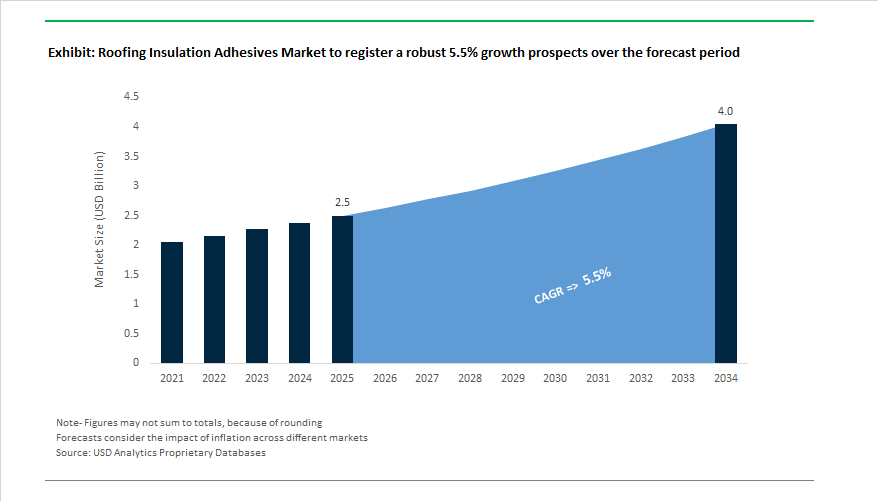

The Global Roofing Insulation Adhesives Market is forecast to expand from $2.5 billion in 2025 to $3.8 billion by 2034, growing at a CAGR of 5.5%. This steady growth trajectory is driven by the global construction sector’s transition toward energy-efficient roofing systems, green building certification compliance, and low-VOC insulation adhesives that support next-generation continuous insulation systems. Roofing insulation adhesives play a crucial role in bonding rigid foam insulation boards—such as Polyisocyanurate (PIR), Extruded Polystyrene (XPS), and Expanded Polystyrene (EPS)—to roof decks, eliminating thermal bridging and improving both structural integrity and building envelope performance.

North America remains a dominant market, led by surging demand for high-performance polyurethane adhesives tailored for low-slope commercial roofing applications. The adoption of cool roofs, vegetative roofs, and reflective coatings is fueling the need for adhesives that exhibit high bond strength, cold-weather flexibility, and compatibility with diverse substrates such as gypsum boards and mineral wool insulation.

Simultaneously, sustainability regulations are accelerating the shift away from high-GWP propellants toward eco-friendly adhesive chemistries. Modern canister-based roofing adhesive systems utilizing CO₂ and naturally occurring atmospheric gases (such as H.B. Fuller’s patented ECO2 Driven™ technology) are replacing older solvent-based alternatives, marking a key step toward environmental compliance and net-zero building goals.

The commercial construction sector — including logistics hubs, data centers, and large healthcare facilities — accounts for the majority of insulation adhesive consumption, given its need for high wind uplift performance and non-mechanical fastening to preserve thermal continuity. Meanwhile, Asia-Pacific is witnessing rapid market growth as infrastructure investment in China, India, and Southeast Asia drives the use of cost-effective bitumen-based and water-based adhesives for roofing insulation in harsh climatic environments.

The Roofing Insulation Adhesives Industry is undergoing rapid transformation, driven by innovation in low-VOC formulations, sustainable manufacturing, and digitalized construction technologies. Major players are realigning their portfolios, expanding production capacity, and introducing new chemistries that comply with stringent environmental and energy-efficiency standards.

In March 2025, H.B. Fuller launched the Millennium PG-1 EF ECO2™, a canister-based sprayable roofing adhesive featuring its patented ECO2 Driven™ technology. This innovation replaces traditional high-GWP chemical propellants with naturally occurring atmospheric gases, significantly reducing environmental impact while improving spray pattern precision and installation efficiency. The adhesive is optimized for bonding polyisocyanurate (PIR) insulation boards in low-slope commercial roofing and directly supports carbon footprint reduction initiatives in North America.

In March 2025, Sika AG expanded its roofing systems business with the acquisition of Cromar Building Products in the UK, strengthening its distribution footprint and product synergies in sealants and adhesives. Similarly, GAF (Standard Industries) introduced its EnergyGuard™ NH TCPP-Free Polyiso insulation product line in February 2025, setting a new industry standard for sustainable roofing insulation. The new offering eliminates potentially hazardous tris(1-chloro-2-propyl) phosphate (TCPP) flame retardants, increasing the demand for chemically compatible, environmentally safe adhesives for insulation attachment.

In August 2024, Sika AG expanded its Bekasi, Indonesia plant, doubling mortar and adhesive production to meet Southeast Asia’s infrastructure boom, while Huntsman Corporation (June 2024) held a major industry briefing emphasizing compliance with the EU’s Revised Construction Products Regulation (CPR) — a move directly influencing product development in polyurethane foam insulation adhesives. In April 2024, Sika further diversified by acquiring Kwik Bond Polymers (KBP) in the U.S., a leader in polymer systems for infrastructure repair, strengthening its expertise in high-performance resin and adhesive systems applicable to roofing and insulation.

By July 2025, Dow Inc. reported portfolio optimization actions in its European operations under its Polyurethanes & Construction Chemicals division, streamlining its focus on high-margin insulation adhesives and advanced polyurethane technologies. Meanwhile, H.B. Fuller (September 2025) reinforced its sustainability-driven innovation agenda, emphasizing low-VOC, HFO-free adhesive systems tailored for future-ready building standards.

Market Trend 1: Regulatory Mandates Accelerate the Transition Toward Ultra-Low VOC and HAPs-Free Roofing Adhesives

The roofing insulation adhesives market is being reshaped by tightened environmental regulations, compelling manufacturers to shift from solvent-heavy formulations to water-based, high-solids, and reactive polyurethane systems that meet evolving standards on volatile organic compound (VOC) and hazardous air pollutant (HAP) emissions.

Under the U.S. Environmental Protection Agency’s (EPA) Clean Air Act and its National Emission Standards for Hazardous Air Pollutants (NESHAP), adhesives used in construction and manufacturing must increasingly conform to emissions thresholds as low as 50 g/L or approach zero-VOC levels. Similarly, Europe’s REACH Regulation is restricting the use of high-toxicity solvents and reactive intermediates, leading to a significant rise in non-flammable, sustainable adhesive technologies suitable for large-scale commercial roofing projects.

In parallel, green building certifications such as LEED v4.1, WELL Building Standard, and BREEAM are driving a surge in demand for low-emitting roofing materials. To qualify under the California Department of Public Health (CDPH) Standard Method v1.2–2017, roofing insulation adhesives must limit total VOC emissions to ≤0.5 mg/m³ after 28 days. The has pushed manufacturers to prioritize formaldehyde-free, HAPs-free polyurethane and waterborne acrylic chemistries that achieve strong adhesion with minimal environmental impact.

For instance, a leading global chemical producer recently introduced a water-based polyurethane adhesive with a bio-based content exceeding 60%, achieving both EPA NESHAP compliance and a 66% reduction in CO₂ emissions relative to conventional solvent-based formulations. These regulatory-driven innovations not only mitigate air quality risks but also create a competitive advantage in regions adopting carbon disclosure and procurement transparency policies for construction materials.

Market Trend 2: Spray-Applied, High-Traction Adhesives Revolutionizing Roofing Installation Efficiency

The industry-wide labor shortage and the rising cost of skilled roofing contractors are accelerating the adoption of spray-applied insulation adhesives that dramatically improve productivity and coverage rates. Unlike traditional trowel- or roller-applied systems, two-component spray polyurethane (SPF) adhesives enable faster curing, uniform bonding, and superior traction across large roofing surfaces.

Field data shows that trained applicators can achieve coverage of 2,500–3,500 square feet per day using modern spray foam systems—nearly double the rate of manual application methods. These systems not only streamline installation but also improve adhesive consistency, thermal performance, and wind uplift resistance, making them ideal for large commercial and industrial roofing projects.

For example, technical documentation from a top adhesive manufacturer demonstrates that its fast-curing two-part polyurethane insulation adhesive can securely bond 1,000 square feet of insulation board in under 45 minutes, providing high tensile strength and rapid set times crucial for tight construction schedules. A major warehouse retrofit project using a spray-applied single-ply membrane adhesive reported a 20% reduction in installation time, resulting in significant cost savings and minimized business interruption.

Additionally, spray-applied systems reduce cold-weather installation constraints, offering robust performance at sub-zero temperatures without compromising adhesion quality. The technological advancement directly supports fast-track commercial roofing, high-coverage re-roofing, and energy-efficient retrofits—a key growth avenue for contractors operating in time-sensitive industrial sectors.

Market Opportunity 1: Adhesive Formulations for Over-the-Top Roof Insulation in Building Decarbonization Projects

The global transition toward net-zero buildings and stricter energy performance codes is driving the demand for specialized adhesives that can bond new insulation layers over existing roofing systems, enabling cost-effective retrofits without complete tear-offs. The "over-the-top" insulation approach supports building decarbonization by improving thermal performance and extending roof lifespan.

The European Union’s Energy Performance of Buildings Directive (EPBD) and comparable U.S. state-level building codes are compelling commercial property owners to upgrade existing roofs to achieve minimum thermal resistance (R-value) benchmarks. Adhesives used in these projects must maintain strong adhesion to weathered TPO, EPDM, and bitumen membranes, which are often contaminated by aging or environmental exposure.

Material data from a major polyurethane adhesive supplier reports that achieving sufficient wind uplift resistance on weathered TPO requires enhancing adhesive stability by 20% compared to new substrates, ensuring consistent green strength and long-term durability. Further, according to the U.S. Department of Energy (DOE), roof insulation retrofits can reduce total building energy consumption by 10–15%, offering compelling value for property owners seeking compliance with net-zero and ESG performance metrics.

Manufacturers are therefore focusing on moisture-tolerant, solvent-free polyurethane adhesives that deliver exceptional bond strength, adhesion flexibility, and compatibility across aged substrates—positioning these solutions as critical enablers of roof energy retrofitting and decarbonization goals worldwide.

Market Opportunity 2: Next-Generation Bio-Based and Circular Adhesives to Reduce Embodied Carbon in Roofing Systems

The rise of “Buy Clean” government procurement policies and corporate net-zero construction commitments is catalyzing the development of bio-based and circular adhesives designed to minimize the embodied carbon of the roofing system. The evolution marks a significant step toward carbon-neutral building materials, as manufacturers replace petroleum-derived raw materials with renewable or recycled alternatives.

Major insulation producers are incorporating Environmental Product Declarations (EPDs) for entire roofing systems, which include adhesives as a critical component. Adhesive suppliers are following suit by introducing bio-enhanced polyurethane formulations derived from plant oils, starches, or CO₂ feedstocks, offering comparable performance to conventional systems while reducing lifecycle emissions. Academic research has demonstrated that substituting up to 60% of petroleum-based polyols with renewable feedstocks can lower overall Global Warming Potential (GWP) by up to 40%.

Policy initiatives like the U.S. Federal Buy Clean Initiative are further incentivizing the adoption of low-embodied carbon adhesives in public infrastructure projects, providing a clear economic advantage to manufacturers prioritizing renewable chemistry and circular material design.

For instance, a recent commercial launch of a bio-based roofing adhesive achieved a 71% renewable organic content certified under ISCC PLUS Mass Balance, while delivering the same mechanical strength and moisture resistance as its fossil-based equivalent. As sustainability credentials become integral to construction tenders and certification systems, bio-based roofing adhesives are emerging as a premium solution for environmentally conscious contractors and developers.

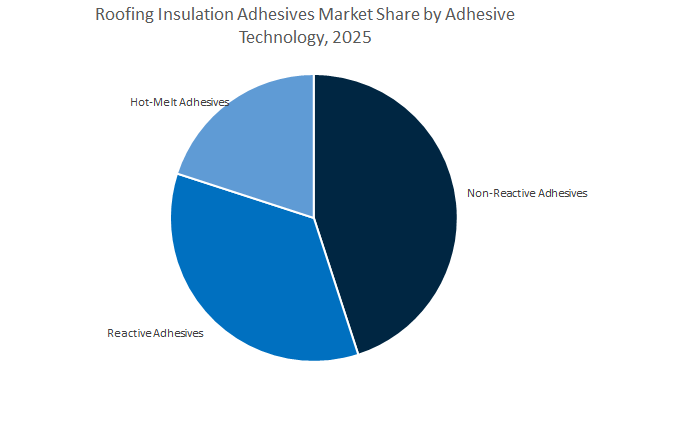

Roofing Insulation Adhesives Market Share Insights, 2025-2034

Market Share by Adhesive Technology

Non-Reactive Adhesives dominate the global roofing insulation adhesives market, capturing an estimated 47.2% share in 2025, largely due to their ease of use, low cost, and proven reliability in standard roofing applications. These adhesives—typically acrylic-based or bituminous formulations—are preferred in both residential and light commercial roofing for attaching insulation boards such as EPS, XPS, and polyiso. The key strength of non-reactive adhesives lies in their simple application process and compatibility with a wide range of substrates, including concrete decks, gypsum, and metal. Their ability to provide consistent adhesion under variable site conditions has established them as the go-to solution for contractors seeking fast installation with minimal specialized equipment. The sustained demand for cost-efficient roofing systems in developing economies continues to anchor this segment’s leadership position.

Meanwhile, Reactive Adhesives, primarily based on polyurethane (PU) and silicone chemistries, represent the high-performance segment of the market. They are increasingly adopted for industrial and commercial roofing systems, where superior adhesion, thermal resistance, and weather durability are critical. These adhesives form strong, long-lasting bonds capable of withstanding extreme temperature fluctuations, UV exposure, and wind uplift forces—making them indispensable in high-performance roofing assemblies, particularly in single-ply membranes and energy-efficient roofs. Hot-Melt Adhesives, especially reactive polyurethane hot melts (PUR HMA), are emerging as the fastest-growing technology in this market. Their instant tack and rapid curing capabilities enable faster installation and early load-bearing strength, ideal for time-sensitive construction projects and large roofing surfaces. The increasing use of automated spray and bead application systems in large-scale projects is further accelerating the adoption of reactive and hot-melt technologies, signaling a clear market shift from traditional adhesive systems toward high-efficiency, performance-driven bonding technologies.

Market Share by Application Method

Spray-Applied Adhesives hold the dominant position, commanding approximately 43.2% of the global roofing insulation adhesives market in 2025, driven by their high application speed, uniform adhesive coverage, and labor-saving benefits. These systems are extensively used in large-scale commercial and industrial roofing installations, particularly when bonding foam insulation boards (polyiso, EPS, or mineral wool) to various substrates. Spray-applied methods enable a continuous, even layer of adhesive, enhancing bond consistency and minimizing material waste. Their compatibility with low-VOC, moisture-cure, and solvent-free formulations aligns with the growing regulatory and sustainability trends shaping the global roofing industry. Contractors favor this method not only for its efficiency but also for reduced downtime and faster project completion, making it a preferred choice in time-critical building applications.

The Cartridge or Caulking Gun Dispensed method remains a strong segment, particularly for mid-sized projects, roof repairs, and detail applications such as flashings, perimeters, and penetrations. Its precision and portability make it ideal for fieldwork and retrofit roofing where accessibility is limited. Trowel or Bead Applied Adhesives continue to serve niche uses in applications requiring patterned coverage or enhanced mechanical interlocking, such as heavily textured substrates or irregular insulation surfaces. Brush/Roller Applied methods are integral for primer coatings and specialized sealing tasks, particularly when combined with liquid-applied roofing systems.

The global roofing insulation adhesives market is dominated by a select group of chemical and construction material leaders — including H.B. Fuller, Sika AG, Huntsman Corporation, GAF (Standard Industries), and Dow Inc. — each driving innovation through sustainability, performance chemistry, and digital transformation. These firms are strategically focused on reducing installation time, enhancing building energy efficiency, and meeting global green construction mandates through advanced adhesive technologies.

H.B. Fuller (NYSE: FUL) continues to lead the market in sustainable adhesive innovation with the Millennium PG-1 EF ECO2™ system, launched in March 2025, representing a breakthrough in canister-based roofing adhesive technology. By using atmospheric gases instead of high-GWP propellants, H.B. Fuller’s adhesives align with global low-VOC standards and EPA guidelines. The company offers a comprehensive range of single- and dual-component polyurethane systems compatible with PIR, EPS, XPS, and mineral wool insulation. With over 20,000 adhesive formulations and 700+ patents, the company continues to deliver contractor-friendly, equipment-free solutions that reduce job-site complexity and environmental impact.

Sika AG (SIX: SIKA) remains a global frontrunner in construction adhesives and roofing technologies, expanding aggressively through acquisitions such as Cromar Building Products (March 2025) and Chema (Peru, 2024). Its integrated product line includes adhesives, sealants, TPO/PVC roofing membranes, and insulation bonding systems under the Sikaflex® and SikaTack® brands. The company’s strategic manufacturing expansions in Indonesia and China enhance regional supply resilience, while its SBTi-validated net-zero roadmap ensures sustainable innovation. Sika’s adhesive portfolio supports energy-efficient building envelopes, offering high bond integrity and environmental compliance for both commercial and industrial roofing insulation systems.

Huntsman Corporation (NYSE: HUN) leverages its leadership in MDI-based polyurethane technologies—the foundation of high-performance insulation materials such as PIR and Polyiso boards—to supply critical adhesive systems for cold chain, roofing, and industrial insulation. The company actively engages in European Union regulatory reform, particularly the 2025 Construction Products Regulation (CPR), aligning its adhesive development with energy efficiency and fire safety standards. Huntsman is investing heavily in low-emission polyurethane catalysts and low-GWP blowing agent-compatible systems, cementing its role as a trusted partner for sustainable insulation bonding in temperature-sensitive construction environments.

GAF, the largest roofing and waterproofing manufacturer in North America, has redefined sustainability in commercial roofing insulation through its EnergyGuard™ NH TCPP-Free Polyiso insulation products (launched February 2025). The standardization of TCPP-free formulations promotes safer and environmentally responsible roofing insulation practices. GAF’s adhesive-compatible insulation systems, including TPO aerosol primers and sprayable bonding adhesives, enable high-speed installation and strong substrate bonding. The company’s digital contractor tools, such as GAF Takeoff™ and GAF Present™, reinforce its leadership in digital construction integration, making GAF a cornerstone in modern roofing efficiency and sustainability.

Dow Inc. (NYSE: DOW) integrates its material science expertise to produce high-performance polyurethane foam adhesives and elastomeric roof bonding systems under its Polyurethanes & Construction Chemicals division. The company’s focus on circular chemistry, bio-based polyols, and energy-efficient formulations supports long-term carbon reduction targets within the EU Green Deal framework. Through its European portfolio optimization (July 2025), Dow is streamlining its polyurethane adhesive offerings for smart building solutions and thermal insulation performance. Its advanced chemistry continues to drive energy-efficient envelope systems, particularly in data centers, logistics facilities, and sustainable infrastructure projects.

Country Analysis: Regional Insights and Innovation Drivers in the Global Roofing Insulation Adhesives Market

United States: Regulatory Push and Technological Shift Toward Low-VOC Roofing Insulation Adhesives

The United States roofing insulation adhesives market is advancing rapidly under the influence of environmental regulation, technological modernization, and infrastructure investment. The Environmental Protection Agency (EPA)’s 2025 amendments to the National VOC Emission Standards for Aerosol Coatings have become a pivotal regulatory force driving innovation toward low-reactivity and zero-VOC polyurethane foam adhesive systems. Roofing manufacturers are now emphasizing sustainable, high-speed spray application systems, particularly in commercial flat roofing, where single-ply membranes and polyisocyanurate (PIR) insulation boards are commonly installed.

The Inflation Reduction Act (IRA) is accelerating the transformation by incentivizing energy-efficient retrofitting of commercial buildings, directly boosting the demand for high-performance polyurethane foam adhesives that provide both thermal insulation and superior wind uplift resistance. Leading manufacturers such as 3M and Carlisle are leveraging their extensive U.S. manufacturing presence to deliver CO₂-propelled, low-GWP (Global Warming Potential) adhesive technologies that eliminate chemical blowing agents during field application. The innovation reduces emissions while ensuring efficient adhesion across multiple substrates like XPS foam, metal decks, and concrete.

Moreover, the U.S. construction market’s climate diversity—from arid regions to sub-zero zones—drives continuous formulation improvement in adhesives to maintain flexibility at low temperatures and thermal durability under high heat.

Germany: Green Building Leadership and Low-Isocyanate PU Adhesive Innovation

Germany stands as a core European hub for sustainable roofing insulation adhesives, leading the global transition toward low-isocyanate and water-based polyurethane formulations. Under the German ABG Regulation, strict limits on VOC emissions in construction products have accelerated the industry’s shift from solvent-based systems to eco-certified, low-emission adhesives. The aligns with Germany’s broader Energy Performance of Buildings Directive (EPBD) targets, which mandate ultra-efficient thermal insulation in all new and retrofitted structures.

Global chemical leaders headquartered in Germany, such as Henkel AG and BASF SE, are intensifying R&D investments in bio-attributed PU adhesives—sourced partly from renewable carbon—to reduce dependency on fossil-based raw materials. The adhesives are increasingly deployed in thermal renovation programs, especially for sealing around roof penetrations and preventing thermal bridges. Additionally, the rising trend in prefabricated and modular construction across Europe has boosted demand for flexible, long open-time polyurethane adhesives optimized for off-site insulation panel bonding and quick on-site curing.

Germany’s leadership in sustainable construction technology, combined with a policy-driven focus on circular building materials, reinforces its position as the innovation capital of Europe’s roofing insulation adhesives industry—balancing performance, durability, and environmental compliance.

China: Domestic Production Expansion and Green Construction Standards

China remains the largest global consumer and producer of roofing insulation adhesives, propelled by rapid urbanization, industrial infrastructure projects, and stringent green building policies. As the government intensifies its focus on energy-efficient and eco-friendly materials, there has been a surge in production capacity expansion among both multinational and domestic firms. The manufacturers are scaling up facilities to produce bitumen-based and polyurethane adhesives tailored for commercial and industrial roofing systems.

The government’s Green Building Action Plan and 14th Five-Year Plan for Construction Material Development emphasize adopting polymer-modified, high-durability adhesives to replace conventional bonding methods. The policy-driven approach is fostering the domestic development of reactive adhesives suitable for bonding diverse insulation substrates—including PIR, EPS, and mineral wool—to concrete and metal decks.

At the same time, Chinese innovation is increasingly focused on cost-effective, performance-driven roofing adhesives, enhancing compatibility with liquid-applied waterproofing systems and single-ply membranes. As domestic R&D expands and quality standards align with international benchmarks, China is emerging as a self-sufficient manufacturing and export hub for roofing insulation adhesive technologies.

United Kingdom: Fire-Safe Adhesives and Climate-Resilient Roofing Systems

The United Kingdom roofing insulation adhesives market is defined by fire safety regulation, sustainability mandates, and adaptation to extreme weather performance. Following the post-Grenfell regulatory reforms, new building safety laws have tightened fire classification standards for construction materials, compelling adhesive manufacturers to develop non-combustible and certified fire-rated polyurethane systems. The adhesives are critical for flat and low-slope roofs using insulation panels that require superior adhesion and heat resistance.

Sustainability trends under the U.K. Net Zero Strategy and ESG compliance requirements are reshaping sourcing and production practices, encouraging the use of traceable, sustainable ingredients in insulation adhesives. Manufacturers are rolling out high-bond, moisture-tolerant two-component polyurethane adhesives, engineered for reliable performance amid the U.K.’s frequent rainfall and high-wind conditions.

The growing popularity of fully adhered roofing systems—in both new builds and retrofits—is boosting adoption of low-VOC hybrid polyurethane adhesives that enhance membrane adhesion without mechanical fastening. As public infrastructure spending increases and green building certifications gain prominence, the U.K. is poised to remain a leading European market for advanced, fire-safe, and weather-resilient roofing adhesives.

France: Indoor Air Quality Regulation and High-Efficiency Building Codes

France’s roofing insulation adhesives industry operates within one of the world’s most stringent regulatory environments for indoor air quality and energy performance. The mandatory French VOC Labeling System, which rates all construction materials on emissions from A+ (best) to C (worst), has been instrumental in shifting demand toward ultra-low-VOC, water-based, and silicone-modified adhesives. The regulation directly impacts product formulation strategies for manufacturers targeting roof insulation and waterproofing applications in residential and commercial buildings.

Energy efficiency legislation under the French Energy Transition Law and the RE2020 Building Code enforces strict insulation standards, promoting the adoption of high-R-value compatible adhesives designed to create airtight and thermally stable roofing assemblies. The adhesives not only enhance insulation performance but also improve the long-term durability of roofing membranes and panels.

The French market is also witnessing growth in silicone and acrylic dispersion adhesives, particularly for eco-labeled flat roof systems. Combined with rising consumer and regulatory preference for non-toxic, low-emission construction materials, France continues to lead Western Europe in environmentally compliant roofing insulation adhesive innovation.

India: Rapid Urbanization, Industrial Expansion, and Localized Production Growth

India’s roofing insulation adhesives market is on an upward trajectory, driven by urban infrastructure expansion, energy efficiency goals, and foreign investment in local manufacturing. The nation’s Smart Cities Mission and National Infrastructure Pipeline (NIP) are catalyzing large-scale construction of commercial, industrial, and residential projects, significantly increasing demand for high-performance insulation bonding adhesives.

Domestic leaders such as Pidilite Industries and multinational construction chemical firms are investing in localized adhesive production facilities, optimizing formulations for India’s hot and humid climate conditions. Polyurethane-based adhesives are increasingly used in fully adhered roofing systems, offering superior moisture resistance and adhesion to various substrates.

The government’s push for energy-efficient, climate-resilient infrastructure and the transition away from traditional mechanical fastening methods are propelling demand for liquid-applied and foam-based insulation adhesives. As sustainable construction becomes mainstream, India is expected to emerge as a key Asia-Pacific hub for cost-effective, durable, and climate-adaptive roofing adhesives, catering to both domestic growth and export markets.

Roofing Insulation Adhesives Market Report Scope

Roofing Insulation Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2034)

|

$3.8 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Adhesive Technology (Reactive, Non-Reactive, Hot-Melt), By Component Type (One-Component, Two-Component, Multi-Component), By Chemistry (Polyurethane, Polyisocyanurate, Silicone, Acrylic, Epoxy, Bituminous/Asphaltic), By Application Method (Spray-Applied, Trowel/Bead, Brush/Roller, Cartridge), By Insulation Substrate Compatibility (Polyisocyanurate, Extruded Polystyrene, Expanded Polystyrene, Mineral Wool/Stone Wool, Wood Fiber/Composite), By Roof Type (Flat, Pitched, Green, Cool), By End-User (Commercial, Industrial, Residential, Institutional

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, The Dow Chemical Company, 3M Company, Arkema SA (Bostik), Carlisle Companies Incorporated, BASF SE, Huntsman Corporation, GAF Materials Corporation, Johns Manville, Holcim Group, DuPont de Nemours, Inc., MAPEI S.p.A., Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Adhesive Technology

- Reactive

- Non-Reactive

- Hot-Melt

By Component Type

- One-Component

- Two-Component

- Multi-Component

By Chemistry

- Polyurethane

- Polyisocyanurate

- Silicone

- Acrylic

- Epoxy

- Bituminous/Asphaltic

By Application Method

- Spray-Applied

- Trowel/Bead

- Brush/Roller

- Cartridge

By Insulation Substrate Compatibility

- Polyisocyanurate

- Extruded Polystyrene

- Expanded Polystyrene

- Mineral Wool/Stone Wool

- Wood Fiber/Composite

By Roof Type

By End-Use Sector

- Commercial

- Industrial

- Residential

- Institutional

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Roofing Insulation Adhesives Market

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- The Dow Chemical Company

- 3M Company

- Arkema SA (Bostik)

- Carlisle Companies Incorporated

- BASF SE

- Huntsman Corporation

- GAF Materials Corporation

- Johns Manville

- Holcim Group

- DuPont de Nemours, Inc.

- MAPEI S.p.A.

- Wacker Chemie AG

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Roofing Insulation Adhesives Market with decision-grade depth—delivering analysis reviews on demand shifts from mechanical fastening to adhesive-based continuous insulation, performance trade-offs across spray-applied and foam systems, and procurement implications of low-GWP, HAPs-free chemistries; it highlights breakthroughs in CO₂-propelled canister systems, cold-weather flexible bonds for PIR/XPS/EPS, and specification gains in wind-uplift and thermal bridging elimination that enhance whole-roof energy performance; benchmarking product pipelines, regulatory convergence, and installer productivity metrics, we map competitive moves and channel strategies through 2034 so engineering leaders, specifiers, and contractors can act with confidence—this report is an essential resource for professionals aligning envelope durability, sustainability compliance, and total installed cost.

Scope Highlights

Segmentation:

- By Adhesive Technology: Reactive; Non-Reactive; Hot-Melt.

- By Component Type: One-Component; Two-Component; Multi-Component.

- By Chemistry: Polyurethane; Polyisocyanurate; Silicone; Acrylic; Epoxy; Bituminous/Asphaltic.

- By Application Method: Spray-Applied; Trowel/Bead; Brush/Roller; Cartridge.

- By Insulation Substrate Compatibility: Polyisocyanurate; Extruded Polystyrene; Expanded Polystyrene; Mineral Wool/Stone Wool; Wood Fiber/Composite.

- By Roof Type: Flat; Pitched; Green; Cool.

- By End-Use Sector: Commercial; Industrial; Residential; Institutional.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies (global and regional leaders across roofing insulation adhesives).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.