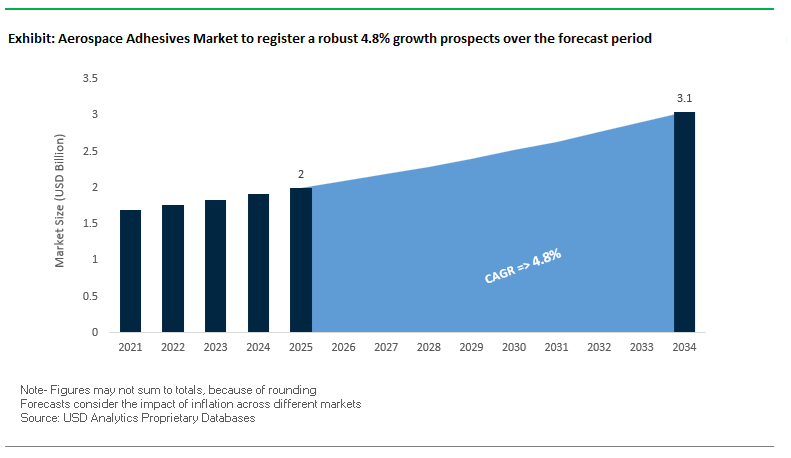

The global aerospace adhesives market is projected to expand from $2.0 billion in 2025 to $3 billion by 2034, growing at a CAGR of 4.8%. This steady growth trajectory is underpinned by surging demand for structural bonding solutions, lightweight composite assembly, and sustainable formulations compliant with tightening Volatile Organic Compound (VOC) regulations. The transition from traditional mechanical fastening to high-strength aerospace structural adhesives is redefining manufacturing efficiency, improving fatigue resistance, and enabling next-generation aircraft designs that are lighter, safer, and more durable.

For aerospace OEMs, Tier-1 suppliers, and MRO facilities, the market’s direction revolves around five operational imperatives — material performance, regulatory compliance, production throughput, sustainability, and weight reduction. With major aircraft platforms increasingly relying on epoxy and film adhesives for composite bonding, manufacturers are focusing on precision-engineered chemistries designed to deliver superior mechanical, thermal, and chemical resistance.

Epoxy resins maintain dominance due to their exceptional strength, cohesive durability, and adhesion versatility across composite ribs, wing skins, and metallic fuselage sections. Structural bonding applications ensure the replacement of mechanical fasteners with lightweight adhesive systems that meet rigorous FAA and EASA certifications. The commercial aviation segment is driven by growing fleet deliveries and robust MRO (Maintenance, Repair, and Overhaul) cycles. Manufacturers are also innovating with metal bonding films capable of enduring temperatures up to 550°F (288°C) for engine and nacelle structures, a vital factor in sustaining integrity under extreme flight conditions.

Further, global players are rapidly transitioning toward low-VOC, water-borne, and 100% solids formulations. These technologies align with sustainability targets under EU REACH and U.S. EPA frameworks, signaling a transformative shift toward eco-compliant, high-performance aerospace adhesive systems.

The global aerospace adhesives industry is in a phase of structural evolution, driven by material innovation, sustainability mandates, and supply chain consolidation. In August 2025, Bron Tapes acquired NSL Aerospace, a leading distributor of aerospace adhesives, sealants, and rotables in the U.S., reflecting an ongoing trend of vertical integration and supply chain optimization. This acquisition strengthens North American technical distribution networks, ensuring enhanced logistics and technical support for OEMs and aviation MRO clients across the commercial and defense sectors.

In September 2025, PPG Industries announced a $380 million investment to construct a dedicated aerospace coatings and sealants plant in Shelby, North Carolina, signaling a major capacity expansion in the U.S. market. This facility is strategically aligned with the rising demand from civil aviation, defense aircraft production, and OEM supply contracts, enhancing domestic production resilience for critical aerospace coatings and sealants.

Throughout Q4 2025, key suppliers unveiled new two-part, room-temperature-curing paste adhesives with improved work-life and accelerated strength development, catering to the need for faster assembly cycles and cost-efficient structural bonding. Similarly, during Q3 2025, companies like 3M, Henkel, and Solvay expanded R&D initiatives targeting lightweight sealants tailored for eVTOL (Electric Vertical Take-Off and Landing) platforms. These next-generation lightweight aerospace adhesives are engineered for thermal stability, vibration damping, and multi-material bonding, crucial to the performance and safety of electric and hydrogen-powered aircraft.

Looking forward, regulatory shifts are redefining the aerospace adhesive chemistry landscape. In Q1 2026, European authorities finalized new PFAS (per- and polyfluoroalkyl substances) restrictions, directly affecting fluoropolymer-based sealants. Anticipating these mandates, leading formulators have accelerated the qualification of PFAS-free aerospace adhesives and low-VOC systems. Meanwhile, Q4 2025 marked the debut of UV-cured elastomeric sealants engineered for rapid exterior aircraft repairs, reducing downtime and improving MRO turnaround efficiency. The period also saw a surge in partnerships centered on Benzoxazine Resin Technology, which offers low-outgassing and high thermal stability for composite aircraft structures.

Finally, in Q1 2026, an Asian chemical manufacturer commissioned a new production line for high-purity polyurethane (PU) and silicone aerospace sealants, supporting Asia-Pacific’s rapidly expanding aviation manufacturing ecosystem. This regional development underscores the sector’s globalization trend, as suppliers race to meet rising demand for fuel tank, interior, and structural sealants in both commercial and defense segments.

The shift toward sustainable, high-performance propulsion systems—including ultra-efficient jet engines, SAF-compatible combustion designs, and hydrogen-based propulsion architectures—is driving a new generation of aerospace adhesives capable of maintaining structural integrity in extreme thermal and chemical environments. Traditional epoxy systems, while dominant in airframe bonding, are being supplemented by polyimide, phenolic, and ceramic-based adhesives that can operate at significantly higher service temperatures.

Advanced turbine assemblies in modern engines often expose bonded joints to continuous operating temperatures exceeding 260°C (500°F). To meet these demands, manufacturers have introduced polyimide formulations that maintain adhesive strength and mechanical stability at these elevated temperatures. These next-generation materials are specifically engineered for engine nacelles, afterburner components, and high-stress interfaces, where standard aerospace-grade epoxies lose adhesion under cyclic thermal load.

Major OEM suppliers are actively investing to scale the innovation. 3M, for instance, committed over $40 million in expansion investments to bolster production of high-performance adhesives and tapes for aerospace applications—specifically targeting next-generation propulsion bonding solutions for both civil and defense programs. The industry-wide push reflects a structural trend toward capacity expansion in high-performance polymer production, particularly for adhesives serving high-heat and high-vibration environments.

In parallel, for extreme aerospace environments—such as rocket engines, thermal protection systems (TPS), and atmospheric re-entry components—R&D has advanced ceramic adhesives that maintain bond rigidity up to 1000°C (1832°F). These inorganic adhesives, often based on alumina and zirconia systems, offer exceptional oxidation resistance, dielectric stability, and creep performance, marking the frontier of thermal management innovation in aerospace bonding materials.

The transition toward composite-intensive airframes represents one of the most significant paradigm shifts in modern aerospace engineering. Advanced commercial aircraft—such as the Boeing 787 Dreamliner and Airbus A350 XWB—incorporate over 50% composite materials by weight, necessitating highly specialized structural adhesives that can deliver both strength and flexibility under dynamic load conditions.

Research published in the Journal of Adhesion confirms that advanced toughened epoxy systems, tested using double strap joint (DSJ) composite adherends, demonstrate superior damage tolerance even when subjected to manufacturing defects such as bond-line voids or porosity. These properties are critical for airworthiness certification and ensure load-bearing stability across bonded joints, even under fatigue or high-strain cycling.

The aerospace sector’s design philosophy has evolved from a “safe-life” to a “damage-tolerant” approach, placing a premium on adhesives capable of withstanding crack propagation and delamination. Formulations incorporating elastomeric modifiers or nano-reinforcements (e.g., silica nanoparticles, carbon nanotubes) have been shown to deliver a 4–10× improvement in fracture toughness (GIC) compared to conventional aerospace-grade epoxies. These adhesive systems not only enhance structural integrity but also ensure predictable failure modes, a crucial factor for FAA and EASA certification in primary load-bearing applications.

Additionally, global research roadmaps from NASA, Airbus, and the UK Aerospace Technology Institute (ATI) highlight that bonded primary structures are expected to dominate future aircraft assembly—but success depends on improving inspectability, environmental resistance, and long-term aging predictability of the adhesive bond line. As a result, the focus of ongoing R&D is shifting toward adhesives with self-monitoring capabilities, offering in-situ health tracking of structural joints.

The expanding market for Unmanned Aerial Vehicles (UAVs)—ranging from high-endurance surveillance drones to attritable combat platforms—is creating a new segment of demand for fast-curing, lightweight aerospace adhesives. UAV manufacturers require bonding solutions that combine high strength-to-weight ratios, chemical resistance, and automated process compatibility to support rapid, high-throughput production.

The ongoing evolution of UAV design emphasizes speed and scalability. To meet the, manufacturers are increasingly turning to UV-cured and structural acrylic adhesives, capable of polymerizing in seconds under ultraviolet exposure. These systems are particularly beneficial for composite and thermoplastic assemblies, where faster cure cycles dramatically reduce production time and labor costs.

In defense UAV production, where multi-material construction (e.g., aluminum frames bonded to 3D-printed nylon 12 or carbon fiber composites) is common, the use of cyanoacrylate and rapid-setting acrylic adhesives enables high-strength bonding with minimal surface preparation. The enhances automation potential, supporting streamlined assembly lines for large-volume UAV programs.

Thermal management represents another critical design constraint. UAV and eVTOL platforms utilize thermally conductive adhesives (TCAs) to improve battery and power system reliability by dissipating heat evenly across cells, mitigating thermal runaway risks. With rising regulatory scrutiny over electric propulsion safety, the application alone is emerging as a high-margin niche for adhesive manufacturers.

The global commercial aviation fleet, with an average age exceeding 13 years, is driving a long-term opportunity for certified aerospace MRO adhesives used in airframe repair, structural restoration, and composite patch bonding. Fleet aging—combined with production delays in new aircraft deliveries—has intensified reliance on maintenance, repair, and overhaul (MRO) operations to ensure flightworthiness and extend service life.

Data from Aviation Week Network indicates that older aircraft, particularly those over 20 years old, require more frequent use of structural adhesives for corrosion repair, fairing bonding, and composite patch application. Certified repair adhesives have become indispensable for 7000-series aluminum structures and early-generation CFRP panels, both of which dominate aging fleet inventories.

Emerging MRO technologies such as automated scarfing and bonding robots have increased composite repair efficiency by up to 60% compared to manual methods, reducing turnaround times while ensuring repeatable bond quality. The automation trend is fueling demand for rapid-cure, ambient-temperature repair adhesives that are compatible with on-wing repair protocols, minimizing downtime.

The economics of composite repair versus component replacement also reinforce adhesives’ strategic importance. Certified structural bonding methods can deliver repair cost savings of up to 70% compared to full replacement of composite assemblies such as flaps, winglets, and fairings. Consequently, the aftermarket adhesives segment has emerged as a high-margin, recurring revenue source for both OEM suppliers and specialized MRO distributors.

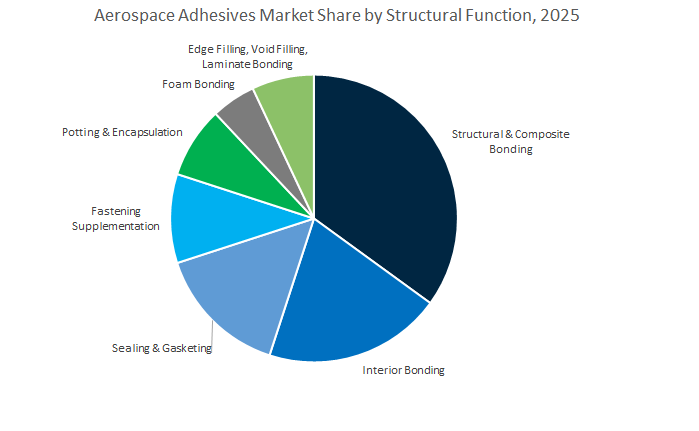

Aerospace Adhesives Market Share Insights, 2025-2034

The structural and composite bonding segment dominates the global aerospace adhesives industry, accounting for approximately 35% of the total market share in 2025. This leadership stems from the aerospace sector’s accelerating shift toward lightweight composite materials in primary structures such as wings, fuselage panels, and empennage assemblies. Structural adhesives are vital for replacing traditional fasteners like rivets and bolts, enabling weight reduction, improved aerodynamics, and fuel efficiency without compromising strength. Epoxy and film adhesives are the preferred chemistries in this segment, offering exceptional load-bearing capability, fatigue resistance, and durability under extreme temperatures and stress cycles. The aerospace industry’s growing dependence on carbon-fiber-reinforced polymers (CFRPs) and hybrid composite-metal joints has solidified structural bonding’s critical role in next-generation aircraft manufacturing. With OEMs such as Boeing and Airbus adopting automated adhesive bonding technologies to enhance precision and reduce assembly complexity, this segment continues to represent the core performance and value driver of the aerospace adhesives market.

The interior bonding segment, holding around 20% of the market share, plays a key role in cabin assembly, interior panels, and aesthetic components where both functionality and passenger comfort are paramount. Adhesives are extensively used for overhead stowage bins, flooring systems, galley modules, insulation panels, and decorative laminates, ensuring lightweight construction while meeting stringent flammability, smoke density, and toxicity (FST) regulations mandated by global aviation authorities. Polyurethane, acrylic, and epoxy adhesives dominate this category for their flexibility, sound-damping, and vibration-absorption characteristics. The rise of next-generation cabin designs, with an emphasis on noise reduction, space optimization, and premium finishes, is amplifying demand for multi-functional, low-VOC, and low-density adhesive systems. Furthermore, the growing use of composite interior materials and thermoplastic laminates in aircraft cabins is expanding the need for specialized adhesives that can bond dissimilar substrates. This segment’s steady growth reflects the broader shift toward passenger-centric design and sustainability-driven material innovation within the aerospace sector.

The sealing and gasketing segment represents one of the most critical functional applications in aerospace, as it ensures structural integrity, pressurization, and environmental protection across the aircraft. Sealants and gasket adhesives are indispensable for fuel tanks, windows, airframe joints, and fuselage seams, where they provide airtight sealing, corrosion resistance, and protection against extreme temperatures and fluids. Silicones, polysulfides, and fluorosilicones dominate this category due to their exceptional elasticity, chemical resistance, and compliance with FAA and EASA specifications. As aircraft platforms evolve to incorporate advanced fuel systems, composite structures, and hybrid propulsion, the demand for low-density, non-corrosive, and high-temperature sealants is growing significantly. The sealing and gasketing segment also plays a vital role in spacecraft and military aircraft, where exposure to vacuum and cryogenic conditions requires specialized formulations capable of maintaining stability beyond –150°C and above +250°C. This segment’s resilience lies in its indispensability across both OEM assembly and long-term maintenance operations, ensuring consistent demand throughout the aerospace lifecycle.

The fastening supplementation segment represents a strategic evolution in aircraft assembly, driven by the push for weight optimization and structural efficiency. Adhesives are increasingly used alongside mechanical fasteners to reduce stress concentrations, enhance load distribution, and improve fatigue life in bonded joints. This function is particularly valuable in fuselage skin-to-frame bonding, stringer attachment, and wing rib assemblies, where adhesives enable smoother aerodynamic surfaces and reduce the number of required rivets. Reactive adhesives such as epoxies and polyurethanes dominate this area, offering both structural and vibration-damping benefits. OEMs are integrating bonded-fastening hybrid systems into modern aircraft platforms to enhance strength-to-weight ratios, reduce assembly time, and improve manufacturability. As automated adhesive dispensing systems become more prevalent in aerospace production lines, fastening supplementation will continue to gain share, bridging the gap between traditional joining techniques and advanced material bonding technologies.

The OEM (Original Equipment Manufacturer) segment holds the largest share of the global aerospace adhesives market, estimated at 65% in 2025. This dominance is driven by the production of new commercial, military, and space-grade aircraft, each requiring hundreds of kilograms of adhesives for structural assembly, composite bonding, and surface sealing. The OEM sector is the innovation hub of the aerospace adhesives industry, continuously pushing material science to develop lighter, stronger, and more sustainable bonding systems that meet the next generation of aircraft design challenges. Epoxy and film adhesives are widely used in primary airframe assembly, while polyurethane and acrylic formulations dominate interior and secondary structures. The growing adoption of automated adhesive dispensing, robotic assembly, and out-of-autoclave curing processes has improved manufacturing efficiency and precision at scale. Furthermore, leading OEMs like Airbus, Boeing, Lockheed Martin, and Embraer are partnering with chemical manufacturers to co-develop certified adhesive solutions for composite-intensive aircraft platforms. With aircraft production recovering post-pandemic and long-term order backlogs expanding, the OEM sector remains the primary engine of demand and material innovation for aerospace adhesives globally.

The MRO (Maintenance, Repair, and Overhaul) segment, holding approximately 35% of market share, forms the long-term revenue foundation of the aerospace adhesives industry. Unlike the cyclical nature of OEM production, MRO demand remains steady, driven by the expanding global fleet, increasing aircraft utilization rates, and strict airworthiness regulations. Adhesives in this sector are essential for structural repairs, composite patching, cabin refurbishments, and component re-bonding, where performance reliability and certification compliance are paramount. MRO operations require OEM-approved, qualified adhesives that can seamlessly integrate with existing materials and processes, ensuring flight safety and structural integrity. The segment’s stability is further reinforced by the aging aircraft population, with many airframes requiring re-bonding of interior panels, windows, and seals during scheduled maintenance intervals. Moreover, as airlines pursue cabin modernization and comfort upgrades, there is a rising demand for flame-retardant, low-VOC adhesives compatible with next-generation interior materials. With the global fleet projected to double over the next two decades, the MRO segment offers a resilient, recurring demand base, balancing the cyclical fluctuations of OEM production.

Both OEM and MRO segments play complementary yet strategically distinct roles in the aerospace adhesives ecosystem. The OEM sector drives technological innovation, certification, and material qualification, while the MRO sector ensures sustainability, longevity, and operational reliability of aircraft fleets.

The global aerospace adhesives market features a highly consolidated structure dominated by technology leaders like Henkel, H.B. Fuller, Arkema (Bostik), 3M Company, and Solvay S.A. Each player is intensifying R&D efforts to align with the aerospace industry’s goals of lightweighting, automation, VOC reduction, and composite integration. Their strategic priorities span from high-temperature epoxy systems to low-outgassing and PFAS-free formulations, underpinned by global investments in production capacity and regulatory-compliant product innovation.

Henkel remains a global leader in structural and non-structural aerospace adhesives through its Loctite and Hysol brands. Its LOCTITE EA 9658 AERO film adhesive delivers exceptional flow control and toughness at 350°F (177°C) service conditions, ideal for composite and metal bonding. Products like LOCTITE EA 9696 offer long out-times (up to 90 days at 77°F), enabling flexibility in complex multi-day aircraft assembly. Henkel’s R&D pipeline focuses on Benzoxazine resin technology, optimizing for low outgassing and high thermal stability, suitable for next-generation defense and space programs. The company also provides two-part epoxy pastes for honeycomb repair, offering superior performance and ease of application.

H.B. Fuller continues to excel as the world’s largest pure-play adhesives company, with specialization in aerospace fuel tank sealants and flexible bonding applications. The company’s polysulfide sealants, qualified to AMS-S-8802 and MIL-PRF-81733 standards, are widely used in fuselage and wing sealing. Operating an AS9100 and NADCAP-certified facility in Wilmington, California, H.B. Fuller ensures compliance with stringent aerospace quality standards. Its portfolio includes polyurethane and PVC adhesives for elastomeric structures like escape slides, while its Double Bubble Red product line supports defense MRO and ground support equipment with rapid-setting adhesive performance.

Arkema’s Bostik division focuses on “smart adhesives” that combine elasticity, torsional rigidity, and extreme temperature resistance. As part of Arkema’s High-Performance Materials segment, Bostik’s aerospace adhesives prioritize low-VOC and solvent-free technologies, aligned with sustainable manufacturing initiatives. Following the Polytec PT acquisition in 2023, Bostik expanded into thermally and electrically conductive adhesives for aerospace electronics and battery systems. Its R&D strategy emphasizes elastic bonding, polymer-modified binders, and pressure-sensitive hotmelt adhesives—key enablers in aircraft interiors and insulation assemblies.

3M Company remains at the forefront of high-performance aerospace bonding with its Scotch-Weld structural adhesives and VHB tapes, renowned for strength, fatigue resistance, and environmental durability. 3M’s product innovations meet FAR 25.853 standards for fire, smoke, and toxicity compliance in aircraft interiors. The company’s R&D investments center on developing adhesives and sealants that improve assembly efficiency and surface protection for metallic and composite substrates. 3M’s integrated approach extends beyond adhesives to include surface preparation systems, enhancing corrosion protection and adhesion reliability across critical structures.

Solvay commands a strong position in advanced thermoset and thermoplastic aerospace adhesives, with proven expertise in BMI (Bismaleimide) and epoxy-based film systems used in primary structural assemblies. Its adhesives are engineered for extreme heat and chemical resistance, with several qualified for NASA ASTM E-595 low-outgassing standards, ensuring compatibility with spacecraft and satellite applications. Solvay’s R&D emphasizes fast-curing, high-rate production adhesives to improve OEM efficiency and enable CFRP-to-metal bonding for hybrid aircraft structures. This innovation-driven approach supports the industry’s transition toward lightweight, fuel-efficient aircraft platforms.

The United States aerospace adhesives industry remains the global leader, driven by an extensive network of aircraft OEMs, defense contractors, and R&D institutions that consistently push the boundaries of advanced bonding materials. With the FY 2025 U.S. defense budget allocating over $143 billion to RDT&E, the demand for high-performance epoxy systems and structural film adhesives has surged, particularly for sixth-generation fighter jets, composite fuel tanks, and stealth applications. Companies are focusing on lightweighting and next-generation materials, targeting improved fuel efficiency, structural durability, and reduced maintenance costs across defense and commercial aviation.

In terms of industrial expansion, PPG Industries’ $380 million North Carolina facility, announced in May 2025, will significantly enhance domestic supply for aerospace coatings and sealants, bolstering U.S. manufacturing resilience amid global supply chain disruptions. Meanwhile, Park Aerospace Corp. continues to innovate, launching the Aeroadhere FAE-350-1 structural film adhesive (July 2023), designed for bonding primary and secondary aircraft structures. U.S. R&D remains heavily focused on self-healing structural adhesives, toughened epoxy formulations, and low-VOC sealants that meet FAA 14 CFR 25.853 flame, smoke, and toxicity (FST) standards. The innovations ensure compliance and safety while optimizing performance in composite wing bonding, avionics potting, and high-temperature applications, solidifying the United States’ dominance in aerospace-grade adhesive engineering.

Germany is at the forefront of Europe’s aerospace adhesive innovation, driven by its advanced manufacturing base and aerospace R&D ecosystem. German adhesive suppliers are pioneering automated robotic bonding lines for Airbus and European OEMs, improving consistency and productivity in composite assembly. R&D partnerships between chemical giants and engineering universities are accelerating the development of bio-based aerospace adhesives that align with the EU’s REACH regulations and Green Deal sustainability goals.

As the country advances its lightweighting strategy, demand for toughened epoxy adhesives and co-curing formulations used in carbon fiber reinforced polymer (CFRP) components continues to grow. The materials are essential for aircraft like the Airbus A350 and next-generation Eurofighter platforms, where weight reduction directly enhances range and fuel efficiency. Additionally, German manufacturers are scaling capacity for fast-curing structural adhesives and high-performance polyurethane sealants, crucial for Maintenance, Repair, and Overhaul (MRO) operations across Europe. The integration of sustainability, automation, and high-strength bonding positions Germany as a core hub for precision aerospace adhesive technologies in Europe.

China’s aerospace adhesives market is witnessing rapid expansion, driven by its domestic aircraft programs, MRO capacity building, and strategic localization policies. With the success of the COMAC C919 and ARJ21 aircraft, demand for aerospace-grade epoxy and polyurethane adhesives has surged, especially in laminate bonding, composite fuselage assembly, and cabin interior applications. China is also expanding its local resin production capacity, addressing regional supply gaps for high-performance aerospace adhesives.

Government-backed initiatives emphasizing import substitution and indigenous innovation are propelling domestic R&D in fire-retardant sealants, polysulfide-based fuel tank adhesives, and high-temperature epoxies. The 2025 expansion of MRO hubs across cities such as Shanghai and Chengdu highlights a robust rise in adhesive demand for fuselage maintenance, crack repair, and interior refurbishment. September 2025 industry updates confirm strong growth in aerospace interior adhesives, as the nation modernizes both commercial and military fleets. By combining policy-driven localization with technology partnerships from Western firms, China is consolidating its role as Asia-Pacific’s largest aerospace adhesive production and consumption hub.

France, home to Airbus’s largest production facilities, remains one of the most dynamic markets for aerospace adhesives and bonding materials. French suppliers are deeply integrated into OEM supply chains, particularly focusing on film adhesives, bonding pastes, and acrylic systems tailored for high-volume single-aisle aircraft production. Ongoing R&D in digital adhesive application systems and process automation supports Airbus’s goal of achieving precision-controlled, zero-defect composite assembly lines.

The Arkema Group (Bostik) continues to lead in smart adhesives—materials that self-heal and adapt to dynamic stress conditions—paving the way for more reliable aerospace structures. Meanwhile, cryogenic and extreme-temperature bonding solutions are gaining traction in France’s space and defense sectors, supported by European Space Agency projects. Acrylic and methacrylate adhesives are also replacing traditional mechanical fasteners in interior assemblies, enhancing durability and reducing maintenance. France’s synergy of smart material innovation, digital process control, and OEM integration reinforces its leadership in European aerospace adhesive technology.

India’s aerospace adhesives industry is rapidly advancing, driven by the government’s ‘Make in India’ initiative, defense modernization, and growing commercial fleet expansion. The push toward indigenous manufacturing through Hindustan Aeronautics Limited (HAL) and private-sector collaborations has spurred investments in certified aerospace epoxy, polyurethane, and polysulfide adhesives. International firms like Henkel have strengthened their footprint with new manufacturing plants at Kurkumbh (near Pune) and an Application Engineering Centre in Chennai, improving access to high-performance adhesive and coating technologies for aerospace applications.

India’s aviation infrastructure is expanding, with multiple new MRO hubs under development to support both defense and civil aircraft fleets. The facilities are creating strong demand for repair-grade adhesives and sealants that meet stringent aerospace quality certifications (AMS, MIL-STD). Local R&D efforts are also focused on producing climate-resilient bonding systems capable of withstanding India’s diverse temperature and humidity profiles. Furthermore, the rise in UAV and defense component manufacturing is increasing the use of lightweight film adhesives for composite-metal hybrid structures, marking India as an emerging hub for aerospace material innovation in the Asia-Pacific region.

Japan’s aerospace adhesive market is built upon its precision manufacturing expertise and deep materials science capabilities. Companies such as Teijin, Toray, and Three Bond Co. Ltd. are global leaders in high-temperature, chemically resistant adhesives for engine assemblies, electronics, and composite structures. In July 2025, Teijin Carbon Europe achieved Nadcap accreditation, confirming compliance with the highest aerospace standards for its epoxy resin systems and composite prepregs, underscoring Japan’s commitment to quality in advanced adhesive materials.

Japan’s focus on R&D-driven breakthroughs includes polyimide-based adhesives for high-temperature sensors, flexible circuits, and insulation applications, as well as ceramic bonding systems for aerospace and space missions. The country’s defense and space sectors are also increasing reliance on ceramic and ultra-heat-resistant adhesives capable of withstanding re-entry conditions. Simultaneously, Japanese manufacturing facilities are deploying automation and robotics for adhesive dispensing and curing, ensuring uniform bond-line control in composite-to-metal joints. The integration of material innovation and precision automation ensures Japan’s continued dominance in next-generation aerospace adhesive technologies.

Aerospace Adhesives Market Report Scope

Aerospace Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$3 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Silicone, Acrylic, Cyanoacrylate (CA), Polyimide, Polysulfide, VAE/EVA, Others), By Product Type (Adhesives, Sealants), By Structural Function (Structural Bonding, Interior Bonding, Composite Bonding, Edge Filling, Void Filling, Potting & Encapsulation, Laminate Bonding, Foam Bonding, Sealing & Gasketing, Fastening Supplementation), By Technology (Solvent-Based, Water-Based, Reactive, Hot Melt, UV Cured Adhesives, Film Adhesives), By End-User (OEM, MRO), By Aircraft Type (Commercial Aircraft, Military Aircraft, General Aviation, Helicopters, Spacecraft/Launch Vehicles, Unmanned Aerial Vehicles (UAVs)), By Application Area (Fuselage/Primary Structure, Wings, Cabin Interiors, Engine Components/Nacelles, Landing Gear, Windows/Canopies, Avionics/Electronics), By Form (Liquid, Paste, Film, Powder

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, PPG Industries Inc., H.B. Fuller Company, Huntsman International LLC, Arkema Group (Bostik), Sika AG, Solvay, Dow Inc., Hexcel Corporation, Master Bond Inc., Delo Industrial Adhesives LLC, Permabond LLC, Three Bond Co. Ltd., Ashland Global Holdings

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type (Chemical Type)

- Epoxy

- Polyurethane

- Silicone

- Acrylic

- Cyanoacrylate (CA)

- Polyimide

- Polysulfide

- VAE/EVA

- Others

By Product Type/Function

By Structural Function

- Structural Bonding

- Interior Bonding

- Composite Bonding

- Edge Filling

- Void Filling

- Potting & Encapsulation

- Laminate Bonding

- Foam Bonding

- Sealing & Gasketing

- Fastening Supplementation

By Technology

- Solvent-Based

- Water-Based

- Reactive

- Hot Melt

- UV Cured Adhesives

- Film Adhesives

By End-Use Sector

By Aircraft Type

- Commercial Aircraft

- Military Aircraft

- General Aviation

- Helicopters

- Spacecraft/Launch Vehicles

- Unmanned Aerial Vehicles (UAVs)

By Application Area

- Fuselage/Primary Structure

- Wings

- Cabin Interiors

- Engine Components/Nacelles

- Landing Gear

- Windows/Canopies

- Avionics/Electronics

By Form

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- PPG Industries Inc.

- H.B. Fuller Company

- Huntsman International LLC

- Arkema Group (Bostik)

- Sika AG

- Solvay

- Dow Inc.

- Hexcel Corporation

- Master Bond Inc.

- Delo Industrial Adhesives LLC

- Permabond LLC

- Three Bond Co. Ltd.

- Ashland Global Holdings

*- List not Exhaustive

Research Coverage

Developed by USDAnalytics, this report investigates the global aerospace adhesives market’s climb from $2.0 billion in 2025 to $3 billion by 2034, decoding how structural bonding, composite-intensive builds, and VOC-free chemistries realign OEM and MRO specifications. Our analysis reviews rate-readiness (film vs. paste), cure windows, out-time discipline, and certification pathways under FAA/EASA while mapping breakthroughs in high-temperature polymers, damage-tolerant toughened epoxies, and PFAS-free reformulations. It highlights sourcing risk, cost-in-use, and automation fit (robotic layup, OOA/OOI) across primary/secondary structures and interiors. With scenario bands, price/mix models, and program backlog linkages, this report is an essential resource for strategy, procurement, engineering, and product teams seeking lighter airframes, faster takt, and assured airworthiness—without sacrificing durability or sustainability.

Scope Includes

- By Resin Type (Chemical Type): Epoxy; Polyurethane; Silicone; Acrylic; Cyanoacrylate (CA); Polyimide; Polysulfide; VAE/EVA; Others.

- By Product Type/Function: Adhesives; Sealants.

- By Structural Function: Structural Bonding; Interior Bonding; Composite Bonding; Edge Filling; Void Filling; Potting & Encapsulation; Laminate Bonding; Foam Bonding; Sealing & Gasketing; Fastening Supplementation.

- By Technology: Solvent-Based; Water-Based; Reactive; Hot Melt; UV Cured Adhesives; Film Adhesives.

- By End-Use Sector: OEM; MRO.

- By Aircraft Type: Commercial; Military; General Aviation; Helicopters; Spacecraft/Launch Vehicles; UAVs.

- By Application Area: Fuselage/Primary Structure; Wings; Cabin Interiors; Engine Components/Nacelles; Landing Gear; Windows/Canopies; Avionics/Electronics.

- By Form: Liquid; Paste; Film; Powder.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Horizon: Historical 2021–2024; Forecast 2025–2034.

- Companies: 15+ company analysis/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.