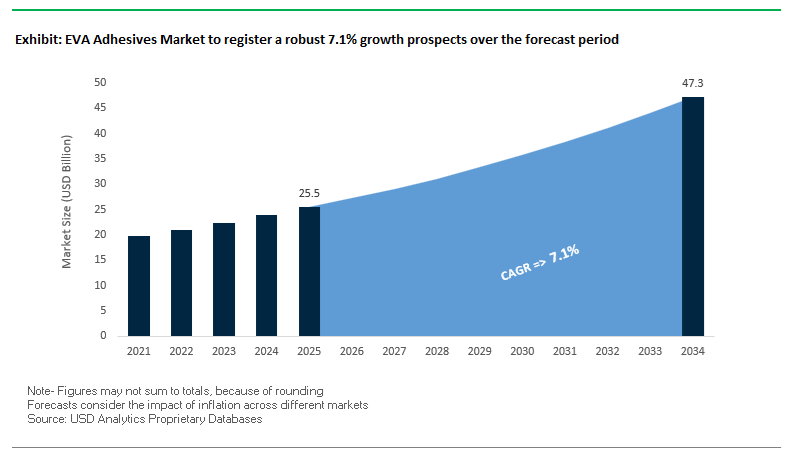

The Global EVA Adhesives Market is projected to expand from USD 25.5 billion in 2025 to USD 47.3 billion by 2034, advancing at a CAGR of 7.1%, as EVA-based bonding systems continue to scale across packaging, footwear, photovoltaic modules, and construction. Growth is structurally driven by EVA’s ability to balance processability, thermal stability, flexibility, and cost efficiency while remaining compliant with tightening VOC and odor regulations. As OEMs and converters pursue higher line speeds, lower application temperatures, and recyclable or low-emission material stacks, EVA adhesives—particularly hot melts and encapsulation grades—are increasingly specified as baseline solutions rather than secondary options. The market is simultaneously shifting toward higher vinyl acetate (VA) content grades, low-odor formulations, and bio-compatible copolymers, aligning EVA chemistry with circular economy and sustainability mandates without disrupting existing manufacturing infrastructure.

From a manufacturing and performance standpoint, EVA adhesives are deeply embedded in high-throughput packaging and converting operations. High-MFI EVA hot melt formulations (≥800 g/10 min) are enabling rapid wet-out, short set times, and consistent bond formation on automated lines used in bookbinding, case sealing, and flexible food packaging. Premium high-VA EVA grades (≥28% VA) are increasingly selected where enhanced tack, peel strength, and flexibility are required, particularly in flexible laminates and performance packaging substrates. Typical softening points in the 70–85°C range and application temperatures of 120–140°C allow EVA adhesives to support low-temperature processing, reducing energy consumption and minimizing thermal stress on heat-sensitive substrates such as films, papers, and nonwovens. These characteristics position EVA as a process-enabling adhesive platform in environments where uptime, consistency, and substrate versatility are critical.

In renewable energy and advanced materials, EVA’s role is even more structurally entrenched. Approximately 80% of global photovoltaic modules rely on EVA encapsulants, reflecting the material’s combination of high light transmittance exceeding 91%, strong adhesion to glass, and long-term durability under UV exposure and thermal cycling. Beyond solar, EVA’s inherent flexibility and toughness are supporting its integration into bio-based composites, lamination films, and nonwoven hygiene adhesives, where resilience and controlled softness are required. At the same time, leading producers are advancing bio-based EVA formulations and compostable tackifier systems to enable recyclable, low-VOC adhesive architectures.

The EVA adhesives sector experienced significant investment and innovation cycles, spanning expansions in resin capacity, bio-based copolymer introductions, and government-backed regional projects. The shift toward high-VA EVA formulations—especially for solar encapsulation, sustainable packaging, and construction adhesives—has triggered multiple capacity expansions and technology upgrades across North America, Asia, and Europe.

In May 2025, a leading U.S.-based specialty materials firm completed a debottlenecking project at its Gulf Coast plant, expanding output of high-Vinyl Acetate EVA resins to address the surging demand from solar energy and industrial hot melt adhesives sectors. Similarly, in April 2025, an Asian petrochemical giant introduced bio-compatible EVA copolymers specifically designed for compostable flexible packaging, combining enhanced low-temperature adhesion with compatibility to bio-based tackifiers, a major leap toward circular packaging solutions.

Europe is witnessing a parallel sustainability surge — in February 2025, a leading European chemical producer announced a $50 million investment to expand VAE (Vinyl Acetate Ethylene) emulsions capacity, strengthening the supply chain for low-VOC construction adhesives and waterborne coatings. Meanwhile, in December 2024, a top Chinese manufacturer commissioned a new high-pressure autoclave reactor boosting EVA production by 65,000 metric tons annually, directly benefiting the footwear and adhesive feedstock sectors in Asia-Pacific.

Global integration trends have also accelerated. In September 2024, a major adhesives multinational acquired a UK-based hot melt specialist to strengthen its portfolio of high-temperature EVA adhesives used in automotive interiors and filtration assemblies. On the materials front, August 2024 saw the introduction of a new Evatane EVA grade by Arkema, engineered with high VA content and a tailored Melt Index for food-grade multilayer extrusion coatings.

Complementing these developments, July 2024 marked a U.S. producer’s successful completion of an energy-efficiency upgrade at its Texas EVA facility, reducing carbon intensity per ton by nearly 5% while modestly improving output. In June 2024, academic researchers published breakthrough findings on curing agents improving UV and damp-heat resistance in EVA PV encapsulants — enhancing solar module lifespan and weatherability.

As the packaging industry moves toward sustainable, high-throughput production systems, EVA adhesive manufacturers are pioneering low-temperature formulations to optimize performance, energy efficiency, and substrate compatibility. Conventional EVA hot-melts, which require application temperatures exceeding 150°C, are being replaced by advanced EVA-based systems designed for operation at just 110–120°C, significantly reducing both thermal stress and operational costs.

Studies show that using low-temperature EVA hot-melts can reduce energy consumption during operation by as much as 68% per hour compared to conventional systems. The shift directly lowers factory power usage and supports corporate carbon-reduction goals, aligning with ISO 14001 sustainability frameworks.

Modern packaging materials—such as thin polyethylene films, foamed laminates, and bioplastics—are often sensitive to deformation under high heat. Low-temperature EVA adhesives ensure robust adhesion at application temperatures as low as 90–130°C, enabling safe and efficient sealing of temperature-vulnerable substrates without compromising bond integrity.

Formulators are enhancing the thermal stability and oxidative resistance of these adhesives to minimize charring, nozzle clogging, and downtime in continuous high-speed packaging lines. By maintaining stable viscosity and eliminating gel formation, modern low-temp EVA adhesives improve equipment lifespan and ensure consistent adhesive flow, particularly in automated production environments.

The rising pressure from global sustainability mandates, including EU Green Deal, US EPA VOC standards, and brand owner circularity goals, is propelling EVA adhesive manufacturers toward bio-based, recyclable, and PFAS-free formulations. These new-generation adhesives integrate renewable feedstocks and enable compatibility with recycling processes, positioning EVA as a core material for circular packaging systems.

Major producers are commercializing USDA Biopreferred-certified bio-based EVA adhesives, boasting renewable carbon content above 50%. These adhesives are microplastic-free, PFAS-free, and meet EU Packaging and Packaging Waste Directive (PPWD) requirements—making them ideal for use in food packaging and consumer goods applications that demand both performance and sustainability.

Researchers are advancing thermo-reversible EVA-based adhesives that can transition from a strong adhesive to a flowable material at temperatures above 160°C, allowing packaging materials (e.g., PET or laminated paper) to be easily separated and recovered during industrial recycling. The innovation supports Design for Recycling (DfR) objectives and facilitates closed-loop material reuse.

A major innovation in sustainable EVA adhesive production is the use of upcycled waxes from mixed polyolefin waste streams. These waxes—produced with yields up to 92% recovery—can replace up to 30% of the petroleum-based wax content in traditional EVA hot melts, enhancing sustainability while maintaining tack, viscosity control, and mechanical strength.

The explosive growth of e-commerce logistics and automated carton sealing systems has created a multi-billion-dollar opportunity for high-performance EVA adhesives capable of delivering speed, versatility, and environmental resistance across complex supply chains.

With e-commerce shipments traversing varied climatic conditions—from cold-chain logistics to hot, humid storage facilities—EVA hot melts are being engineered with enhanced cold resistance and heat stability, ensuring tamper-proof sealing even in extreme temperature fluctuations. These adhesives deliver reliable bonding on corrugated and laminated substrates, maintaining packaging integrity from warehouse to last-mile delivery.

E-commerce fulfillment centers demand adhesives that support high-speed label and carton application—often exceeding 600 boxes per minute. The fast-setting nature of EVA adhesives ensures instant bond strength, eliminating downtime and enabling continuous packaging throughput critical to just-in-time logistics systems.

Modern EVA and metallocene-modified EVA (mEVA) hot melts provide superior wetting and adhesion to recycled corrugated board, coated paper, and polymer-laminated films. The adaptability positions EVA adhesives as the go-to solution for automated case sealing, box forming, and specialty carton applications in e-commerce operations.

The surge in automated furniture and engineered wood production is fueling demand for industrial-grade EVA adhesives that deliver precision bonding, high strength, and aesthetic performance across laminated and coated wood substrates.

In edge banding and panel lamination, EVA hot melt adhesives provide rapid setting (within 2–5 minutes), essential for high-speed robotic assembly lines. Their consistent viscosity and open time ensure seamless operation in automated systems, enhancing throughput while minimizing adhesive waste and rework costs.

As mass timber and ready-to-assemble (RTA) furniture gain traction, EVA adhesives are being optimized to achieve strong, flexible bonds on HPL, MDF, particleboard, and veneer. These adhesives provide clean, aesthetic bond lines with excellent heat and moisture resistance, crucial for long-term furniture durability.

Furniture producers adopting eco-label and VOC-free compliance standards are increasingly selecting EVA hot melts that are solvent-free, formaldehyde-free, and suitable for LEED-certified building materials, aligning with global sustainability trends in home and commercial interiors.

The competitive environment of the Global EVA Adhesives Market is dominated by highly integrated resin producers and specialty adhesive formulators leveraging acetyl chemistry expertise, polymer blending innovations, and regional expansion strategies. Industry leaders such as Celanese Corporation, ExxonMobil Chemical, LyondellBasell, and Arkema (Bostik & Vinavil) are focusing on capacity scaling, circular material development, and hot melt formulation performance to meet the evolving demands of packaging, solar, footwear, and construction industries.

Celanese Corporation maintains a commanding presence across the acetyls and derivatives value chain, producing Ateva® EVA polymers with up to 42% Vinyl Acetate content and melt indices exceeding 1000 g/10 min for precision bonding and extrusion applications. The company’s 2023 expansion at Nanjing, China, introduced a third VAE reactor with 65,000 metric tons/year capacity to serve the fast-growing Asia-Pacific adhesives and redispersible powders markets. Celanese’s Ateva® ExtruBond™ grades deliver enhanced line speed and adhesion for flexible packaging, while Vitaldose® EVA enables pharmaceutical-grade controlled-release systems—showcasing the company’s innovation beyond industrial hot melts.

ExxonMobil Chemical combines its upstream ethylene and tackifier production capabilities with its Escorene™ Ultra EVA copolymers, widely used in case and carton sealing hot melt adhesives. The synergy between Escorez™ tackifying resins and EVA polymers allows formulators to achieve up to 90% polymer loading with low odor, high clarity, and superior flexibility. The company’s EVA 5727.12 grade (26.7% VA) balances toughness with melt flow performance ideal for wax blends and sealants. ExxonMobil’s Prowaxx™ food-contact-compliant waxes (FDA 21 CFR 175.105) reinforce its strong foothold in packaging and hygiene adhesives.

LyondellBasell supplies its Ultrathene® EVA copolymer range, tailored for films, adhesives, and compounding applications requiring low heat seal initiation temperatures and superior flexibility. The company’s Icorene N1012 (27.5% VA) is particularly suited for hot melt adhesives and masterbatch compounding, while its advanced high-pressure polymerization process enables the fine-tuning of melt strength and comonomer distribution. With a strong manufacturing base across North America and Europe, LyondellBasell serves both industrial adhesive producers and film converters with EVA products engineered for mechanical consistency and high processing efficiency.

Arkema Group, through its Bostik and Vinavil divisions, leads the transformation of EVA-based adhesives into smart, sustainable systems. Its Evatane® EVA line spans VA contents between 18–42%, offering formulation flexibility for industrial hot melts, sealing, and disposable hygiene adhesives. The Bostik brand focuses on smart bonding solutions for transportation, packaging, and aerospace, while Vinavil contributes vinyl-based dispersion polymers for waterborne coatings. Arkema’s product innovation strongly aligns with the bio-circular economy, emphasizing bio-based raw materials, reduced VOC content, and regional growth in Asia-Pacific, which rose from 18% to 32% of group sales (2005–2023).

EVA Adhesives Market Report Scope

EVA Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.5 Billion

|

|

Market Size (2034)

|

$47.3 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Technology (Hot Melt Adhesives, Water-Borne, Solvent-Borne, Reactive EVA), By End-User Industry (Packaging, Woodworking & Joinery, Footwear & Leather, Bookbinding & Graphic Arts, Construction, Automotive Interiors), By Vinyl Acetate (VA) Content (Below 18% VA, 18% VA, 28% VA, Above 28% VA

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Jowat SE, 3M Company, Arkema Group (Bostik), Dow Inc, Sika AG, Tex Year Industries Inc. , Wacker Chemie AG, Avery Dennison Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Technology / Formulation

- Hot Melt Adhesives

- Water-Borne

- Solvent-Borne

- Reactive EVA

By End-User Industry

- Packaging

- Woodworking & Joinery

- Footwear & Leather

- Bookbinding & Graphic Arts

- Construction

- Automotive Interiors

By Vinyl Acetate (VA) Content

- Below 18% VA

- 18% VA

- 28% VA

- Above 28% VA

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in EVA Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Jowat SE

- 3M Company

- Arkema Group (Bostik)

- Dow Inc

- Sika AG

- Tex Year Industries Inc.

- Wacker Chemie AG

- Avery Dennison Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global EVA Adhesives Market with a focus on performance-critical use cases in packaging, solar encapsulation, footwear, woodworking, and construction; it delivers analysis reviews on resin architecture, VA-content optimization, rheology and set-time control, thermal/oxidative stability, and end-of-line productivity. It highlights breakthroughs in low-temperature hot-melt operation, high-VA copolymer grades for flexible laminates, recyclable/bio-based blends for circular packaging, and PV encapsulation durability—translating lab metrics (MFI, ring-and-ball softening point, peel/tack/shear, haze/transmittance) into plant-ready specifications and cost-in-use playbooks. With vendor benchmarking, route-to-market dynamics, regulatory trajectories (VOC, food-contact, PFAS-free), and risk dashboards for feedstock and energy intensity, this report is an essential resource for R&D, procurement, and operations leaders seeking faster line speeds, lower temperatures, and compliant adhesive systems at scale.

Scope Highlights

Segmentation:

- By Technology / Formulation: Hot Melt Adhesives; Water-Borne; Solvent-Borne; Reactive EVA.

- By End-User Industry: Packaging; Woodworking & Joinery; Footwear & Leather; Bookbinding & Graphic Arts; Construction; Automotive Interiors.

- By Vinyl Acetate (VA) Content: Below 18% VA; 18% VA; 28% VA; Above 28% VA.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company profiles/analyses covering technology focus, strategic moves, certifications, and sustainability positioning.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.