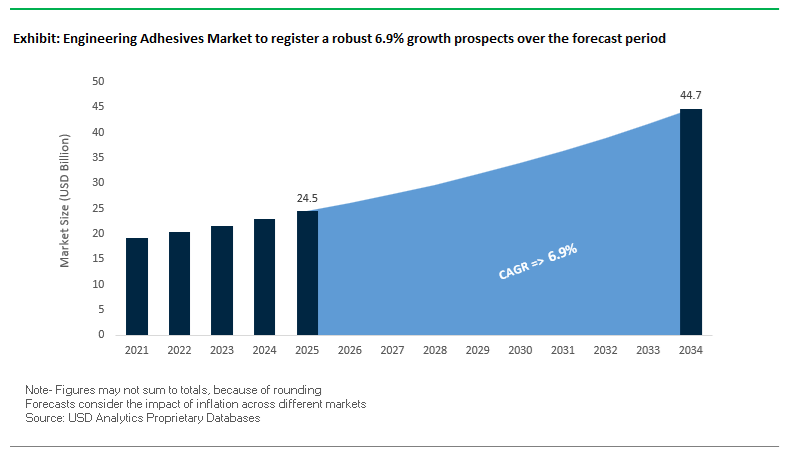

The Global Engineering Adhesives Market is projected to expand from USD 24.5 billion in 2025 to USD 44.7 billion by 2034, advancing at a CAGR of 6.9%, as structural bonding becomes a foundational element of modern engineering design rather than a secondary joining step. Across automotive, aerospace, construction, and electronics manufacturing, engineering adhesives are increasingly specified to replace mechanical fasteners and welding in order to support lightweighting strategies, multi-material integration, thermal management, and modular assembly architectures. Epoxies, polyurethanes, methacrylates, and UV-curable acrylics are embedded in OEM qualification frameworks because they enable consistent load transfer, corrosion isolation, and design freedom that traditional joining methods cannot achieve in high-performance applications.

From a performance and materials standpoint, market growth is anchored in the ability of structural adhesives to meet stringent mechanical, thermal, and durability requirements under real-world operating conditions. Automotive-grade epoxy adhesives routinely specified in Body-in-White (BiW) platforms deliver shear strength in the range of 18–35 MPa, supporting crash energy management and long-term corrosion resistance across mixed-metal joints. In parallel, two-component polyurethane adhesives with elongation at fracture exceeding 50% are increasingly adopted in construction and transport structures where dynamic loads, vibration, and differential thermal expansion must be absorbed without bond failure. Aerospace applications further elevate performance thresholds, with structural adhesive films requiring controlled curing cycles at 121°C or 177°C to meet fatigue, temperature, and environmental resistance criteria mandated for composite airframe bonding.

Regulatory pressure and manufacturing efficiency are reinforcing these adoption trends. OEMs are actively transitioning toward low-VOC and low-hazard chemistries, exemplified by polyurethane adhesive platforms achieving below 0.1% free monomeric diisocyanate content, aligning with REACH and occupational exposure limits while preserving structural performance. At the same time, high-throughput manufacturing environments—particularly in electronics, optics, and medical devices—are accelerating the use of UV-curable acrylates and epoxies capable of curing within seconds, materially improving line speed and assembly precision.

In September 2025, Sika AG expanded its Sikaflex® and SikaTack® polyurethane adhesive range incorporating Purform® technology, achieving ultra-low (<0.1%) free monomeric diisocyanate content. This advancement simplifies regulatory compliance under EU REACH legislation and enhances worker safety, particularly in automotive glazing and industrial assembly lines. The innovation aligns with global sustainability and safety goals, reflecting how next-generation adhesives are evolving toward environmentally responsible chemistry without compromising mechanical durability.

In July 2025, Arkema announced the construction of a high-performance Rilsan® Clear polyamide unit in Singapore, marking a major step in scaling bio-based transparent polymers derived from castor oil. These materials are critical for engineering adhesives used in lightweight composites and structural assemblies, offering both clarity and strength while reducing carbon footprints. Around the same period, Parker Hannifin’s LORD division expanded its CoolTherm® series, notably the SC-2000 RW (reworkable) and UR-2000 (urethane) adhesives—targeting EV battery systems with high thermal conductivity and vibration control, ensuring optimal battery safety and serviceability.

By October 2024, 3M Company introduced a new generation of Scotch-Weld™ Structural Adhesive Films designed for primary and secondary aerospace structures, optimized for both 250°F and 350°F cure cycles. This product line supports faster composite fabrication and enhanced bonding integrity, reinforcing 3M’s dominance in aerospace adhesive solutions. Meanwhile, a 2025 industry report underscored the growing traction of bio-based adhesives, citing that modern formulations reduce CO₂-equivalent emissions by up to 60%, expanding their reach into construction, paper, and packaging applications traditionally reliant on petrochemical alternatives.

Further emphasizing military-grade innovation, a late-2024 partnership between a defense OEM and Huntsman Corporation resulted in the co-development of high-toughness methacrylate adhesives (MMAs) engineered to bond dissimilar materials for land-based defense vehicles. These formulations exhibit fast curing and exceptional shock resistance, meeting the demands of next-generation armored systems. In the automotive manufacturing sector (early 2025), a leading adhesive manufacturer launched snap-cure hybrid PU adhesives, capable of drastically reducing cycle times while maintaining superior creep and thermal resistance, improving productivity across global assembly operations.

Complementing these trends, Master Bond’s mid-2025 release of a low-viscosity, high-elongation epoxy designed for large-area potting and encapsulation expanded the range of thermal-resistant materials suitable for electronics and optical applications. With an operational temperature range of −60°F to +250°F, this development addressed the miniaturization and durability challenges facing next-gen electronic devices. Further, the late-2024 investment in digital manufacturing centers by a major adhesive supplier reflected the growing integration of automation, robotics, and precision dispensing technologies—signaling the onset of a new era in Industry 4.0 adhesive applications.

The shift toward wide-bandgap semiconductors (WBG) such as Silicon Carbide (SiC) and Gallium Nitride (GaN) is fundamentally transforming the requirements for engineering adhesives in power electronics, 5G infrastructure, and EV inverters. These materials, operating at higher voltages and temperatures, demand thermally conductive yet electrically insulating adhesives to ensure efficient heat dissipation without compromising safety.

High-performance thermally conductive adhesives (TCAs) are designed to support the extreme heat flux generated by SiC (340–490 W/m·K) and GaN (110–270 W/m·K) substrates. Traditional thermal interface materials fail to provide adequate conductivity or adhesion strength, leading to overheating and premature device failure. The newest generation of silicone-based TCAs—such as the recently introduced 2K silicone adhesives—achieve thermal conductivities of 1.5 W/m·K, tested per DIN EN ISO 22007-2:2015-12, while retaining electrical insulation and mechanical stability between −60 °C to 200 °C, making them ideal for EV power modules and inverter packaging.

Additionally, the market is witnessing a strong transition toward structural thermal adhesives, combining high mechanical modulus (up to 60 N/mm²) with a Shore A hardness of 70. These hybrid materials are replacing metal fasteners in high-reliability assemblies, streamlining EV inverter production while enhancing vibration resistance and operational reliability. The integration of such dual-function TCAs aligns with the growing emphasis on lightweight, thermally optimized EV powertrain architectures.

The increasing complexity and miniaturization of electronic assemblies in sectors like automotive electronics, flexible displays, and sensor modules are accelerating the adoption of low-temperature and ultrafast-curing adhesives to protect heat-sensitive substrates. These innovations directly enhance manufacturing efficiency and component reliability in high-throughput production environments.

Advanced UV-curing acrylic adhesives achieve complete cure in under 2 seconds, enabling immediate downstream processing and significantly improving line throughput for display bonding and PCB staking. Manufacturers are further innovating with dual-cure hybrid systems, combining UV and moisture-curing mechanisms to overcome shadow zone limitations in complex geometries—ensuring total crosslinking even in non-irradiated areas, a crucial feature for structural bonding in dense or opaque electronics assemblies.

Cutting-edge induction curing technologies are also revolutionizing the bonding process for structural adhesives. By embedding Curie particles (CP)—metallic fillers with controlled magnetic transition temperatures (e.g., 110 °C)—adhesives can be cured rapidly and uniformly under localized induction heating, achieving bond strengths equivalent to high-temperature oven processes. The innovation reduces energy consumption and material stress, unlocking new applications for automotive lightweighting and composite bonding.

The semiconductor industry’s transition to Heterogeneous Integration (HI) and chiplet-based architectures presents a lucrative, high-precision opportunity for engineering adhesives in 3D System-in-Package (SiP) and Multi-Chip Module (MCM) applications. These advanced systems require ultra-thin, uniform bond lines, superior thermal stability, and minimal contamination for high-reliability microelectronic assemblies.

The industry is rapidly adopting Die Attach Films (DAFs) as replacements for traditional paste adhesives, providing exceptional bond-line control at 5–10 μm thickness while eliminating voiding issues and ensuring uniform pressure distribution during curing. Their superior mechanical integrity and clean processing are essential for fine-pitch chip stacking in high-density computing modules.

In addition, micro-dam adhesive technologies are being used to define flow boundaries during underfill dispensing, achieving line widths under 100 μm with high aspect ratios (>5:1). These precision-engineered materials prevent overflow and maintain interconnect reliability in AI and high-performance computing (HPC) applications. Additionally, the growing use of temporary bonding adhesives—engineered to withstand processing temperatures up to 350 °C and release cleanly after UV exposure (low peel strength <10 ppi)—is facilitating wafer thinning and chip-to-wafer hybrid bonding for 3D-IC manufacturing.

The combination of DAF precision, micro-dam control, and temporary bonding stability positions adhesive materials as foundational enablers of the semiconductor packaging revolution.

The global electrification wave is driving an unprecedented surge in engineering adhesive demand across battery pack assembly, cell-to-module bonding, and structural integration. As governments and automakers commit to net-zero targets, investments in battery gigafactories are expanding rapidly—fueling the need for high-performance, automation-ready adhesive systems.

Global lithium-ion battery capacity is projected to exceed 5,456 TWh by 2036, underpinning exponential growth in adhesive consumption for EV module manufacturing and energy storage systems (ESS). Engineering adhesives in the domain serve multifunctional roles—providing structural reinforcement, sealing, and thermal control.

In battery enclosures, toughened epoxy and acrylic structural adhesives are widely employed for bonding dissimilar substrates such as aluminum, steel, and CFRP composites. These adhesives not only deliver high fatigue resistance and crash durability, but also mitigate Noise, Vibration, and Harshness (NVH) for improved passenger comfort. Further, flame-retardant silyl-modified and non-silicone sealants are gaining traction for pack case sealing and thermal barrier applications, offering compliance with UL 94 V-0 and other EV safety standards.

The shift toward cell-to-chassis (CTC) and cell-to-pack (CTP) designs further amplifies adhesive demand, as bonding must ensure load-bearing structural strength while enabling thermal runaway protection. The integration of adhesives that combine flame retardancy, electrical insulation, and mechanical toughness is becoming a defining factor in the safety and efficiency of next-generation EV battery systems.

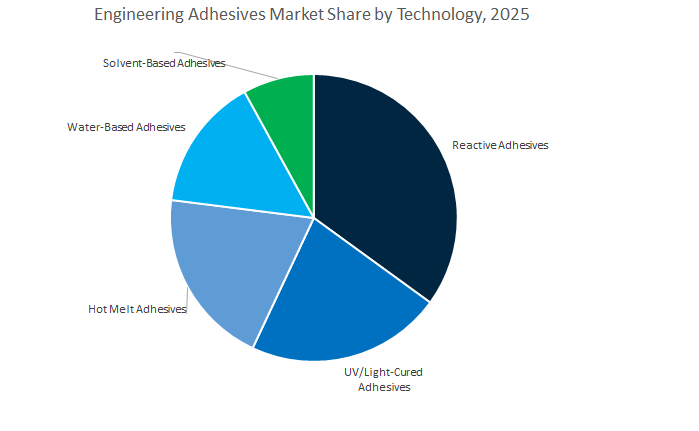

Engineering Adhesives Market Share Insights, 2025-2034

Reactive adhesives remain the cornerstone of the engineering adhesives market, accounting for the largest share due to their unparalleled mechanical performance, chemical resistance, and versatility. These adhesives cure through chemical reactions—such as moisture, heat, or catalyst activation—forming strong, permanent bonds capable of withstanding high mechanical stress, vibration, and environmental exposure. Their dominance is rooted in wide-ranging adoption across automotive, aerospace, construction, and industrial equipment manufacturing, where structural bonding and high durability are paramount. Epoxy, polyurethane, and acrylic-based reactive adhesives are particularly valued in applications like composite bonding, metal assembly, and structural reinforcement. In addition, two-component (2K) formulations are favored for precision-engineered systems, offering controlled curing and superior adhesion to dissimilar substrates. The shift toward lightweight and multi-material joining in EVs and aircraft is reinforcing the demand for reactive systems, which offer better fatigue resistance and corrosion protection compared to mechanical fasteners. As global manufacturers emphasize sustainability, low-VOC and solvent-free reactive formulations are gaining prominence, enabling compliance with environmental standards while maintaining performance excellence.

The UV/light-cured adhesives segment is witnessing rapid growth, fueled by its ability to deliver instant curing, precision application, and high throughput—qualities essential for electronics, medical devices, and optical component manufacturing. These adhesives polymerize within seconds when exposed to UV or LED light, significantly improving production efficiency and reducing energy consumption. Their excellent optical clarity, low shrinkage, and compatibility with transparent substrates make them indispensable in display bonding, lens assembly, and medical device encapsulation. The surge in LED curing technology—offering lower heat generation and greater flexibility compared to traditional mercury lamps—is accelerating adoption across cleanroom environments. Additionally, the growing miniaturization of electronic components in smartphones, wearables, and semiconductors has intensified the need for UV adhesives that provide fine-line precision and thermal control. As sustainability and automation trends advance, UV/light-cured systems are set to capture a greater share of the engineering adhesives landscape due to their eco-efficient curing and superior productivity advantages.

While reactive systems dominate performance-driven applications, hot melt and water-based adhesives are emerging as key enablers of cost-effective and sustainable bonding solutions. Hot melt adhesives, including reactive PUR variants, offer rapid bond strength, short processing times, and compatibility with automation, making them ideal for automotive interiors, woodworking, and electronic encapsulation. Their ability to combine flexibility with mechanical robustness underpins their growing use in modern lightweight assemblies. Meanwhile, water-based adhesives continue to replace solvent-based systems, driven by stringent environmental regulations (e.g., REACH, EPA) and corporate sustainability goals. They are particularly strong in construction, packaging, and general industrial assembly, providing good adhesion to porous substrates with minimal VOC emissions. These formulations align with global trends toward greener manufacturing and safer work environments, while advances in emulsion polymer chemistry continue to improve water-based adhesive performance.

The automotive and transportation sector stands as the dominant end-user in the global engineering adhesives industry, commanding nearly one-third of total demand. Adhesives are critical to lightweight vehicle manufacturing, enabling the replacement of traditional welding and mechanical fastening with advanced bonding solutions that join metals, plastics, and composites without compromising strength or durability. Engineering adhesives are used in structural body bonding, windshield assembly, interior trim, and sealing of electronic modules, contributing to improved fuel efficiency and crash safety. The rise of Electric Vehicles (EVs) has further expanded adhesive usage for battery module assembly, thermal interface bonding, and EMI shielding, where performance, heat resistance, and vibration damping are crucial. Automotive OEMs increasingly favor reactive epoxy, polyurethane, and acrylic systems for structural integrity and hot-melt PUR formulations for fast cycle times in mass production. As sustainability becomes central to automotive manufacturing, adhesives designed for recyclability, low-VOC content, and lightweight material compatibility are defining the next phase of innovation in the transportation sector.

The electronics and electrical industry is one of the fastest-growing end-use sectors for engineering adhesives, supported by the global boom in consumer electronics, semiconductors, and smart devices. These adhesives play an indispensable role in thermal management, miniaturization, and protective encapsulation, ensuring performance and reliability in compact assemblies. Applications include die attach, conformal coating, underfilling, and component sealing in printed circuit boards (PCBs), displays, and sensors. Electrically and thermally conductive adhesives are replacing traditional soldering techniques, especially in sensitive or miniaturized electronics where heat exposure must be minimized. Additionally, the transition to 5G communication systems and IoT-connected devices has created new adhesive performance demands—requiring low outgassing, electromagnetic shielding, and precise dispensing. The growing integration of adhesives in flexible electronics, EV power modules, and wearables highlights their strategic role in enabling the next generation of high-performance electronic systems.

Building and construction applications remain a stable and high-volume driver, relying on engineering adhesives for structural glazing, curtain wall bonding, flooring, and waterproofing. The push for energy-efficient and green buildings is spurring adoption of low-VOC and moisture-curing reactive systems capable of handling heavy mechanical loads and thermal expansion. Similarly, general industrial assembly represents a broad segment encompassing machinery, appliances, and fabricated products, where adhesives provide vibration damping, chemical resistance, and aesthetic joining benefits. Industrial manufacturers are increasingly shifting from mechanical fastening to adhesive bonding to improve production efficiency, design flexibility, and noise reduction. Across both sectors, hybrid polymer systems such as silyl-modified polyurethanes (SMPs) are gaining popularity for combining elasticity with structural integrity. The continued growth in global infrastructure projects, renewable energy installations, and modular industrial design ensures steady adhesive consumption across construction and general manufacturing markets.

The engineering adhesives market features a blend of global chemical giants and specialized innovators that dominate through R&D excellence, sustainable formulation strategies, and application-specific expertise. Key players — including 3M, Henkel, Sika, Huntsman, Arkema, and Parker Hannifin (LORD) — are setting new standards for structural bonding performance, bio-based polymer innovation, and low-emission polyurethane systems across aerospace, automotive, and electronics markets.

3M remains a global benchmark in engineering adhesives and structural films, offering solutions through its Scotch-Weld™ brand for aerospace, composites, and industrial bonding. Its latest high-performance adhesive films support 250°F and 350°F cure cycles, catering to advanced carbon fiber manufacturing. With deep R&D integration across sealants, tapes, and thermal management materials, 3M delivers superior performance in lightweight structures, electric components, and critical mechanical joints.

Henkel dominates across epoxy, polyurethane, and acrylic adhesives, marketed through Loctite and Technomelt. Its engineering adhesive solutions enable lightweighting and structural integrity in automotive and aerospace assembly lines, while its low-VOC polyurethane technologies contribute to environmentally compliant production. The company is further advancing automated dispensing systems for precision bonding, aligning with Industry 4.0 integration in high-speed assembly and maintenance operations.

Sika AG is at the forefront of polyurethane innovation, leveraging its Purform® technology to develop low-free monomer PU adhesives for enhanced safety and compliance. Its SikaPower® and Sikaflex® product lines dominate automotive glazing, wind turbine assembly, and structural construction sectors. Sika’s strong foothold in two-component epoxy systems (Sikadur®) also ensures performance under extreme environmental and mechanical conditions, cementing its global leadership in construction-grade adhesives.

Huntsman continues to expand its Araldite® brand portfolio, offering methacrylate and epoxy-based adhesives that provide exceptional toughness and heat resistance for aerospace, rail, and wind energy applications. Its custom MMA systems are tailored for defense and industrial composites, excelling in vibration and impact resistance. The company’s focus on amine-cured epoxy technology further supports lightweight, high-performance composite assembly.

Arkema has made significant investments in bio-based high-performance polymers, notably through its Rilsan®, Pebax®, and Platamid® product families. Its Singapore expansion (July 2025) enhances global supply of renewable polyamides for adhesive films and flexible bonding applications. Additionally, Arkema’s expertise in UV-curable resins and 3D printing materials underscores its leadership in next-generation bio-circular adhesive technologies for automotive and industrial engineering.

Parker Hannifin’s LORD Corporation specializes in thermal management and structural bonding solutions for electric vehicles and aerospace applications. The CoolTherm® adhesive family, including SC-2000 RW and UR-2000, delivers reworkable, thermally conductive properties essential for battery modules and power systems. By integrating adhesives, vibration damping, and shock absorption technologies, Parker Hannifin plays a pivotal role in enhancing EV performance, safety, and sustainability.

The United States remains a powerhouse in the global engineering adhesives market, leading in both technological innovation and regulatory transformation. The introduction of 3M’s next-generation water-based pressure-sensitive adhesives (PSA) in 2024 marks a major leap in sustainability and compliance, reflecting the country’s strong focus on eco-friendly adhesive formulations. The adhesives are designed to meet evolving Environmental, Health, and Safety (EHS) standards across consumer goods and industrial applications. Moreover, the General Services Administration (GSA) 2024 P100 Facilities Standards continues to influence the adoption of low-VOC structural adhesives across federal projects, pushing the market toward greener, performance-oriented bonding technologies.

Simultaneously, H.B. Fuller’s investment in aerospace adhesives represents a strategic pivot towards carbon reduction in aircraft manufacturing. Its 2024 product launch, featuring environmentally friendly aerospace-grade adhesives, underscores the shift to lightweight, high-strength, and sustainable bonding systems. With the U.S. government incentivizing clean manufacturing practices and federal building standards prioritizing green construction materials, the domestic market is witnessing robust demand for bio-based, reactive, and polyurethane adhesives. The convergence of sustainability mandates, federal procurement policies, and industrial innovation positions the United States as a global benchmark for sustainable and high-performance engineering adhesive technologies.

Germany continues to dominate the European engineering adhesives industry, driven by technological sophistication and strategic investment. Henkel AG & Co. KGaA’s €20 million expansion project in Bopfingen, announced in October 2024, highlights Germany’s commitment to scaling production of hot-melt and polyurethane adhesives for critical sectors such as packaging, woodworking, and furniture manufacturing. The investment reflects a broader European shift toward localized production of energy-efficient, compliant adhesive systems.

In parallel, Jowat SE’s expansion of its GROW bio-based hot melt adhesive technology marks a pivotal innovation trend. By incorporating renewable raw materials, Jowat’s adhesives extend into textile and product assembly sectors, underscoring Germany’s leadership in bio-based adhesive development. Regulatory frameworks such as REACH are also exerting significant influence, compelling manufacturers to phase out solvent-based formulations and invest in high-performance, low-emission reactive adhesives. Germany’s R&D ecosystem, supported by academic-industry collaboration, remains critical to the global supply chain of advanced polyurethane, epoxy, and hot melt engineering adhesives that align with sustainability and efficiency standards.

China represents the largest and fastest-growing market for engineering adhesives, propelled by its dominance in the electric vehicle (EV) and electronics manufacturing sectors. The nation’s adhesive producers are innovating rapidly, developing high-thermal conductivity and electrically insulating thermal adhesives for EV battery pack assembly. The specialized formulations ensure efficient heat management and structural integrity in high-performance battery systems, aligning with China’s EV leadership goals.

Supporting The growth, Henkel’s Adhesive Technologies Inspiration Center in Shanghai has become a regional hub for R&D and application testing, particularly for electronics bonding, EV thermal management, and high-speed assembly solutions. Meanwhile, the Chinese government’s push for green building standards is accelerating the use of low-VOC polyurethane and acrylic adhesives, replacing traditional solvent-based formulations. The transition complements the country’s broader carbon reduction targets under its 2060 carbon neutrality roadmap. With substantial infrastructure investment and domestic manufacturing leadership, China’s engineering adhesives industry continues to set global benchmarks in industrial-scale production and sustainable bonding technologies.

India’s engineering adhesives market is rapidly evolving, driven by strong industrial policy support and global partnerships. In August 2025, Henkel Adhesive Technologies collaborated with domestic partners to support the country’s first mid-haul re-powered electric truck operations, utilizing advanced structural adhesives for component bonding and frame integration in heavy-duty electric vehicles. The milestone showcases India’s growing expertise in adhesive solutions for EV assembly, industrial manufacturing, and mobility electrification.

Simultaneously, Henkel’s planned adhesive materials manufacturing plant in Maharashtra underscores rising foreign investment in India’s industrial and automotive sectors. The country’s ‘Make in India’ initiative continues to boost domestic production of electronics, automotive parts, and infrastructure components, directly fueling demand for high-strength, thermally stable engineering adhesives and coatings. As global manufacturers localize production, India’s combination of policy incentives, cost-effective manufacturing, and expanding R&D capabilities positions it as a key growth market for reactive and structural adhesive systems across automotive, electronics, and general industrial applications.

France’s engineering adhesives industry benefits immensely from its position as a leading aerospace manufacturing hub, home to global leaders such as Airbus. The nation’s R&D efforts are concentrated on aerospace structural adhesives capable of bonding advanced composites and lightweight materials—critical for aircraft fuel efficiency and performance optimization. Driven by the European Union Aviation Safety Agency (EASA) and regional sustainability mandates, France continues to prioritize high-performance epoxy and polyurethane adhesives with improved heat resistance, strength, and chemical stability.

Arkema Group’s ongoing strategic expansion, particularly through its Bostik and Sartomer divisions, underscores the country’s momentum in specialty and high-temperature engineering adhesives. Arkema’s product innovation caters to high-performance industries including aerospace, electronics, and automotive manufacturing, aligning with France’s national agenda for decarbonized and technology-driven industrial production. As sustainable material integration grows in European aerospace and infrastructure, France remains at the forefront of advanced adhesive engineering and composite bonding solutions.

Japan’s engineering adhesives market is characterized by unmatched innovation in electronics bonding and precision manufacturing. Domestic R&D has heavily focused on developing fast-curing, high-precision adhesives such as Liquid Optically Clear Adhesives (LOCA) used in display assemblies, touch panels, and optical sensors. The materials meet the miniaturization and high-speed assembly demands of the global electronics and semiconductor supply chains, where precision and clarity are paramount.

In parallel, Japan’s automotive sector—renowned for technological sophistication—is continuously advancing the use of methyl methacrylate (MMA) and two-component epoxy adhesives in structural bonding. The adhesives provide superior crash resistance and durability for next-generation electric and hybrid vehicles. With a focus on sustainability, miniaturization, and performance, Japan remains a cornerstone in the Asia-Pacific engineering adhesives landscape, driving global adoption of smart bonding materials for automotive and electronic applications.

Engineering Adhesives Market Report Scope

Engineering Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.5 Billion

|

|

Market Size (2034)

|

$44.7 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Resin Type (Epoxy Adhesives, Polyurethane Adhesives, Acrylic Adhesives, Cyanoacrylate Adhesives, Silicone Adhesives, Anaerobic Adhesives, Reactive Hot Melts), By Technology (Reactive Adhesives, Solvent-Based Adhesives, Water-Based Adhesives, Hot Melt Adhesives, UV/Light-Cured Adhesives), By End-Use Industry (Automotive & Transportation, Aerospace & Defense, Electronics & Electrical, Building & Construction, Wind Energy, Medical Devices, General Industrial Assembly

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Sika AG, Arkema Group, Dow Inc., Huntsman Corporation, Wacker Chemie AG, Avery Dennison Corporation, RPM International Inc., DuPont de Nemours, Inc., Jowat SE, Pidilite Industries Ltd., DELO Industrial Adhesives, Ashland Global Holdings Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin/Chemistry Type

- Epoxy Adhesives

- Polyurethane Adhesives

- Acrylic Adhesives

- Cyanoacrylate Adhesives

- Silicone Adhesives

- Anaerobic Adhesives

- Reactive Hot Melts

By Technology

- Reactive Adhesives

- Solvent-Based Adhesives

- Water-Based Adhesives

- Hot Melt Adhesives

- UV/Light-Cured Adhesives

By End-Use Industry

- Automotive & Transportation

- Aerospace & Defense

- Electronics & Electrical

- Building & Construction

- Wind Energy

- Medical Devices

- General Industrial Assembly

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Sika AG

- Arkema Group

- Dow Inc.

- Huntsman Corporation

- Wacker Chemie AG

- Avery Dennison Corporation

- RPM International Inc.

- DuPont de Nemours, Inc.

- Jowat SE

- Pidilite Industries Ltd.

- DELO Industrial Adhesives

- Ashland Global Holdings Inc.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Engineering Adhesives Market with executive-grade analysis reviews of demand drivers, specification trends, and regulatory inflection points across mobility, aerospace, construction, electronics, wind energy, medical devices, and general industrial assembly. It highlights commercialization breakthroughs in low-monomer polyurethane platforms, aerospace-grade structural films, thermally conductive systems for power electronics, and ultra-fast UV/LED curing that compress cycle times without compromising bond integrity. Benchmarks span shear/peel strength, toughness under fatigue, thermal cycling stability, creep, dielectric performance, corrosion mitigation, and total applied cost—mapped to joining of metals, composites, plastics, and multi-material stacks. With comparative vendor capability grids and use-case playbooks for Body-in-White, composite bonding, battery pack assembly, and precision electronics, this report is an essential resource for engineering leaders, sourcing and quality teams, and R&D professionals seeking defensible specifications and faster qualification in safety-critical, low-VOC manufacturing.

Scope Highlights

Segmentation:

- By Resin/Chemistry Type: Epoxy Adhesives; Polyurethane Adhesives; Acrylic Adhesives; Cyanoacrylate Adhesives; Silicone Adhesives; Anaerobic Adhesives; Reactive Hot Melts.

- By Technology: Reactive Adhesives; Solvent-Based Adhesives; Water-Based Adhesives; Hot Melt Adhesives; UV/Light-Cured Adhesives.

- By End-Use Industry: Automotive & Transportation; Aerospace & Defense; Electronics & Electrical; Building & Construction; Wind Energy; Medical Devices; General Industrial Assembly.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ companies covering strategy, capacity moves, certifications, and sustainability roadmaps.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.