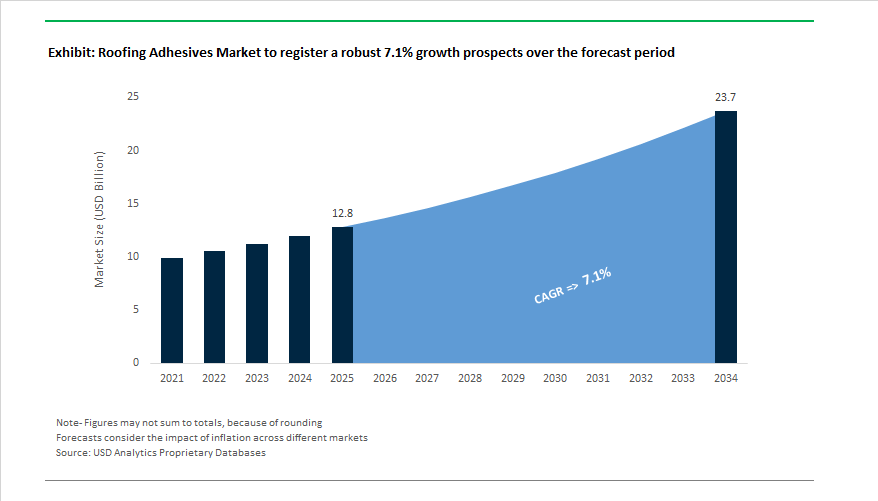

The Global Roofing Adhesives Market is projected to expand from USD 12.8 billion in 2025 to USD 23.7 billion by 2034, growing at a CAGR of 7.1%, as roofing systems transition toward mechanically fastener-free, energy-efficient, and wind-resilient designs. Growth is structurally linked to urban reroofing cycles, tightening building energy codes, and the rising specification of single-ply membranes and insulated roofing assemblies in commercial and industrial construction. Roofing adhesives are increasingly evaluated for uplift resistance, long-term adhesion under thermal cycling, and compatibility with low-carbon building envelopes.

From a technology standpoint, polyurethane roofing adhesives dominate high-performance applications due to their fast green strength, moisture tolerance, and ability to bond dissimilar substrates such as concrete, steel decks, polyiso insulation, and TPO/PVC membranes. Manufacturers such as Carlisle Construction Materials, Sika, SOPREMA, Henkel, and H.B. Fuller have expanded portfolios of two-component and low-rise foam PU adhesives designed to meet FM Global and UL wind uplift standards, often exceeding traditional mechanically fastened systems in uplift performance. These adhesive systems are increasingly specified in hurricane- and high-wind zones, where reduced point loading and continuous bonding improve roof system integrity and lifecycle reliability.

Sustainability and labor efficiency are reinforcing adoption. Low-VOC and solvent-free roofing adhesives are gaining preference as contractors and asset owners align with LEED, ENERGY STAR®, and regional green building requirements, particularly for occupied buildings where odor and indoor air quality are critical considerations. Water-based and low-monomer PU formulations allow installation without hot work, reducing fire risk and insurance constraints while accelerating project timelines. At the same time, adhesive-bonded roofing systems reduce thermal bridging and fastener penetration, supporting higher overall R-value performance and improved building energy efficiency.

The market is also being shaped by the renovation-led nature of roofing demand, especially in North America and Europe, where aging commercial roofs are being upgraded rather than replaced structurally. Adhesive systems enable overlay and recover applications without full tear-off, lowering waste generation and minimizing downtime for facilities such as warehouses, hospitals, and data centers. As roofing assemblies become more integrated with solar installations and rooftop equipment, adhesives are increasingly treated as load-distributing structural layers rather than secondary consumables.

The global roofing adhesives market has entered a transformative phase where sustainability, digital construction technology, and supply chain optimization define corporate strategies. The industry is witnessing a series of mergers, acquisitions, and product launches reflecting a strong move toward eco-efficient materials and system-integrated roofing solutions.

In March 2025, H.B. Fuller unveiled its Millennium PG-1 EF ECO2 adhesive, a commercial-grade product powered by ECO2 Driven™ technology. This system utilizes naturally occurring atmospheric gases as a propellant instead of high-GWP chemical blowing agents, eliminating harmful emissions while maintaining superior bonding performance for insulation boards and single-ply membranes. The innovation highlights a significant step toward low-VOC roofing adhesives aligned with EPA and CARB environmental standards.

In April 2025, Sika AG strengthened its presence in the UK roofing systems market through the acquisition of Cromar Building Products, expanding its distribution network and product reach for roofing adhesives, sealants, and waterproofing solutions. Later, in January 2025, the company acquired Elmich Pte Ltd (Singapore), enhancing its Asia-Pacific roofing portfolio and tapping into the growing demand for urban greening and sustainable rooftop systems. Sika also made a strategic investment in Giatec™ Scientific (June 2025)—a leader in digital concrete technologies—signaling its commitment to smart construction integration and real-time adhesive performance monitoring.

H.B. Fuller further advanced its sustainability agenda in June 2025 through global operational upgrades, including new eco-efficient production lines in Cairo, Germany, and the UAE, aimed at reducing carbon emissions and water consumption across manufacturing facilities. Meanwhile, APPLIED Adhesives (July 2025) bolstered its North American footprint with the acquisition of BTmix, expanding its custom adhesive formulation and distribution network across the industrial and construction segments.

Continuous R&D innovation remains a defining theme, particularly with Sika’s Purform® polyurethane technology (2024–2025)—a next-generation chemistry with ultra-low monomeric diisocyanate content. This formulation aligns with European REACH compliance, significantly improving worker safety while maintaining high performance in adhesive and sealant applications.

Market Trend 1: Low-VOC, Water-Based Roofing Adhesives Gain Momentum Amid Global Air Quality Regulations

A dominant shift is occurring across the roofing adhesives market, driven by the tightening of air quality and emission control standards globally. Regulatory agencies like the U.S. Environmental Protection Agency (EPA) and European Chemicals Agency (ECHA) are setting stringent limits on volatile organic compound (VOC) content, catalyzing a transition away from solvent-based adhesives toward water-based and bio-based alternatives.

The trend aligns closely with the increasing emphasis on Indoor Environmental Quality (IEQ) and green building certification systems such as LEED v4.1 and BREEAM, which reward the use of low-emitting materials in roofing assemblies. Under California’s CDPH Standard Method v1.2–2017, roofing adhesives must limit Total VOC emissions to ≤0.5 mg/m³ after 28 days to qualify for premium certification.

To maintain market access in major construction hubs like California, the EU, and Japan, adhesive manufacturers are rapidly scaling their waterborne polyurethane (PU) and acrylic emulsion-based systems. A leading chemical company recently introduced a bio-based one-component polyurethane adhesive containing ≈63% renewable organic mass, achieving a ≈66% reduction in CO₂ emissions compared to conventional formulations. The directly supports green procurement initiatives and "Buy Clean" policies mandating low-embodied carbon construction materials.

The growing adoption of these low-VOC systems is transforming roofing adhesive selection criteria, making sustainability compliance and environmental certification as critical as bond strength or cure speed in both commercial and residential construction sectors.

Market Trend 2: Fully-Adhered Roofing Systems Outperform Mechanical Fastening in Wind Resistance and Longevity

Climate change and the rising frequency of hurricane-intensity wind events are accelerating the adoption of adhesive-applied, fully-adhered roofing systems over mechanically fastened alternatives. The transition is especially critical for commercial and industrial buildings located in coastal and high-wind zones, where roofing failure poses major safety and insurance risks.

Adhesive-applied membranes, such as thermoplastic polyolefin (TPO) and polyvinyl chloride (PVC) single-ply sheets, provide superior wind uplift resistance by distributing stress evenly across the substrate. Testing by FM Global and other standards bodies confirms that fully adhered systems can achieve wind uplift ratings as high as FM 1-225, outperforming mechanically attached systems that often struggle to meet FM 1-150 standards in perimeter and corner zones.

Further, adhesive-applied systems reduce seam frequency by enabling the use of wider membrane rolls, minimizing leak-prone joints and ensuring consistent waterproofing integrity. Recent product innovations have also solved one of the industry’s persistent challenges—cold-weather installation limits. Modern low-odor, low-VOC poly-based adhesives cure effectively at −4°C (25°F), extending the roofing season and reducing costly weather-related delays.

These advancements make fully adhered single-ply membranes the preferred specification in large-scale projects requiring both durability and environmental compliance. As insurers and regulators tighten resilience standards, adhesive technologies will continue to drive wind-resistant, energy-efficient roofing system adoption worldwide.

Market Opportunity 1: Adhesive Solutions for Non-Penetrating Photovoltaic (PV) Mounting Systems

The global boom in rooftop solar installations is generating a high-value opportunity for roofing adhesives engineered for photovoltaic (PV) integration. Traditional mechanical PV mounts, which require roof penetration, compromise membrane integrity and void warranties. The next generation of adhesive-based, non-penetrating PV attachment systems is resolving the issue by enabling durable, watertight bonding that preserves the roof’s structural and warranty performance.

Adhesive manufacturers are developing elastomeric bonding agents and pressure-sensitive adhesive (PSA) tapes for use with flexible thin-film PV modules and Building-Integrated Photovoltaics (BIPV). These systems must perform reliably under extreme UV exposure, thermal cycling, and wind uplift conditions. Research and field data show that advanced silicone-based adhesives retain ≈95% elasticity after over 10 years of solar exposure, withstanding temperature extremes from −59°C to 260°C.

In addition, the emergence of pre-applied adhesive flashings is revolutionizing on-site installation efficiency. These systems, where butyl-based sealants are pre-bonded to PV mounting bases, eliminate curing time and reduce the risk of human error, ensuring faster, consistent installations.

As governments and corporations push for net-zero energy buildings, adhesive bonding technologies are poised to become the backbone of next-generation solar roofing systems, integrating energy generation seamlessly with long-term waterproofing and durability.

Market Opportunity 2: Formulation of Bio-Based and Low-Carbon Roofing Adhesives for Sustainable Construction

As the construction sector accounts for approximately 37% of global CO₂ emissions, the demand for bio-based and low-carbon roofing adhesives is intensifying under government "Buy Clean" procurement policies and corporate ESG frameworks. These policies encourage contractors to select materials verified for reduced embodied carbon and renewable content.

Manufacturers are focusing on renewable polyol chemistry, producing polyurethane adhesives with >70% bio-based content, verified under ISCC PLUS certification. These adhesives are not only solvent-free and low-VOC, but also deliver comparable or superior performance to fossil-based formulations in terms of adhesion, elasticity, and aging resistance.

In addition, life cycle assessments (LCAs) report that replacing petroleum-derived components with renewable feedstocks can yield up to a 62% reduction in CO₂ emissions per unit of adhesive produced. These bio-based formulations contribute directly to Scope 3 emission reductions for construction firms seeking LEED and ISO 14040 compliance.

From a performance standpoint, bio-polyurethane roofing adhesives also exhibit better moisture tolerance and long-term thermal stability, making them particularly suited for insulation board attachment and reflective cool roof systems. As sustainability becomes a competitive differentiator, bio-based adhesive systems will define the next generation of roofing material innovation.

Roofing Adhesives Market Share Insights, 2025-2034

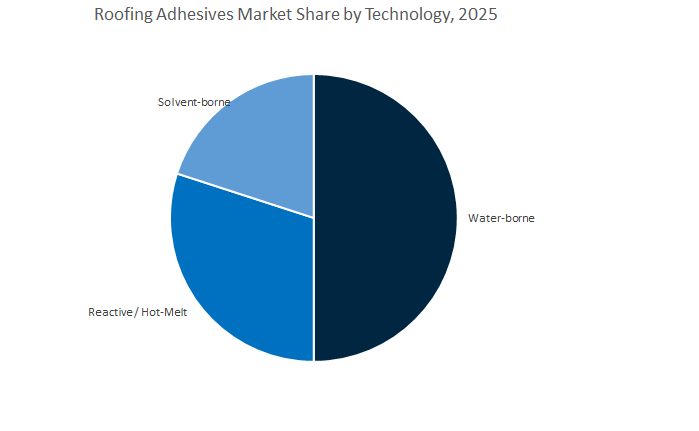

Market Share by Technology

Water-borne roofing adhesives dominate the global market with a projected 48.6% share in 2025, reflecting the industry’s decisive shift toward environmentally sustainable and low-VOC formulations. The growing emphasis on green construction standards, LEED certification, and eco-friendly roofing systems has significantly accelerated the adoption of water-borne technologies in both commercial and residential applications. These adhesives deliver strong bonding performance, superior weather resistance, and excellent compatibility with a wide range of roofing substrates, including EPDM, TPO, and PVC membranes. The dominance of this segment is further supported by regulatory initiatives in North America and Europe that restrict solvent emissions, compelling manufacturers and roofing contractors to transition toward water-based chemistries.

Meanwhile, Reactive and Hot-Melt roofing adhesives are emerging as the fastest-growing technologies, driven by their rapid curing properties, exceptional strength, and superior durability in extreme weather environments. They are increasingly used in high-performance roofing systems requiring immediate handling strength—particularly in industrial and large-scale commercial projects where downtime and application time must be minimized. Their robust adhesion to metal, concrete, and foam substrates makes them indispensable in flat roofing, insulation attachment, and edge sealing applications. On the other hand, Solvent-borne adhesives—once a dominant formulation—are witnessing a gradual decline due to VOC concerns and evolving occupational safety regulations. However, they remain relevant in specific environments such as cold-weather roofing installations, where fast evaporation rates are advantageous for consistent bond strength.

Market Share by Application

Roof Membrane Adhesion stands as the largest application segment, commanding a 37.2% share of the roofing adhesives market in 2025, primarily driven by the widespread use of single-ply roofing systems (TPO, PVC, EPDM) across industrial, commercial, and institutional buildings. These membranes require high-performance adhesives that can provide durable, weatherproof bonds while withstanding mechanical stress, UV radiation, and temperature fluctuations. The expansion of commercial real estate and the rise of energy-efficient roofing systems, such as cool roofs and solar-integrated membranes, have further propelled this segment’s dominance. Roofing adhesives play a critical role in ensuring structural integrity and long-term waterproofing, reducing the need for mechanical fasteners and enhancing insulation performance.

The Insulation Board Attachment segment follows closely, supported by the global focus on thermal efficiency and sustainable construction practices. Polyurethane and water-borne adhesives are extensively used for bonding foam insulation boards (polyiso, EPS, XPS) to various substrates, providing strong adhesion without thermal bridging. Flashings and Seaming applications account for a significant market portion, ensuring watertight performance around roof penetrations, parapets, and joints—crucial for long-term system reliability in high-rainfall or hurricane-prone regions. Deck-to-Deck and Substrate Bonding serve specialized structural purposes, especially in retrofitting or multi-layer roof assemblies requiring mechanical reinforcement. Meanwhile, Coating and Repair applications are gaining traction in the aftermarket and roof maintenance sector, where liquid-applied adhesives and hybrid sealant systems are used for restoration, leak prevention, and performance extension of aging roofs.

The competitive environment of the global roofing adhesives industry is dominated by multinational giants such as H.B. Fuller, Sika AG, Arkema (Bostik), 3M Company, and Dow Inc., each leveraging advanced chemistry, sustainable innovation, and geographic expansion to strengthen market share. These companies are transitioning from traditional adhesive manufacturing to smart, integrated system solutions that combine durability, environmental responsibility, and performance efficiency.

H.B. Fuller remains the largest pure-play adhesives manufacturer globally, with a focus on sustainable and contractor-centric solutions. The company’s Millennium PG-1 EF ECO2 roofing adhesive (launched in March 2025) represents a major advancement in sustainable formulation, utilizing CO₂ propellant technology to eliminate harmful GWP chemicals. Its product line caters to commercial roofing systems, including insulation boards, cover boards, and single-ply membranes (EPDM, TPO, PVC). With over $3.6 billion in 2024 revenue, H.B. Fuller continues to lead in low-VOC roofing solutions and rapid-deployment adhesive systems that align with modern construction practices.

Sika AG, a leading force in construction adhesives and waterproofing systems, continues to dominate through integrated roofing solutions such as Sikaflex® and SikaTack®, alongside specialized adhesives for TPO and bituminous membranes. The company’s acquisitions of Cromar Building Products (April 2025) and Elmich Pte Ltd (January 2025) expanded its reach in the UK and Asia-Pacific roofing markets, respectively. Additionally, Sika’s investment in Giatec™ Scientific (June 2025) underscores its ambition to digitize adhesive performance monitoring. Backed by its global footprint and the successful integration of MBCC (July 2025), Sika remains the benchmark for construction chemicals innovation and system-level roofing solutions.

Through its Bostik division, Arkema S.A. has positioned itself as a pioneer in smart adhesives for building and construction markets. Bostik’s roofing adhesive portfolio spans polyurethane, Silyl Modified Polymer (SMP), and waterproofing formulations, designed for green building compliance and thermal performance. Leveraging Arkema’s expertise in specialty polymers, Bostik’s R&D initiatives—like its 2KPU® adhesive platform—enable high-performance bonding in complex roofing and insulation systems. The Smart House testing facility in France validates next-gen adhesives under real-world conditions, supporting the company’s vision of energy-efficient, low-emission roofing systems.

3M utilizes its proprietary expertise in precision coating, film processing, and microreplication technologies to deliver high-durability adhesives and roofing materials. Its roofing product portfolio includes Cool Color Roofing Granules for solar reflectivity, industrial tapes, and adhesive-backed protective films used in roofing assemblies. In 2024, 3M achieved a 59.1% reduction in greenhouse gas emissions since 2019 (SBTi-validated), underscoring its leadership in sustainability. The company’s ability to merge adhesive technology with energy efficiency materials makes it a leading innovator in next-generation reflective and adhesive-integrated roofing systems.

Dow Inc., one of the largest global suppliers of polyurethane raw materials and elastomeric systems, continues to shape the roofing adhesives sector through its focus on polyols, MDI, and acrylic-based chemistries. Dow’s Building Solutions division enables the formulation of durable, energy-efficient polyurethane adhesives and coatings, improving the weather resistance and insulation performance of roofing systems. Its current R&D initiatives emphasize bio-based inputs, circular raw materials, and polyurethane innovation aimed at reducing embodied carbon in construction. Through collaborations across the building materials value chain, Dow is redefining sustainability in adhesive-enabled roofing envelopes.

Country Analysis: Strategic Regional Hubs Driving Innovation and Growth in the Global Roofing Adhesives Market

United States: Low-VOC Formulations and Growth in TPO Roofing Adhesives

The United States roofing adhesives market is at the forefront of low-VOC compliance, technological innovation, and energy-efficient roofing system integration. Driven by evolving EPA emission standards, particularly the 2025 National VOC Emission Standards for Aerosol Coatings, adhesive manufacturers are pivoting toward low-reactivity, solvent-free polyurethane and silicone systems. Polyurethane (PU) foam adhesives dominate commercial flat roofing applications, particularly for attaching Polyiso and PIR insulation boards, as contractors increasingly prefer one- and two-component reactive systems for their fast cure times, thermal resistance, and high bond strength.

Key players such as 3M Co. continue to innovate with next-generation adhesives like Fastbond Insulation Adhesive 49, enhancing productivity for insulation attachment in large-scale construction projects. The shift toward fully adhered TPO and PVC membranes is reshaping adhesive demand, requiring UV-resistant, elastomeric bonding formulations that ensure long-term durability under varying climate conditions. The acquisition of HPS North America, Inc. in 2024 has bolstered U.S. distribution networks for high-performance adhesives, strengthening the domestic supply chain for construction chemicals. Additionally, residential roofing renovation is increasingly adopting liquid-applied polyurethane and silicone adhesives, emphasizing seamless waterproofing, energy efficiency, and extended roof lifespan. With local companies like Tropical Roofing Products, Inc. introducing innovative repair solutions such as Rx Roof Repair (2024), the U.S. roofing adhesives sector continues to lead in sustainability, VOC compliance, and application efficiency.

China: Infrastructure Expansion and the Rise of PU and Epoxy Roofing Adhesives

China remains the world’s largest construction market and an epicenter for polyurethane and epoxy roofing adhesive production. As urbanization and infrastructure investments accelerate, demand for high-performance roofing adhesives is rising sharply across commercial, industrial, and public infrastructure projects. Moisture-cure polyurethane adhesives are rapidly replacing bituminous materials, offering high humidity tolerance and superior adhesion to substrates like metal, concrete, and membranes. A global adhesives manufacturer expanded its Xi’an production facility in 2024, manufacturing tile adhesives and cementitious waterproofing compounds for domestic consumption, demonstrating China’s growing local manufacturing capacity.

The Chinese epoxy adhesive segment is gaining traction for industrial roofing systems, where chemical resistance and structural strength are critical. The government’s public building refurbishment initiatives across tier-two cities emphasize low-odor, waterborne adhesive formulations that align with national emission reduction policies. Moreover, local manufacturers are investing heavily in localized supply chains to reduce dependency on imported bonding agents. The rise of liquid-applied roofing systems and polymer-modified bitumen (ModBit) adhesives further underscores China’s transformation into a technology-driven, sustainable construction hub. The integration of advanced PU and epoxy adhesives with smart application technologies positions China as a dominant global exporter of roofing adhesive systems in the coming years.

Germany: Energy Efficiency, Silicone Adhesives, and Green Building Leadership

Germany continues to set global standards for green building adhesives, driven by the European Union’s Energy Performance of Buildings Directive (EPBD) and the REACH regulatory framework. The market is characterized by strong demand for low-VOC, high-resilience adhesives used in energy-efficient roofing insulation systems to minimize thermal loss and achieve near-zero energy building standards. Major German firms are leading innovations in silicone-based and hybrid polyurethane adhesives, prized for their exceptional UV resistance, elasticity, and long-term durability under Europe’s variable climate conditions.

Recent developments include the introduction of sustainable epoxy hardeners through collaborations between leading material science companies, targeting eco-friendly roofing applications. Manufacturers are scaling up cold-applied liquid roofing systems (LQD-PUR) using single-component polyurethane adhesives, offering flame-free, fast-curing waterproofing solutions that improve installation safety. Facility modernization projects across Germany and wider Europe are focused on increasing output of advanced hybrid adhesives to meet rising regional demand. Germany’s strong emphasis on carbon-neutral construction materials, paired with stringent environmental standards, reinforces its position as the leading European hub for next-generation roofing adhesives and sealants.

United Kingdom: Cold-Applied Systems and Growth in Re-Roofing Applications

The U.K. roofing adhesives industry is undergoing a rapid transformation driven by renovation and re-roofing projects, where contractors prioritize time-efficient, moisture-tolerant adhesives. The surge in demand for liquid-applied polyurethane systems—especially LQD-PUR single-component adhesives—reflects a growing preference for low-VOC, cold-applied bonding technologies that minimize disruption during installation. A recent acquisition by a global construction chemical company of a prominent U.K. roofing supplier has significantly expanded the distribution network and portfolio diversity, reinforcing supply for large-scale commercial projects.

The U.K. government’s increased infrastructure investment, coupled with stricter fire safety regulations, is propelling the use of non-flammable, high-durability adhered roofing systems in residential and industrial applications. The market is also witnessing innovation in hybrid polyurethane and silicone formulations, designed for consistent curing in damp environments. With growing adoption in retrofit energy efficiency projects and smart city developments, the U.K. roofing adhesives market is establishing itself as a key European destination for cold-applied and hybrid adhesive systems that combine sustainability, compliance, and installation speed.

India: Urbanization, Commercial Construction, and Bio-Based Adhesive Innovation

India’s roofing adhesives market is expanding rapidly under the influence of urban infrastructure growth, industrialization, and government-led development programs. The Smart Cities Mission and National Infrastructure Pipeline (NIP) are driving large-scale construction projects across hospitals, commercial complexes, and logistics facilities, where polyurethane adhesives are increasingly preferred for their bonding strength, thermal insulation, and waterproofing performance. Contracts exceeding USD 670 million were secured in 2024 for new construction, underlining the expanding domestic consumption of roofing insulation adhesives.

The market is witnessing a dual trend of international investment and local innovation, as global players strengthen their Indian presence with sustainable, region-specific adhesive formulations. Bio-based and natural adhesives—derived from asphalt, starch, and organic polymers—are gaining momentum as cost-effective, eco-conscious alternatives for roofing applications. Meanwhile, industrial warehousing and logistics projects are fueling adoption of fully adhered roofing systems, requiring high-performance adhesives for SBS-modified bitumen membranes. The focus on energy-efficient, waterproof roofing systems and Make-in-India-backed production capacity expansions ensures India’s continued ascent as one of the fastest-growing roofing adhesive markets in Asia-Pacific.

Switzerland: Global Innovation Hub and R&D Leadership in Sustainable Roofing Adhesives

Switzerland stands as a global innovation center for roofing adhesives, housing one of the world’s leading specialty chemical corporations known for pioneering polyurethane, acrylic, and silicone adhesive technologies. The company’s ongoing R&D initiatives focus on low-carbon, high-durability chemistries, aligning with the global sustainability shift in construction materials. Strategic acquisitions, including the purchase of a green roof provider in Singapore and a mortar manufacturer in Denmark, demonstrate its efforts to expand globally while enhancing its roofing and building envelope product portfolio.

The company’s 2024 announcements underscore targeted investments in production facilities across Singapore, Kazakhstan, and China, reinforcing its presence in high-growth emerging markets. Furthermore, the integration of MBCC’s global operations has significantly strengthened its construction adhesive and sealant portfolio. Switzerland is also spearheading digital transformation in construction, partnering with technology firms to develop IoT-enabled adhesive systems capable of real-time monitoring. Collaborative efforts with BASF in 2025 to launch an eco-friendly epoxy hardener further highlight Switzerland’s leadership in sustainable, high-performance adhesive chemistry. As the center for advanced adhesive research and global expansion, Switzerland continues to shape the future of roofing adhesives through innovation, sustainability, and smart construction integration.

Roofing Adhesives Market Report Scope

Roofing Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.8 Billion

|

|

Market Size (2034)

|

$23.7 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Resin Type (Polyurethane, Epoxy, Silicone, Acrylic, Other Resin Types), By Technology (Water-borne, Solvent-borne, Reactive / Hot-Melt), By Application (Roof Membrane Adhesion, Insulation Board Attachment, Deck-to-Deck/Substrate Bonding, Flashings and Seaming, Coating and Repair), By End-User Industry (Non-Residential/Commercial, Residential, Infrastructure

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, H.B. Fuller Company, Henkel AG & Co. KGaA, The Dow Chemical Company, BASF SE, 3M Company, Arkema SA (Bostik), Carlisle Companies Inc., GAF Materials LLC, Huntsman Corporation, Wacker Chemie AG, MAPEI S.p.A., Johns Manville, DuPont de Nemours Inc., OMG Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Polyurethane

- Epoxy

- Silicone

- Acrylic

- Other Resin Types

By Technology

- Water-borne

- Solvent-borne

- Reactive / Hot-Melt

By Application

- Roof Membrane Adhesion

- Insulation Board Attachment

- Deck-to-Deck/Substrate Bonding

- Flashings and Seaming

- Coating and Repair

By End-User Industry

- Non-Residential/Commercial

- Residential

- Infrastructure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Roofing Adhesives Market

- Sika AG

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- The Dow Chemical Company

- BASF SE

- 3M Company

- Arkema SA (Bostik)

- Carlisle Companies Inc.

- GAF Materials LLC

- Huntsman Corporation

- Wacker Chemie AG

- MAPEI S.p.A.

- Johns Manville

- DuPont de Nemours Inc.

- OMG Inc.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Roofing Adhesives Market from resin chemistries to application workflows, delivering analysis reviews on adoption drivers, specification trends, cost-of-install impacts, and regulatory risks; it highlights breakthroughs in low-VOC and CO₂-propelled systems, high-bond PUR solutions for single-ply membranes, cold-weather cure technologies, and fully-adhered assemblies that lift wind-uplift performance and lifecycle watertightness; benchmarking supplier strategies, channel moves, and certification pathways, the study maps how sustainability mandates and digital jobsite practices are redefining product selection across commercial, residential, and infrastructure projects—this report is an essential resource for procurement leaders, technical specifiers, OEMs, and contractors seeking decision-grade insights through 2034.

Scope Highlights

Segmentation:

- By Resin Type: Polyurethane; Epoxy; Silicone; Acrylic; Other Resin Types.

- By Technology: Water-borne; Solvent-borne; Reactive / Hot-Melt.

- By Application: Roof Membrane Adhesion; Insulation Board Attachment; Deck-to-Deck/Substrate Bonding; Flashings and Seaming; Coating and Repair.

- By End-User Industry: Non-Residential/Commercial; Residential; Infrastructure.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies (global and regional leaders across roofing adhesives value chains).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.