaA, Permabond LLC, Illinois Tool Works Inc., Pidilite Industries Ltd., Sika AG, Dymax Corporation, Master Bond Inc., NANPAO RESINS CHEMICAL GROUP, ThreeBond Holdings Co., Ltd., Hubei Huitian New Materials Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Ethyl Cyanoacrylate

- Methyl Cyanoacrylate

- Alkoxy-Ethyl Cyanoacrylate

- Octyl/Butyl Cyanoacrylate

- Others

By Technology/Formulation

- Reactive

- UV/Light Curable

- Toughened/Reinforced

- Gel/Thickened

By Application Method

- Manual/Handheld

- Automated Dispensing

By End-Use Industry

- Transportation

- Medical & Healthcare

- Electronics

- Industrial

- Consumer Goods

- Woodworking & Furniture

- Footwear & Leather

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- 3M Company

- Arkema Group

- Toagosei Co., Ltd.

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Permabond LLC

- Illinois Tool Works Inc.

- Pidilite Industries Ltd.

- Sika AG

- Dymax Corporation

- Master Bond Inc.

- NANPAO RESINS CHEMICAL GROUP

- ThreeBond Holdings Co., Ltd.

- Hubei Huitian New Materials Co., Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Cyanoacrylate Adhesives Market, delivering analysis reviews that connect instant-bonding chemistry with line throughput, reliability under heat/humidity, and precision aesthetics in automotive, electronics, industrial, and medical workflows. It highlights next-gen breakthroughs such as elastomer-toughened, low-odor/low-bloom, light-curable, and gap-filling cyanoacrylates that extend performance from quick fixes to engineering-grade assemblies; profiles regulatory-ready moves toward low-monomer, VOC-safe platforms; and benchmarks vendors on strength, fixture time, durability, and clean-finish metrics critical to automated dispensing. By uniting techno-economic scorecards with adoption barriers and qualification pathways, this report is an essential resource for CTOs, R&D formulators, process/quality engineers, sourcing leaders, and investors evaluating fast-curing, high-durability bonding solutions at scale.

Scope Highlights

Segmentation:

- By Product Type: Ethyl Cyanoacrylate; Methyl Cyanoacrylate; Alkoxy-Ethyl Cyanoacrylate; Octyl/Butyl Cyanoacrylate; Others.

- By Technology/Formulation: Reactive; UV/Light Curable; Toughened/Reinforced; Gel/Thickened.

- By Application Method: Manual/Handheld; Automated Dispensing.

- By End-Use Industry: Transportation; Medical & Healthcare; Electronics; Industrial; Consumer Goods; Woodworking & Furniture; Footwear & Leather.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies including strategy, innovation pipelines, and regional capacity.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.