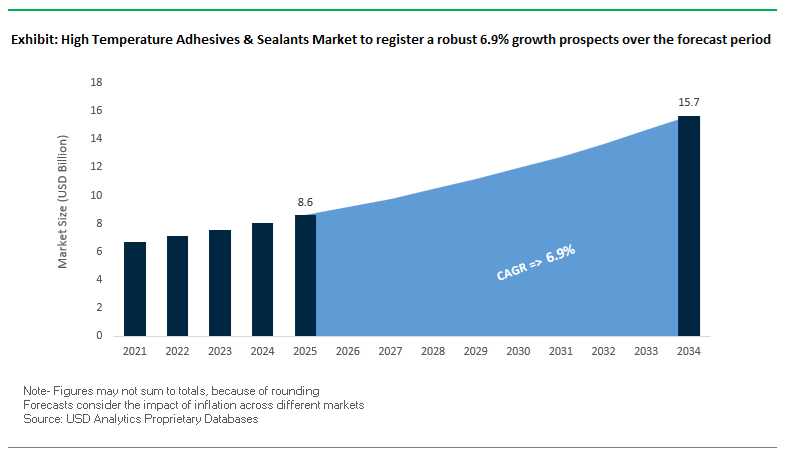

The Global High Temperature Adhesives and Sealants Market is projected to expand from USD 8.6 billion in 2025 to USD 15.7 billion by 2034, advancing at a CAGR of 6.9%, as adhesive and sealing materials move into continuous-service thermal regimes above 250°C that were previously dominated by mechanical fastening, welding, and gasketing solutions. Growth is structurally anchored in aerospace, defense, automotive electrification, power electronics, and high-performance industrial equipment, where assemblies are exposed to sustained heat, oxidative environments, vibration, and aggressive chemicals. In these applications, failure is not cosmetic—it directly affects safety, uptime, and certification—making adhesive selection a design-critical engineering decision rather than a procurement-driven choice.

Further, manufacturers such as Henkel, 3M, Dow, Huntsman, Parker Lord, and Momentive are advancing polyimide, specialty epoxy, silicone, and hybrid systems engineered for extreme thermal stability. Aerospace-grade polyimide and epoxy formulations qualified for structural bonding are designed to maintain mechanical integrity beyond 260°C (500°F), enabling use in jet engine compartments, composite airframes, and propulsion-adjacent assemblies where thermal cycling and oxidation are unavoidable. In parallel, electronics and semiconductor manufacturers are increasingly specifying high-temperature acrylic adhesive transfer tapes that can withstand lead-free solder reflow temperatures approaching 280°C without shrinkage, loss of peel strength, or dielectric degradation—supporting advanced PCB assembly, 5G module bonding, and display lamination under tightly controlled tolerances.

Electrification is adding a new demand layer centered on thermal containment and environmental sealing. In EV battery packs, motors, and inverters, high-temperature silicone and polyurethane sealants are being deployed to deliver combined thermal resistance, electrical insulation, flame retardancy, and ingress protection up to IP68, while remaining compatible with automated liquid-dispense processes and future module disassembly. At the same time, thermal oxidation resistance has emerged as a governing performance parameter, as oxygen exposure can accelerate adhesive degradation by multiple factors at elevated temperatures. This has driven innovation in epoxy-phenolic hybrids and oxygen-stable formulations for long-duration exposure above 260°C. Overlaying these performance requirements is a clear manufacturing imperative: UV- and thermally cured systems capable of achieving functional bond strength in under 15 seconds are increasingly specified in EV and electronics production lines to maintain takt time without compromising reliability.

The high temperature adhesives and sealants market is undergoing a phase of rapid technological refinement driven by sustainability regulations, energy transition applications, and electric mobility expansion. In October 2025, Huntsman Advanced Materials launched a new ARALDITE® epoxy range free from Bisphenol A (BPA) and CMR-classified chemicals, marking a pivotal shift toward safer, regulation-ready structural adhesives for the transportation and industrial segments. Simultaneously, Huntsman introduced PCR-based packaging for ARALDITE cartridges, achieving a 36% reduction in CO₂ emissions, reinforcing the circular economy in adhesive packaging.

In October 2025, Meridian Adhesives Group, under its EPO-TEK® brand, launched 353NDP, a next-generation high-temperature epoxy tailored for electronic and optical assembly. Engineered to enhance thermal cycling reliability and resist delamination, the product addresses connectivity and performance requirements in semiconductors, photonics, and aerospace electronics. Earlier in July 2025, Meridian expanded its technical leadership by appointing a new Global Technical Director for Electronics, emphasizing its growing investment in specialty adhesive R&D.

Henkel AG & Co. KGaA, in August 2025, announced major expansions of its Battery Engineering Centers (BECs) in the USA and China, focusing on developing advanced EV sealing, gap-filling, and adhesive solutions optimized for high-throughput battery module manufacturing. These centers complement the earlier May 2023 launch of Loctite TLB 9300 APSi, a thermally conductive polyurethane adhesive with a conductivity of 3W/mK, enabling improved battery cooling system integration.

In June 2025, Meridian strengthened its Asia-Pacific presence by inaugurating a new Penang Application Development Center, supporting local R&D for high-reliability electronic assembly adhesives. This follows its January 2025 acquisition of PAS Bangkok Co., Ltd., strategically enhancing its supply chain in Southeast Asia.

Meanwhile, 3M and Henkel continued to push boundaries in healthcare and industrial-grade adhesives. 3M’s February 2023 launch of a 28-day wear medical adhesive and Henkel’s November 2023 IBOA-free medical adhesive illustrate the cross-industry adoption of temperature-resilient, skin-safe adhesive chemistries for long-term use in both clinical and industrial environments.

The push to achieve bonding reliability under ultra-high temperatures is transforming the High Temperature Adhesives Market, with the spotlight firmly on ceramic-filled and inorganic adhesive systems. Traditional organic polymers typically degrade at 250°C to 400°C, limiting their application in aerospace, foundry, and energy generation sectors. To overcome the, manufacturers are transitioning to Zirconia and Alumina-based ceramic adhesives that deliver exceptional performance well beyond these thermal limits.

Specialized Zirconia-based adhesives demonstrate continuous service capabilities exceeding 2,200°C (3,992°F), a temperature range suitable for joining ceramics, metals, and refractory materials in turbine and metallurgical applications. Academic breakthroughs in aluminum phosphate adhesives have achieved remarkable bonding strengths of 67.2 MPa at 1,500°C, even after extended thermal cycling—making them ideal for high-stress ceramic-to-ceramic joining in aerospace or defense components. In addition, Alumina-filled adhesive systems maintain superior dielectric strength at up to 1,530°C, offering both thermal and electrical insulation essential for power electronics, instrumentation housings, and high-voltage energy systems.

The move toward inorganic, ceramic-based sealants represents a structural shift in materials science, aligning with industries that demand high-temperature stability coupled with electrical resistance. These advanced formulations are increasingly used in semiconductor equipment, gas turbines, heat exchangers, and plasma-resistant chambers, marking a pivotal evolution in extreme environment bonding technology and setting the foundation for the next generation of high-temperature structural materials.

The aerospace adhesives and sealants market is witnessing a decisive transformation through the adoption of Polyimides (PI) and Bismaleimides (BMI)—high-performance thermosets engineered for lightweight, high-temperature-resistant structures. The industry’s push for greater fuel efficiency and lightweighting in aircraft and spacecraft demands adhesives that can withstand continuous exposure to temperatures between 250°C and 300°C without degradation.

Advanced Polyimide adhesives are co-developed with aerospace-grade resins and are qualified to retain a high proportion of their original flexural strength for over 5,000 hours at 250°C and 1,000 hours at 300°C. The exceptional durability provides thermo-oxidative stability critical to jet engine housings, turbine blades, and airframe bonding. Likewise, Epoxy-modified BMI structural adhesive films have achieved shear strengths of 17.3 MPa at 200°C when applied to carbon fiber reinforced polymer (CFRP) substrates, validating their role in next-generation composite bonding applications for high-speed, high-heat aerospace systems.

In manufacturing innovation, addition-type polyimide adhesives—which cure without releasing volatile by-products—are revolutionizing aerospace production by enabling void-free bond lines. The advancement not only reduces the risk of delamination under flight-induced vibration and temperature fluctuations but also minimizes inspection costs in critical aerospace assemblies.

The rapid expansion of the Electric Vehicle (EV) and e-mobility industry is creating an enormous growth avenue for high-temperature thermally conductive adhesives (TCAs) and sealants engineered for battery pack assembly, power modules, and inverter integration. As EV architectures become more compact and energy-dense, efficient thermal management becomes essential to prevent overheating and enhance battery life.

Conventional adhesives typically offer thermal conductivities around 0.3 W/m·K, whereas next-generation TCAs designed for EV applications achieve 1–5 W/m·K or higher, ensuring rapid heat dissipation to cooling plates and module surfaces. These adhesives double as structural bonding materials, providing both mechanical strength and vibration dampening over operational ranges from −40°C to 150°C, thus ensuring the stability and longevity of sensitive lithium-ion or solid-state cells.

Further, sustainability is being integrated into adhesive design. Emerging silicone-free, silyl-modified polymer (SMP) gap fillers combine high thermal conductivity with easy disassembly properties, allowing end-of-life EV batteries to be more efficiently dismantled for recycling. The innovation not only enhances performance during use but also supports EV circular economy initiatives, ensuring compliance with global sustainability mandates. The intersection of thermal efficiency, structural reliability, and recyclability positions high-temperature EV adhesives as a cornerstone technology for the next decade of electrification and clean transport.

The expansion of renewable energy infrastructure—particularly Concentrated Solar Power (CSP) and Thermal Energy Storage (TES) systems—represents a high-value frontier for high-temperature adhesives and sealants. These materials are vital for the assembly, sealing, and insulation of systems exposed to temperatures exceeding 700°C, where mechanical durability and chemical stability directly determine system efficiency and lifespan.

Next-generation solar power tower systems are being engineered to operate at receiver temperatures above 1,000 K (727°C), necessitating thermal shock-resistant sealants for receiver panels, molten salt containment vessels, and high-pressure heat exchangers. In a prominent example, the completion of heliostat installations for a 100 MW CSP hybrid pilot project in China showcases the industrial-scale application of high-performance sealants in reflective assemblies and high-enthalpy systems.

Further, government policies and incentives are accelerating R&D in advanced high-temperature materials. For instance, the National Policy on Geothermal Energy promotes exploration of hot rock and high-enthalpy resources, which directly overlaps with the adhesive technologies used in CSP and geothermal plants. These adhesives must maintain structural integrity, chemical inertness, and sealing efficiency up to 200°C and beyond, ensuring leak-free performance under cyclic thermal and mechanical stress.

With global renewable energy capacity rapidly expanding, the integration of CSP sealants, high-temperature jointing compounds, and corrosion-resistant adhesives into solar and geothermal infrastructure offers a lucrative market opportunity. These products are indispensable for achieving sustainable, efficient, and maintenance-free renewable energy generation systems, reinforcing the role of the High Temperature Adhesives Market in the global transition to clean energy.

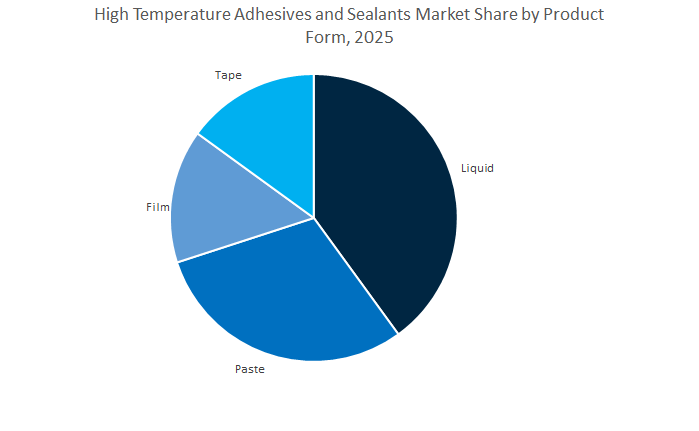

High Temperature Adhesives & Sealants Market Share Insights, 2025-2034

Liquid high-temperature adhesives hold the largest share at 40.9% in 2025, owing to their dispensing versatility (spray, bead, jet), automated metering compatibility, and uniform coverage on complex geometries across metals, ceramics, and composites. Liquids enable thin, consistent bondlines with controlled rheology for under-hood, turbine, and furnace assemblies where thermal cycling and vibration are severe. Pastes retain a strong presence where gap-filling, non-sag, and vertical hold are essential—think engine housings, refractory joints, and structural seams—providing creep resistance under sustained heat. Films and tapes serve engineered applications, notably aerospace composite layups, heat shields, and electronic thermal interfaces—where pre-defined thickness, FST/UL compliance, clean handling, and instant fixturing outweigh material cost.

Aerospace & defense leads with a projected 29.4% share in 2025, reflecting the sector’s extreme service temperatures, oxidation resistance, and fatigue durability requirements in engines, thermal shields, and advanced composite bonding. Electrical & electronics is accelerating on the back of power electronics, wide-bandgap semiconductors, and LED/mini-LED displays, where adhesives must combine dielectric stability, thermal conductivity, and reflow survivability. Automotive & transportation expands with EV battery packs, e-motors, and under-hood components, prioritizing thermal stability, flame retardance, and structural integrity to replace fasteners and reduce mass. Industrial/power generation and building & construction sustain steady demand for furnace linings, high-temp piping, fire-rated joints, and façade/fire-stopping systems, where long-term heat and fire performance are paramount. Medical devices & instruments, while smaller, deliver high value—sterilization-resistant bonds, biocompatibility, and dimensional stability for equipment exposed to autoclave cycles and cautery heat.

The global competitive landscape is defined by R&D-intensive leaders such as Henkel, 3M, Huntsman, H.B. Fuller, and Dow, each leveraging material expertise in polyimides, silicones, and epoxy hybrids to serve aerospace, EV, electronics, and industrial markets. These companies are setting new standards in sustainability, process efficiency, and performance longevity at extreme temperatures.

Henkel continues to dominate the e-mobility and electronics segment, offering resealable gasket systems for EV battery modules approved by major OEMs. The company’s Loctite thermally conductive adhesives feature 3.0 W/mK conductivity and are silicone-free, preventing migration issues in sensitive electronics. Its solvent-free polyurethane adhesive systems cure at room temperature, helping customers reduce energy usage and manufacturing emissions. Henkel’s ongoing global expansion of Battery Engineering Centers (BECs) underlines its strategy to lead in high-temperature EV applications.

3M remains a global frontrunner with products like the 3M™ Ultra High Temperature Acrylic Adhesive Transfer Tape 9085, capable of 280°C short-term resistance for solder reflow environments. Its VHB™ and Scotch-Weld™ product lines deliver reliable bonding under extreme vibration, thermal stress, and reflow cycles, making them ideal for flexible printed circuits (FPCs), automotive under-hood components, and industrial assemblies. The company’s innovations also target low outgassing for cleanroom and semiconductor use, strengthening its dominance in thermal and electronic assembly applications.

Huntsman’s ARALDITE® line remains synonymous with high-performance structural bonding across aerospace, automotive, and industrial markets. Its new BPA-free and non-CMR epoxy adhesives enhance worker safety and environmental compliance, while delivering up to 75% weight savings over mechanical fastening. The company’s MDI-based polyurethane chemistries also advance lightweighting for EVs and transportation, supporting thermal durability and fuel efficiency.

H.B. Fuller maintains a strong presence across industrial, medical, and electronics adhesives, emphasizing biocompatible and climate-resistant hot melts. Its Swift Melt 1515-I is a regionally compliant, heat- and humidity-resistant adhesive tailored for medical tapes in tropical markets. The company’s broad epoxy, silicone, and polyurethane portfolio addresses harsh-environment assembly, and ongoing expansion in Asia-Pacific supports high-growth opportunities in renewable energy and clean transportation sectors.

Dow leads the silicone segment with sealants capable of −50°C to +250°C service ranges, used in industrial ovens, energy infrastructure, and high-heat enclosures. Its formulations deliver superior UV, oxidation, and chemical resistance, extending product lifespans in power generation and construction applications. Dow’s silicone-based coatings also offer thermal insulation and electrical protection, critical for high-power electronics and EV modules. Its infrastructure solutions support thermal flexibility and energy-efficient building envelopes.

The United States high-temperature adhesives and sealants market is witnessing robust growth, propelled by next-generation polymer innovation, electrification of transportation, and aerospace engineering advancements. Companies are emphasizing thermal performance, lightweighting, and compliance with environmental standards, positioning the U.S. as a hub for cutting-edge adhesive technologies.

Dow Inc. launched its VORATRON™ MA 8200S series, a thermal-elastic adhesive line designed specifically for electric vehicle (EV) battery pack assembly, enhancing vibration resistance and safety in high-temperature operating environments. Meanwhile, 3M Company continues to lead with high-strength structural adhesives that enable multi-material bonding in aerospace, EV, and defense applications—critical to weight reduction and performance efficiency. The acquisition of ND Industries Inc. by H.B. Fuller in 2024 significantly strengthened its footprint in aerospace and automotive assembly adhesives, while expanding capabilities in fastener sealing and locking solutions.

Additionally, Department of Energy (DOE) initiatives under the Advanced Manufacturing Office are funding R&D for thermal interface materials (TIMs) and high-temperature sealants that optimize energy storage and hydrogen fuel cell performance. Master Bond Inc. has introduced specialized epoxy systems capable of withstanding up to 300°C, widely applied in medical devices, electronics, and aerospace instrumentation. Growing adoption of low-outgassing, thermally conductive adhesives also supports the semiconductor sector, where adhesives must maintain bond strength and thermal stability during high-temperature reflow processes.

China continues to dominate the Asia-Pacific high-temperature adhesives and sealants market, driven by policy incentives, large-scale infrastructure projects, and rapid industrial capacity expansion. The country’s New Energy Vehicle (NEV) program, supported by extensive subsidies and tax exemptions, has spurred massive adhesive demand for battery-to-chassis bonding, thermal insulation, and safety sealing applications.

China’s EV production—representing nearly 60% of global EV output in 2023—has created strong domestic demand for thermally conductive gap fillers, flame-retardant structural adhesives, and high-strength potting compounds that can withstand continuous thermal cycling. Simultaneously, state-led investments in high-speed rail and urban infrastructure development are generating sustained need for fire-resistant and elastomeric sealants used in joint movement and structural sealing.

Local manufacturers such as Hubei Huitian Glue Co., Ltd. are increasingly self-reliant, accelerating R&D in automotive-grade high-temperature structural adhesives aligned with national goals for domestic materials independence. The Made in China 2025 initiative further promotes technological self-sufficiency in electronic-grade adhesives, fostering innovation in silicone-based, thermally conductive formulations essential for consumer electronics, battery safety, and advanced manufacturing. China’s combination of policy backing, production capacity, and domestic innovation positions it as the fastest-growing global market for high-temperature adhesives in both mobility and infrastructure sectors.

Germany remains Europe’s engineering and manufacturing powerhouse, with its high-temperature adhesives and sealants market underpinned by precision engineering, automotive electrification, and industrial plant construction. German companies are at the forefront of low-VOC polyurethane, silicone, and ceramic-based adhesive systems designed for long-term durability under extreme conditions.

Henkel AG & Co. KGaA leads innovation with low-VOC, high-durability adhesives tailored for lightweight automotive and EV battery assembly, meeting stringent REACH and EU Green Deal compliance. The company’s advanced structural adhesives are crucial in ensuring both mechanical stability and thermal dissipation within high-voltage battery packs. Meanwhile, CeramTec GmbH drives development in ceramic-based bonding technologies, introducing heat- and chemical-resistant adhesive systems operating above 900°C, specifically for industrial furnaces and aerospace materials.

Germany’s strong industrial manufacturing ecosystem depends on two-component epoxy and silicone systems that resist both high heat and corrosive environments, particularly in petrochemical and power plant applications. The country’s adherence to strict environmental and emission regulations also accelerates the transition toward solvent-free formulations and non-isocyanate polyurethane systems, establishing Germany as a benchmark for sustainable high-performance adhesives in Europe.

Japan’s market for high-temperature adhesives and sealants is anchored by its expertise in automotive engineering, precision electronics, and semiconductor fabrication. The nation’s major manufacturers—Three Bond Co., Ltd., Nitto Denko Corporation, and Shin-Etsu Chemical—are pioneering silicone and epoxy formulations with advanced heat resistance and substrate adaptability for hybrid and electric vehicles.

Japanese automotive OEMs increasingly rely on high-temperature silicone sealants for engine gasketing, under-hood sealing, and powertrain components, valued for thermal stability up to 250°C and excellent resistance to oil and weather exposure. In the electronics sector, specialized potting compounds and encapsulants are essential to protect semiconductors, displays, and integrated circuits from thermal degradation during continuous operation.

Three Bond Co., Ltd. has developed advanced formulations capable of bonding dissimilar substrates exposed to dynamic heat stress, which is crucial for hybrid vehicle systems and miniaturized electronic assemblies. Regulatory compliance under Japan’s Air Pollution Control Act and Chemical Substances Control Law further drives innovation in low-VOC, high-purity adhesive technologies, ensuring safer production and application. The synergy of regulation, R&D, and industrial precision secures Japan’s position as a global leader in high-temperature silicone and hybrid adhesive technologies.

India’s high-temperature adhesives and sealants market is expanding rapidly, supported by infrastructure growth, automotive manufacturing, and construction sector modernization. Sika AG’s new manufacturing and R&D facility in Pune, Maharashtra, demonstrates growing international confidence in India’s potential as a high-value adhesives hub. The plant’s focus on high-performance and temperature-resistant adhesive systems directly aligns with demand from the industrial, automotive, and construction sectors.

Government initiatives like “Make in India” and increased Foreign Direct Investment (FDI) in automotive manufacturing have made India the world’s fifth-largest automobile market, creating surging demand for structural and heat-resistant adhesives across EV battery systems, lightweight components, and internal combustion engine assemblies. Moreover, large-scale infrastructure programs—with projected growth exceeding 6.5% annually through 2030—necessitate durable sealants capable of performing in diverse climatic conditions and heavy-duty applications such as bridges, airports, and metro systems.

The country’s dual emphasis on industrial expansion and sustainable construction practices is driving R&D investments in silicone and polyurethane-based sealants designed to withstand extreme heat, humidity, and mechanical stress. As India continues to urbanize and industrialize, it is emerging as a key regional manufacturing and export base for high-performance adhesive products.

South Korea is establishing itself as a global leader in high-temperature adhesive and sealant innovation, driven by its EV battery, semiconductor, and advanced display industries. Major conglomerates—including LG Energy Solution, Samsung SDI, and SKC Co., Ltd.—are investing heavily in thermal management materials and flame-retardant adhesives for battery module and pack-level applications in electric vehicles.

High-strength polyurethane and silicone laminating adhesives are increasingly integrated into battery casing and module assembly to ensure mechanical stability and fire safety under high thermal loads. Simultaneously, the nation’s dominance in flexible electronics and high-end displays fuels demand for thermally stable, optically clear adhesives (OCAs), essential for bonding layers in OLED screens and micro-LED assemblies.

South Korea’s research ecosystem—supported by public-private partnerships and national funding—focuses on next-generation heat-resistant polymers and encapsulants designed for semiconductor miniaturization and flexible circuits. With its deep expertise in advanced materials and automation, South Korea continues to strengthen its global leadership in thermal-resistant adhesive technologies across electronics, EVs, and clean energy applications.

High Temperature Adhesives & Sealants Market Report Scope

High Temperature Adhesives & Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.6 Billion

|

|

Market Size (2034)

|

$15.7 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Chemistry (Epoxy, Silicone, Polyurethane, Acrylic, Others), By Product Form (Liquid, Paste, Film, Tape), By End-User Industry (Automotive & Transportation, Aerospace & Defense, Electrical & Electronics, Building & Construction, Industrial/Power Generation, Medical Devices & Instruments

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Dow Inc., H.B. Fuller Company, Sika AG, Arkema S.A., Wacker Chemie AG, Huntsman Corporation, Avery Dennison Corporation, Master Bond Inc., PPG Industries, Inc., Three Bond Co. Ltd., Delo Industrial Adhesives LLC, Permabond LLC, Hubei Huitian Glue Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Epoxy

- Silicone

- Polyurethane

- Acrylic

- Others

By Product Form

By End-User Industry/Key Application

- Automotive & Transportation

- Aerospace & Defense

- Electrical & Electronics

- Building & Construction

- Industrial/Power Generation

- Medical Devices & Instruments

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Dow Inc.

- H.B. Fuller Company

- Sika AG

- Arkema S.A.

- Wacker Chemie AG

- Huntsman Corporation

- Avery Dennison Corporation

- Master Bond Inc.

- PPG Industries, Inc.

- Three Bond Co. Ltd.

- Delo Industrial Adhesives LLC

- Permabond LLC

- Hubei Huitian Glue Co., Ltd.

*- List not Exhaustive

Research Coverage

Purpose-built for materials engineers, packaging converters, and strategy leaders, the USDAnalytics study on the High Temperature Adhesives and Sealants Market distills the forces reshaping extreme-temperature bonding across aerospace, electronics, and e-mobility: this report investigates how resin chemistries, filler systems, and curing routes translate into reliability above 250 °C; tracks breakthroughs in ceramic-filled/inorganic systems, low-outgassing films, and rapid UV/thermal cures; analysis reviews regulatory momentum (REACH/FDA), qualification cycles, and line-speed productivity; and highlights oxidation-resistant designs, reflow endurance, IP-rated sealing, and design-for-recyclability in EV packs. Built to inform portfolio bets, plant conversions, and specification roadmaps, this report is an essential resource for CTOs, R&D chemists, application engineers, sourcing and QA teams seeking defensible choices on durability, dielectric stability, flame/smoke/tox performance, and lifecycle economics, etc……

Scope Highlights

Segmentation

- By Chemistry: Epoxy; Silicone; Polyurethane; Acrylic; Others

- By Product Form: Liquid; Paste; Film; Tape

- By End-User Industry / Key Application: Automotive & Transportation; Aerospace & Defense; Electrical & Electronics; Building & Construction; Industrial / Power Generation; Medical Devices & Instruments

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 with forecast outlook 2025–2034.

Companies: 15+ company analyses/profiles included (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.