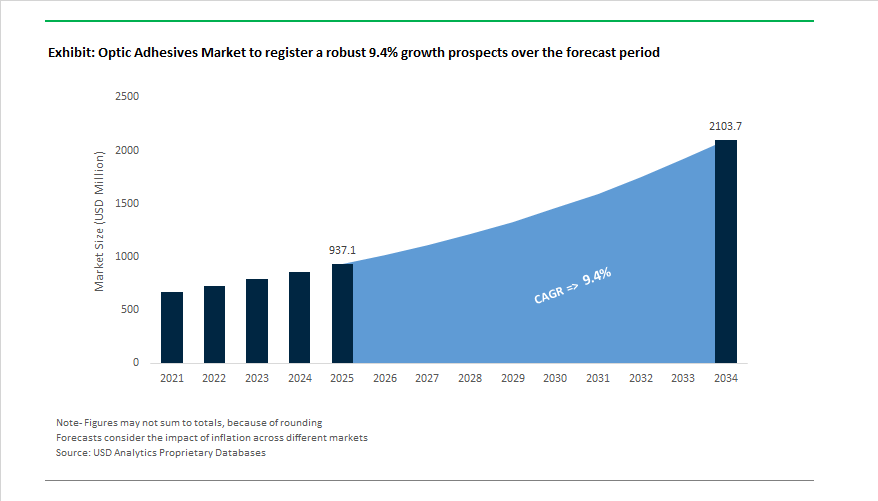

The Global Optic Adhesives Market is projected to expand from USD 937.1 million in 2025 to USD 2.1 billion by 2034, advancing at a CAGR of 9.4%, as optical assemblies become increasingly miniaturized, tolerance-sensitive, and performance-critical across AR/VR, automotive sensing, photonics, and advanced display technologies. Market growth is being driven not simply by rising optical device volumes, but by the tight coupling between adhesive behavior and system-level yield, calibration stability, and long-term optical performance. In modern optical architectures, adhesives are determinants of alignment accuracy, signal fidelity, and lifetime reliability.

Optic adhesives play a central role in maintaining optical axis stability, transmission efficiency, and environmental robustness in applications such as LiDAR modules, camera assemblies, fiber optic connectors, waveguides, and semiconductor photonic devices. As optical systems move toward smaller form factors and higher integration density, even minor adhesive-induced stress or shrinkage can degrade performance. In response, manufacturers such as DELO, Dymax, Henkel (Loctite), and Shin-Etsu are advancing UV-curable and hybrid dual-cure formulations engineered for sub-micron active alignment processes, where positional accuracy must be locked in within seconds. Shrinkage control has become a defining specification, with volumetric shrinkage reduced to as low as 0.2%, directly mitigating optical axis drift during and after cure.

Refractive index engineering is increasingly shaping product differentiation. To support waveguide bonding and AR/VR optical stacks, adhesive suppliers are optimizing high-refractive-index polymers ranging from 1.49 to 1.72, enabling improved light coupling and reduced Fresnel reflection losses at material interfaces. These properties are critical in augmented reality combiners, micro-displays, and photonic integrated circuits, where optical efficiency and color fidelity directly influence device usability. At the same time, UV-LED curing systems achieving fixture strength in under 5 seconds are becoming standard in high-volume manufacturing environments, supporting tight takt times without sacrificing alignment precision.

Environmental and regulatory performance is gaining importance alongside optical metrics. Optical-grade silicones and epoxies qualified to 85/85 durability standards—maintaining bond strength after 1,000 hours at 85°C and 85% relative humidity—are increasingly specified in automotive ADAS, telecom, and outdoor sensing applications. In parallel, there is a clear shift toward low-outgassing, solvent-free, and biocompatible adhesive systems, driven by aerospace, defense, and medical optics requirements under standards such as MIL-A-3920 and ISO 10993. Thermal management is also emerging as a secondary but growing consideration: thermally conductive epoxy adhesives are gaining traction in LiDAR and ADAS sensor assemblies, where heat dissipation supports optical stability and long-term calibration retention.

The optic adhesives industry is experiencing major advancements across R&D, industrial automation, and sustainable materials, driven by the convergence of AR/VR optics, autonomous systems, and high-performance photonic integration.

In Q1 2025, a government-backed EU Photonics Partnership announced a $75 million R&D initiative to develop silicon photonics packaging and optical coupling adhesives for data centers and integrated photonics. The program aims to achieve low-loss optical interconnects and thermally stable adhesives, marking a significant investment in Europe’s optic materials ecosystem. Around the same period, DeepMaterial (Feb 2025) introduced one-component underfill epoxy adhesives for flip-chip photonics packaging, addressing mechanical stress challenges during thermal cycling in compact semiconductor devices.

In January 2025, a major adhesive producer (Henkel) completed a multi-million-dollar expansion to enhance its capacity for biocompatible and low-outgassing optical-grade silicones—a key move to meet demand from medical optics and surgical device manufacturers requiring ISO 10993-compliant bonding solutions.

Research and innovation have also taken center stage. In Q4 2024, a team from NIMS, Japan, published findings on a mussel-protein-inspired optical adhesive, capable of maintaining exceptional bond strength in humid environments—a potential breakthrough for marine and outdoor photonics. Around November 2024, Panacol-Elosol launched a dual-cure optical adhesive (UV/thermal) with a refractive index of 1.58, targeting shadowed-area bonding in miniaturized sensor modules and display systems.

The manufacturing technology landscape has also seen transformative partnerships. In October 2024, a leading dispensing equipment manufacturer collaborated with a major adhesive producer to co-develop an automated micro-dispensing system with ±5μm precision—vital for mass-producing stacked optical components. Meanwhile, automotive sensor manufacturers (Q3 2024) qualified a thermally-conductive epoxy adhesive for ADAS lenses, enhancing thermal stability and operational life.

Simultaneously, DELO Adhesives (Sept 2024) intensified R&D for micro-LED and mini-LED applications, engineering low-yellowing optical adhesives that preserve >99% light transmission post-aging tests. Similarly, Dymax Corporation (Q3 2024) upgraded its product line with a low-modulus, UV-curing acrylate—designed for flexible displays and high-stress lens mountings.

Market Trend 1: Development of Low-Refractive Index and Low-Stress Encapsulants for Advanced Image Sensors

The proliferation of high-resolution imaging systems, from smartphone cameras to automotive LiDAR sensors, is accelerating demand for low-refractive-index (LRI) adhesives engineered to maintain optical clarity and resist mechanical stress. The newest LRI encapsulants—offering refractive indices as low as 1.426 at 589 nm—enable superior optical coupling between glass, polymer, and semiconductor layers in image sensors and waveguides.

Material innovation has focused on maintaining precise refractive index control (±0.005 tolerance) to prevent internal reflection mismatches that lead to pixel crosstalk or optical distortion. Additionally, adhesives with low elastic modulus (around 4.3 MPa) provide mechanical compliance against thermal expansion, preventing birefringence and stress cracking in high-density optical assemblies.

Performance metrics from environmental testing underline the durability of modern optical encapsulants. For example, specialized acrylate-based adhesives designed for fiber optics have successfully passed 2,000 hours at 85°C and 85% Relative Humidity (RH)—a benchmark that ensures sustained optical performance in both industrial and consumer imaging applications. These advancements directly address the growing reliability requirements in smartphone camera modules, CMOS image sensors, and automotive optical sensing technologies, positioning low-refractive-index formulations as a cornerstone of next-generation optical engineering.

Market Trend 2: Adoption of UV-LED Curable Systems with Enhanced Thermal and Environmental Durability

The rapid transition toward UV-LED curing systems (365–405 nm) is reshaping optical adhesive processing in manufacturing environments prioritizing speed, energy efficiency, and environmental safety. The switch to LED curing allows high-precision bonding with fixture times as short as 5 seconds at a 1 W/cm² intensity, drastically reducing production cycles for displays, camera modules, and optical components compared to conventional mercury-based curing systems.

Material durability is also being redefined. High-reliability UV-curable silicone adhesives for optical encapsulation have shown complete adhesion retention (25/25 crosscut test) even after 1,000 hours of exposure at 85°C/85% RH, underscoring their resilience in harsh automotive and outdoor environments. The long-term adhesion stability ensures minimal yellowing or delamination, critical for maintaining luminous efficacy and display clarity.

A major leap in material science comes from hybrid systems using Nanostrength® technology, combining high elongation (up to 170–180%) with low shrinkage rates. These materials effectively absorb stress during curing and thermal cycling, preventing microcracks and optical misalignment. As automotive, consumer electronics, and wearable optics move toward ultra-thin, precision optical assemblies, UV-LED curable adhesives are emerging as the global manufacturing standard for optically clear bonding (OCB) and optical coupling applications.

Market Opportunity 1: Enabling the Mass Production of Augmented Reality (AR) Waveguides and Combiners

The Augmented Reality (AR) and Mixed Reality (MR) segment represents one of the fastest-growing application areas for optic adhesives, particularly in waveguide and combiner lamination. As AR devices trend toward lighter and thinner form factors, ultra-precise optical bonding materials are essential for maintaining visual fidelity and mechanical alignment.

AR waveguide assembly requires adhesives that support highly parallel air gaps between 10 μm and 250 μm, often with embedded spacer elements to ensure uniform layer thickness. These precision gaps preserve the grating structure and eliminate optical distortion, enabling seamless light propagation within the diffractive optical element (DOE). To minimize ghost images and parasitic reflections, adhesive developers are creating blackened polymers with >99% light absorption efficiency at film thicknesses as low as 40 μm.

Further, the customization of refractive index (ranging from 1.49 to 1.72) allows adhesive manufacturers to match diverse optical substrates, such as high-index glass and polymer composites, ensuring optimal light coupling. As global AR device production scales, these specialized optical adhesives are becoming vital in the mass manufacturing of AR combiners and transparent displays, enabling companies to transition from prototype to commercial-grade assembly with precision and repeatability.

Market Opportunity 2: Servicing the Automotive Industry’s Transition to Solid-State Lighting and Full-Field Displays

The transformation of the automotive sector toward electric and autonomous platforms is creating a surge in demand for optical-grade adhesives with exceptional thermal resistance, optical clarity, and environmental durability. These materials are integral to solid-state lighting (SSL), transparent OLED panels, and full-field display systems in next-generation vehicles.

In LED-based lighting systems, adhesive materials must maintain transparency and structural stability at operating temperatures up to 450 K (177°C) to prevent color shift and lumen degradation. High-temperature silicone and epoxy-based encapsulants ensure consistent light transmission and minimize the risk of optical delamination under high heat flux.

Automotive environments also present challenges like humidity, UV exposure, and vibration, requiring high-durability optical coupling adhesives that retain adhesion strength after prolonged exposure to harsh conditions. These performance requirements are especially crucial in LiDAR sensors, camera modules, and adaptive lighting systems, where adhesive integrity directly affects sensor accuracy and visibility performance.

For in-vehicle display integration, UV-curable adhesives with low shrinkage and outgassing characteristics are being adopted for bonding large-format OLED and HUD systems. These formulations deliver high optical transmission and prevent haze or bubble formation during lamination, ensuring pristine visual quality for smart dashboards and transparent display surfaces. The rise of intelligent cockpits and interactive vehicle interfaces places optical adhesives at the core of the evolving automotive design ecosystem, representing one of the most profitable future segments in the industry.

Optic Adhesives Market Share Insights, 2025-2034

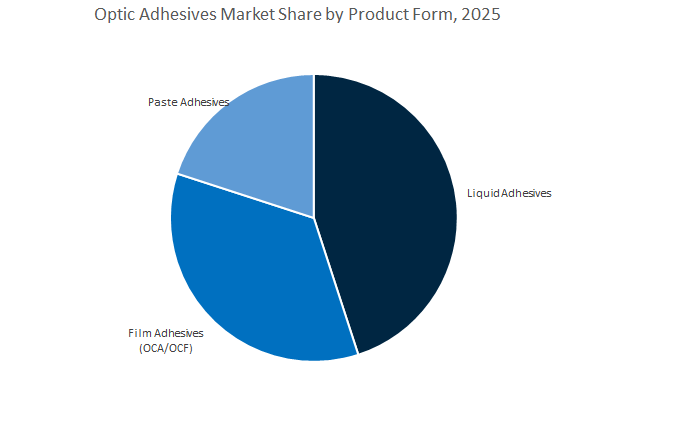

Market Share by Product Form

The liquid adhesives segment holds the dominant position in the global optic adhesives market, projected to capture 46.2% of the market share by 2025. Liquid optic adhesives are widely favored due to their versatility, ease of application, and ability to conform to complex geometries, making them indispensable in optical bonding, lens cementing, and electronic display manufacturing. Their high optical clarity, strong adhesion to glass and plastic substrates, and ability to minimize light scattering and reflection losses have cemented their importance in consumer electronics, automotive displays, and precision optical devices. The ongoing expansion of OLED, AR/VR, and head-up display (HUD) technologies is driving manufacturers to invest in advanced UV-curable and two-part liquid formulations that provide low shrinkage, high transparency, and long-term environmental stability.

Film adhesives (OCA/OCF) are gaining traction as a high-growth category, particularly in display lamination and touchscreen applications, where uniform thickness, optical clarity, and bubble-free bonding are crucial. Their superior dimensional stability and reworkability make them preferred materials for automotive infotainment systems, smartphones, and tablets. The increasing adoption of flexible and foldable displays is further fueling demand for ultra-thin, high-adhesion optical films. Meanwhile, paste adhesives maintain relevance for niche applications that require gap filling, thermal management, and vibration resistance, especially in lens assembly, fiber optic splicing, and laser component manufacturing. These materials are particularly valuable for applications demanding mechanical reinforcement alongside optical precision.

Market Share by Application

The display lamination segment leads the global optic adhesives market, holding a projected 32.3% share in 2025, driven by the booming demand for smartphones, tablets, televisions, and automotive displays. Optical adhesives play a critical role in laminating cover glass, touch sensors, and display panels, ensuring improved light transmission, contrast ratio, and mechanical durability. The trend toward AR/VR headsets, curved screens, and transparent displays is further increasing the need for UV-curable and optically clear adhesives (OCAs) that deliver high bonding precision with minimal optical distortion. Additionally, growing investments in automotive infotainment and digital cockpit systems are accelerating adoption of optical adhesives that can endure vibration, heat, and humidity without performance degradation.

The optical bonding and assembly segment maintains a strong position in industrial optics, medical imaging devices, and sensors, where adhesives provide permanent alignment, environmental protection, and high refractive index matching. Lens bonding and cementing applications continue to be vital in camera modules, microscopes, and projectors, requiring adhesives that combine optical transparency with low yellowing and high resistance to thermal expansion. Fiber optic splicing and encapsulation applications are expanding rapidly, particularly in telecommunications, 5G networks, and data centers, where nano-engineered optic adhesives ensure signal integrity and micro-scale precision.

The optic adhesives market is characterized by a mix of global giants and niche innovators specializing in UV-curable, thermally conductive, and optically clear adhesive formulations. Companies such as Henkel, Dymax, DELO, Heraeus, 3M, and Master Bond dominate through continuous R&D, product diversification, and automation partnerships, enabling them to cater to semiconductors, displays, AR/VR, and photonics packaging markets worldwide.

Henkel leads through its Loctite and ABLESTIK brands, focusing on active alignment adhesives for automotive cameras and mobile optics. Its materials achieve sub-micron bonding accuracy and superior moisture resistance for harsh automotive and telecom environments. Henkel’s recent expansion supports biocompatible silicone adhesives for medical devices, while its low-outgassing epoxy portfolio meets NASA space-grade standards. The firm continues to invest in dual-cure systems and high-viscosity pastes optimized for large-area display bonding in next-gen flexible electronics.

Dymax is recognized for its expertise in UV-light-curable adhesives that achieve fixture strength in under one second, revolutionizing high-speed consumer electronics assembly. The company’s low-modulus acrylate formulations mitigate CTE mismatch stress in glass-to-plastic and metal bonding. Its proprietary See-Cure technology, where adhesives visibly change color upon curing, ensures reliability in automated lines. Dymax also leads in medical-grade optical adhesives that are USP Class VI and ISO 10993-certified, expanding rapidly in endoscopes and disposable optical sensors.

DELO Adhesives specializes in micro-optics and MEMS sensor bonding, offering precision materials with refractive indices up to 1.72, ideal for waveguide stacking in AR/VR displays. Its innovations include edge-blackening polymers that cure simultaneously with optical adhesives to suppress stray light and enhance contrast. DELO also offers defined air gap bonding technologies (10–250μm) for advanced display assemblies. The firm’s R&D focus on AR/VR and miniaturized optical components makes it a cornerstone of next-generation mixed-reality optics manufacturing.

Heraeus, through its Epurio division, develops ultra-pure photoresins and silicones for OLED, mini-LED, and wafer-level optics (WLO) applications. Its silicone encapsulants deliver superior photothermal stability for high-power LEDs and automotive headlamps. The company’s continued expansion in photoresin capacity supports the semiconductor industry’s shift toward co-packaged optics (CPO). Heraeus’ expertise in optical lithography materials positions it as a key enabler of miniaturized, high-transmission optical systems for next-gen electronics.

3M holds a dominant position with its Optically Clear Adhesives (OCA) films used in display panels, touchscreens, and flexible electronics. These adhesives provide exceptional clarity, reworkability, and ultra-thin profiles (<50μm), supporting innovations in foldable and rollable displays. 3M’s thermally conductive OCA series extends its reach into defense and aerospace, where optical transparency must coexist with heat management and mechanical ruggedness. The company’s tape-based adhesive systems enable clean, repeatable assembly for mass-produced consumer and industrial optics.

Master Bond excels in epoxy and silicone-based optical adhesives that comply with MIL-A-3920 standards, serving aerospace, defense, and high-reliability optical systems. Its dual-cure epoxies (UV/heat) offer low shrinkage (≈1–2%) and chemical resistance for deep-set lenses and fiber optic assemblies. Master Bond’s ultra-low viscosity formulations (100–300 cps) enable deep capillary wicking into fine fiber bundles, ensuring excellent light transmission. Additionally, its adhesives withstand aggressive sterilization (EtO and autoclave), making them indispensable for medical imaging instruments.

Country Analysis: Global Optic Adhesives Industry — Regional Innovation and Technology Hubs

United States: Pioneering UV-Curing and Advanced Optical Adhesive Technologies

The United States leads in UV-curing adhesive innovation and high-performance optical bonding solutions for advanced photonic and electronic applications. Recent advancements from major U.S.-based chemical and adhesive manufacturers include dual-cure UV adhesives engineered for complex bonding geometries found in LiDAR systems and Advanced Driver Assistance Systems (ADAS). The adhesives ensure complete polymerization in shadowed regions, a critical requirement for autonomous vehicle sensor assemblies.

R&D investment across U.S. optics and electronics sectors is expanding significantly. Leading material science firms are channeling funds into the development of ultra-low stress, temperature-stable epoxy adhesives designed for fiber optic transceivers and photonic modules, ensuring precise component alignment and low signal loss in 5G and data center infrastructure. In the aerospace and defense sectors, government-backed projects such as those funded by DARPA and the Department of Defense (DoD) are focusing on radiation-resistant optical epoxies tailored for avionics displays, targeting systems, and rugged sensors.

Furthermore, the miniaturization trend in electronics is fueling innovation in optically clear silicone adhesives for compact camera modules (CCMs) and micro-LED displays. The formulations feature exceptional resistance to outgassing and fogging, maintaining long-term optical clarity. With a growing emphasis on biocompatible Nano-Optic Adhesives for medical sensors and wearables, the U.S. is consolidating its dominance in precision optical material science, underpinned by strong regulatory support and private-sector innovation.

Germany: Engineering Precision and Photonics Integration in Optic Adhesives

Germany remains the European powerhouse for precision-engineered optical adhesives, driven by its strengths in automotive photonics, industrial sensors, and manufacturing automation. German adhesive specialists are investing heavily in high-speed UV-curing adhesives optimized for automated dispensing systems, enabling efficient, repeatable bonding for micro-optics and sensor assemblies.

In the automotive sector, Germany is at the forefront of large-format, curved display bonding technologies, where Optically Clear Adhesives (OCAs) with high thermal stability and moisture resistance are essential for next-generation infotainment systems. The adhesives must meet stringent VDA and OEM durability standards, ensuring clarity and structural integrity in extreme environmental conditions.

Collaborations between major adhesive producers and research institutes such as Fraunhofer Institutes are advancing hermetic sealing systems for industrial and AR/VR sensors, combining optical clarity with high chemical resistance. At the same time, German manufacturers are aligning with the EU Green Deal by developing solvent-free, bio-based optical adhesives that minimize VOC emissions. The sustainability-driven innovations position Germany as a leader in green photonics adhesives, combining environmental responsibility with engineering precision.

Japan: Advancing High-Index OCAs and Semiconductor Photonics Adhesives

Japan stands as a global hub for high-index optical materials and display adhesive technology, supporting industries ranging from semiconductors to OLED displays. Japanese chemical corporations are spearheading the development of next-generation Optically Clear Adhesives (OCAs) tailored for 8K, mini-LED, and flexible OLED panels, delivering superior optical transparency, refractive index matching, and adhesion performance under thermal cycling.

In semiconductor photonics, Japan’s material scientists are advancing thermally conductive, optically clear epoxies for LED and laser diode bonding, ensuring efficient heat dissipation without compromising optical precision. The materials are increasingly critical in high-density photonics packaging, including optical sensors and microprojectors used in AR/VR systems. Additionally, the country’s long-term investment in UV-curable optical fiber adhesives supports the expansion of 5G telecommunications networks, while new developments in bio-compatible nano-adhesives are revolutionizing medical optics and wearable sensors.

Automation and robotics integration are also central to Japan’s adhesive industry. Precision micro-dispensing and UV-curing systems have been optimized for the mass production of optical components, ensuring consistent bonding performance at micro-scale tolerances. The combination of high-purity materials and automated precision cements Japan’s role as a global leader in display and semiconductor photonics adhesives.

China: Rapid Scale-Up in Display, Fiber Optics, and EV Sensor Adhesives

China has become a dominant production base and innovation hub for optical adhesives, driven by massive investments in OLED fabrication, fiber optics, and electric vehicle (EV) sensors. The nation’s state-backed industrial policies are propelling a surge in Optically Clear Adhesive (OCA) production for domestic OLED display lines, as the country aims to achieve near-complete supply chain localization for display technologies.

In telecommunications, the national rollout of fiber-to-the-home (FTTH) networks and 5G backbone infrastructure is generating immense demand for low-cost, high-performance fiber splicing adhesives. The is complemented by the government’s support for eco-friendly production, leading to a rapid transition toward low-VOC, solvent-free adhesive formulations.

The EV manufacturing boom further strengthens China’s position in the global optic adhesives market. Thermally stable, optically clear adhesives are increasingly specified for LiDAR systems, in-vehicle cameras, and advanced driver-assistance sensors (ADAS)—applications that demand high durability and optical accuracy. Chinese chemical firms are investing heavily in independent R&D for silicone-based encapsulants used in LED backlighting and optical displays, signaling the country’s ambition to reduce dependency on imported raw materials and technologies while becoming a self-sufficient optics materials powerhouse.

South Korea: Global Leadership in Foldable Display and OLED Optical Bonding

South Korea is at the forefront of innovation in flexible and foldable display adhesives, serving as a critical market for advanced Optically Clear Adhesives (OCAs) that combine flexibility, transparency, and durability. Major South Korean display manufacturers are pushing material suppliers to develop next-generation foldable adhesives capable of withstanding over 200,000 bending cycles without clouding or delamination. The adhesives are essential for the continued evolution of foldable smartphones, tablets, and rollable displays.

At the same time, the country’s OLED ecosystem—driven by both mobile and TV panel production—is investing heavily in moisture-resistant bonding solutions for WOLED and QD-OLED modules, ensuring long-term optical clarity and adhesion strength under varied environmental conditions.

Strategic R&D collaborations between domestic adhesive manufacturers and display panel giants are targeting optical bonding materials for IT OLED applications, including monitors and laptops, which are projected to see exponential demand growth. South Korea’s focus on electronics miniaturization, OLED integration, and high-speed material innovation cements its position as a global leader in next-generation display adhesives and hybrid optical bonding technologies.

Optic Adhesives Market Report Scope

Optic Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$937.1 Million

|

|

Market Size (2034)

|

$2,103.5 Million

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Resin Type (Epoxy, Acrylic, Silicone, Cyanoacrylate, Polyurethane, Polyimide), By Curing Mechanism (UV-Curable, Thermal-Curable, Two-Part, Moisture-Curable, Dual-Curing), By Product Form (Liquid, Film, Paste), By Application (Optical Bonding & Assembly, Lens Bonding/Cementing, Fiber Optics Splicing/Termination, Waveguide Sealing, Display Lamination, Encapsulation), By End-Use Industry (Electrical & Electronics, Automotive, Telecommunications, Medical Devices, Aerospace & Defense, Consumer Optics

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Dow Inc., 3M Company, H.B. Fuller Company, Dymax Corporation, DELO Industrie Klebstoffe GmbH & Co. KGaA, Shin-Etsu Chemical Co., Ltd., DIC Corporation, Nippon Kayaku Co., Ltd., Norland Products Inc., Master Bond Inc., Panacol-Elosol GmbH, Epotek, Inc., Permabond Engineering Adhesives Ltd., Lord Corporation (Parker Hannifin)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Epoxy

- Acrylic

- Silicone

- Cyanoacrylate

- Polyurethane

- Polyimide

By Curing Mechanism

- UV-Curable

- Thermal-Curable

- Two-Part

- Moisture-Curable

- Dual-Curing

By Product Form

By Application

- Optical Bonding & Assembly

- Lens Bonding/Cementing

- Fiber Optics Splicing/Termination

- Waveguide Sealing

- Display Lamination

- Encapsulation

By End-Use Industry

- Electrical & Electronics

- Automotive

- Telecommunications

- Medical Devices

- Aerospace & Defense

- Consumer Optics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Optic Adhesives Market

- Henkel AG & Co. KGaA

- Dow Inc.

- 3M Company

- H.B. Fuller Company

- Dymax Corporation

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Shin-Etsu Chemical Co., Ltd.

- DIC Corporation

- Nippon Kayaku Co., Ltd.

- Norland Products Inc.

- Master Bond Inc.

- Panacol-Elosol GmbH

- Epotek, Inc.

- Permabond Engineering Adhesives Ltd.

- Lord Corporation (Parker Hannifin)

*- List not Exhaustive

Research Coverage

This report investigates the Optic Adhesives Market, delivering analysis reviews on demand catalysts from AR/VR waveguides and automotive sensors to photonics packaging and advanced displays, curates breakthroughs in ultra-clear, low-shrinkage UV/dual-cure chemistries, thermally stable epoxies for LiDAR/ADAS, and high-index optical polymers for precise coupling, and highlights processing windows for sub-micron alignment, low-outgassing/biocompatibility compliance, and long-term 85/85 durability that underpin scalable mass production; developed by USDAnalytics, this report is an essential resource for product managers, optical/mechanical engineers, sourcing leaders, and investors who need defensible forecasts, competitive benchmarking, and route-to-market clarity across consumer, medical, telecom, and automotive optics.

Scope Highlights

Segmentation:

- By Resin Type: Epoxy; Acrylic; Silicone; Cyanoacrylate; Polyurethane; Polyimide.

- By Curing Mechanism: UV-Curable; Thermal-Curable; Two-Part; Moisture-Curable; Dual-Curing.

- By Product Form: Liquid; Film; Paste.

- By Application: Optical Bonding & Assembly; Lens Bonding/Cementing; Fiber Optics Splicing/Termination; Waveguide Sealing; Display Lamination; Encapsulation.

- By End-Use Industry: Electrical & Electronics; Automotive; Telecommunications; Medical Devices; Aerospace & Defense; Consumer Optics.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies covering strategies, portfolios, and recent product/capacity moves.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.