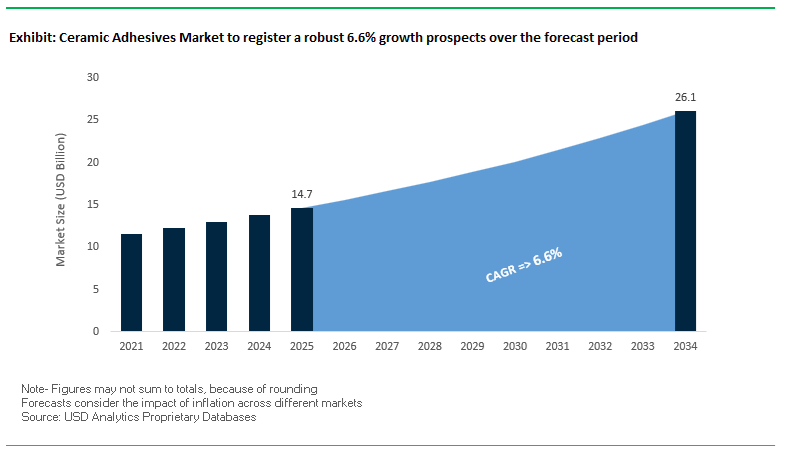

The ceramic adhesives market has become strategically critical as construction specifications shift toward larger tile formats, faster installation cycles, and verified indoor air quality performance. Valued at USD 14.7 billion in 2025 and projected to reach USD 26.1 billion by 2034 at a CAGR of 6.6%, growth reflects the central role of adhesive systems in managing the mechanical and thermal stresses introduced by large-format porcelain, thin panels, façade systems, and underfloor heating assemblies. For professional installers, façade engineers, and OEM-aligned contractors, adhesive selection directly influences placement accuracy, long-term durability, and compliance with evolving building standards rather than serving as a secondary consumable.

The core structural shift reshaping demand is the rapid replacement of conventional cementitious mortars with polymer-modified, high-deformation ceramic adhesives engineered to meet S2 performance requirements. As tile dimensions increase and substrates experience greater movement, polymer-modified cementitious systems are being specified for their ability to accommodate deformation without debonding, particularly in exterior façades and heated floor systems. In parallel, low-VOC ceramic adhesives—supported by water-based and bio-based epoxy technologies—are becoming standard across commercial and residential projects as LEED, BREEAM, and WELL certification frameworks tighten indoor air quality thresholds. In industrial and chemically aggressive environments, R2-grade reaction resin adhesives, predominantly epoxy-based, continue to displace legacy systems by delivering sustained resistance to acids, alkalis, and high mechanical loads where cementitious products fail.

Installation efficiency and precision are decisive performance drivers, accelerating adoption of gel-technology ceramic adhesives with thixotropic behavior. These next-generation formulations provide zero vertical slip and extended open times exceeding 30 minutes, enabling accurate placement of large-format porcelain on vertical and overhead surfaces while reducing rework and downtime. By stabilizing tiles immediately upon placement and extending working time, gel adhesives translate material performance into measurable business outcomes—lower labor intensity, faster project completion, and reduced installation risk. Looking forward, competitive advantage in the ceramic adhesives market will increasingly depend on manufacturers’ ability to scale low-VOC, polymer-enhanced, and gel-based systems with consistent rheology, standards compliance, and formulation control aligned with modern construction practices and regulatory requirements.

The Global Ceramic Adhesives Industry has undergone significant evolution in recent years, underpinned by sustainability regulations, raw material innovation, and automation in construction material production.

In May 2025, Mapei launched its Keraflex S1 Evolution Zero, a low-carbon, eco-sustainable cementitious adhesive that incorporates 20% recycled material and meets EN 12004 C2TES1 standards. This launch reflects the company’s long-term commitment to carbon-neutral construction products designed for sustainable infrastructure and façade cladding. Earlier, in April 2025, H.B. Fuller strengthened its regional presence by commissioning a new specialty adhesive production facility in Southeast Asia, aiming to improve supply chain resilience and localize production for high-traffic flooring adhesives.

In February 2025, Sika Corporation introduced a next-generation polymer-modified tile adhesive engineered for high-rise facades and thermal-cycling performance, emphasizing compliance with European wind-load standards. This followed the June 2024 launch of SikaCeram-255 Large Tile, a no-slip, extended open-time adhesive optimized for heavy porcelain tile installations up to 3600 cm², addressing the professional market’s need for flexibility and stability in large tile applications.

Sustainability directives are shaping the industry’s formulation strategies. In September 2024, the European Union announced new Life Cycle Assessment (LCA) standards for construction materials, compelling adhesive manufacturers to adopt low-impact binders and sustainable polymer additives. Meanwhile, Saint-Gobain Weber reinforced its contractor support through expanded Weber Academy programs in December 2024, promoting correct application of high-flexibility, waterproof tile adhesives for swimming pools and wet zones.

Additionally, innovations in raw material sourcing and chemistry are transforming epoxy technologies. In July 2024, a construction technology firm patented a bio-based epoxy adhesive derived from vegetable oils, cutting fossil-fuel dependency in high-performance tile bonding applications. Similarly, an October 2024 merger between a specialty chemical giant and an epoxy resin manufacturer secured vital feedstock supply for reaction resin (R2) ceramic adhesives, enhancing vertical integration and ensuring material consistency for industrial flooring.

The industry is witnessing a decisive shift from traditional, long-curing adhesives toward rapid-setting, high-performance cementitious formulations, reflecting the market’s growing emphasis on speed, productivity, and reliability in both commercial and residential construction. Modern tile adhesives classified under EN 12004 C2FT standards exhibit tensile adhesion strengths of ≥0.5 MPa within six hours, a stark improvement over the conventional 28-day curing cycle. The enhanced early strength performance enables walk-on capability within 2–3 hours post-installation—an essential advantage in high-traffic zones such as airports, shopping complexes, and public infrastructure projects where downtime equates to significant financial loss.

Technological innovation in cement-polymer chemistry is central to the transition. Advanced formulations employ Alumina Cement as a core binder, combined with polymer dispersions and cellulose ethers to deliver both rapid hydration and controlled viscosity. These formulations achieve full bonding within 24 hours, offering structural reliability without shrinkage or loss of adhesion. In addition, they ensure consistent results in adverse temperature conditions, a critical factor for emergency repairs and fast-track renovations. The emergence of these high-efficiency systems is also supported by the global shift toward performance-certified adhesives, emphasizing consistent curing times, reduced installation risks, and robust compatibility across varied substrates. Consequently, rapid-set cementitious adhesives are becoming indispensable to contractors and tiling professionals aiming to optimize construction productivity and reduce labor costs while maintaining superior bond integrity.

The rapid architectural shift toward large-format porcelain slabs, underfloor heating systems, and lightweight building panels has amplified demand for ultraflexible, polymer-rich ceramic adhesives capable of absorbing thermal expansion, vibration, and structural movement without compromising adhesion. Adhesives meeting EN 12004-1 Class S2 (highly deformable) or S1 (flexible) standards have become the new performance benchmark, characterized by transverse deformability of ≥5 mm and long-term crack-bridging resilience.

The chemistry behind the flexibility lies in advanced polymer-modified blends, where latex, acrylic copolymers, and toughened epoxy systems increase elongation and elasticity. Comparative studies demonstrate that composite-modified epoxy adhesives improve Elongation at Break by 13–20% over single-component formulations, significantly enhancing fracture toughness and resistance to substrate movement. The allows these adhesives to accommodate temperature-induced stresses, particularly in heated floors, terraces, façades, and high-rise claddings exposed to cyclic thermal gradients. The rising popularity of ultra-large porcelain slabs (5x10 ft) and thin-format tiles further reinforces the need for flexible adhesives that maintain bonding integrity over expansive areas with minimal grout joints. These deformable, polymer-modified systems are also optimized for dynamic substrates like gypsum boards and concrete composites, providing the critical combination of adhesion strength, elasticity, and durability required for modern architectural installations.

As the construction industry undergoes a global sustainability transition, the ceramic adhesives market is experiencing growing demand for eco-friendly, low-carbon, and recycled-content formulations. Manufacturers are increasingly replacing traditional Portland cement with industrial byproducts like slag, fly ash, and recycled rubber powders, which not only enhance workability but also maintain adhesion levels consistent with EN 12004 C1 standards (≥0.5 MPa). These innovations contribute to both embodied carbon reduction and performance enhancement, enabling construction companies to meet net-zero goals and green certification criteria.

Further, the regulatory push toward sustainability is reshaping the manufacturing ecosystem. In Western Europe, for instance, 63% of producers are investing in dual-cure (UV + thermal) and low-VOC technologies, while 59% have initiated carbon-neutral production lines in alignment with the EU Green Deal. The adoption of Environmental Product Declarations (EPDs) and transparent lifecycle reporting has become a commercial differentiator in tender processes, particularly for large-scale public projects. Manufacturers are responding with bio-based polymeric binders, solvent-free dispersions, and energy-efficient curing systems, ensuring compliance with LEED and BREEAM standards. As green construction incentives expand, suppliers offering verified sustainable ceramic adhesives with quantifiable carbon footprint reductions are expected to secure competitive advantages in the European and North American markets.

The increasing architectural preference for large-format and seamless porcelain slabs is driving the evolution of specialized adhesive technologies that deliver exceptional non-sag (thixotropic) behavior and superior load-bearing performance. Modern installations often use tiles exceeding 5 feet by 10 feet, necessitating adhesives capable of sustaining their weight without slippage or void formation. According to EN 12004-1 Class T standards, high-performance tile adhesives must demonstrate slip resistance ≤0.5 mm, ensuring precise alignment during vertical or façade installations.

These adhesives feature rheology-controlled formulations that exhibit both fluidity for coverage and thixotropy for positioning stability. Combined with back-buttering techniques—where adhesive is applied to both the tile and substrate—they enable 100% surface contact, minimizing voids and reducing the risk of cracking under stress. The application of fluid-bed or gel-based systems has further enhanced wetting and cohesion on low-porosity surfaces such as polished porcelain and glass mosaics. The innovation directly caters to high-end architectural applications where aesthetic precision, long-term performance, and structural uniformity are non-negotiable.

With global megatrends in urban interiors favoring minimalist, continuous-surface designs, the demand for thixotropic, high-strength, large-format slab adhesives is expected to surge, especially in luxury residential, hospitality, and corporate infrastructure projects. Manufacturers focusing on high-ultimate-strength and zero-slip systems are positioned to capture premium segments of the construction adhesive market that prioritize installation efficiency, appearance quality, and lifetime durability.

Ceramic Adhesives Market Share Insights, 2025-2034

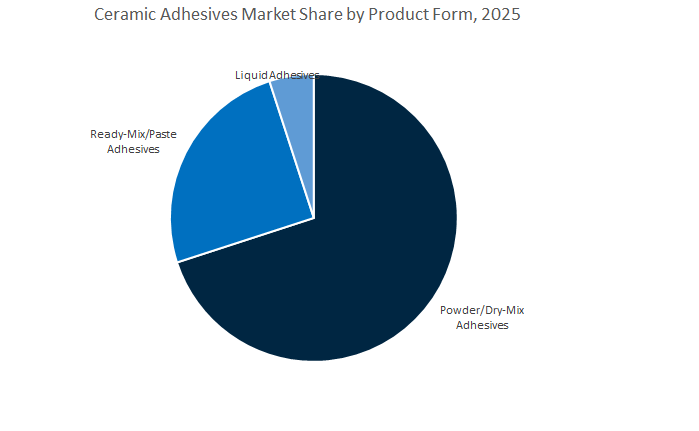

The Powder/Dry-Mix Adhesives segment dominates the global ceramic adhesives industry, accounting for approximately 68.2% of the projected 2025 market share. This strong position is driven by their unmatched performance characteristics and wide applicability across both residential and commercial construction projects. These cementitious or polymer-modified formulations—commonly based on Portland cement, redispersible polymer powders (RDPs), and specialty fillers—offer excellent adhesion strength, water resistance, and flexibility, making them ideal for high-performance tiling in wet areas, facades, and high-traffic zones. Powder adhesives are also favored by contractors and professionals for their customizable mixing ratios, long pot life, and extended open time, which enable precise work on large installations such as flooring, walls, and industrial tiles. From a logistics standpoint, they offer long shelf life, reduced transport weight, and minimal packaging waste, aligning with sustainability trends in construction materials. The continued rise in large-format and porcelain tiles, particularly in Europe, the Middle East, and Asia-Pacific, further strengthens this segment’s leadership, as these applications demand high bond strength and flexibility—properties that dry-mix systems deliver reliably. Additionally, regulatory pushes toward low-VOC and solvent-free products have reinforced the dominance of powder adhesives, which inherently comply with green building standards such as LEED and BREEAM.

The Ready-Mix or Paste Adhesives segment is emerging as a key growth area in the ceramic adhesives market, primarily catering to the residential renovation and DIY sectors. While holding a smaller share than dry-mix systems, this segment benefits from its ease of application, time-saving characteristics, and zero mixing requirements, making it particularly appealing for non-professional users and small contractors. Ready-mix adhesives, often dispersion-based or pre-blended polymer systems, are widely used for wall tiles, splashbacks, and small-area flooring where lightweight tiles and lower moisture exposure are typical. Despite their convenience, their relatively lower shear strength, heat resistance, and moisture tolerance restrict their use in heavy-duty or outdoor applications. However, continuous improvements in formulation—such as enhanced acrylic polymers, thixotropic modifiers, and antimicrobial additives—are helping ready-mix adhesives bridge the performance gap with cement-based counterparts. Growth is especially notable in urban renovation projects and small commercial refurbishments, where convenience and aesthetics outweigh heavy-duty performance needs. Furthermore, as the DIY tile installation trend accelerates, particularly in North America and Western Europe, the demand for these ready-to-use adhesives is expected to see steady gains through 2034.

The Liquid Adhesives segment represents a niche but technologically advanced portion of the global ceramic adhesives industry. These adhesives, often epoxy-based, polyurethane, or hybrid polymer formulations, cater to applications that require exceptional chemical resistance, rapid cure time, and superior adhesion to non-porous or metal substrates. Their use is especially critical in industrial facilities, laboratories, chemical processing units, and high-temperature environments, where standard cementitious or dispersion adhesives fail to perform. In these contexts, liquid systems are used for bonding ceramic tiles to steel, fiberglass, or composite surfaces, ensuring high mechanical strength and dimensional stability even under thermal or vibrational stress. While the volume share remains limited due to their higher cost and specialized handling requirements, the value contribution per unit is significant. The growing adoption of epoxy and reactive hybrid systems in food-grade and cleanroom environments further boosts this segment. Additionally, manufacturers are investing in low-VOC, solvent-free liquid adhesive technologies to align with global sustainability and workplace safety standards, ensuring that this segment maintains a critical position in the market despite its smaller volume share.

The Residential Construction segment is the undisputed leader in the global ceramic adhesives market, representing approximately 53.6% of the total market share in 2025. This dominance stems from the continuous global demand for housing construction, renovation, and remodeling activities, particularly in emerging economies across Asia-Pacific, the Middle East, and Latin America. Ceramic adhesives are integral to residential tiling applications, including bathrooms, kitchens, flooring, and exterior facades, where both functionality and aesthetics are key. The segment benefits from strong consumer preference for ceramic and porcelain tiles due to their durability, low maintenance, and cost-effectiveness compared to natural stone or vinyl flooring. Additionally, increasing investments in energy-efficient and sustainable housing drive demand for eco-friendly, low-VOC adhesives that align with green building standards. Rapid urbanization and the surge in DIY home improvement projects in developed economies also contribute to consistent growth in this segment. As disposable incomes rise and home renovation cycles shorten, the residential market will continue to dominate global adhesive consumption volumes.

The Commercial Construction segment is a critical value-driven contributor to the ceramic adhesives market, encompassing hotels, hospitals, shopping complexes, offices, and transportation hubs. This segment is characterized by stringent performance specifications, as adhesives must endure heavy foot traffic, mechanical loads, and frequent cleaning cycles. Commercial projects often employ large-format tiles (LFTs), stone-look ceramics, and composite surfaces, necessitating adhesives with high flexibility, crack-bridging ability, and strong substrate compatibility. The adoption of polymer-modified cementitious adhesives, reactive epoxies, and deformable thin-set mortars is high in this sector. Moreover, the ongoing global shift toward sustainable infrastructure and smart buildings is driving the preference for high-durability, low-emission adhesive systems that reduce maintenance costs and environmental impact. As large-scale construction projects expand in regions such as the Middle East, India, and Southeast Asia, commercial construction will remain a major driver of advanced adhesive technologies in the years ahead.

The Industrial and Infrastructure segments form a specialized but strategically important part of the ceramic adhesives industry. Industrial facilities—such as manufacturing plants, chemical factories, food processing units, and pharmaceutical cleanrooms—demand adhesives that provide exceptional chemical resistance, compressive strength, and tolerance to temperature and vibration extremes. Epoxy and hybrid systems dominate here, enabling long-term adhesion in harsh operational environments. Meanwhile, the Infrastructure segment includes public buildings, transport terminals, bridges, subways, and tunnels, where the adhesive must withstand heavy loads, environmental exposure, and water ingress. These high-durability requirements have led to increasing adoption of flexible, high-bond strength, and rapid-setting adhesive formulations, particularly for large-format or non-porous tiles. Moreover, government-driven infrastructure programs—especially in Asia-Pacific and the Middle East—are boosting consumption in this segment.

The ceramic adhesives market remains dominated by five multinational manufacturers—Mapei, Sika Corporation, Saint-Gobain Weber, H.B. Fuller, and Bostik (Arkema Group)—each leveraging distinct strengths in polymer chemistry, R&D infrastructure, and integrated tiling system solutions. Their focus areas span cementitious, dispersion-based, and epoxy reaction resin adhesives, with an emphasis on green chemistry and automation-ready formulations.

Mapei commands a leading position in polymer-modified tile adhesive systems, offering products across the C2TES1 and S2 categories for large-format and flexible applications. The 2025 launch of Keraflex S1 Evolution Zero—a low-carbon, recycled-content adhesive—strengthens Mapei’s eco-sustainability profile under its Zero Line initiative. Its products are trusted for high-deformation façade tiling, underfloor heating systems, and heavy-duty commercial flooring, proven in landmark projects like metro lines and the Mont Blanc SkyWay. Mapei’s system integration approach—covering substrate preparation, waterproofing, adhesives, and grouts—ensures seamless performance and compliance for professional contractors.

Sika Corporation continues to advance polymer-modified cementitious adhesives through its SikaCeram series, tailored for facades, swimming pools, and industrial flooring. Flagship products such as SikaCeram FLX 25 provide superior deformability and adhesion for large-format porcelain and natural stone tiles, particularly in hot and humid climates. The company’s global strategy centers on acquisitions to expand regional production facilities and supply networks, ensuring local manufacturing resilience. With a strong reputation for multi-surface compatibility—including drywall, existing tile, and lightweight panels—Sika is a preferred partner for renovation and façade modernization projects.

Saint-Gobain Weber specializes in cementitious tile adhesives designed for residential and commercial construction, emphasizing long-term adhesion, flexibility, and waterproofing integration. Through its Weber Academy, the company prioritizes installer training in emerging markets to ensure correct specification of high-flexibility adhesives for wet rooms, pools, and balconies. Its solutions align with ISO and EN standards, promoting confidence among contractors. Leveraging its strong industrial base across Asia-Pacific and the Middle East, Weber provides cost-efficient, high-quality adhesives suited for fast-growing construction markets.

H.B. Fuller brings deep expertise in epoxy-based reaction resin adhesives and specialty bonding systems for high-performance flooring and structural tiling. The company’s R&D centers emphasize reactive resin systems, instant adhesives, and hot-melt technologies, which it increasingly applies to prefabricated and modular building applications. In April 2025, H.B. Fuller expanded its Southeast Asian operations to strengthen local availability of specialty construction adhesives. Its focus on sustainable and rapid-curing technologies aligns with global construction demands for productivity and green compliance.

Bostik, under Arkema Group, leverages its parent company’s expertise in advanced polymer chemistry to develop cementitious and dispersion-based tile adhesives with enhanced flexibility and workability. The company’s R&D prioritizes low-VOC, water-based acrylics to comply with global green building codes and indoor air quality standards. Bostik’s adhesives are optimized for moisture-sensitive substrates and rapid renovation environments, ensuring strong performance in both residential and commercial installations. The synergy with Arkema’s specialty polymer portfolio enhances Bostik’s competitive edge in high-performance polymer-modified tile mortars.

The U.S. ceramic adhesives market remains resilient, driven by a booming renovation and remodeling sector and a shift toward high-end architectural finishes. Residential construction alone exceeded $853 billion in 2023, creating steady demand for polymer-modified cementitious adhesives used in large-scale remodeling and commercial refits. The rise of large-format tiles and slabs in premium interiors has accelerated the need for non-sag, flexible, high-grab adhesives, capable of preventing cracking, delamination, and substrate stress.

Market dynamics are evolving under the influence of tariff changes and supply chain diversification, prompting manufacturers to increase domestic R&D and localized sourcing of bonding agents. Companies like H.B. Fuller and MAPEI Corporation are expanding production footprints to serve North American clients with regionally optimized, low-VOC tile adhesives. Furthermore, the EPA’s enhanced indoor air standards and LEED-compliant construction codes continue to drive eco-friendly formulations. The U.S. market is shifting toward next-generation lightweight, polymer-rich adhesives engineered for high bond strength, flexibility, and sustainability across residential, healthcare, and institutional projects.

Germany stands as a central pillar of Europe’s ceramic adhesives and construction chemicals market, backed by strict energy performance legislation and sustainability leadership. The Energy Performance of Buildings Directive (EPBD) and surging renovation activity are fueling demand for high-efficiency tile adhesives compatible with thermal insulation and radiant heating systems. Rising energy prices are prompting widespread adoption of high-flex, low-shrinkage polymer adhesives, crucial for retrofits and complex substrates in residential and commercial projects.

Simultaneously, Germany’s skilled trades are evolving—installers are expected to manage multifunctional home improvement tasks, combining tile installation with sustainability upgrades like underfloor heating and heat pump integration. The has increased the preference for versatile, multi-purpose ceramic adhesives that deliver strength, elasticity, and ease of use. The nation’s strong alignment with EU Green Deal objectives and a growing preference for bio-based and recyclable adhesives reinforce its role as a hub for sustainable innovation in ceramic bonding technologies.

Egypt is quickly emerging as a key production hub in the Middle East and Africa (MEA) ceramic adhesives industry, driven by substantial investments in construction materials manufacturing. In early 2025, Mapei inaugurated a state-of-the-art production plant in Egypt to meet surging demand for locally produced tile adhesives, grouts, and waterproofing solutions, supporting large infrastructure projects across North Africa and the Middle East. The strategic expansion enhances regional supply resilience and reduces import dependency for critical construction chemicals.

Additionally, domestic leaders like Al Omaraa – La Beauté are investing in powder adhesive production systems, adding value to Egypt’s ceramic tile ecosystem. The country’s massive investments in urban megaprojects such as New Administrative Capital and infrastructure corridors are creating strong demand for high-strength, weather-resistant ceramic adhesives tailored to high-temperature and heavy-use environments. Egypt’s emergence as a manufacturing and export hub underscores its growing influence in the global construction adhesives supply chain.

Italy remains synonymous with premium tile design and high-performance adhesive systems, driven by constant innovation from leading domestic brands. In 2024, Kerakoll launched H40 Advanced Gel Tile Adhesive, a flexible, rapid-setting, thixotropic gel-based formulation designed for universal substrates, representing a leap in performance versatility and curing speed. Italian adhesive producers consistently push the boundaries of aesthetics and function, catering to luxury interiors, designer finishes, and large-format porcelain installations.

The Italian market’s alignment with global sustainable construction trends promotes low-emission, water-based adhesive formulations. Furthermore, Italy’s dominance in ceramic manufacturing and design exports sustains its position as a technology originator in color-matched, epoxy-modified, and rapid-bond tile adhesive systems. Italian companies also emphasize user-friendly packaging, extended pot life, and quick installation, aligning product innovation with evolving installer preferences in Europe’s renovation-heavy building landscape.

Switzerland plays a leading role in advanced formulation development within the global ceramic adhesives market, spearheaded by Sika AG’s pioneering innovations. In 2024, Sika launched SikaCeram-50 BH, a premixed one-pack cementitious tile adhesive that requires only water addition, simplifying logistics and reducing on-site errors. The innovation is particularly beneficial for large-scale commercial and residential ceramic installations, where productivity and consistent performance are paramount.

Aligned with Europe’s rigorous sustainability and indoor air quality standards, Sika continues heavy R&D investment in low-VOC, polymer-modified adhesives that reduce environmental impact without compromising on adhesion strength or flexibility. The company’s focus on energy-efficient production and bio-based additives demonstrates Switzerland’s commitment to eco-responsible construction chemicals, further positioning it as a hub for sustainable materials innovation.

Ceramic Adhesives Market Report Scope

Ceramic Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.7 Billion

|

|

Market Size (2034)

|

$26.1 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Chemistry Type (Cementitious Adhesives, Epoxy Adhesives, Acrylic Adhesives, Polyurethane Adhesives, Silane-Modified Polymers, Cyanoacrylate Adhesives), By Product Form (Powder/Dry-Mix Adhesives, Ready-Mix/Paste Adhesives, Liquid Adhesives), By Tile Type (Ceramic Tiles, Porcelain Tiles, Large Format Tiles, Natural Stone Tiles, Mosaic and Glass Tiles), By Construction Type (New Construction, Repairs & Renovation), By End-User (Residential Construction, Commercial Construction, Industrial Facilities, Infrastructure), By Application Method (Thin-Set Mortar Application, Medium-Bed Mortar Application, Thick-Bed Mortar Application, Trowel Application, Caulking Gun Application, Spray Application), By Functionality (Standard-Set Adhesives, Rapid-Set Adhesives, High-Performance Adhesives, Waterproof Adhesives, Low-Dust Adhesives, Low-VOC Adhesives

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mapei S.p.A., Sika AG, Henkel AG & Co. KGaA, Bostik, LATICRETE International, Inc., Saint-Gobain Weber S.A., BASF SE, Pidilite Industries Ltd., ARDEX GmbH, ParexGroup SA, H.B. Fuller Company, Fosroc International Limited, Kerakoll S.p.A., Davco Construction Materials, Nuvoco Vistas Corp. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry Type

- Cementitious Adhesives

- Epoxy Adhesives

- Acrylic Adhesives

- Polyurethane Adhesives

- Silane-Modified Polymers

- Cyanoacrylate Adhesives

By Product Form

- Powder/Dry-Mix Adhesives

- Ready-Mix/Paste Adhesives

- Liquid Adhesives

By Tile Type

- Ceramic Tiles

- Porcelain Tiles

- Large Format Tiles

- Natural Stone Tiles

- Mosaic and Glass Tiles

By Construction Type

- New Construction

- Repairs & Renovation

By End-Use Sector

- Residential Construction

- Commercial Construction

- Industrial Facilities

- Infrastructure

By Application Method

- Thin-Set Mortar Application

- Medium-Bed Mortar Application

- Thick-Bed Mortar Application

- Trowel Application

- Caulking Gun Application

- Spray Application

By Functionality

- Standard-Set Adhesives

- Rapid-Set Adhesives

- High-Performance Adhesives

- Waterproof Adhesives

- Low-Dust Adhesives

- Low-VOC Adhesives

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Mapei S.p.A.

- Sika AG

- Henkel AG & Co. KGaA

- Bostik

- LATICRETE International, Inc.

- Saint-Gobain Weber S.A.

- BASF SE

- Pidilite Industries Ltd.

- ARDEX GmbH

- ParexGroup SA

- H.B. Fuller Company

- Fosroc International Limited

- Kerakoll S.p.A.

- Davco Construction Materials

- Nuvoco Vistas Corp. Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Ceramic Adhesives Market with a focus on the transition toward polymer-modified, low-VOC, and gel-technology systems that enable large-format and thin-panel installations. It delivers analysis reviews of demand drivers, regulatory impacts, and technology roadmaps; highlights performance benchmarks (deformability, open time, non-sag behavior, chemical resistance); and maps capacity additions and product pipelines that signal the next breakthroughs in cementitious, dispersion, and reaction-resin chemistries. Leveraging standardized testing frameworks (e.g., EN 12004 classes) and installer productivity metrics, the study quantifies value creation in residential, commercial, industrial, and infrastructure projects while clarifying where rapid-set, high-grab, and ultra-flexible adhesives outperform legacy mixes. By integrating lifecycle and IAQ considerations with procurement-ready insights, this report is an essential resource for manufacturers, formulators, distributors, contractors, architects, and specifiers seeking fact-based guidance on product design, portfolio positioning, and market entry strategy across priority regions.

Scope Highlights

Segmentation:

- By Chemistry Type: Cementitious Adhesives; Epoxy Adhesives; Acrylic Adhesives; Polyurethane Adhesives; Silane-Modified Polymers; Cyanoacrylate Adhesives.

- By Product Form: Powder/Dry-Mix Adhesives; Ready-Mix/Paste Adhesives; Liquid Adhesives.

- By Tile Type: Ceramic Tiles; Porcelain Tiles; Large Format Tiles; Natural Stone Tiles; Mosaic & Glass Tiles.

- By Construction Type: New Construction; Repairs & Renovation.

- By End-Use Sector: Residential Construction; Commercial Construction; Industrial Facilities; Infrastructure.

- By Application Method: Thin-Set Mortar; Medium-Bed Mortar; Thick-Bed Mortar; Trowel Application; Caulking Gun Application; Spray Application.

- By Functionality: Standard-Set; Rapid-Set; High-Performance; Waterproof; Low-Dust; Low-VOC.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034 with market sizing, growth rates, and technology adoption outlook.

Companies: Analysis/profiles of 15+ companies covering strategy, innovation pipelines, regional footprints, and product benchmarking.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.