Market Overview: Ultra-Thin, High-Temperature and CUI-Resistant Insulation Driving An 8.2% CAGR To 2035

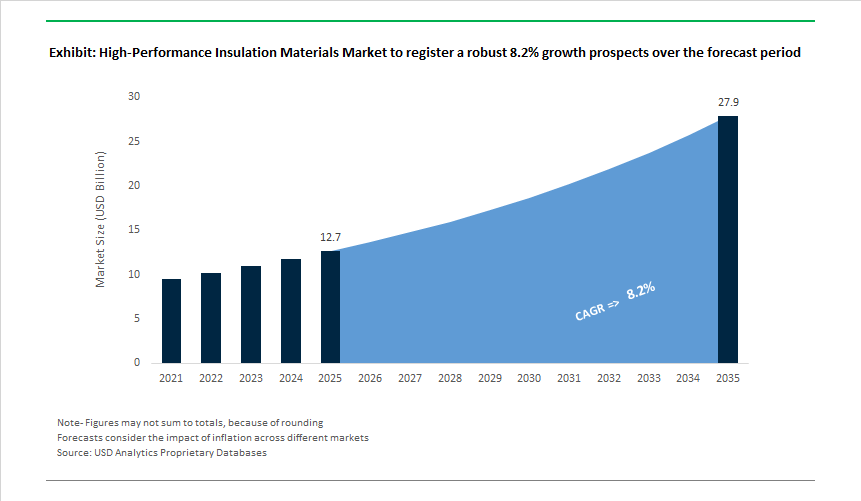

The High-Performance Insulation (HPI) Materials Market (USD 12.7 billion in 2025; projected to reach USD 27.9 billion by 2035 at an 8.2% CAGR) is expanding as asset owners and OEMs confront a converging set of constraints: tighter energy codes, elevated fire-safety standards, space-limited retrofits, and escalating costs associated with corrosion under insulation (CUI) and thermal failure. In contrast to conventional mineral wool and commodity foams, HPI materials are engineered to deliver certifiable thermal efficiency, high continuous-use temperatures, and moisture resistance within minimal thickness, making them increasingly non-substitutable in high-risk and space-constrained environments.

At the system level, adoption is being pulled by applications where insulation performance directly influences asset integrity and safety outcomes. Silica aerogel blankets (λ ≈ 0.018-0.020 W/m·K) and vacuum insulated panels (VIPs) delivering R-50 to R-60 per inch enable dramatic envelope thickness reduction in building retrofits, offshore platforms, and subsea or LNG piping where clearance is limited and heat loss penalties are high. Polyisocyanurate (PIR) rigid foams, with stable performance up to ~120-150°C, continue to see specification in industrial and commercial construction where fire performance and dimensional stability are required at scale. In parallel, advanced elastomeric and mica-based thermal barriers are gaining traction in EV battery packs and power electronics, where controlled heat propagation and thermal-runaway mitigation are now design-level requirements rather than optional safeguards.

Over the forecast period, value capture in the HPI market will be defined less by nominal R-value claims and more by validated performance under real operating conditions. Buyers increasingly require documented CUI resistance (e.g., water absorption below ~0.2%, leachable chlorides below ~30 ppm), certified continuous-temperature ratings, and proven thermal-barrier delay performance of 5-15 minutes in battery and fire-protection applications. Suppliers that can pair these performance credentials with low-embodied-carbon formulations, recyclability pathways, and scalable manufacturing are best positioned to secure premium specification status.

Market Analysis: Policy Pushes, Product Launches and Capacity Moves Accelerating Adoption

The HPI market’s momentum reflects coordinated policy, product innovation and capacity investments across building, industrial and transport sectors. In January 2025, a global chemicals producer published breakthrough data for a phenolic foam panel achieving R-7.5 per inch, positioning phenolic technology as a high-performance, non-combustible rigid insulation alternative for demanding fire-rated applications. March 2025 saw Soudal Group introduce SMX Foam, an isocyanate-free polyurethane formulation that addresses VOC and installer-safety concerns-an important innovation as regulations tighten on construction product emissions.

Sustainability and retrofit drivers surfaced in May 2025, when Knauf North America launched an enhanced glass mineral wool using a bio-based binder (ECOSE™) that reduces embodied carbon by ~15% while meeting WELL standards for indoor air quality. At the policy level, the European Commission (July 2025) finalized stricter EPBD standards pushing public buildings to Near-Zero Energy Building (NZEB) levels by 2027, directly increasing demand for premium thermal insulation solutions. On the industrial and EV fronts, September 2025 awarded Aspen Aerogels a major multi-year supply contract for PyroThin® thermal barriers to a North American EV OEM, while October 2025 Armacell announced targeted PET foam core capacity expansion in Asia to serve wind and automotive composite markets. The year closed with November-December 2025 strategic moves including Kingspan’s acquisition of Tecresa (Nov 2025) to bolster passive fire protection capability and the joint BASF/Welion unveiling in December 2025 of a next-generation solid-state pack using BASF polyurethanes for weight reduction and enhanced thermal protection - signaling cross-sector integration of HPI materials into next-generation energy and mobility platforms.

High-Performance Insulation Materials Market Section 4: Trends and Opportunities

Trend 1: Ultra-High-Temperature (>1200°C) Insulation for Green Hydrogen & Critical Process

Heavy industry is shifting toward "Hard-to-Abate" sector modernization, requiring insulation that can survive the extreme thermal loads of Methane Pyrolysis and Solid Oxide Electrolysis (SOEC), where temperatures often exceed the limits of standard mineral wool. Nuclear-Hydrogen Integration (January 2025): Mitsubishi Heavy Industries (MHI) released technical blueprints for integrating High-Temperature Gas-cooled Reactors (HTGR) with hydrogen production. These systems utilize helium coolants at temperatures exceeding 900∘C, requiring advanced ceramic-matrix composites (CMCs) and internal insulation linings to maintain pressure-vessel integrity and reduce heat loss in the SMR (Steam Methane Reforming) loop. Methane Pyrolysis Benchmarks (2025): Recent studies in Energy & Environmental Science (Volume 18) highlight the rise of "Turquoise Hydrogen" via methane pyrolysis. This process, which operates at 600∘C to 1,200∘C, demands insulation that is chemically inert to solid carbon by-products. New high-alumina insulation and biosoluble ceramic fibers are being qualified to handle these loads, offering a 15–30% improvement in thermal containment over legacy refractory bricks. Industrial Decarbonization CAPEX: The U.S. Department of Energy (DOE) "Pathways to Commercial Liftoff" report (updated Feb 2025) outlines that approximately 57% of industrial heat emissions can be abated through high-efficiency thermal management. This is propelling a shift toward refractory ceramic wool replacements that comply with the latest EU CLP Regulations on low-biopersistence, ensuring worker safety without compromising the 1,400∘C threshold.

Trend 2: Bio-Based and Recyclable Aerogel-Like Materials

To meet 2025 ESG mandates, the insulation market is pivoting toward nanocellulose-based aerogels and bio-inspired composites that offer the same porous architecture as silica aerogels but with a vastly lower carbon footprint. Nanocellulose Breakthrough (September 2025): Research published in the Journal of Bioresources and Bioproducts demonstrated a new class of bio-based nanocellulose aerogels with thermal conductivities as low as 0.032 W/m⋅K. These materials utilize directional freeze-drying to create anisotropic structures that are inherently flame-retardant through carbonization (char-forming), eliminating the need for toxic halogenated additives. Mechanical Resilience Stats: These next-gen bio-aerogels show a 90% recovery rate after repeated compression cycles. This resilience addresses the primary drawback of traditional silica aerogels—fragility—enabling their use in high-vibration environments like automotive battery enclosures and transportation insulation. Circular Economy Initiatives: Under the EU’s Circular Economy Action Plan, insulation producers are now required to provide Environmental Product Declarations (EPDs). This has led to the development of "tendon-like" composite aerogels (reported in Materials, 2025) that incorporate recycled glass fiber into a bio-polymer matrix, increasing abrasion resistance by 12.3 times while lowering thermal conductivity by 25.9%.

Opportunity 1: Deep Energy Retrofit of Building Envelopes

New legislative frameworks in the EU and North America are forcing a "Renovation Wave," creating an urgent need for thin, high-performance materials like Vacuum Insulation Panels (VIPs) that can upgrade historical and space-constrained urban buildings. EU EPBD Compliance (December 2025): Under the Energy Performance of Buildings Directive (EU) 2024/1275, Member States must submit National Building Renovation Plans (NBRP) by December 31, 2025. These plans mandate a reduction in average primary energy use by at least 16% by 2030, specifically targeting the 43% worst-performing buildings. VIP Space Efficiency: For internal retrofits, Vacuum Insulation Panels (VIPs) offer an R-value per inch that is 5x to 10x higher than traditional foam or mineral wool. This allows for "Deep Retrofits" that save up to 20% more floor space in dense urban centers like Paris or London, where real estate value exceeds the premium cost of high-performance insulation. Incentive Prohibitions: From January 1, 2025, EU Member States are prohibited from providing financial incentives for fossil-fuel boilers. This regulatory shift is redirecting billions in subsidies toward "fabric-first" approaches, where high-performance envelopes (U-values below 0.15 W/m2K) are a prerequisite for heat pump installation grants.

Opportunity 2: Cryogenic Insulation for Liquid Hydrogen (LH2) Infrastructure

The transition to Liquid Hydrogen (LH2) for aviation and heavy shipping requires storage at −253∘C (20 K). At this temperature, even minor heat leaks cause massive "boil-off," making Multilayer Insulation (MLI) a critical strategic commodity. Zero Boil-Off (ZBO) Research (2025): NASA’s Glenn Research Center and the International Space Station (ISS) are currently conducting the ZBOT-NC (Zero Boil-Off Tank) experiments to optimize LH2 storage. These studies show that advanced MLI specimens integrated with active cooling shields can reduce heat leakage by two to four orders of magnitude compared to standard spray-on foam (SOFI), reaching rates as low as 0.298 W/m2. Hydrogen Aviation Scaling: In December 2025, technical papers in International Communications in Heat and Mass Transfer detailed "Advanced Hybrid Thermal Management" for LH2 aircraft. These systems use vapor-cooled shields coupled with variable-density MLI to maintain dormancy periods (time before venting) of over 48 hours, a critical metric for commercial airport operations. ASTM Standardization (2025): Based on the testing of over 100 different MLI specimens, two new technical consensus standards were adopted under ASTM International in early 2025. These standards provide the first global benchmarks for cryogenic-vacuum thermal performance, facilitating the cross-border trade of LH2 storage tanks and transport trailers.

Market Share Analysis: High-Performance Insulation Materials Market

Market Share by Product Form: Blankets and Rolls Cement Leadership Through Installability and Lifecycle Economics

Blankets and rolls account for approximately 35% of the High-Performance Insulation Materials Market, a position sustained by their unmatched balance of installation efficiency, thermal versatility, and total installed cost advantages. Unlike rigid boards or sprayed systems that require skilled labor and precise surface preparation, blankets and rolls are inherently adaptable to both standardized building envelopes and complex industrial geometries, enabling faster deployment across residential, commercial, and process-industry sites. Their dominance is reinforced by an exceptionally wide operating temperature envelope, allowing the same product form to serve applications ranging from residential attics to high-temperature industrial equipment without material substitution. From a supply-chain perspective, the segment benefits from extreme compression ratios that dramatically reduce logistics and storage costs, an increasingly critical factor as insulation volumes rise under large-scale retrofit mandates. Performance improvements have also eliminated historical weaknesses: next-generation hydrophobic binders prevent moisture uptake and long-term sagging, preserving thermal resistance over decades of service. Equally important, blankets and rolls now deliver strong acoustic absorption, enabling specifiers to address thermal efficiency, noise control, and fire performance with a single material choice. These combined functional and economic advantages explain why blankets and rolls remain the default, high-volume insulation format across global markets.

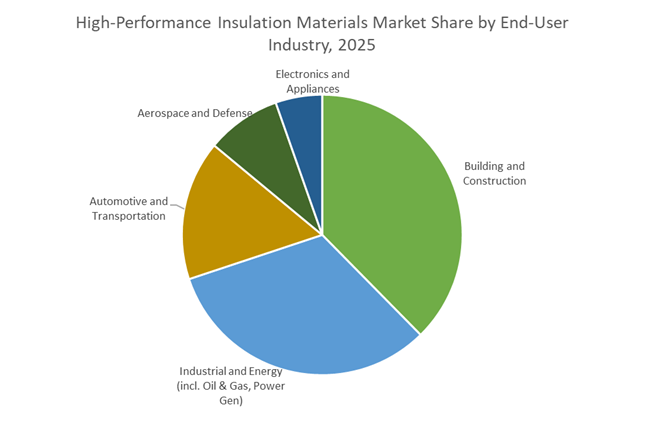

Market Share by Application: Building and Construction Drive Volume Through Regulation and Retrofit Demand

Building and construction represent roughly 35% of total demand, making this segment the primary volume anchor for high-performance insulation materials. This leadership is structurally driven by tightening energy-efficiency regulations, net-zero building targets, and an accelerating wave of deep energy retrofits across mature housing stock in North America and Europe. High-performance insulation has shifted from a discretionary upgrade to a regulatory requirement, as building codes increasingly mandate lower U-values and stricter fire-safety classifications. The segment’s scale is reinforced by clear economic payback, with energy savings translating directly into lower operating costs over the building lifecycle—an argument that resonates strongly with developers, asset owners, and public authorities alike. Sustainability credentials further strengthen demand, as high recycled content enables compliance with LEED, BREEAM, and other green-building frameworks without compromising performance. Fire integrity has become an equally decisive driver, particularly in high-rise and mixed-use developments, where non-combustible insulation is now viewed as a core risk-mitigation component rather than a specification add-on. Together, regulatory pressure, retrofit economics, sustainability targets, and fire safety requirements position building and construction as the most stable and structurally resilient end-use segment in the high-performance insulation market.

Competitive Landscape: Specialized Suppliers Scaling Aerogel, PIR, VIP and Elastomeric Technologies To Meet Safety, Efficiency and Retrofit Demand

The market is led by firms that combine proprietary material science (aerogel chemistries, VIP cores, phenolic and PIR formulations), validated performance (R-value, λ, CUI specs), and broad manufacturing footprints that serve building, industrial, O&G and transport sectors. Leading companies differentiate through DOE-backed scale projects, circularity and high-temperature capability.

Market players concentrate on validated product lines for EV thermal barriers, subsea cryogenic insulation, thin-profile façade retrofits, and low-VOC construction foams, while pursuing acquisitions and capacity expansions to secure supply chains and certifications.

Aspen Aerogels: Market Leader Scaling Aerogel Thermal Barriers For Evs and Industrial Cryogenics

Aspen Aerogels is the aerogel market frontrunner, focused on PyroThin® battery barriers and flexible Pyrogel®/Cryogel® blankets. Backed by a significant US$670 million DOE-linked investment, Aspen targets automotive thermal runaway mitigation and large-scale industrial insulation (including subsea cryogenic projects). Its PyroThin® architecture is specified by OEMs for cell-to-cell barriers that preserve >90% thermal resistance under compression and provide multi-minute propagation delay - an essential safety metric for modern EV modules. Aspen’s product durability (reusable blankets for piping) also reduces lifecycle maintenance costs for power and petrochemical operators.

Kingspan Group: Integrated Building Envelope Insulation and Passive Fire Protection Expansion

Kingspan combines premium Kooltherm® phenolic boards (λ ≈ 0.020 W/(m·K)) with a large global manufacturing footprint to serve thin wall and roof applications. The Tecresa acquisition (Nov 2025) strengthens Kingspan’s passive fire protection and mineral insulation offering, integrating fire-resistant liners and coatings into its high-performance portfolio. Kingspan’s circularity targets (mass upcycling of PET into insulation) and net-zero manufacturing credentials position it strongly for public building retrofits driven by EPBD NZEB mandates.

Armacell International: Elastomeric Insulation Leader For HVAC, Piping and PET Foam Cores For Composites

Armacell is recognized for ArmaFlex® elastomeric insulation with low leachable chloride (<30 ppm) and continuous service temperatures to ~125°C, addressing CUI and HVAC needs. Its expansion of PET foam core capacity in Asia targets lightweight sandwich cores for wind blades and automotive composites, leveraging upcycled PET streams. Armacell’s closed-cell elastomers offer built-in vapor barriers and superior flexibility for maintenance-heavy industrial installations.

Cabot Corporation: Nanogel® Aerogel Particles For Translucent Glazing and Extreme Temperature Processes

Cabot supplies Nanogel® aerogel particles that enable translucent building panels and high-temperature process insulation. Nanogel® delivers very low λ (down to ~0.011 W/(m·K) in particulate form), enabling daylighting panels with U-values near 0.85 W/(m²·K) while preserving light transmission. Cabot’s nanomaterials also address extreme thermal ranges (-50°C to 800°C), serving specialty industrial process and advanced glazing markets across North America, Europe and APAC.

Soudal Group: Polyurethane and Isocyanate-Free Foam Innovations For Sealing and High-Performance Building Insulation

Soudal’s portfolio spans professional PUR foams (Soudafoam™) and the new SMX isocyanate-free foam, targeting installers and building projects seeking low-VOC, safer formulations. Soudal products focus on airtightness, seam sealing and acoustic performance for building envelopes, and innovations in non-isocyanate chemistries help comply with evolving health and environmental regulations while delivering high thermal and acoustic insulation performance.

The United States high-performance insulation materials market is being reshaped by direct federal capital deployment and regulatory pull-through aimed at EV battery safety, residential retrofits, and industrial heat efficiency. In late 2024, the U.S. Department of Energy issued a USD 670.6 million conditional loan to Aspen Aerogels to expand domestic production of PyroThin® aerogel thermal barriers, a decisive move to secure supply for thermal runaway prevention in lithium-ion batteries. This investment positions aerogels as a strategic safety material rather than a premium niche product.

Demand is amplified by policy incentives. Under Inflation Reduction Act (IRA) extensions active through December 31, 2025, homeowners can claim up to USD 1,200 annually (30% of product cost) for high-performance insulation upgrades—accelerating adoption of closed-cell spray foams, high-R-value rigid boards, and hybrid aerogel solutions in the residential retrofit market. On the industrial side, the DOE’s Industrial Technical Validation Program is piloting aerogel-based pipe insulation in heavy manufacturing, targeting a 15% reduction in process heat loss, reinforcing U.S. leadership across EV, buildings, and energy-intensive industries.

China: Made in China 2025 Drives FST Compliance and VIP Self-Sufficiency

China’s high-performance insulation market is transitioning from volume-driven output to precision-engineered, regulation-compliant materials, aligned with the final phase of Made in China 2025. In December 2025, the Ministry of Industry and Information Technology (MIIT) expanded the China RoHS catalogue, imposing stricter hazardous substance limits on appliances such as air conditioners and refrigerators. This regulatory shift is accelerating adoption of FST-compliant insulation, including microporous silica, ceramic fibers, and advanced vacuum insulation panels (VIPs).

Self-sufficiency remains central. By 2025, China reached 70% domestic supply for “core basic materials,” including VIP components and microporous silica, reducing dependence on imported high-R-value products. Infrastructure deployment further anchors demand: in October 2025, large-scale projects in Henan and Guangdong integrated basalt-based mineral wool and aerogel blankets into district cooling and heating systems, leveraging superior moisture resistance and long-term thermal stability in humid climates.

Germany & European Union: EPBD Renovation Wave and Carbon-Accounted Insulation

Europe—led by Germany—remains the largest regional market for high-performance insulation, propelled by binding climate regulation rather than discretionary spending. The Recast Energy Performance of Buildings Directive (EPBD) requires EU member states to submit National Building Renovation Plans (NBRPs) by end-2025, mandating that all new public buildings achieve Zero-Emission Building (ZEB) status by 2028. This has triggered strong demand for VIPs and phenolic foams, which deliver maximum thermal resistance at minimal thickness—critical for urban retrofits.

Corporate innovation aligns with regulation. In August 2025, BASF launched a low-carbon-footprint carbon aerogel for aerospace and hydrogen storage, meeting stringent EU life-cycle carbon reporting rules. Parallel incentives under the EU Green Deal are accelerating bio-based high-performance insulation, with STEICO expanding capacity to serve low-embodied-carbon construction—cementing Europe’s leadership in circular, carbon-accounted insulation systems.

India: Aatmanirbhar Push Turns Insulation into a Manufacturing Scale Play

India is rapidly shifting from insulation imports to domestic, industrial-scale manufacturing, driven by urbanization, building code enforcement, and infrastructure growth. In August 2025, Saint-Gobain began construction of its fifth mineral wool insulation line in Chennai, part of a ₹3,400 crore (USD 400 million) investment—set to become one of the world’s largest integrated sites for high-performance building materials.

Regulatory enforcement is creating immediate demand. The Bureau of Energy Efficiency (BEE) updated Eco Niwas Samhita (ENS) 2025, tightening U-value requirements for roofs and walls, catalyzing adoption of reflective insulation, advanced foams, and mineral wool across residential and commercial real estate. Indirectly, India’s PLI schemes for electronics are boosting demand for thermal interface materials (TIMs) and functional insulation films, supporting cooling needs for the 505 GW power capacity targeted by late 2025.

Japan: Extreme Insulation for 6G, Hydrogen, and Industrial Efficiency

Japan’s 2025 strategy emphasizes “extreme insulation” for high-tech and energy-transition applications. The GX2040 Vision, announced in February 2025, allocates part of a ¥20 trillion (USD 135 billion) investment pool to next-generation technologies, including cryogenic insulation for liquid hydrogen—a cornerstone of Japan’s decarbonized energy roadmap.

Technological progress spans telecom and industry. In early 2025, Japan Display Inc. and Nichias Corporation reported advances in nanoporous insulation films for 6G signal reflectors, combining electromagnetic transparency with thermal insulation for smart city infrastructure. The 7th Strategic Energy Plan (mid-2025) further prioritizes microporous insulation in industry to support a 36–38% renewable energy share by 2030, anchoring long-term demand.

United Arab Emirates: Giga-Projects, District Cooling, and Extreme-Heat Performance

The UAE high-performance insulation market is expanding rapidly, driven by extreme climate conditions and mega-scale urban development. In 2025, the Arab Basalt Fiber Company and regional partners launched a basalt-reinforced insulation ecosystem aligned with the Dubai Urban Plan 2040, targeting up to 30% HVAC energy reduction in large commercial and residential developments.

Industrial demand adds a second growth vector. Major oil & gas capacity expansions in 2025 adopted ceramic fiber and aerogel-based pipe cladding to manage high process temperatures and coastal salinity—conditions that degrade conventional insulation. This positions the UAE as a high-value testbed for technical insulation solutions designed for extreme heat, corrosion, and continuous operation.

2025 National Strategic Matrix: High-Performance Insulation Materials

High-Performance Insulation Materials Matrix

|

Country

|

Primary Development Focus

|

Strategic Policy / Event

|

Core Material Technologies

|

|

United States

|

EV safety & retrofits

|

USD 670.6M DOE loan; IRA credits

|

Aerogels, closed-cell foams

|

|

China

|

Industrial self-sufficiency

|

MIIT RoHS update (Dec 2025)

|

FST-compliant VIPs, silica

|

|

Germany / EU

|

Deep renovation (ZEB)

|

EPBD Recast; Green Deal

|

Bio-based & carbon aerogels

|

|

India

|

Manufacturing scale-up

|

Saint-Gobain ₹3,400 Cr complex

|

Mineral wool, reflective foams

|

|

Japan

|

6G & hydrogen energy

|

GX2040 Vision; Energy Plan

|

Nanoporous, cryogenic insulation

|

|

UAE

|

Extreme-heat HVAC

|

Dubai Urban Plan 2040

|

Basalt, ceramic fiber, aerogels

|

High-Performance Insulation Materials Market Report Scope

High-Performance Insulation Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.7 Billion

|

|

Market Size (2035)

|

$27.9 Billion

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Material Type (Aerogels, Vacuum Insulation Panels, Ceramic Fiber, Glass Fiber, Foams & Others), By Product Form (Blankets & Rolls, Rigid Boards & Panels, Loose-Fill & Particles, Specialty Forms), By Temperature Range (Cryogenic, Low-to-Mid Temperature, High Temperature), By End-User Industry (Oil & Gas, Building & Construction, Automotive, Aerospace & Defense, Industrial & Energy, Electronics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Aspen Aerogels Inc., Cabot Corporation, Saint-Gobain, Kingspan Group, Armacell International S.A., Morgan Advanced Materials, Owens Corning, Rockwool A/S, Knauf Insulation, Unifrax, Guangdong Alison Hi-Tech Co., Ltd., JIOS Aerogel, BASF SE, Svenska Aerogel Holding AB, Panasonic Holdings Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High-Performance Insulation Materials Market Segmentation

By Material Type

- Aerogels

- Vacuum Insulation Panels (VIPs)

- Ceramic Fiber

- Glass Fiber

- Foams and Others

By Product Form

- Blankets and Rolls

- Rigid Boards and Panels

- Loose-fill and Particles

- Specialty Forms

By Temperature Range

- Cryogenic

- Low to Mid Temperature

- High Temperature

By End-User Industry

- Oil and Gas

- Building and Construction

- Automotive

- Aerospace and Defense

- Industrial and Energy

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High-Performance Insulation Materials Market

- Aspen Aerogels, Inc.

- Cabot Corporation

- Saint-Gobain

- Kingspan Group

- Armacell International S.A.

- Morgan Advanced Materials

- Owens Corning

- Rockwool A/S

- Knauf Insulation

- Unifrax

- Guangdong Alison Hi-Tech Co., Ltd.

- JIOS Aerogel

- BASF SE

- Svenska Aerogel Holding AB

- Panasonic Holdings Corporation

*- List not Exhaustive