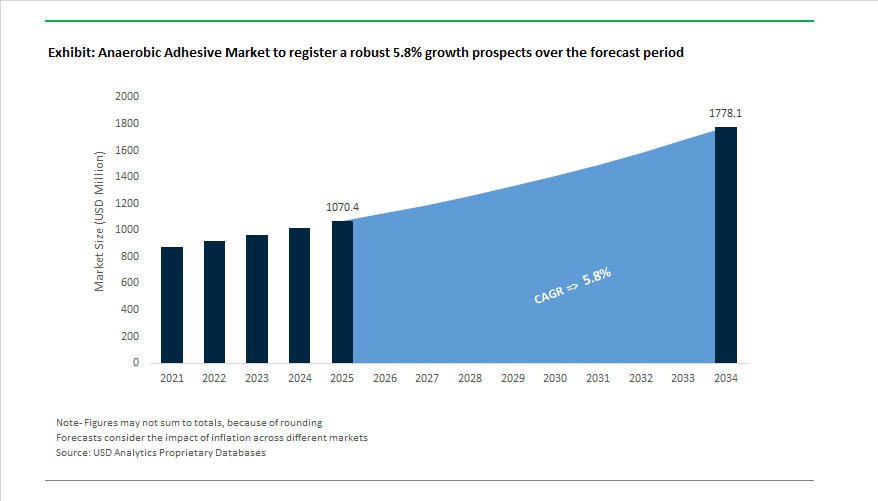

The global anaerobic adhesive market is projected to expand from USD 1,070.4 million in 2025 to USD 1,777.9 million by 2034, registering a 5.8% CAGR, as OEMs and Tier-1 suppliers increasingly specify anaerobic chemistries for threadlocking, retaining, flange sealing, and form-in-place gasketing (FIPG) in mechanically stressed assemblies. Growth is fundamentally driven by the need for vibration-resistant, leak-free joints that outperform traditional mechanical fasteners, gaskets, and PTFE tapes under thermal cycling, pressure pulsation, and dynamic loads.

Leading manufacturers such as Henkel (LOCTITE®), Permabond, ThreeBond, Hylomar, and Parker LORD position anaerobic adhesives as functional structural elements rather than auxiliary consumables. Modern retaining compounds and threadlockers are engineered to deliver high shear strength, controlled cure kinetics, and long-term chemical resistance, enabling downsizing of mechanical components while improving joint reliability. LOCTITE® high-performance anaerobic grades are validated for continuous service temperatures up to ~230 °C, with short-term exposure capability approaching 340 °C, supporting demanding applications in powertrain assemblies, exhaust systems, turbines, and rotating equipment.

Pressure integrity remains a core adoption driver. Manufacturer data from Permabond, ThreeBond, and Hylomar confirms that anaerobic pipe thread sealants routinely achieve leak-free sealing up to ~1,000 psi, even in hydraulic oils, fuels, steam, and hydrocarbons. Unlike PTFE tapes or paste sealants, anaerobic systems cure into a thermoset polymer within the thread interface, eliminating cold flow, vibration loosening, and re-torque requirements—critical for industrial fluid handling and automotive systems.

Manufacturing efficiency and automation compatibility increasingly shape product selection. Fast-cure anaerobic formulations, enabled by advanced activator and initiator chemistry, achieve fixture times below 10 minutes on passive substrates such as stainless steel, plated fasteners, and aluminum. This capability is heavily promoted by LOCTITE®, ThreeBond, and Parker LORD for robotic dispensing, high-speed assembly lines, and in-line quality assurance, where predictable cure profiles and minimal downtime are essential. At the component level, gap-filling performance is expanding the functional envelope of anaerobic gasketing materials. High-viscosity FIP gasketing compounds from manufacturers like ThreeBond and Hylomar reliably fill joint gaps up to ~0.5 mm (0.020 in), maintaining oil and pressure sealing across engine blocks, gearboxes, compressors, and pump housings. This capability reduces machining tolerances, eliminates inventory of pre-cut gaskets, and supports modular assembly strategies.

The anaerobic adhesives industry has entered a phase of rapid innovation and diversification, marked by new product developments, strategic partnerships, and sustainability-oriented R&D investments. In September 2025, Henkel (LOCTITE®) launched a high-speed curing anaerobic adhesive tailored for automotive and industrial assembly lines, enabling faster fixture times on both active and passive metals. This innovation underscores Henkel’s strategic focus on e-mobility, precision assembly, and reduced cycle times, reflecting the global manufacturing shift toward smart factory operations.

In the same month, Sekisui Chemical introduced a fast-curing anaerobic adhesive in Japan, specifically optimized for precision metal bonding in high-volume electronics manufacturing. The launch reinforces the growing importance of anaerobic adhesives in consumer electronics, where micro-tolerance, dimensional accuracy, and bonding uniformity are paramount. Earlier, in August 2025, 3M Company announced a $100 million investment in R&D aimed at developing eco-friendly anaerobic formulations with superior chemical resistance, aligning with global initiatives for sustainable and low-emission manufacturing materials. In parallel, Nitto Denko (Japan) invested in the development of high-strength anaerobic adhesives with enhanced temperature and chemical stability, targeting automotive assembly and industrial machinery bonding applications.

July 2025 witnessed multiple significant product introductions. Permabond Engineering Adhesives launched a next-generation high-temperature anaerobic threadlocker designed for aerospace and defense-grade applications, capable of withstanding extreme cyclic thermal stresses. Around the same time, DIC Corporation introduced a metal-to-metal anaerobic sealant formulated for industrial machinery and automotive assemblies, emphasizing precision sealing and reduced solvent use. In June 2025, Illinois Tool Works (ITW) began pilot testing of robotic adhesive dispensing systems integrated directly into automated assembly lines, while Mitsui Chemicals completed a successful pilot project on anaerobic adhesive integration to improve bonding consistency and cycle time across automated manufacturing environments.

This series of launches and investments demonstrates the industry’s focus on four strategic priorities — faster cure speed, eco-friendly formulations, automated application compatibility, and extended service temperature and pressure performance. These advancements position anaerobic adhesives as indispensable in automotive electrification, aerospace assembly, and precision electronics manufacturing, strengthening their role in the global industrial adhesives ecosystem.

As the global automotive industry pivots toward electrification and advanced mobility, anaerobic adhesives are playing a pivotal role in ensuring durability, chemical resistance, and thermal stability across critical EV assemblies. The transition from cell-to-module (CTM) and cell-to-pack (CTP) architectures to cell-to-chassis (CTC) designs has heightened the need for adhesives capable of withstanding higher temperatures, electrical insulation demands, and exposure to novel coolants and lubricants.

In an October 2025 announcement, Wacker Chemical Corporation introduced its hybrid silane-terminated polyether (STP-E) adhesive, offering the flexibility of silicone combined with the mechanical strength of organic polymers—an essential property for maintaining battery pack structural integrity under thermal cycling and vibration stress. Such innovations highlight the industry’s move toward hybrid anaerobic formulations capable of delivering multi-functional performance for battery housing, e-mobility motors, and high-voltage connections.

Traditional anaerobic adhesives typically perform up to 150°C (302°F) and resist degradation from hydraulic oils and lubricants. However, modern high-temperature formulations endure 230°C (446°F) or more, a performance threshold critical for powertrain components, threaded joints, and high-temperature pipe sealing systems. These advancements are reinforced by empirical performance data showing that over 70% of threaded joints in EV traction assemblies utilize anaerobic threadlockers, replacing heavier mechanical devices like lock washers and split pins—directly supporting lightweighting initiatives and improving overall vehicle efficiency and range.

From a chemical compatibility standpoint, anaerobic adhesives also demonstrate exceptional resistance to modern EV-specific fluids, such as ethylene glycol-based coolants and specialized transmission oils. The ensures reliable long-term sealing and mechanical bonding even under continuous thermal cycling—making anaerobic adhesives indispensable for the next generation of electric and hybrid propulsion systems.

The global shift toward low-emission manufacturing and ESG-driven production is reshaping the formulation chemistry of anaerobic adhesives. Regulators, particularly in Europe, are enforcing stricter VOC limits under the REACH framework, compelling manufacturers to eliminate solvent-based components and hazardous monomers while maintaining mechanical performance and curing reliability.

Europe’s evolving environmental policies are driving label-free, solvent-free anaerobic threadlockers and sealants, formulated using next-generation dimethacrylate monomers with minimal toxicological impact. These new-generation adhesives combine low odor, low skin sensitization potential, and reduced environmental footprint, aligning with corporate sustainability targets and ISO 14001-compliant manufacturing practices.

In parallel, adjacent adhesive technologies demonstrate the market potential for zero-emission systems. A leading manufacturer’s water-based rubber-to-substrate adhesive recently achieved VOC emission reduction from over 11 kg to zero per kilogram of dried adhesive, showcasing the feasibility of fully solvent-free bonding chemistries—a model influencing the anaerobic adhesive sector.

Further, the inherent low-toxicity profile of dimethacrylate-based anaerobics positions them favorably against competing chemistries, offering a natural pathway toward regulatory compliance without compromising adhesion strength or cure speed. The balance of operator safety, sustainability, and performance consistency is becoming a major purchasing criterion for industrial buyers in the automotive, aerospace, and heavy machinery sectors, where regulatory audits increasingly evaluate chemical safety and workplace air quality.

The rise of industrial 3D printing presents a powerful growth opportunity for anaerobic adhesives in post-processing and hybrid assembly applications. The size limitations of additive manufacturing platforms necessitate the bonding of multiple printed components, and anaerobic adhesives offer the ideal solution—enabling structural integrity, dimensional precision, and high-strength bonding between metallic and polymeric substrates.

Studies indicate that adhesively bonded 3D-printed joints can achieve mechanical strength equivalent to the base polymer material, a crucial factor for load-bearing and functional assemblies. The combination of anaerobic and structural acrylic systems is particularly effective in joining metals to high-performance plastics such as ABS, PETG, and carbon-filled Nylon 6 or Nylon 12 (PA6/PA12), common in aerospace prototypes, industrial tools, and automotive lightweighting parts.

A key advantage in additive manufacturing lies in the surface topology of 3D-printed parts, which enhances micromechanical interlocking. Techniques like Selective Laser Sintering (SLS) or Fused Deposition Modeling (FDM) naturally produce slightly porous textures that improve adhesive wetting and bonding strength. The compatibility opens new avenues for adhesive-assisted modular design, particularly where lightweight hybrid assemblies combine printed thermoplastics and machined metals.

As the 3D printing sector continues to industrialize, with AM system sales growing at over 20% annually, the role of anaerobic adhesives in post-processing will expand—anchoring their importance as a precision bonding solution for high-performance additive manufacturing environments.

The ongoing miniaturization of consumer and automotive electronics has created a multi-billion-dollar opportunity for anaerobic adhesives—particularly threadlockers, retaining compounds, and sealants—that deliver high reliability, vibration damping, and micro-gap sealing in small-scale assemblies.

With modern vehicles integrating over 3,000 electronic sub-assemblies, anaerobic threadlockers are crucial for securing miniature fasteners in infotainment modules, sensors, and electronic control units (ECUs). By filling micro-gaps and curing to a solid thermoset plastic, these adhesives eliminate micro-vibration-induced loosening, prevent fretting corrosion, and maintain long-term torque retention, which is vital for vehicle safety systems and consumer electronics durability.

In precision consumer devices like smartphones and wearables, specialized low-viscosity anaerobic formulations are applied to fasteners as small as M1.4 or M1.6 threads, providing consistent clamp load retention even under repeated mechanical shocks. The technology not only enhances mechanical reliability but also supports design freedom for compact, non-serviceable enclosures, aligning with modern product design philosophies emphasizing slim profiles and structural integrity.

Additionally, anaerobic retaining compounds play an indispensable role in electromechanical systems, securing miniature bearings, shafts, and bushings in small motors and actuators. By creating 100% surface contact within cylindrical joints, these adhesives prevent movement and wear—extending product lifespan and reducing the need for frequent maintenance in precision systems.

Anaerobic Adhesive Market Share Insights, 2025-2034

The metals segment overwhelmingly dominates the global anaerobic adhesive industry, accounting for nearly 85% of the total market share in 2025. This dominance is rooted in the unique chemistry of anaerobic adhesives, which cure only in the absence of oxygen and in the presence of active metal ions—a combination ideally suited for steel, aluminum, brass, copper, and other alloys. These adhesives are indispensable in mechanical assembly, powertrain, aerospace, and heavy machinery applications, where they are used extensively for threadlocking, retaining bearings, flange sealing, and gasketing. Their ability to withstand vibration, prevent loosening, and seal against fluids makes them a cornerstone of industrial reliability. As manufacturers strive for zero-maintenance mechanical joints and extended equipment life, the demand for high-performance anaerobic adhesives continues to surge. In industries such as automotive and wind energy, where metal-to-metal bonding precision is critical, anaerobics are increasingly favored over mechanical fasteners and tapes due to their uniform stress distribution, chemical resistance, and temperature endurance. The segment’s dominance is further reinforced by the ongoing industrial automation wave, where anaerobics support high-precision metal assembly operations with consistent, long-term bonding strength.

The plastics and composites segment, though smaller, is experiencing steady growth driven by lightweighting and material diversification trends across modern manufacturing. Traditional anaerobic adhesives are metal-dependent, but advancements in formulation chemistry allow the use of surface activators and primers to enable curing on plastics and fiber-reinforced composites. This has opened new opportunities in electronics, consumer goods, and electric vehicle components, where weight reduction and non-metallic assemblies are key design imperatives. For instance, anaerobic adhesives are increasingly used for sealing plastic housings, bonding thermoset composites, and securing inserts or fasteners in hybrid material structures. The segment’s growth is further supported by the miniaturization of devices and the demand for clean, vibration-resistant bonding solutions that eliminate mechanical fasteners. However, adoption remains niche compared to metal applications, as surface preparation and activator compatibility remain essential to ensure performance reliability. Nevertheless, as composite materials continue to proliferate in aerospace and EV design, this segment is poised for incremental yet meaningful expansion within the broader anaerobic adhesives market.

The other engineering materials segment remains a highly specialized and low-volume domain, underscoring the material-specific nature of anaerobic technology. Applications in ceramics, glass, or non-reactive metals (like titanium) are rare due to the lack of surface activity required for polymerization. In such cases, secondary activators or hybrid adhesive systems are often employed to facilitate bonding, but these solutions fall outside the traditional anaerobic chemistry spectrum. The limited penetration into this category highlights the technology’s precise performance niche—optimized for metallic interfaces where chemical resistance, gap-filling, and mechanical strength are paramount.

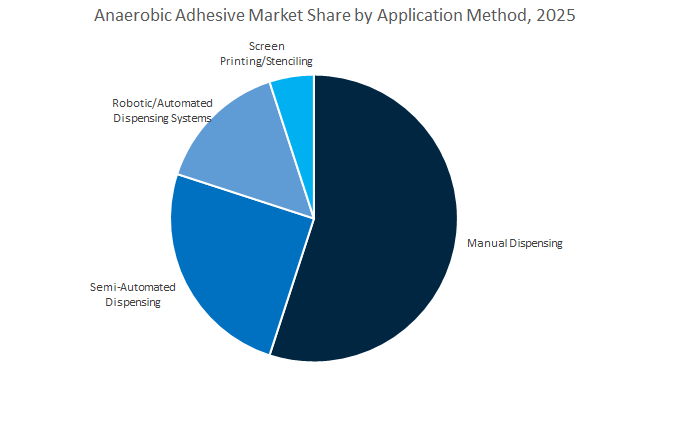

The manual dispensing segment continues to hold the largest share of the global anaerobic adhesive market, accounting for approximately 55% of total applications in 2025. This dominance is attributed to the widespread use of anaerobic adhesives in maintenance, repair, and overhaul (MRO) operations and low-to-medium volume assembly environments where flexibility and ease of application are paramount. Manual dispensing—typically through bottles with precision needle tips or handheld dispensing guns—offers simplicity, minimal setup, and adaptability across diverse repair scenarios. The segment is particularly strong in industrial equipment servicing, automotive workshops, and field maintenance, where operators rely on anaerobic adhesives for threadlocking, sealing, and retaining applications without the need for curing equipment or heat. Its continued prevalence is also supported by the cost-effectiveness and portability of manual methods, making it the go-to choice for small-scale users and aftermarket applications. Despite the growth of automation, manual dispensing remains a mainstay for flexibility-driven industries, where product reliability and ease of use outweigh process automation priorities.

The semi-automated and robotic dispensing systems segment is the fastest-growing category, fueled by the global push toward precision manufacturing, repeatability, and process optimization. These systems—ranging from benchtop pneumatic dispensers to fully robotic, multi-axis platforms—are increasingly adopted in automotive, electronics, and aerospace assembly lines where consistency, minimal waste, and micro-volume accuracy are essential. Automated dispensing ensures precise adhesive dosing and uniform bond line control, particularly in applications like threadlocking of fasteners, bearing retention, and flange sealing on high-volume production runs. Robotics also enable closed-loop feedback systems and vision-guided pattern placement, improving both quality assurance and process throughput. Moreover, the rise of Industry 4.0 integration and smart manufacturing has further accelerated adoption, as dispensing systems feature programmable controls, digital flow monitoring, and data traceability. The use of anaerobic adhesives with automation-compatible viscosities and cure profiles is becoming a key enabler for scalable, lean production. As manufacturers pursue zero-defect assembly processes and reduced rework rates, automated dispensing systems are reshaping the operational dynamics of the anaerobic adhesive landscape.

The screen printing and stenciling application segment, while niche, plays a critical role in form-in-place (FIP) gasket manufacturing for engines, pumps, compressors, and hydraulic systems. This method allows for precise, repeatable deposition of anaerobic sealants onto flanges or mating surfaces, forming a continuous, customized gasket that replaces traditional cut gaskets. The process ensures uniform thickness, minimal material waste, and excellent sealing performance, making it invaluable for high-performance machinery and aerospace engine assemblies. Screen printing also enhances process efficiency in OEM lines by reducing assembly time and improving alignment accuracy, particularly in complex or curved geometries. The growing adoption of CNC-integrated stenciling platforms and robotic FIP gasket systems has further improved productivity and consistency. The segment underscores the precision engineering trend in anaerobic sealant applications, where form-in-place gasketing delivers superior durability, leak resistance, and lifecycle reliability.

The global anaerobic adhesives market is dominated by technology-driven companies including Henkel AG & Co. KGaA (LOCTITE®), 3M Company, Illinois Tool Works (ITW), Permabond Engineering Adhesives, and Huntsman Corporation. Each player leverages its chemical expertise, global distribution networks, and automation-driven innovation to serve automotive, aerospace, and industrial assembly markets with advanced adhesive solutions that combine durability, environmental compliance, and process efficiency.

Henkel dominates the anaerobic adhesive market with its LOCTITE® brand, offering the widest portfolio of threadlockers, retaining compounds, and gasketing sealants. Products such as LOCTITE® 620 deliver continuous temperature resistance up to 230°C, enabling their use in automotive transmissions, turbines, and exhaust assemblies. The company’s strategic focus on e-mobility and lightweighting positions its anaerobic solutions in battery packs, electric motors, and powertrain assemblies. Henkel also provides automated dispensing and curing systems, integrating its adhesives seamlessly into robotic manufacturing lines to improve precision and reduce assembly time.

3M combines its materials science expertise with sustainability innovation, investing $100 million in R&D (August 2025) to develop eco-friendly anaerobic adhesives with enhanced chemical resistance. The company’s 3M™ Scotch-Weld™ Anaerobic Adhesives are designed for threadlocking, pipe sealing, and retaining applications, ensuring leak-proof protection against hydraulic fluids and hydrocarbons. 3M’s anaerobic product line supports vibration-dampening and noise reduction (NVH) performance in automotive and transportation sectors. Through its global technical support and OEM partnerships, 3M continues to strengthen its presence in electronics, aerospace, and general manufacturing markets.

Illinois Tool Works, through its Permatex® brand, leads in MRO and automotive aftermarket adhesives, offering robust flange sealants and threadlockers designed for high-temperature and heavy-duty environments. In June 2025, ITW launched a pilot program integrating anaerobic adhesive dispensing into robotic assembly lines, boosting production precision and cycle speed. Products like Permatex® Orange Threadlocker combine high strength with removability, making them ideal for maintenance-intensive industries. The company’s anaerobic sealants, capable of filling 0.020-inch gaps, are widely used for engine gasketing, transmission covers, and petrochemical sealing applications.

Permabond specializes in engineering-grade anaerobic adhesives that outperform traditional mechanical joints by delivering up to five times greater load-carrying capacity. Its high-temperature threadlocker launched in July 2025 targets aerospace and defense sectors requiring thermal and vibration stability under extreme conditions. The company’s low-viscosity wicking-grade adhesives enable post-assembly sealing and porosity filling, while PTFE-based pipe sealants deliver instant 1,000 psi pressure resistance. With a focus on custom formulations for non-destructive disassembly, Permabond caters to OEMs seeking precision, flexibility, and NSF-certified reliability.

Huntsman leverages its expertise across epoxy, polyurethane, and acrylate chemistries to deliver multi-material bonding solutions in aerospace, automotive, and industrial equipment sectors. While renowned for its Araldite® structural adhesives, the company is also expanding its anaerobic product offerings for retention, gasketing, and metal bonding. Its strategy centers on weight reduction and stress distribution, replacing traditional fasteners with lightweight adhesive systems. Huntsman’s anaerobic adhesives complement its broader portfolio in wind energy, machinery assembly, and transportation, aligning with sustainability and performance-driven manufacturing trends.

The U.S. anaerobic adhesive market remains a global innovation hub, led by strong industrial R&D, sustainability mandates, and large-scale EV and aerospace production. In September 2025, Henkel (Loctite) completed a major expansion of its Brandon, South Dakota facility, boosting production for thermal management and anaerobic adhesive solutions crucial to EV battery and electronics manufacturing.

Innovation continues at a fast pace, with Loctite launching a new high-performance anaerobic adhesive (September 2025) engineered for faster curing on metal assemblies, significantly improving assembly efficiency for automotive and industrial equipment manufacturers. Meanwhile, 3M’s $100 million R&D investment (August 2025) is targeting eco-friendly anaerobic adhesives with enhanced chemical resistance and sustainability profiles, aligning with North American low-VOC regulatory standards.

The Environmental Protection Agency (EPA)’s National VOC Emission Standards (effective January 2025) are prompting a strategic shift toward solvent-free threadlockers and gasket sealants. Concurrently, Permabond’s July 2025 aerospace-grade threadlocker optimized for high-temperature service marks a leap in performance for defense and aerospace applications. Industrial automation is another major trend—Illinois Tool Works (ITW) initiated robotic integration pilots (June 2025) that use automated anaerobic dispensing systems, reducing cycle times and enhancing consistency.

Germany’s anaerobic adhesive industry anchors Europe’s precision manufacturing landscape, with a distinct focus on decarbonization, digitalized production, and automotive innovation. In October 2025, Henkel and Dow expanded their global collaboration to integrate low-carbon feedstocks into adhesive production—reducing the product carbon footprint while advancing Germany’s EU Green Deal goals.

Leading manufacturer DELO Industrial Adhesives continues to set benchmarks in microelectronics assembly, validating its directional conductive adhesives for miniLED applications, ensuring reliability in high-precision electronic retaining systems. Its August 2025 lens-bonding solution demonstrates innovation in automotive camera module adhesives, supporting next-generation autonomous driving technologies.

Germany remains Europe’s largest vehicle production hub, creating massive baseline demand for anaerobic threadlockers, flange sealants, and retaining compounds for engine and transmission assembly. Henkel’s sustainability roadmap, which incorporates renewable electricity and circular feedstocks, ensures compliance with EU REACH regulations, further reinforcing Germany’s leadership in eco-efficient chemical manufacturing.

China dominates the Asia-Pacific anaerobic adhesive market, driven by enormous manufacturing volume in automotive, electronics, and industrial machinery. The country’s strategic objective under the “Made in China 2025” initiative is strengthening domestic chemical manufacturing self-reliance, prompting rapid local production capacity expansions for aerospace- and automotive-grade anaerobic adhesives.

As the world’s largest vehicle manufacturer, China’s baseline demand for anaerobic threadlockers, retaining compounds, and flange sealants remains unmatched. Local manufacturers are scaling cost-efficient production for industrial fasteners and heavy machinery applications, while foreign players continue expanding local operations through joint ventures and acquisitions to secure market presence.

The booming electronics manufacturing sector—including smartphones, consumer devices, and industrial controls—is a key growth driver for low-viscosity, rapid-curing anaerobic adhesives designed for micro-fastener locking. The growing EV battery ecosystem further accelerates demand for adhesives with vibration resistance and high mechanical strength, particularly for e-motors and drivetrain components.

Japan’s anaerobic adhesive industry is defined by precision, reliability, and material excellence. The country’s manufacturing ecosystem—spanning high-tech automotive, advanced robotics, and miniaturized electronics—requires ultra-pure, high-strength anaerobic adhesives engineered for performance and precision.

Sekisui Chemical (September 2025) launched a fast-curing anaerobic adhesive tailored for high-speed electronic assembly lines, addressing the critical need for precision metal bonding in compact device manufacturing. Simultaneously, Nitto Denko continues to lead in chemical-resistant anaerobic formulations capable of enduring extreme mechanical and chemical stresses found in heavy machinery and EV propulsion systems.

DIC Corporation’s July 2025 release of a next-generation anaerobic sealant optimized for complex metal assemblies reinforces Japan’s dominance in industrial adhesives for high-specification mechanical parts. Additionally, Mitsui Chemicals’ automation pilot project (June 2025) successfully integrated anaerobic adhesives into fully robotic assembly lines, marking a new era of precision and productivity in Japanese manufacturing.

India is fast emerging as a high-growth anaerobic adhesives market, underpinned by large-scale automotive component manufacturing, infrastructure development, and industrial modernization. Henkel’s facility at Kurkumbh continues to play a central role in meeting local demand for high-performance threadlockers, gasketing compounds, and retaining adhesives, enabling supply chain independence.

The country’s thriving automotive Tier 1 and Tier 2 ecosystem drives sustained consumption of high-torque anaerobic compounds for gearbox, powertrain, and fastener assembly. Simultaneously, India’s infrastructure boom—spanning energy, transportation, and defense—necessitates pressure-resistant anaerobic pipe sealants for oil & gas and power sectors.

Government initiatives like “Make in India” are fostering domestic adhesive R&D, while industrial automation adoption is spurring the use of faster-curing formulations for high-throughput assembly operations. India’s diverse climate conditions further stimulate demand for temperature- and humidity-resistant anaerobic sealants, vital for long-term durability in challenging environments.

South Korea’s anaerobic adhesive market is rapidly scaling, powered by its dominance in electric vehicle battery manufacturing, advanced electronics, and semiconductor assembly. The Henkel Songdo facility, operational since 2022, represents a €30 million global hub for electronics adhesives, meeting the precision demands of miniaturized device bonding and micro-assembly applications.

The nation’s leadership in EV technology drives high demand for vibration-resistant anaerobic retaining compounds, critical for securing rotors, e-axles, and drivetrain fasteners in high-speed electric motors. Advanced chemical firms are also innovating heat-stable anaerobic formulations capable of withstanding thermal cycling within EV battery modules.

South Korea’s industrial innovation and automation focus further integrate smart dispensing systems for consistent sealant application in mass-production lines, positioning the country as a technology-intensive hub for anaerobic adhesive innovation in Asia.

Anaerobic Adhesive Market Report Scope

Anaerobic Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1070.4 Million

|

|

Market Size (2034)

|

$1777.9 Million

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Product Type (Threadlockers, Thread Sealants, Retaining Compounds, Gasketing Compounds, Weld Sealants), By Substrate Material (Metals, Plastics and Composites, Other Engineering Materials), By Application Method (Manual Dispensing, Semi-Automated Dispensing, Robotic/Automated Dispensing Systems, Screen Printing/Stenciling), By Curing Mechanism (Standard Cure, Heat-Accelerated Cure, Primer/Activator-Accelerated Cure), By Viscosity/Gap Fill (Low Viscosity, Medium Viscosity, High Viscosity, Large Gap Filling), By End-Use Industry (Automotive and Transportation, Electrical and Electronics, Industrial Machinery & Equipment, Building and Construction, Aerospace, Oil & Gas, DIY/Consumer

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Permabond LLC, DELO Industrial Adhesives, Sika AG, Arkema, Illinois Tool Works Inc., Dymax Corporation, Huntsman Corporation, Wacker Chemie AG, Master Bond Inc., TANGIT, ThreeBond Holdings Co., Ltd., Anabond Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Threadlockers

- Thread Sealants

- Retaining Compounds

- Gasketing Compounds

- Weld Sealants

By Substrate Material

- Metals

- Plastics and Composites

- Other Engineering Materials

By Application Method

- Manual Dispensing

- Semi-Automated Dispensing

- Robotic/Automated Dispensing Systems

- Screen Printing/Stenciling

By Curing Mechanism

- Standard Cure

- Heat-Accelerated Cure

- Primer/Activator-Accelerated Cure

By Viscosity/Gap Fill

- Low Viscosity

- Medium Viscosity

- High Viscosity

- Large Gap Filling

By End-Use Industry

- Automotive and Transportation

- Electrical and Electronics

- Industrial Machinery & Equipment

- Building and Construction

- Aerospace

- Oil & Gas

- DIY/Consumer

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Permabond LLC

- DELO Industrial Adhesives

- Sika AG

- Arkema

- Illinois Tool Works Inc.

- Dymax Corporation

- Huntsman Corporation

- Wacker Chemie AG

- Master Bond Inc.

- TANGIT

- ThreeBond Holdings Co., Ltd.

- Anabond Limited

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Anaerobic Adhesive Market across products, substrates, curing routes, and application methods; our analysis reviews qualification needs, automation readiness, and lifecycle performance under heat, pressure, and vibration. It highlights temperature-capable threadlockers, high-pressure thread sealants, gap-filling gasketing compounds, and factory-friendly activator systems that unlock rapid fixture on passive metals. We benchmark leaders on cure speed, chemical resistance, shear/torque retention, and ESG progress, quantify demand across OEM lines and MRO, and map risks tied to VOC rules and feedstock volatility. Technology breakthroughs—from <10-minute fixture anaerobics to 230 °C service grades and robotic dosing—are translated into throughput, scrap, and warranty impacts. Combining bottom-up consumption models with platform, EV, and precision-machinery growth curves, this report is an essential resource for engineering, sourcing, and operations teams seeking cost-down with quality-up in metal assemblies.

Scope Includes

- By Product Type: Threadlockers; Thread Sealants; Retaining Compounds; Gasketing Compounds; Weld Sealants

- By Substrate Material: Metals; Plastics & Composites; Other Engineering Materials

- By Application Method: Manual Dispensing; Semi-Automated Dispensing; Robotic/Automated Dispensing Systems; Screen Printing/Stenciling

- By Curing Mechanism: Standard Cure; Heat-Accelerated Cure; Primer/Activator-Accelerated Cure

- By Viscosity/Gap Fill: Low; Medium; High; Large Gap Filling

- By End-Use Industry: Automotive & Transportation; Electrical & Electronics; Industrial Machinery & Equipment; Building & Construction; Aerospace; Oil & Gas; DIY/Consumer

- Geographic Scope: 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

- Time Horizon: Historic 2021–2024; Forecast 2025–2034

- Companies: 15+ company analysis/profiles (strategy, portfolio, certifications)

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.