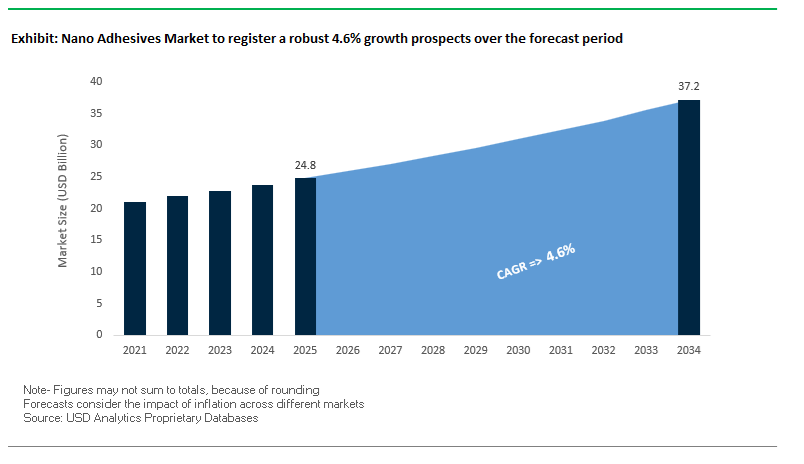

The Global Nano Adhesives Market is projected to grow from USD 24.8 billion in 2025 to USD 37.2 billion by 2034, expanding at a CAGR of 4.6% during the forecast period. This steady growth is being driven by the rising adoption of nano-engineered bonding solutions in electronics, electric vehicles (EVs), aerospace, and renewable energy sectors. Nano adhesives, which integrate nanoparticles such as silica, graphene, carbon nanotubes (CNTs), and silver, deliver superior thermal conductivity, high-temperature stability, and enhanced mechanical strength compared to conventional bonding agents.

In the semiconductor and microelectronics industry, nano adhesives are enabling ultra-thin bond lines (as low as 28 nm), ensuring precise bonding for chip packaging, flexible displays, and microelectronic devices. Meanwhile, the automotive and aerospace industries are turning to nano epoxy and acrylic formulations for structural lightweighting, high shear strength, and long-term durability under extreme heat and stress. As the shift toward electrification accelerates, thermally conductive nano adhesives are becoming indispensable in EV battery assemblies, heat sinks, and power modules, where efficient heat dissipation is critical.

From a regulatory perspective, the industry’s shift toward low-VOC, sustainable nano adhesive formulations is being reinforced by global environmental mandates such as the European Green Deal and REACH compliance standards. Continuous R&D investment by top manufacturers in nano-hybrid epoxy systems, silver-filled adhesives, and flexible conductive inks is expected to drive significant performance breakthroughs over the next decade.

Key Product Insights

- Ultra-Thin Bonding: Nano adhesives achieve bond-line thicknesses down to 28–85 nm, far surpassing traditional die attach adhesives and improving both thermal and electrical conductivity in semiconductor packaging.

- Extreme Heat Resistance: Advanced nano-epoxy systems can withstand up to 540°F (280°C), critical for solder reflow, under-hood automotive, and aerospace applications.

- Mechanical Stability: Finite element studies show that 100 nm GaN resin joints achieve stress resistance around 3.66 MPa, offering improved reliability for microelectronic and photonic devices.

- Lightweighting Integration: The automotive sector’s lightweighting initiatives are fueling demand for nano-epoxy structural adhesives, which enhance composite bonding in CFRP (carbon fiber-reinforced polymer) assemblies.

- Superior Conductivity: Silver nanoparticle-filled adhesives demonstrate volume resistivity below 0.006 ohm-cm, outperforming conventional epoxies in thermal and electrical conductivity for EV and semiconductor applications.

The nano adhesives industry is witnessing rapid technological advancements and strategic collaborations across the adhesives, materials science, and energy sectors. From semiconductor packaging to electric vehicle battery assembly, nanomaterial integration is redefining adhesive properties, enabling higher temperature resistance, superior conductivity, and environmentally compliant formulations.

In July 2025, Sonoco Products Company announced a USD 30 million capital investment aimed at expanding its adhesives and sealants production capacity across three global facilities. This initiative is expected to add 100 million units in annual output, underscoring rising market demand for advanced bonding materials integrated with nano-reinforced resins for packaging and industrial manufacturing. Just a month earlier, in June 2025, TrinANO Technologies launched a breakthrough nanocoating solution for solar modules, which integrates light-trapping, anti-reflection, and self-cleaning nanolayers—boosting solar energy output by up to 4%. This marks a key milestone in applying nanotechnology-based adhesives and coatings to renewable energy efficiency enhancement.

3M Company, a leading player in adhesive innovations, introduced its Ultra High Temperature Adhesive Transfer Tape in May 2025, rated for short-term thermal resistance up to 540°F (280°C). Specifically designed for flexible electronics and under-hood automotive components, this adhesive system offers improved dimensional stability and high thermal endurance. Meanwhile, in April 2025, a published study on hybrid nanoparticle (GNP/Ag) conductive inks demonstrated how optimized curing conditions significantly enhanced both adhesion and conductivity, establishing new performance benchmarks for wearable electronics and semiconductor interconnects.

Earlier in March 2025, Elkem ASA emphasized its specialty silicones division, highlighting the integration of nanomaterials into high-reliability adhesives for EV battery thermal management and power electronics sealing. In February 2025, Henkel (Loctite) strengthened its product line with the LOCTITE EA 9340—a high-temperature, two-part nano-epoxy engineered for metal, ceramic, and composite bonding, offering exceptional resistance to chemicals and extreme conditions.

By December 2024, Sika and Dow Inc. had jointly advanced their portfolios of thermally conductive nano adhesives for EV battery module sealing, while Acculon Energy’s September 2024 partnership with Forge Nano focused on next-generation aerospace and defense batteries. The collaboration’s goal—to enhance energy density, heat dissipation, and adhesion at nano-scale precision—illustrates how nanotechnology and adhesive chemistry are converging in high-reliability engineering.

Advances in Nanomaterial Engineering, Miniaturization & Smart Functional Adhesion

Trend 1: Nanoparticle-Reinforced Structural Adhesives Enabling Lightweighting in Aerospace and Automotive

Aerospace and electric vehicle manufacturers are accelerating the use of nanoparticle-reinforced adhesives to achieve stronger, lighter, and more damage-tolerant structures. Incorporating nanoscale fillers such as alumina, nanosilica, and carbon nanotubes significantly enhances shear strength, impact resistance, and fracture toughness—properties essential for high-load, crash-resistant joints. Studies show that epoxy adhesives reinforced with Al₂O₃ nanoparticles can increase absorbed impact energy by 23.4% and improve shear strength by 22.5%, enabling the reliable bonding of composite scarf joints used in aircraft and high-performance automotive structures. CNT-modified epoxies used in automotive bonding demonstrate superior environmental durability, with 1 wt% CNT preventing premature adhesive failure even after prolonged exposure to 60°C water immersion, where unmodified bonds fail within hours. Further research shows nanoparticle-reinforced epoxies used for titanium bonding can retain 95%+ joint strength after exposure to extreme aerospace climatic cycles and maintain thermal stability up to 350°C, underscoring their critical role in next-generation electrified propulsion systems and high-temperature aviation assemblies.

Trend 2: Commercialization of Nano-Engineered PSAs for Miniaturized Electronics and Long-Wear Medical Devices

The miniaturization of electronics and the rise of long-duration medical wearables are propelling demand for nano-engineered pressure-sensitive adhesives (PSAs) with superior adhesion, flexibility, and biocompatibility. In wearables, silicone-based nano-PSAs are becoming the material of choice due to their exceptional skin compatibility and tack retention over multi-day wear cycles. Companies such as 3M are commercializing nano-enhanced Hi-Tack Silicone Adhesives designed for continuous glucose monitors and long-wear health patches, providing stronger adhesion without compromising breathability or patient comfort. In consumer electronics, nano-structured PSAs engineered with refined acrylic or silicone polymer chains support bonding at ultra-fine pitches and deliver high dielectric strength, making them indispensable for flexible circuits in smartphones and smartwatches. Simultaneously, sustainability initiatives are fueling the adoption of water-based nano-PSAs, which deliver high performance with lower VOCs, enabling their use in premium packaging tapes, electronic components, and next-generation assembly lines.

Opportunities in Smart, Reversible & Printed Electronics Adhesive Technologies

Opportunity 1: Stimuli-Responsive Smart Nano-Adhesives Enabling On-Demand Bonding and Circular Manufacturing

A major opportunity is emerging in smart nano-adhesives engineered to bond strongly during use but debond cleanly when triggered by heat, UV light, or chemical agents—supporting repairability, modular design, and circular economy requirements. Research into UV-responsive polyurethane adhesives shows extraordinary potential, with bond strength reductions of up to 86% after just 5 minutes of exposure at 365 nm, enabling clean removal from glass and electronic substrates without damage. Parallel studies on chemically responsive nano-adhesives incorporating degradable groups demonstrate controlled debonding via fluoride-ion activation, producing a 23% bonding-strength reduction sufficient for disassembly and material recovery. These reversible bonding platforms present enormous value for consumer electronics, EV battery recycling, modular robotics, and end-of-life management of composite structures.

Opportunity 2: Nano-Adhesives for Printed & Structural Electronics in Additive Manufacturing

The convergence of additive manufacturing, flexible electronics, and nanotechnology is creating a fast-growing opportunity for nano-adhesives designed for direct deposition, interconnect formation, and 3D circuit fabrication. Electrically conductive nano-adhesives (ECAs), formulated with silver nanoparticles, graphene, or CNTs, are increasingly viewed as the leading alternative to toxic lead-based solder, enabling ultra-fine interconnect pitches down to 50 μm for high-density microelectronics. Carbon nanotube-reinforced adhesives significantly reduce the percolation threshold needed to establish conductivity due to CNTs’ extremely high aspect ratio, allowing manufacturers to achieve required electrical performance with less filler material—improving cost efficiency and mechanical flexibility. These advancements are pivotal for printed antennas, flexible hybrid electronics, wearable sensors, 3D printed circuitry, and semiconductor packaging, positioning nano-adhesives as a foundational technology for next-generation electronic manufacturing ecosystems.

Nano Adhesives Market Share Insights, 2025-2034

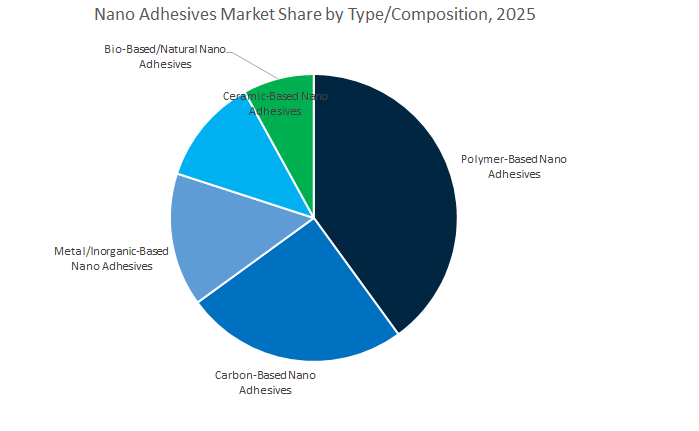

Market Share by Type/Composition

The polymer-based nano adhesives segment dominates the global nano adhesives market, accounting for a projected 41.4% share in 2025, owing to their superior mechanical performance, processability, and compatibility with existing adhesive manufacturing technologies. These formulations leverage nanoscale fillers such as silica, alumina, and titanium dioxide nanoparticles to significantly enhance tensile strength, adhesion, and heat resistance, making them the most versatile option for electronics, automotive, construction, and healthcare applications. Their ability to be easily incorporated into conventional epoxy, acrylic, or polyurethane systems has accelerated industrial adoption, particularly in microelectronics packaging, flexible circuits, and precision assembly lines. Furthermore, the increasing demand for lightweight, high-strength bonding solutions in the automotive and aerospace sectors continues to favor polymer-based nano adhesives, which offer improved fatigue resistance and dimensional stability over traditional formulations.

Carbon-based nano adhesives, including those utilizing carbon nanotubes (CNTs) and graphene nanocomposites, are rapidly emerging as a high-growth category due to their exceptional electrical and thermal conductivity. These adhesives are gaining traction in semiconductor interconnects, wearable devices, and advanced battery systems, where they enable efficient heat dissipation and enhanced electrical connectivity. Meanwhile, metal/inorganic and ceramic-based nano adhesives serve specialized roles in aerospace, defense, and high-temperature energy applications, where extreme environmental resistance and structural reliability are required. These materials exhibit superior thermal conductivity and oxidation resistance, positioning them as the adhesive of choice for engine components, turbines, and high-performance composites. On the sustainability front, bio-based nano adhesives are gaining attention for biomedical and consumer product applications, combining renewable raw materials with nano-enhanced bonding performance.

Market Share by End-Use Industry

The electronics and semiconductors segment leads the global nano adhesives market, capturing a projected 36.5% share in 2025, driven by the increasing miniaturization and functional density of modern electronic devices. Nano adhesives are essential in advanced semiconductor packaging, printed circuit board (PCB) assembly, and microelectronic component bonding, where they provide high precision, superior adhesion, and enhanced thermal management. The integration of nanofillers such as carbon nanotubes, silver nanoparticles, and silica enables adhesives to achieve high conductivity and low dielectric constants, essential for high-frequency and high-power electronic systems. As the demand for 5G infrastructure, IoT devices, and flexible electronics continues to surge, nano adhesives are becoming indispensable for ensuring device reliability, low outgassing, and long-term stability under varying operational conditions.

The medical and healthcare sector is another major growth area, driven by the increasing adoption of biocompatible nano adhesives in surgical instruments, dental applications, drug delivery systems, and implantable devices. These adhesives enable precise, durable, and sterile bonding, ensuring safety in critical medical environments. The aerospace and defense industry maintains a significant share, utilizing nano adhesives in lightweight composite bonding, satellite systems, and structural reinforcement, where high strength-to-weight ratios and resistance to radiation or temperature extremes are vital. Similarly, the automotive and transportation sector is embracing nano adhesives for EV battery assembly, lightweight panel bonding, and sensor integration, contributing to improved performance and energy efficiency. Energy applications, particularly in solar panels, wind turbines, and fuel cells, also represent a growing opportunity as nano adhesives offer superior thermal conductivity, corrosion resistance, and mechanical integrity under continuous stress.

The Global Nano Adhesives Market is moderately consolidated, with major players such as Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Dow Inc., and Sika AG investing heavily in nanocomposite formulations, high-temperature systems, and sustainable chemistry innovations. These companies are leveraging advanced material science to strengthen their competitive edge across key applications—ranging from electronics and EV battery bonding to aerospace composite assembly.

Henkel continues to lead the Nano Adhesives Market through its flagship Loctite brand, offering high-strength, nano-engineered epoxy and acrylic adhesives for aerospace, industrial, and automotive applications. Its LOCTITE EA series integrates nano-fillers that deliver superior temperature stability and enhanced stress resistance. In addition, Henkel’s R&D teams are incorporating bio-based and sustainable monomers to reduce environmental impact. Recent advancements in additive manufacturing resins demonstrate Henkel’s ability to combine nano-adhesive chemistry with 3D printing technologies, producing highly durable, complex structural components.

3M Company dominates the field of nano adhesive transfer tapes and pressure-sensitive films, widely adopted in flexible electronics and automotive manufacturing. Its 3M™ Ultra High Temperature Series, launched in May 2025, is capable of withstanding 540°F (280°C) for short-term exposure, making it ideal for reflow soldering and under-hood bonding. Through advanced nano-filler integration, 3M enhances both thermal conductivity and vibration damping. The company’s low-outgassing formulations, such as the 3M 9085 series, further extend the reliability of high-density semiconductor devices and aerospace sensors.

H.B. Fuller continues to strengthen its presence in industrial assembly, electronics, and specialty transportation sectors, emphasizing the development of nano-epoxy and nano-acrylic adhesives for high-load and high-heat environments. Its products are widely used in automotive lightweighting, EV battery packs, and composite bonding. The company’s Asia-Pacific expansion initiatives are aligned with the region’s booming electronics and automotive production, positioning Fuller as a global supplier for next-generation nano-bonding solutions. Further, its focus on automation-compatible adhesives ensures consistent, high-speed application efficiency for OEMs.

Dow Inc. combines its deep expertise in silicone chemistry and thermal management to develop thermally conductive nano-adhesives and encapsulants for EVs, aerospace, and defense electronics. These materials feature nano-silica and carbon-based fillers for improved conductivity and mechanical resilience in high-power modules. Dow’s sustainability strategy includes transitioning toward solvent-free, low-VOC formulations that align with global green manufacturing standards. With strong R&D capabilities and global production reach, Dow continues to play a critical role in the development of heat-resistant nano-bonding materials for next-generation technologies.

Sika AG integrates nano-technology into its polyurethane and epoxy adhesive systems (under Sikaflex and SikaPower brands) to enhance fatigue resistance, durability, and impact performance in automotive, marine, and aerospace applications. The company focuses on structural lightweighting by developing nano-reinforced adhesives suitable for CFRP and aluminum bonding, critical for reducing vehicle mass without compromising strength. Sika’s fire-retardant and thermally conductive nano-adhesive developments are key to ensuring safety and performance in EV battery modules and railcar assemblies. Its ongoing production expansions in emerging markets further consolidate its leadership in structural nano-bonding systems.

Country Analysis: Global Nano Adhesives Industry

United States: Innovation Driven by Defense, Electronics, and Biocompatible Nano Adhesives

The United States remains at the forefront of Nano Adhesives innovation, propelled by federal initiatives, defense-funded research, and a rapidly expanding consumer electronics base. The National Nanotechnology Initiative (NNI), featured prominently in the FY2024 U.S. Presidential Budget, underscores national priorities in nano-enabled materials development — including adhesives for defense, aerospace, and renewable energy applications. Recent DARPA-funded projects have accelerated research into Reversible Nano Adhesives, engineered for adaptive maintenance and on-demand disassembly in military and aerospace systems.

In the medical and healthcare domain, FDA oversight has prompted companies to develop biocompatible nano-polymer adhesives suitable for Class III implantable devices. Meanwhile, Silicon Valley’s semiconductor packaging ecosystem is seeing a surge in start-ups developing Anisotropic Conductive Adhesives (ACAs) for miniaturized electronics. The rise of flexible electronics has also led to breakthroughs in skin-friendly nano adhesives for wearable sensors and smart patches, optimizing comfort and long-term adhesion.

China: Expanding Capacity and Integrating Nano Adhesives into National Infrastructure and EV Growth

China’s Nano Adhesives market is advancing at a rapid pace, driven by industrial policy support, EV manufacturing, and large-scale infrastructure expansion. The government’s strategic emphasis on domestic self-sufficiency in advanced materials—reinforced through the Made in China 2025 initiative—has spurred massive R&D investments in graphene, carbon nanotubes (CNTs), and nano-silica production. With The, local adhesive formulators benefit from reduced raw material costs and enhanced supply chain stability. A reported 1.9% drop in Q2 2025 MMA and nanomaterial input costs has further strengthened the competitiveness of local producers.

High-performance Epoxy and Polyurethane Nano Adhesives are increasingly specified for EV battery thermal management, high-speed rail assembly, and prefabricated building systems. In parallel, 5G and data center investments are driving the demand for thermally conductive nano epoxy adhesives for server and telecom hardware. Major electronics manufacturers have also begun adopting UV-curing Nano Adhesives for OLED displays and flexible panels to enhance bonding precision and longevity. As regulatory frameworks tighten around VOC emissions, China’s adhesives market is rapidly converging with global sustainability standards, reinforcing its status as a manufacturing and innovation powerhouse.

Germany: Engineering Precision and Sustainable Innovation in Nano-Reinforced Adhesives

Germany dominates the European Nano Adhesives landscape, combining advanced manufacturing infrastructure with an unwavering commitment to sustainability and material innovation. Automotive giants are leading the integration of Nano-Reinforced Structural Adhesives in multi-material bonding applications, supporting the EU’s lightweighting and decarbonization objectives. Research organizations like the Fraunhofer Institutes have achieved breakthroughs in Nano-Structured Hot Melt Adhesives that deliver exceptional peel strength and durability, positioning Germany as a global leader in mechanical bonding efficiency.

The country’s industrial adhesives sector—anchored by firms such as Henkel and Covestro—continues to expand portfolios of solvent-free, reactive Nano Adhesives tailored for REACH-compliant manufacturing. Applications extend from wind turbine rotor blades to machinery assembly and electronic encapsulation, requiring vibration resistance and long-term adhesion reliability. Investments in automated dispensing systems have further strengthened Germany’s reputation as a center for scalable, precision-driven nano adhesive manufacturing.

Japan: High-Precision Nano Adhesives for Miniaturized Electronics and Structural Engineering

Japan is a technological leader in Nano Adhesive innovation, leveraging its deep expertise in electronics, photonics, and materials science. The country’s semiconductor ecosystem is fueling R&D in low-temperature curing Die-Attach Nano Adhesives optimized for 3D IC packaging, memory devices, and flexible displays. Japanese companies are pioneering Reworkable Edge Bonding Adhesives, such as Panacol Structalit 5705, that allow selective disassembly—essential for high-value OLED repair operations.

In infrastructure, Nano Adhesives are being tested in seismic-resistant structural components and high-speed rail car assemblies, offering superior fatigue and vibration resistance. R&D collaborations between academia and industry are advancing bio-compatible Nano Adhesives for optical imaging tools, endoscopy devices, and AR/VR optical lenses, emphasizing transparency and high-temperature performance. With its dual focus on miniaturization and durability, Japan remains a global benchmark for nano-enabled precision bonding solutions.

South Korea: Electronics Powerhouse Advancing Conductive and Self-Healing Nano Adhesives

South Korea’s Nano Adhesives industry is tightly integrated with its dominance in semiconductor fabrication, display technology, and EV manufacturing. Leading firms are investing in Silver Nanowire and Graphene-based formulations to enhance electrical conductivity in transparent electrodes and encapsulation adhesives for foldable OLED screens. The government’s targeted R&D funding for Self-Healing Nano Adhesives demonstrates a commitment to extending product lifespans in consumer electronics and automotive systems.

The medical technology sector in South Korea also plays a vital role, driving innovation in ultra-thin Electronic Skin Patch Adhesives that offer high flexibility and biocompatibility for long-term patient monitoring. Moreover, as EV exports grow, domestic automakers increasingly utilize Nano-Reinforced Structural Adhesives for battery protection, vibration dampening, and lightweight body structures. The nation’s continuous investment in nanomaterial synthesis, automation, and high-precision bonding cements its leadership in next-generation hybrid adhesive systems.

Switzerland: High-End Nano Adhesives for Precision Engineering and Biotech Applications

Switzerland represents the premium segment of the Nano Adhesives market, emphasizing quality, precision, and biocompatibility. The country’s specialty chemical manufacturers—such as Dätwyler Holding AG—are scaling production of solvent-free Nano-Polyurethane Adhesives for construction, industrial sealing, and advanced assembly applications. Swiss companies are at the forefront of micro-dispensing Nano Adhesives, meeting the precision needs of watchmaking, medical device assembly, and filtration technologies.

In the biotech and pharmaceutical sectors, innovation is focused on bio-inspired Nano Adhesives designed for drug delivery systems and wound closure applications, utilizing natural adhesion mechanisms to improve patient outcomes. Aerospace remains another strategic focus area, with Swiss R&D dedicated to fire-resistant, lightweight Nano Epoxy formulations that meet aviation-grade performance standards. With strong academic collaboration and precision manufacturing expertise, Switzerland continues to define the high-value frontier of nano-adhesive engineering.

Nano Adhesives Market Report Scope

Nano Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.8 Billion

|

|

Market Size (2034)

|

$37.2 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type (Polymer-Based, Ceramic-Based, Bio-Based/Natural, Metal/Inorganic-Based, Carbon-Based), By Filler Type (Structurally Reinforced, Functionally Enhanced, Bio-Mimetic/Gecko, Nanoporous/Meso-porous), By Form (Liquid/Dispersion, Film/Tape, Paste, Preformed Gaskets/Sealants), By Application (Die Attach and Semiconductor Packaging, Flexible and Printed Electronics, Structural Bonding, Medical Devices and Wearables, Optoelectronics and Photonics, Battery Thermal Management), By End-Use Industry (Electronics and Semiconductors, Automotive and Transportation, Aerospace and Defense, Medical and Healthcare, Construction and Infrastructure, Energy

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, Arkema S.A., H.B. Fuller Company, BASF SE, Dupont de Nemours, Inc., Dexerials Corporation, Panacol-Elosol GmbH, DELO Industrial Adhesives, Elkem ASA, Cabot Corporation, Wacker Chemie AG, LG Chem Ltd., Nan Ya Plastics Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type/Composition

- Polymer-Based

- Ceramic-Based

- Bio-Based/Natural

- Metal/Inorganic-Based

- Carbon-Based

By Filler Type/Mechanism

- Structurally Reinforced

- Functionally Enhanced

- Bio-Mimetic/Gecko

- Nanoporous/Meso-porous

By Form

- Liquid/Dispersion

- Film/Tape

- Paste

- Preformed Gaskets/Sealants

By Application

- Die Attach and Semiconductor Packaging

- Flexible and Printed Electronics

- Structural Bonding

- Medical Devices and Wearables

- Optoelectronics and Photonics

- Battery Thermal Management

By End-Use Industry

- Electronics and Semiconductors

- Automotive and Transportation

- Aerospace and Defense

- Medical and Healthcare

- Construction and Infrastructure

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Nano Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- Arkema S.A.

- H.B. Fuller Company

- BASF SE

- Dupont de Nemours, Inc.

- Dexerials Corporation

- Panacol-Elosol GmbH

- DELO Industrial Adhesives

- Elkem ASA

- Cabot Corporation

- Wacker Chemie AG

- LG Chem Ltd.

- Nan Ya Plastics Corporation

*- List not Exhaustive

Research Coverage

This report investigates the Nano Adhesives Market, delivering analysis reviews of demand inflection points across semiconductors, EV thermal management, aerospace composites, renewable power, and advanced medical devices; it curates breakthroughs in nano-engineered systems—such as CNT/graphene, silica/alumina, and silver-filled formulations—that unlock ultra-thin bond lines, superior heat/electrical conductivity, and high-temperature structural reliability; it highlights manufacturability (film/tape, paste, liquid/dispersion, preforms), automation readiness for precision micro-dispensing, and sustainability trajectories aligned to low-VOC and REACH frameworks; developed by USDAnalytics, this report is an essential resource for product managers, materials scientists, sourcing leaders, and investors who require defensible forecasts, competitive benchmarking, and clear route-to-market strategies in nano-enabled bonding technologies.

Scope Highlights

Segmentation:

- By Type/Composition: Polymer-Based; Ceramic-Based; Bio-Based/Natural; Metal/Inorganic-Based; Carbon-Based.

- By Filler Type/Mechanism: Structurally Reinforced; Functionally Enhanced; Bio-Mimetic/Gecko; Nanoporous/Meso-porous.

- By Form: Liquid/Dispersion; Film/Tape; Paste; Preformed Gaskets/Sealants.

- By Application: Die Attach and Semiconductor Packaging; Flexible and Printed Electronics; Structural Bonding; Medical Devices and Wearables; Optoelectronics and Photonics; Battery Thermal Management.

- By End-Use Industry: Electronics and Semiconductors; Automotive and Transportation; Aerospace and Defense; Medical and Healthcare; Construction and Infrastructure; Energy.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies with strategies, portfolios, and recent developments.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.