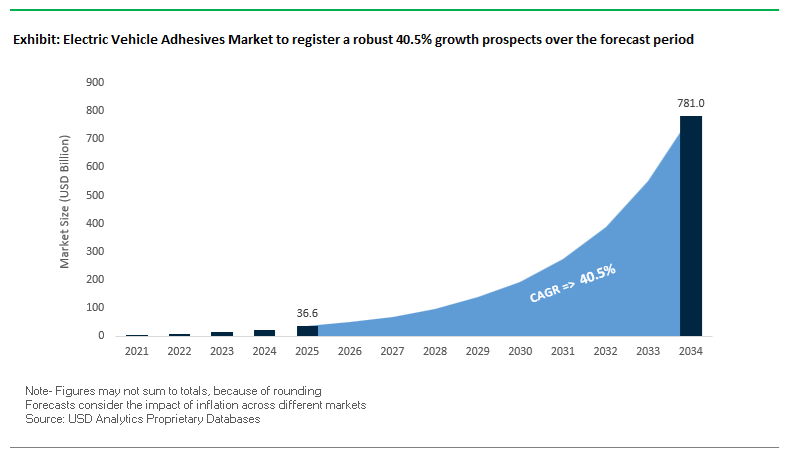

The electric vehicle adhesives market has become a strategic growth arena as OEMs redesign vehicle architectures around electrification, lightweighting, and high-voltage safety. The market is projected to expand from USD 36.6 billion in 2025 to USD 780.9 billion by 2034, reflecting an exceptional CAGR of 40.5% driven by rapid EV penetration and a fundamental rethinking of joining technologies. Adhesives are no longer auxiliary materials; they are central to vehicle performance, influencing mass reduction, battery range, crash behavior, and thermal stability. As EV platforms shift toward mixed-material architectures and large-format battery packs, adhesive solutions are increasingly specified at the platform-design stage rather than selected post-engineering.

This demand inflection is rooted in a clear structural substitution. Structural epoxies and polyurethanes are systematically replacing welds, rivets, and bolts across body-in-white, battery enclosures, and chassis assemblies. These materials enable weight reductions of up to 20% by eliminating fasteners and allowing thinner-gauge substrates, while maintaining tensile shear strengths above 15 MPa when bonding dissimilar materials such as aluminum and high-strength steel. In parallel, thermally conductive adhesives have become critical safety components within battery systems, where formulations are required to deliver thermal conductivity of at least 1.5 W/m·K to dissipate heat efficiently and mitigate thermal runaway risk. Adhesive performance is therefore directly linked to vehicle range, pack durability, and compliance with increasingly stringent safety validation protocols.

Manufacturing and regulatory considerations are further shaping adoption patterns. OEMs are accelerating the use of e-coat-resistant adhesive systems capable of withstanding curing temperatures exceeding 200 °C in body-in-white processes, reducing rework and improving line efficiency. At the same time, REACH-compliant, monomer-free polyurethane chemistries are being adopted to address worker exposure and regulatory risk without compromising mechanical performance. Silicone-based adhesives and foams are gaining share in EV interiors and battery modules for their vibration damping, electrical insulation, and noise-reduction properties, supporting higher NVH standards in electric drivetrains. Looking ahead, competitive advantage in this market will depend on the ability to industrialize high-performance adhesive systems at scale, support OEM qualification across multiple vehicle platforms, and align materials innovation with evolving manufacturing and compliance requirements rather than incremental formulation upgrades.

The EV adhesives industry is in a phase of unprecedented expansion, supported by technological innovation, automotive policy shifts, and regional manufacturing scale-ups.Recent developments reveal a global race to enhance battery safety, assembly efficiency, and sustainability across the electric mobility value chain.

In September 2025, a major Asian automotive OEM invested heavily in automating high-viscosity thermal gap filler systems at its European Gigafactory, marking a leap forward in high-speed EV battery module assembly. Just a month earlier, in August 2025, a U.S. specialty chemicals company introduced a low-density polyurethane adhesive series designed for heavy-duty electric trucks, combining lightweighting benefits with high shear resistance for large-format prismatic lithium-ion cells.

July 2025 saw a major Tier-1 supplier acquire a European UV-curing adhesive manufacturer to strengthen its fast-cure acrylic adhesive portfolio, directly addressing the rising demand for sensor encapsulation and ADAS component bonding in autonomous EVs. In June 2025, a global chemical producer unveiled a halogen-free, flame-retardant epoxy adhesive, fully compliant with UL-94 V0 and GBT standards—specifically tailored for EV battery housing and fire safety applications in China.

Further accelerating sustainability trends, a European adhesives leader in May 2025 opened a U.S.-based R&D center focused on bio-based raw materials to develop carbon-reduced sealants for EV assembly. Meanwhile, in April 2025, new European REACH policies mandated ultra-low monomeric polyurethane systems, reshaping the adhesive supply landscape by prioritizing monomer-free and worker-safe chemistries.

Other significant moves include Dow’s strategic partnership (March 2025) for automated dispensing systems of two-component thermal interface materials (TIMs)—a major step toward precision-controlled EV thermal management. Likewise, in February 2025, a Chinese battery manufacturer unveiled cell-to-pack (CtP) designs that eliminate traditional module casings by using structural foam adhesives, boosting energy density while maintaining rigidity.

From high-durability epoxies in BiW bonding (January 2025) to electrically insulating potting compounds for inverters (December 2024), the EV adhesives landscape reflects a unified trajectory—high-performance, sustainability, automation, and compliance are the new pillars shaping the industry’s global future.

Advanced Material Innovations and Structural Integration Shaping EV Adhesive Demand

Trend 1: Rising Investment in Flame-Retardant & Thermally Conductive Adhesives for Battery Safety

The shift toward higher-energy-density EV batteries is accelerating demand for flame-retardant, thermally conductive adhesives and thermal interface materials (TIMs) that ensure safe, efficient heat transfer across cell and module assemblies. A notable example is Henkel's 2024 graphene-enhanced TIM, which improves heat dissipation by up to 40%, reducing thermal runaway risk in high-power EV modules. Manufacturers are also engineering pressure-sensitive adhesive (PSA) systems that maintain bonding strength under normal conditions but release predictably when thermal or pressure thresholds are exceeded—advancing battery venting safety and minimizing structural damage. Suppliers such as H.B. Fuller are simultaneously scaling UL 94 V-0 compliant adhesive foams (EV Protect™), designed to inhibit flame propagation in densely packed cells, while silicone-based thermally conductive adhesives and potting compounds are being optimized for cylindrical, prismatic, and pouch cell formats to enhance vibration resistance and thermal stability.

Trend 2: Transition to Multi-Material Structural Bonding for Integrated Battery-to-Chassis Designs

The global push toward lightweight structural battery packs is elevating the role of multi-material structural adhesives that bond aluminum, composites, and steel while improving stiffness, crashworthiness, and NVH performance. Emerging BEV architectures increasingly use structural bonding to form a battery-floor "sandwich structure," significantly boosting torsional and bending stiffness for improved driving precision. This shift is reducing reliance on mechanical fasteners, with Methyl Methacrylate (MMA) and Polyurethane adhesives providing uniform stress distribution, lowering fatigue risk, and eliminating fastener-related leak paths. Research also highlights the role of structural adhesives in improving crash energy absorption during side impacts—protecting the underbody battery deck through controlled deformation. Additionally, fast-curing cyanoacrylate-hybrid systems enable sub-minute initial bonding and full strength within five minutes, supporting higher-speed EV production lines.

Emerging Opportunities in Next-Generation EV Adhesive Technologies

Opportunity 1: Adhesives Tailored for Solid-State Battery Commercialization

As solid-state batteries (SSBs) move toward commercialization, chemical suppliers have a significant opportunity to develop adhesives compatible with solid electrolytes and new cell architectures. Toyota and Idemitsu’s 2023 collaboration emphasizes the importance of adhesive technology in sulfide-based solid electrolytes, which are inherently soft and adhesive. Their 2027–2028 commercialization target signals a future where adhesives become an intrinsic part of the cell structure rather than a peripheral assembly material. Strategic investments like Umicore’s stake in Blue Current highlight the industry’s focus on validating material compatibility between active materials, electrolytes, and binding chemistries — opening a pathway for next-generation adhesive formulations designed specifically for solid-state battery interfaces, sealing, and protective encapsulation.

Opportunity 2: Development of Reworkable Adhesives Supporting Battery Repair, Recycling & Second-Life Use

Growing EV adoption is accelerating the need for adhesives that support battery pack repairability, disassembly, and recycling without compromising operational durability. Government regulations such as India’s Battery Waste Management Rules (2022), which enforce Extended Producer Responsibility (EPR), create a strong market pull for de-bondable adhesives that enable non-destructive pack disassembly to meet mandated recovery targets. These rules also incentivize circular-economy models by requiring recycled material content in new battery production, prompting OEMs and recyclers to adopt adhesives that simplify end-of-life separation and material reclamation. As second-life energy storage markets expand, reworkable and selective-release adhesives will become essential for restoring battery modules, lowering lifecycle costs, and improving sustainability profiles across EV fleets.

The global electric vehicle adhesives market is defined by rapid innovation among major players such as Henkel AG, Sika AG, H.B. Fuller, and Bostik (Arkema). These companies dominate with specialized adhesive systems that deliver thermal conductivity, crash resistance, NVH reduction, and fire safety—all central to EV manufacturing.

Henkel leads the global EV adhesives segment with its Loctite® portfolio, offering thermally conductive adhesives and gap fillers optimized for battery safety and thermal management. The company’s injectable adhesive (TLB 9300 APSi) achieves 3 W/mK conductivity, combining structural and heat-dissipating functions for high-speed automation. Henkel’s strategic focus on fire-retardant coatings and potting compounds directly addresses battery safety and propagation prevention. By integrating e-motor magnet bonding and full BiW reinforcement solutions, Henkel positions itself as a complete EV platform supplier across structural, electrical, and thermal domains.

Sika AG continues to dominate EV structural bonding through its SikaPower® and SikaForce® adhesives, which enhance crash performance and enable lightweight, multi-material body designs. Its Purform® technology sets industry standards with ultra-low monomer polyurethane formulations compliant with REACH regulations. Sika’s global expansion focuses on regional manufacturing and NVH reduction, with SikaBaffle® and SikaDamp® product lines improving cabin comfort and structural stiffness. By merging mechanical durability with sustainability, Sika delivers end-to-end bonding and sealing solutions for next-generation EVs.

H.B. Fuller has emerged as a specialized leader in E-Mobility adhesives, offering a suite of solutions under EV Protect, EV Therm, EV Seal, and EV Bond product lines. These systems serve all major battery cell configurations—pouch, prismatic, and cylindrical. The EV Protect series features ultra-lightweight, flame-retardant polyurethane foams for thermal propagation prevention, while EV Bond adhesives ensure high-reliability cold plate and mica bonding. Fuller’s commitment to custom formulations allows optimization for evolving battery architectures, ensuring precise balance between thermal conductivity, adhesion, and flammability resistance.

Bostik, a subsidiary of Arkema, focuses on Body-in-White structural adhesives through its Elastosol® technology, designed for aluminum and steel bonding with corrosion protection. It integrates Arkema’s high-performance thermoplastics (Rilsan® Matrix) with adhesive technology to create impact-resistant, lightweight composites. Bostik’s portfolio includes hem-flange and anti-flutter adhesives for EV closures, essential for fit-and-finish integrity. The company’s materials demonstrate superior wash-out resistance and e-coat compatibility, streamlining EV assembly efficiency while supporting sustainability goals.

Electric Vehicle Adhesives Market Report Scope

Electric Vehicle Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$36.6 Billion

|

|

Market Size (2034)

|

$780.9 Billion

|

|

Market Growth Rate

|

40.5%

|

|

Segments

|

By Application (Battery Pack & Module Bonding, Thermal Interface Materials, Battery Cell Encapsulation, Body-in-White, Motor/Rotor Bonding, Interior/Exterior Sealing), By Resin Type (Epoxy, Polyurethane, Silicone, Acrylic, Others), By Form (Liquid Adhesives, Film & Tape, Hot Melt, Sealants), By Vehicle Type (Battery Electric Vehicles, Plug-in Hybrid Electric Vehicles, Electric Trucks and Buses, Two and Three Wheelers), By Substrate (Composite Materials, Metals, Plastics

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, 3M Company, H.B. Fuller Company, Dow Inc., Arkema Group, PPG Industries, Inc., DuPont de Nemours, Inc, Parker Hannifin Corporation, Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Application

- Battery Pack & Module Bonding

- Thermal Interface Materials

- Battery Cell Encapsulation

- Body-in-White

- Motor/Rotor Bonding

- Interior/Exterior Sealing

By Resin Type

- Epoxy

- Polyurethane

- Silicone

- Acrylic

- Others

By Form/Technology

- Liquid Adhesives

- Film & Tape

- Hot Melt

- Sealants

By Vehicle Type

- Battery Electric Vehicles

- Plug-in Hybrid Electric Vehicles

- Electric Trucks and Buses

- Two and Three Wheelers

By Substrate

- Composite Materials

- Metals

- Plastics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Global Electric Vehicle Adhesives Market

- Henkel AG & Co. KGaA

- Sika AG

- 3M Company

- H.B. Fuller Company

- Dow Inc.

- Arkema Group

- PPG Industries, Inc.

- DuPont de Nemours, Inc

- Parker Hannifin Corporation

- Wacker Chemie AG

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Electric Vehicle (EV) Adhesives Market, delivering analysis reviews on demand inflection points, platform-level material selection, and process integration across cell, module, pack, e-powertrain, and Body-in-White lines. It highlights breakthroughs in thermally conductive gap fillers, e-coat-resistant structural systems, flame-retardant encapsulants, and REACH-aligned low-monomer chemistries that underpin lightweighting, safety, and automated dispensing. Mapping specifications, cost-to-performance curves, and regional supply shifts, this report is an essential resource for materials leaders, procurement heads, process engineers, and strategy teams tasked with scaling EV manufacturing while meeting durability, ESG, and total-cost targets.

Scope Highlights

Segmentation:

- By Application: Battery Pack & Module Bonding; Thermal Interface Materials; Battery Cell Encapsulation; Body-in-White; Motor/Rotor Bonding; Interior/Exterior Sealing.

- By Resin Type: Epoxy; Polyurethane; Silicone; Acrylic; Others.

- By Form/Technology: Liquid Adhesives; Film & Tape; Hot Melt; Sealants.

- By Vehicle Type: Battery Electric Vehicles; Plug-in Hybrid Electric Vehicles; Electric Trucks & Buses; Two & Three Wheelers.

- By Substrate: Composite Materials; Metals; Plastics.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: 15+ company analyses/profiles, including product portfolios, technology roadmaps, manufacturing footprint, and go-to-market strategies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Electrical and Electronics Adhesives Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Electrical and Electronics Adhesives Market Landscape & Outlook (2025–2034)

2.1. Introduction to Electrical and Electronics Adhesives Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Demand Drivers and End-Market Dynamics (EV, 5G, Semiconductor Miniaturization, Consumer Electronics)

2.4. Technology Integration: TIMs, ECAs, UV/Moisture Dual-Cure, Potting & Encapsulants

2.5. Regulatory Environment, Sustainability and Raw-Material & Supply-Chain Dynamics

3. Innovations Reshaping the Electrical and Electronics Adhesives Market

3.1. Trend: Thermally Conductive yet Electrically Insulating Adhesives for High-Power Electronics

3.2. Trend: Fast-Curing UV/LED and Low-Temperature Cure Systems for Automated Assembly

3.3. Opportunity: Adhesives for Heterogeneous Integration and Chiplet Packaging (Die-attach, Underfill, Micro-vias)

3.4. Opportunity: Materials and Encapsulants for Solid-State Batteries and Advanced EV Battery Systems

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation (Fillers, Low-ionic Chemistries, Low-outgassing Systems)

4.3. Sustainability and ESG Strategies (Bio-based, Low-VOC, RoHS/REACH Compliance)

4.4. Market Expansion, Localisation and Regional Manufacturing Focus

5. Market Share and Segmentation Insights: Electrical and Electronics Adhesives Market

5.1. By Resin Type

5.1.1. Epoxy

5.1.2. Silicone

5.1.3. Polyurethane

5.1.4. Acrylic

5.1.5. Cyanoacrylate and Others

5.2. By Product Type

5.2.1. Electrically Conductive Adhesives (ECA, ICA, ACA)

5.2.2. Thermally Conductive Adhesives / TIMs

5.2.3. UV-Curable Adhesives

5.2.4. Potting and Encapsulation Compounds

5.2.5. Structural and Specialty Electronic Adhesives

5.3. By End-Use Industry

5.3.1. Consumer Electronics

5.3.2. Automotive & EVs

5.3.3. Computers & Data Centers

5.3.4. Communications (5G Infrastructure)

5.3.5. Industrial, Medical & Others

5.4. By Application

5.4.1. Surface Mount Devices and PCB Assembly

5.4.2. Die-Attach, Underfill and Flip-Chip Packaging

5.4.3. Display and Optical Bonding (OCA, Display Lamination)

5.4.4. Battery Assembly, Heat Sink Attachment, Potting & Encapsulation

5.5. By Form & Delivery

5.1. Liquid and Paste

5.5.2. Film & Tape

5.5.3. Solid (Preforms) and Automated Dispensing Systems

6. Country Analysis and Outlook of Electrical and Electronics Adhesives Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Electrical and Electronics Adhesives Market Size Outlook by Region (2025–2034)

7.1. North America Electrical & Electronics Adhesives Market Size Outlook to 2034

7.1.1. By Resin Type

7.1.2. By Product Type

7.1.3. By End-Use Industry

7.1.4. By Automation & Equipment Adoption

7.2. Europe Electrical & Electronics Adhesives Market Size Outlook to 2034

7.2.1. By Resin Type

7.2.2. By Application (Automotive, Industrial, Telecom)

7.2.3. By End-Use Industry

7.2.4. By Regulatory & Sustainability Impact

7.3. Asia Pacific Electrical & Electronics Adhesives Market Size Outlook to 2034

7.3.1. By Resin Type

7.3.2. By Product Type (TIMs, ECAs, Encapsulants)

7.3.3. By Country (China, Japan, South Korea, India)

7.3.4. By Manufacturing Localisation Trends

7.4. South America Electrical & Electronics Adhesives Market Size Outlook to 2034

7.4.1. By Product Type

7.4.2. By End-Use Industry

7.4.3. By Local Manufacturing and Import Dynamics

7.4.4. By Application Opportunities

7.5. Middle East and Africa Electrical & Electronics Adhesives Market Size Outlook to 2034

5.1. By Resin Type

7.5.2. By End-Use Industry

7.5.3. By Infrastructure and Energy Projects

7.5.4. By Market Entry Considerations

8. Company Profiles: Leading Players in the Electrical and Electronics Adhesives Market

8.1. Henkel AG & Co. KGaA

8.2. 3M Company

8.3. Dow Inc.

8.4. Sika AG (relevant electronic materials portfolio)

8.5. H.B. Fuller Company

8.6. Arkema Group / DELO Industrial Adhesives

8.7. Momentive Performance Materials

8.8. Heraeus Group

8.9. DELO Industrial Adhesives

8.10. Avery Dennison Corporation

8.11. DuPont

8.12. NANPAO RESINS CHEMICAL GROUP

8.13. Shin-Etsu Chemical Co., Ltd.

8.14. Pidilite Industries Ltd.

8.15. Additional niche and regional technology providers

9. Methodology

9.1. Research Scope

9.2. Market Research Approach and Primary/Secondary Sources

9.3. Market Sizing and Forecasting Model (Bottom-Up / Top-Down Assumptions)

9.4. Research Coverage and Product Taxonomy

9.5. Data Horizon, Key Assumptions and Sensitivity Analysis

9.6. Deliverables and Client-Ready Outputs

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures