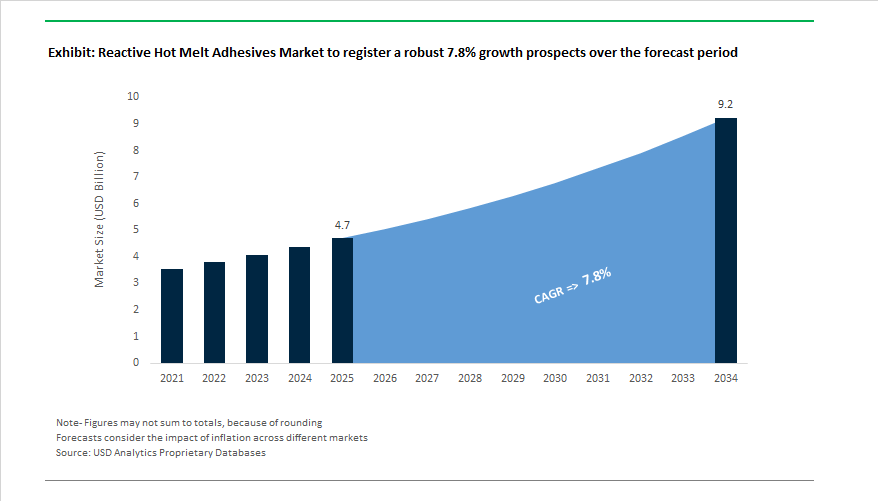

The Global Reactive Hot Melt Adhesives (RHMA) Market is forecast to grow from $4.7 billion in 2025 to $9.2 billion by 2034, at a strong CAGR of 7.8%. This growth reflects the ongoing industrial transformation toward high-performance, sustainable, and heat-resistant bonding solutions, driven by major end-use sectors such as automotive, construction, electronics, and packaging. Reactive hot melt adhesives, particularly polyurethane-based (PUR) formulations, have become indispensable due to their superior bonding strength, flexibility, and chemical durability, making them a cornerstone of modern lightweight design and sustainable manufacturing.

Polyurethane (PUR) adhesives dominate the global RHMA resin market, primarily due to their versatile use across plastics, metals, and wood substrates. High-temperature RHMAs, continue to be the preferred choice for industries requiring thermal stability, especially in automotive engines, electronics assembly, and industrial construction. Additionally, the plastic substrate segment underscores the pivotal role of RHMAs in lightweight vehicle manufacturing, electronics housings, and appliance assembly.

Automotive manufacturers are rapidly embracing RHMAs to achieve superior bond strength, resistance to vibration, and VOC-free assembly processes—vital for electric vehicles (EVs) and advanced interior designs. As global vehicle production surpasses 93 million units, the demand for eco-efficient adhesive systems is expected to scale further, supported by sustainability goals and recyclability initiatives.

The Global Reactive Hot Melt Adhesives Industry is evolving through a combination of sustainability-driven partnerships, high-temperature material innovation, and strategic acquisitions that strengthen regional manufacturing ecosystems. Leading companies are making major moves toward low-carbon manufacturing, recyclability, and high-performance automotive applications.

In October 2025, Henkel and Dow deepened their long-standing partnership to support decarbonization in adhesives manufacturing, introducing low-carbon feedstocks and renewable electricity to Henkel’s hot melt production facilities. This initiative targets a 20–40% reduction in Product Carbon Footprint (PCF), aligning with Europe’s aggressive carbon neutrality mandates. Similarly, in September 2024, Covestro launched Dispercoll U, a PUR-based bonding solution engineered for automotive interior lamination, offering exceptional heat resistance and flexibility for three-dimensional trim parts — a clear signal of how automotive OEMs are integrating advanced adhesives into design innovation.

Henkel, a consistent innovation leader, introduced three new Loctite potting adhesives (August 2024) aimed at EV and traditional automotive components, offering superior durability, heat stability, and protection against environmental degradation. Earlier in April 2024, Henkel, Kraton, and Dow formed a strategic sustainability alliance to advance renewable adhesive formulations for consumer goods, reinforcing the industry’s transition to eco-friendly, renewable material systems.

The packaging sector also saw transformation, with Henkel’s Technomelt E-COM portfolio (December 2023) enabling high-speed, right-sized e-commerce packaging through precision adhesive systems designed for on-demand box manufacturing. Dow and Avery Dennison’s April 2023 collaboration further supported the circular economy, introducing recyclable polyolefin hot melt adhesives that received Recyclass approval for HDPE colored streams—signifying practical advancements in closed-loop packaging systems.

Strategic acquisitions continue to reshape the competitive map. H.B. Fuller’s acquisition of Fourny NV (February 2022) and Apollo (January 2022) enhanced its European market presence in construction and industrial roofing adhesives, while Jowat SE’s February 2020 introduction of Jowatherm-Reaktant MR 604.90, a low-monomer PUR adhesive, became a benchmark for safety-compliant woodworking and profile wrapping.

Market Trend 1: Automotive Lightweighting and Multi-Material Integration Fueling RHMA Adoption

The global automotive sector’s pivot to electric mobility and fuel-efficient vehicle design is creating a significant demand surge for lightweight, multi-substrate bonding solutions, where Polyurethane (PUR) and Silane-Modified Polyolefin (POR) RHMAs deliver superior performance over conventional fasteners and solvent-based adhesives.

According to leading automotive OEM initiatives, interior component manufacturers are targeting a 50%–70% reduction in Volatile Organic Compound (VOC) emissions by 2027, aligning with stricter cabin air quality requirements and consumer health awareness. The transition is accelerating the adoption of low-VOC RHMAs for headliners, seating, dashboard panels, and trim assemblies, where mechanical fasteners are being replaced to cut weight and improve acoustic insulation.

A leading global adhesive producer recently introduced a next-generation moisture-curing RHMA that achieved a 20% increase in lap shear strength on carbon fiber-reinforced polymers (CFRP) and high-strength aluminum substrates compared to its previous formulations. The leap in mechanical performance is vital for structural integrity in EV assemblies, ensuring robust adhesion across dissimilar materials under high stress and temperature cycling conditions.

Beyond performance, RHMAs enable up to 30% weight reduction in vehicle assemblies by eliminating screws, clips, and rivets, contributing directly to extended driving range and improved fuel economy. Their ability to maintain long-term flexibility and mechanical strength under vibration, humidity, and temperature fluctuations positions Reactive Hot Melt Adhesives as a cornerstone of next-generation EV design, interior bonding, and structural applications.

Market Trend 2: Regulatory Pressure and Sustainability Targets Accelerating Bio-Based and Low-VOC RHMA Development

The transition toward environmentally responsible adhesive technologies is intensifying, driven by strict global emission standards and the sustainability commitments of leading brands across automotive, construction, and consumer goods industries.

In both the European Union and the United States, regulators such as the EPA and European Chemicals Agency (ECHA) have implemented low-VOC emission ceilings, with benchmarks as stringent as <1,000 µg/m³ TVOC at 28 days, particularly for interior adhesives used in furniture, flooring, and automotive interiors. To comply, manufacturers are aggressively reformulating solvent-free, low-VOC RHMA systems with bio-based inputs and enhanced indoor air quality certification (e.g., France’s A+ label or Germany’s DIBt approval).

A major milestone in sustainable adhesive chemistry was achieved with the development of bio-based reactive hot melt polyurethanes synthesized from CO₂-derived polycarbonate polyols. These new polyols not only replace fossil-based feedstocks but exhibit enhanced flame retardancy, with Limiting Oxygen Index (LOI) values increasing from 17.2 to 28.2, alongside superior mechanical strength. The aligns with global decarbonization objectives by converting captured CO₂ into performance-grade adhesive materials.

Leading market players such as Henkel, H.B. Fuller, and Bostik are spearheading R&D programs that integrate renewable plant-based raw materials—including castor oil derivatives, cellulose esters, and lignin-based polyols—into RHMA formulations. The focus on bio-based polyurethanes and polyolefins not only lowers environmental footprints but also enhances corporate compliance with global ESG frameworks and carbon neutrality pledges through 2030.

Market Opportunity 1: Circular Economy Expansion Through Deconstructable and Recyclable RHMAs

The ongoing global shift toward a circular economy is driving innovation in debonding-on-demand adhesives, offering a major breakthrough for electronics recycling and durable goods disassembly. The integration of reactive chemistries that can be chemically or thermally deactivated allows manufacturers to recover valuable substrates—such as metals, composites, and semiconductors—without damaging components.

Recent academic developments have yielded photo-debondable reactive adhesives capable of achieving ≥90% substrate separation within one minute when activated by specific UV or electrical triggers. The technology significantly reduces the cost and complexity of end-of-life recycling in consumer electronics, promoting sustainable dismantling of smartphones, displays, and automotive battery modules.

Further research is progressing into magnetically responsive RHMAs incorporating iron oxide nanoparticles, which allow localized heat generation under an oscillating magnetic field to achieve rapid, targeted debonding. These reversible adhesives enable component reuse and reassembly without mechanical degradation, providing a critical technological foundation for zero-waste manufacturing systems.

In high-value industries, the innovation supports circular manufacturing loops by enabling clean separation of bonded interfaces, meeting both Extended Producer Responsibility (EPR) mandates and eco-design directives across the EU, North America, and Asia-Pacific.

Market Opportunity 2: High-Performance Moisture-Curing RHMAs Powering Prefabricated and Modular Construction

The global prefabricated construction industry, valued for its precision and efficiency, presents a major growth opportunity for high-strength, moisture-curing Reactive Hot Melt Adhesives (RHMAs). These adhesives provide the perfect combination of fast curing, durability, and environmental resistance needed for large-scale modular and off-site construction applications.

In a 2024 case study, a leading construction firm reported that adopting specialized RHMAs reduced component clamping time by 40% compared to traditional two-component structural adhesives, enabling faster assembly cycles and greater production throughput in factory environments. The accelerated workflow translates directly to lower labor costs, higher installation precision, and reduced energy use in the manufacturing process.

Unlike conventional polyurethane or epoxy adhesives, RHMAs form instant green bonds upon cooling, followed by a moisture-induced chemical crosslinking reaction, resulting in exceptional weather resistance and long-term elasticity. These properties make them ideal for laminated structural panels, façade systems, insulation bonding, and window assemblies used in modular housing and commercial infrastructure.

Further, their low VOC profile and solvent-free composition align with the green construction movement and regulatory frameworks such as the EU Construction Products Regulation (CPR) and LEED certification standards, reinforcing RHMAs’ pivotal role in sustainable, high-performance building solutions.

Competitive Landscape: Global Leaders Advancing Innovation and Sustainability in Reactive Hot Melt Adhesives

The Global Reactive Hot Melt Adhesives Market is led by a select group of high-performance manufacturers—including Henkel AG & Co. KGaA, H.B. Fuller Company, Bostik (Arkema Group), Sika AG, and Jowat SE—each leveraging innovation, sustainability, and regional expansion to strengthen market share. Their efforts center on decarbonized manufacturing, PUR formulation optimization, and high-speed bonding applications across automotive, packaging, and construction industries.

Henkel stands at the forefront of the RHMA sector with its globally recognized Technomelt and Loctite brands. The company’s strength lies in advanced PUR and polyolefin hot melt technologies for automotive and electronic applications. Its October 2025 partnership with Dow underscores a commitment to sustainability, integrating renewable electricity and low-carbon feedstocks to cut emissions by up to 40%. Henkel’s Technomelt E-COM range (Dec 2023) also reinforces its presence in high-speed e-commerce packaging, while its Loctite automotive potting adhesives (Aug 2024) support thermal management and durability in EV components.

H.B. Fuller is a pioneer in reactive hot melt crosslinking PUR adhesives engineered for demanding industrial and construction applications. The company’s acquisitions of Fourny NV (Feb 2022) and Apollo (Jan 2022) strengthened its European market leadership in commercial roofing and building adhesives. H.B. Fuller’s solutions deliver fast-bonding, solvent-free performance across technical textiles, electronics, and metal assembly. By emphasizing 100% solids RHMA formulations, the company continues to lead in VOC-free production, enabling energy-efficient, automated assembly lines for industrial customers.

Bostik, part of the Arkema Group, has cemented its position as a global smart adhesives leader, investing over 2.7% of its sales in R&D. The company’s elastic bonding and reactive hot melt solutions cater to transportation, flexible packaging, and construction, offering high thermal and mechanical resilience. Bostik’s automotive RHMA line plays a critical role in lithium-ion battery assembly (cell-to-pack), while its Kizen hot-melt series enables end-of-line packaging with exceptional temperature resistance (−40°F to 250°F). Its continued focus on durability, impact resistance, and lightweight bonding aligns perfectly with new mobility trends.

Sika AG maintains its leadership in specialty chemicals and reactive hot melt technologies through innovation in bonding, sealing, and structural adhesives. Its R&D-driven portfolio supports lightweight design and sustainable construction, addressing the growing demand for quick-curing PUR hot melts in door, window, and façade systems. By combining its RHM adhesives with sealant and structural adhesive technologies, Sika delivers integrated bonding systems for e-mobility, building components, and modular construction. The company’s focus on energy efficiency and durability positions it as a trusted partner in smart infrastructure development.

Jowat SE remains a specialist in woodworking, furniture, and textile adhesives, offering customized reactive hot melt solutions renowned for quality and compliance. Its Jowatherm-Reaktant MR 604.90 (Feb 2020) was the first low-monomer PUR adhesive to meet RAL-GZ 716 safety standards, ensuring hazard-free profile wrapping in PVC window systems. The company’s adhesives provide fast setting times, excellent moisture resistance, and high-temperature durability, ideal for edge banding and furniture assembly. Jowat’s continued investment in formulation optimization and technical support underscores its position as a process-efficiency partner for precision manufacturing clients.

Country Analysis: Regional Advancements and Strategic Developments in the Global Reactive Hot Melt Adhesives (RHMA) Industry

China: Rapid Expansion in PUR and POR Production Driven by EV Growth and Infrastructure Projects

China remains the world’s largest and fastest-growing market for Reactive Hot Melt Adhesives (RHMA), underpinned by strong government initiatives in construction, packaging, and electric vehicle (EV) manufacturing. In May 2025, Shandong ADINO New Materials Co., Ltd. inaugurated a major RHMA production facility in Linyi, representing a key milestone in China’s strategy to localize adhesive manufacturing and reduce dependency on imports. The expansion aligns with national goals to advance urbanization, infrastructure development, and sustainable construction, particularly in the packaging and woodworking sectors, where low-VOC, high-strength PUR hot melts are now in high demand.

The EV supply chain continues to serve as one of the country’s most dynamic demand drivers. With government incentives supporting EV adoption, manufacturers are rapidly incorporating structural PUR and Polyolefin Reactive (POR) adhesives in battery pack assembly, thermal insulation, and lightweight component bonding, essential for energy efficiency and safety compliance. Infrastructure megaprojects—such as high-speed rail and smart city construction—are fueling the uptake of moisture-resistant, high-performance RHMA formulations for laminations and sealants that withstand extreme environmental stress. Additionally, automation in packaging production has accelerated the demand for fast-curing PUR hot melts compatible with high-speed dispensing systems. Local R&D efforts are increasingly focusing on bio-based and recyclable RHMA chemistries, reinforcing China’s position as the Asia-Pacific leader in reactive adhesive technology innovation and sustainable manufacturing transformation.

Germany: European Hub for Next-Generation, REACH-Compliant Reactive Hot Melt Adhesives

Germany continues to lead Europe’s high-performance Reactive Hot Melt Adhesives (RHMA) sector, driven by its deep automotive engineering base and commitment to sustainable material innovation. In October 2024, Henkel AG & Co. KGaA announced a €20 million investment to expand and modernize its Bopfingen adhesives facility, strengthening production capacity for heat-resistant PUR and POR systems targeting high-end industrial and automotive applications. The country’s premium automotive OEMs are actively integrating advanced RHMA technologies for multi-material bonding in EV body-in-white structures, which improve vehicle strength, reduce mass, and meet EU crash safety standards.

Germany’s regulatory alignment with the EU’s Green Deal and REACH compliance framework is pushing adhesive formulators toward micro-emission and low-monomer PUR systems, ensuring enhanced worker safety and minimal volatile emissions. R&D collaborations between industry and academic institutes are also driving advancements in low-temperature dispensing PUR adhesives, tailored for heat-sensitive electronic modules like ADAS sensors and interior display assemblies. Furthermore, major European manufacturers are pioneering bio-based and recyclable RHMA products to support circular packaging goals for brands in the textiles, furniture, and consumer goods sectors. With its blend of precision engineering, sustainability leadership, and regulatory foresight, Germany remains the benchmark market for innovation in reactive adhesive chemistry.

United States: Pioneering High-Performance RHMA for Transportation, Electronics, and Sustainable Packaging

The U.S. Reactive Hot Melt Adhesives (RHMA) market is undergoing significant growth across transportation, electronics, healthcare, and packaging industries, fueled by strong R&D investments and sustainability mandates. H.B. Fuller Company continues to lead the expansion of high-performance PUR HMAs designed for medical device manufacturing, offering sterilization-resistant and biocompatible bonds suited for regulatory compliance in FDA-governed applications. Simultaneously, the construction and building materials sector is driving demand for fire-retardant reactive adhesives, aligning with new U.S. green building codes and insulation material standards.

In September 2024, a strategic partnership between a U.S. adhesives company and a UK-based manufacturer introduced biodegradable hot melt adhesives across North America, signifying a major step toward circular and eco-friendly packaging solutions. Trade and tariff adjustments have also encouraged nearshoring initiatives, spurring domestic production of PUR and polyolefin reactive adhesives to shorten supply chains and improve market agility. Moreover, the electronics segment is rapidly adopting low-temperature, high-tack RHMA formulations for delicate component bonding in miniaturized consumer and industrial devices. With strong corporate sustainability commitments and advanced material engineering, the United States continues to define global trends in sustainable, high-performance reactive adhesive innovation.

India: Accelerating Industrial Adoption Through Infrastructure, EV Manufacturing, and Localization Initiatives

India is rapidly emerging as a high-growth hub for Reactive Hot Melt Adhesives, driven by its industrial expansion and strong government-backed manufacturing ecosystem. The Production Linked Incentive (PLI) Scheme for Advanced Automotive Technology (AAT) is directly stimulating domestic adhesive demand by supporting EV and hydrogen fuel cell production, which rely heavily on structural PUR and POR adhesive systems for battery assembly and component encapsulation. Parallelly, India’s infrastructure boom—spanning metro rail, airports, and smart city projects—is increasing consumption of moisture-resistant RHMA for facade bonding, waterproof panel lamination, and insulation materials.

Foreign Direct Investment (FDI) inflows into construction and furniture manufacturing have also boosted local demand for PUR edgebanding adhesives, valued for their heat resistance, low stringing, and superior bond durability. The government’s “Make in India” initiative is further promoting technology transfer and local adhesive production, enabling manufacturers to reduce import dependency while customizing adhesive formulations for India’s diverse climatic and industrial conditions. As manufacturing sophistication increases, India is transitioning into a key production and export center for cost-effective, high-performance RHMA products, meeting the growing needs of packaging, automotive, and construction sectors.

France: Sustainable Adhesive Innovation Anchored by Specialty Chemical Leadership

France is positioning itself as a European leader in sustainable and specialty Reactive Hot Melt Adhesives, driven by Arkema Group’s Bostik division, which has prioritized bio-based and solvent-free bonding technologies. Bostik’s Polyurethane Reactive (PUR) and polyamide adhesive lines are central to France’s innovation ecosystem, targeting high-performance applications in technical textiles, automotive interiors, and flexible packaging. Ongoing R&D efforts are focused on eco-optimized RHMA formulations with increased bio-content and reduced VOCs, meeting France’s stringent national environmental policies and EU sustainability objectives.

The company’s continued investment in advanced production technologies enables energy-efficient, large-scale manufacturing of solvent-free lamination adhesives—critical for recyclable and mono-material packaging films. With The innovations, France not only strengthens its position in European sustainable adhesive production but also acts as a global export hub for performance-oriented and eco-compliant RHMA solutions, especially for textiles, packaging, and industrial bonding applications.

Japan: Precision Engineering in Non-Isocyanate Reactive Systems and Electronics Manufacturing

Japan remains a global pioneer in precision-grade Reactive Hot Melt Adhesives (RHMA), particularly in electronics, EV components, and high-speed automated assembly. Nitto Denko Corporation and other major domestic manufacturers are investing heavily in thermally conductive PUR adhesives, designed for efficient heat management in semiconductor modules, EV batteries, and compact power electronics. The country’s focus on automation and robotics has accelerated the adoption of ultra-fast-curing PUR HMAs compatible with high-speed industrial and electronic assembly lines, ensuring consistent bond strength and performance reliability.

Japan’s research institutions are spearheading advancements in Non-Isocyanate Polyurethane (NIPUR) technologies—next-generation reactive systems that eliminate isocyanates entirely, addressing worker safety and environmental compliance under future global chemical safety directives. The NIPUR formulations promise improved durability, recyclability, and environmental footprint reduction, aligning with Japan’s broader carbon neutrality and smart manufacturing goals. With a culture of high-precision engineering and R&D excellence, Japan continues to shape the next era of sustainable and high-efficiency reactive adhesive technologies for global applications in electronics, automotive, and industrial sectors.

Reactive Hot Melt Adhesives Market Report Scope

Reactive Hot Melt Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2034)

|

$9.2 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Resin Type (Polyurethane, Polyolefin, Others), By Substrate (Wood and Wood Composites, Plastics, Metals, Textiles and Nonwovens, Other Substrates), By Application (Automotive and Transportation, Construction and Building, Furniture and Woodworking, Packaging, Textile and Footwear, Electrical & Electronics, Nonwoven Hygiene, Others), By Curing Mechanism (Single-Component, Two-Component

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema Group (Bostik), 3M Company, Jowat SE, Dow Inc., DuPont de Nemours, Inc., Wacker Chemie AG, Lohmann GmbH & Co. KG, Ashland Global Holdings Inc., Mapei S.p.A., DELO Industrial Adhesives LLC, BASF SE, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Polyurethane

- Polyolefin

- Others

By Substrate

- Wood and Wood Composites

- Plastics

- Metals

- Textiles and Nonwovens

- Other Substrates

By Application/End-Use Industry

- Automotive and Transportation

- Construction and Building

- Furniture and Woodworking

- Packaging

- Textile and Footwear

- Electrical & Electronics

- Nonwoven Hygiene

- Others

By Curing Mechanism

- Single-Component

- Two-Component

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Reactive Hot Melt Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Arkema Group (Bostik)

- 3M Company

- Jowat SE

- Dow Inc.

- DuPont de Nemours, Inc.

- Wacker Chemie AG

- Lohmann GmbH & Co. KG

- Ashland Global Holdings Inc.

- Mapei S.p.A.

- DELO Industrial Adhesives LLC

- BASF SE

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

Developed by USDAnalytics, this report investigates the Reactive Hot Melt Adhesives (RHMA) Market with a practitioner lens—linking demand from automotive, construction, electronics, furniture/woodworking, packaging, nonwovens, and textiles to resin choices, curing routes, and line-speed economics; it delivers analysis reviews of PUR and polyolefin performance on plastics, metals, wood, and technical textiles, and highlights breakthroughs in high-temperature stability, low-monomer safety, non-isocyanate concepts, recyclable chemistries, and debond-on-demand solutions that enable circular manufacturing. Benchmarking adoption in EV battery, interior trim, modular construction, and high-throughput packaging, we map specification drivers (green strength, final strength, heat/chemical resistance, VOC/IAQ compliance, and automation readiness) to purchasing criteria and total cost of ownership—making this report an essential resource for sourcing leaders, application engineers, product managers, and investors who need defensible forecasts, competitive intelligence, and standards alignment across global supply chains.

Scope Highlights

Segmentation:

- By Resin Type: Polyurethane; Polyolefin; Others.

- By Substrate: Wood & Wood Composites; Plastics; Metals; Textiles & Nonwovens; Other Substrates.

- By Application/End-Use Industry: Automotive & Transportation; Construction & Building; Furniture & Woodworking; Packaging; Textile & Footwear; Electrical & Electronics; Nonwoven Hygiene; Others.

- By Curing Mechanism: Single-Component; Two-Component.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies Covered: Analysis/profiles of 15+ companies (global leaders and regional specialists).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.