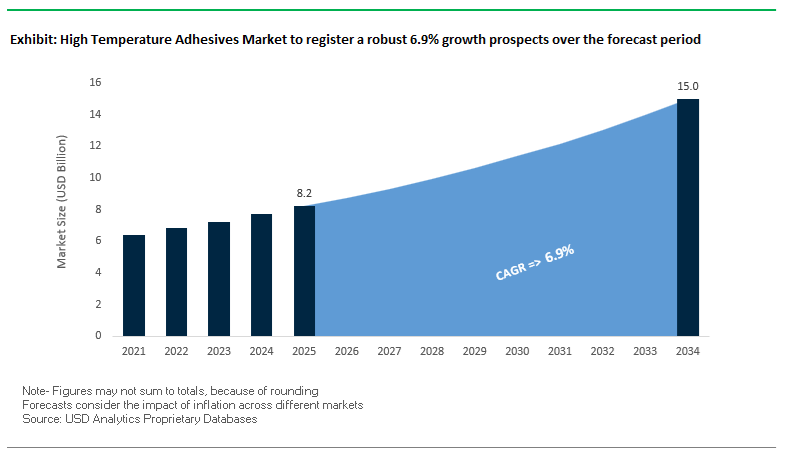

The Global High Temperature Adhesives Market is projected to grow from USD 8.2 billion in 2025 to USD 14.9 billion by 2034, registering a strong CAGR of 6.9%. Growth is fueled by technological advancements in aerospace composite bonding, EV battery module assembly, industrial furnaces, and electronic component encapsulation, where adhesives are replacing mechanical fasteners for improved strength, weight reduction, and durability under sustained high-heat exposure. The industry is characterized by continuous R&D in polyimide, silicone, epoxy, and ceramic-based adhesive chemistries, each offering distinctive advantages across sectors demanding thermal resistance beyond 260°C (500°F).

Aerospace remains a core end-use sector where polyimide adhesives and epoxy hybrids are employed for engine nacelles, composites, and thermal insulation panels capable of tolerating continuous temperatures exceeding 1000°C (1832°F) in ceramic-based formulations. Similarly, EV battery pack designers rely on thermally conductive adhesives (TCAs) rated at ≥3.0 W/mK for cell-to-module bonding and cooling plate attachment, essential for preventing thermal runaway and improving battery safety and longevity.

The automotive and heavy industrial machinery segments are witnessing rapid adoption of silicone and polyurethane adhesives that combine chemical resistance, flexibility, and mechanical integrity at elevated temperatures. These materials ensure reliable sealing and vibration dampening even under exposure to fuel, hydraulic oil, and high-pressure lubricants. On the electronics side, high-temperature acrylic adhesive transfer tapes are critical for lead-free soldering and PCB reflow, offering low outgassing, shear strength retention, and dielectric stability.

The high temperature adhesives market has entered a phase of strategic transformation driven by thermal performance requirements, electrification, and sustainability mandates. In May 2025, a global materials company launched a structural silicone adhesive optimized for high-throughput electronic module assembly, reducing cure time by over 30%—a pivotal advancement for automated electronics manufacturing where precision and cycle efficiency are critical.

Earlier in March 2025, a leading Asian specialty chemicals manufacturer expanded its footprint in Singapore, inaugurating a production line for advanced polyimide adhesive films. These products are engineered for flexible printed circuit boards (FPCBs) and semiconductor packaging, capable of withstanding extreme reflow temperatures and chemical exposure, reinforcing Asia’s dominance in electronics-grade adhesives.

In January 2025, a notable EV adhesive supplier formed a strategic collaboration with a European OEM to co-develop an advanced cell-to-pack adhesive integrating fire-retardant characteristics and achieving a thermal conductivity of 4.0 W/mK—a record-setting parameter for EV safety and energy efficiency. This partnership underscores how adhesive innovation directly correlates with battery safety and lifecycle performance in e-mobility platforms.

In November 2024, an innovation milestone was achieved with a low-temperature curing epoxy (120°C) that retains 230°C continuous service capability, marking a breakthrough for industrial bonding in heat-sensitive assemblies. This was followed by an October 2024 acquisition where a North American chemical firm acquired a European ceramic adhesives company, extending its reach into ultra-high-temperature aerospace and turbine assembly markets.

Further supporting the sustainability narrative, EU regulators (September 2024) enforced new VOC reduction mandates for structural adhesives used in automotive and construction applications, accelerating the industry’s transition to solvent-free and low-VOC epoxy systems.

In parallel, government funding in June 2024 injected $75 million into a U.S. thermal management R&D program developing encapsulants and heat-dissipative adhesives for wide-bandgap (WBG) power electronics—a key enabler for EV inverters and renewable energy systems. These developments highlight how energy transition technologies and environmental regulations are converging to reshape the market’s material innovation trajectory.

High-Heat Material Innovation, Electrification Demands & Fire-Safe Design Requirements

Trend 1: Rising Qualification of Ceramic-Filled & Hybrid High-Temperature Adhesives for Extreme Electrification in Automotive and Aerospace

The rapid expansion of EVs and high-power aerospace systems is driving strong demand for ceramic-filled and hybrid high-temperature adhesives that combine superior bonding strength with highly efficient thermal dissipation. Advanced epoxy TCAs, such as ThreeBond 2045B and 2145B, achieve 2.1 W/m·K thermal conductivity while offering UL94 V-0 flame retardancy—making them ideal for cell-to-module bonding in EV battery packs where heat management and fire resistance are critical. In extreme thermal environments, such as turbine components, propulsion systems, or industrial furnaces, alumina-oxide ceramic adhesives like Resbond® 901 and 903HP deliver continuous heat resistance up to 1,650°C–1,790°C, enabling structural bonding of metals, ceramics, and glass under conditions where polymer-based adhesives fail. Complementary research also shows that alumina-filled formulations can achieve 270 V/mm dielectric strength and volume resistivity of 10¹⁰ Ω·cm, establishing their importance for insulating high-voltage modules, inverters, and e-motors that must withstand increasing thermal loads associated with global electrification.

Trend 2: Adoption of UV/Visible Light-Curing Adhesives for High-Speed Manufacturing in Electronics & Medical Devices

Manufacturers of electronics and medical devices are rapidly transitioning to UV and visible light-curing acrylic adhesives to support automated, ultra-fast production. These formulations enable fixture strength within 1–2 seconds and full cure in under 15 seconds, dramatically reducing assembly times for microelectronics, sensors, and catheter systems. Dual-cure technologies address the historical limitation of UV curing by enabling polymerization in shadowed zones or under opaque components using secondary thermal or moisture-based mechanisms—an essential capability for encapsulation tasks such as “glob top” protection in semiconductors. In smart devices and flexible electronics, UV-tunable optically clear adhesives (OCAs) are engineered for excellent viscoelastic properties and long-term mechanical durability. Their customizable modulus profiles help relieve bending stresses in foldable displays and wearable electronics, supporting the next wave of miniaturized, high-reliability consumer technology.

Opportunities Driven by Circular Manufacturing, Electrification & Fire-Safe Infrastructure

Opportunity 1: Reworkable & Re-usable High-Temperature Adhesives for Satellite, Aerospace & Semiconductor Manufacturing

The extreme cost of component failures in satellites, aerospace electronics, and semiconductor equipment is creating a high-value opportunity for reworkable high-temperature adhesive systems. Next-generation silicone and polyimide adhesives capable of ~260°C continuous heat resistance are being designed for selective debonding, allowing technicians to inspect or replace critical components without damaging high-value substrates such as ceramic boards, wafers, or composite housings. For satellite systems—where repair costs can reach millions—these re-workable HTAs significantly reduce manufacturing and MRO risks. In semiconductor packaging, research is advancing thermally conductive, low-stress adhesives that can be cleaved or solubilized through controlled heat or solvent activation, allowing integrated circuits or heat spreaders to be replaced during equipment refurbishment, improving overall yield and extending equipment lifecycle.

Opportunity 2: High-Temperature Flame-Retardant Adhesives for Electrified Mass Transport & Fire-Safe Infrastructure

As global transit systems electrify, new fire safety mandates such as NFPA 130 and EN 45545 (HL3 rating) are reshaping the demand for high-temperature adhesives with inherent, non-halogenated flame retardancy. Adhesives used in trains, electric buses, and marine cabins must deliver low-smoke, low-toxicity, and self-extinguishing performance while bonding interior panels, battery housings, insulation layers, and floor systems. This regulatory environment is fueling innovation in halogen-free flame-retardant HT adhesives incorporating technologies such as ammonium polyphosphate (APP) and intumescent char-forming additives. These systems activate at elevated temperatures to form a thermally protective carbonaceous layer, drastically improving burn-through resistance in EV enclosures, transit interiors, and marine electrification applications. As fire-safe electrified transport expands worldwide, these advanced HT adhesive formulations are becoming essential components of compliant, high-reliability mass transportation platforms.

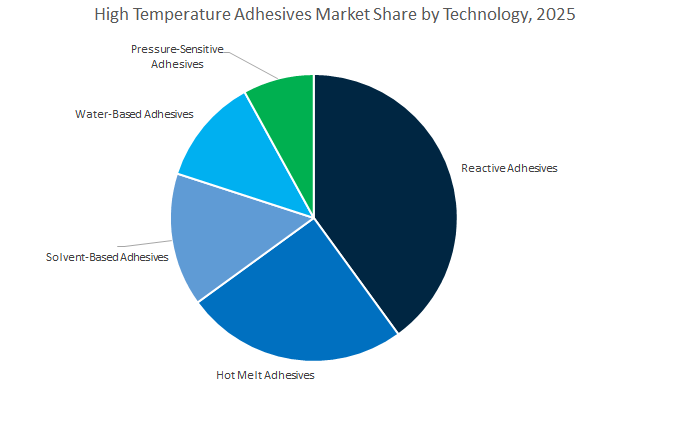

High Temperature Adhesives Market Share Insights, 2025-2034

The reactive adhesives segment commands the largest share of the global high temperature adhesives market, projected at 43.1% in 2025, owing to their exceptional mechanical integrity, chemical resistance, and thermal endurance in extreme environments. Reactive systems—especially epoxies, polyurethanes, and silicones—are the material backbone in aerospace, automotive, and industrial manufacturing where components are exposed to continuous temperatures exceeding 250°C. Their crosslinking cure mechanism yields high cohesive strength, dimensional stability, and sustained adhesion under mechanical stress, making them indispensable in engine compartments, composite structures, and turbine assemblies. As industries intensify their lightweighting, electrification, and high-efficiency design goals, reactive adhesives are increasingly replacing mechanical fasteners and welds to achieve superior strength-to-weight ratios and reduced assembly complexity. Innovations in nano-reinforced and hybrid resin systems are also enabling broader operating temperature windows, driving sustained demand from mission-critical end users seeking high-performance bonding in thermally aggressive settings.

Hot melt adhesives represent a fast-growing segment, benefiting from reactive polyurethane (PUR) and polyamide hot melts that deliver both rapid green strength and thermal resistance. Their solvent-free, high-speed processing advantages make them ideal for automotive interiors, electronics encapsulation, and filter assembly, where productivity and sustainability converge. Solvent-based adhesives, continue to serve specialized applications requiring exceptional substrate wetting and adhesion on metals and composites under high thermal and mechanical loads. Meanwhile, water-based and pressure-sensitive adhesives (PSAs) occupy niche positions where temperature performance must be balanced with flexibility, removability, or comfort, such as in industrial laminates, sensors, and insulation foils.

The aerospace and defense segment leads the global high temperature adhesives market with a projected 28.5% share in 2025, reflecting its stringent requirements for structural integrity, oxidation resistance, and thermal endurance in extreme flight and propulsion environments. Adhesives in this sector are crucial for composite bonding, engine nacelles, thermal shielding, and interior components, where performance failure is unacceptable. The growing adoption of lightweight composite structures and ceramic matrix composites (CMCs) in aircraft manufacturing has amplified the need for high-strength, heat-resistant bonding agents that can sustain thermal cycling, pressure differentials, and jet fuel exposure. Furthermore, defense programs demanding hypersonic materials, missile systems, and stealth composites continue to fuel innovation in silicone, epoxy, and polyimide adhesive systems, reinforcing this segment’s dominant share.

The automotive and transportation segment is experiencing rapid growth, driven by the electrification of vehicles, thermal management in EV battery packs, and lightweight chassis assembly. Adhesives are critical for bonding battery modules, motor components, and under-hood parts, offering resistance to thermal runaway, vibration, and high mechanical loads. As automotive OEMs shift toward metal-polymer hybrid designs and high-temperature curing paints, the demand for high-temperature epoxies, reactive PURs, and silicone-based adhesives has escalated. In the electronics and electrical industry, high-temperature adhesives are increasingly used in semiconductor packaging, PCB protection, power modules, and LED assemblies, where they provide dielectric strength, heat dissipation, and reliability under thermal stress.

The industrial and power generation segments maintain a stable share supported by applications in furnaces, gas turbines, solid oxide fuel cells (SOFCs), and insulation systems, all of which require chemical inertness, creep resistance, and structural stability at extreme operating temperatures. On the other hand, the building and construction segment, though smaller, represents a critical safety-focused domain involving fire-rated sealants, smoke barriers, and structural joints that ensure compliance with stringent fire-resistance and thermal protection standards.

The global high-temperature adhesives industry is led by six core manufacturers—Henkel, 3M, Huntsman, Dow, H.B. Fuller, and PPG Industries—each leveraging domain-specific expertise in structural bonding, e-mobility materials, thermal management, and aerospace-grade formulations. Their collective innovation focus is on extending thermal resistance, reducing cure time, enhancing compliance with VOC/REACH standards, and developing recyclable, solvent-free formulations.

Henkel maintains its position as the global leader in e-mobility adhesive technologies through its Loctite brand, offering thermally conductive, fire-retardant polyurethane and epoxy systems. Its 2025 expansion of R&D centers in China accelerates the development of next-generation thermal management adhesives for EVs. The Loctite TLB 9300 APSi remains a benchmark product with 3.0 W/mK thermal conductivity, enabling efficient heat dissipation and structural bonding in battery modules. Henkel also advances circular economy compliance with recyclable and solvent-free adhesive platforms.

3M continues to dominate through its Ultra High Temperature Adhesive Transfer Tape 9085, offering 280°C resistance for electronics solder reflow. With over 120,000 global patents, 3M’s adhesive division integrates advanced materials science across electronics, automotive, and industrial segments. In Q4 2024, the company launched low-outgassing acrylic foam tapes for automotive under-the-hood and aerospace electronics, offering exceptional vibration and chemical resistance. Its silicone-based adhesives remain vital for flexible circuit and optical assembly where thermal stability and dielectric strength are mandatory.

Huntsman’s Araldite® brand is synonymous with high-strength epoxy systems engineered for aerospace and defense applications. These adhesives provide up to 75% weight reduction versus fasteners, with toughened formulations ensuring impact and fatigue resistance at high temperatures. Huntsman’s innovation pipeline focuses on lightweighting solutions and multi-substrate bonding, integrating polyurethane systems for next-generation transportation. Its continued R&D in non-BPA epoxy chemistries positions the company at the forefront of environmentally compliant aerospace adhesives.

Dow’s DOWSIL™ portfolio remains the industry’s benchmark for silicone-based high-temperature sealants and encapsulants. The DOWSIL™ 736 Heat Resistant Sealant, capable of 260°C continuous and 315°C intermittent service, is widely used in aerospace gasketing and industrial appliances. In Q3 2025, Dow launched silicone encapsulants optimized for thermal cycling durability in solar and power electronics. Its sustainability strategy emphasizes neutral-cure, solvent-less silicone adhesives, catering to electronics and construction sectors seeking long-term thermal stability and low environmental impact.

H.B. Fuller delivers a robust line of reactive polyurethane, epoxy, and hot melt adhesives designed for industrial and medical high-temperature applications. Its Swift® Health biocompatible series ensures sterilization-resistant bonding in medical devices and packaging, while its industrial reactive adhesives provide crosslinking strength for high-pressure sealing in manufacturing and assembly. The company continues to invest in low-VOC and solvent-free solutions, emphasizing regional compliance and sustainable production.

PPG’s Aerospace Products & Services (P&S) division provides epoxy and polyurethane sealants tailored to MIL-SPEC standards, focusing on fuselage, fuel tank, and composite bonding. Its lightweight sealant systems enhance aircraft fuel efficiency and structural integrity. PPG operates multiple Application Support Centers (ASCs) worldwide, ensuring technical compliance, process validation, and customer-specific formulations. The company’s adhesives are crucial for defense and high-performance aerospace programs demanding chemical resistance and extended durability under cyclic thermal stress.

The United States high-temperature adhesives market leads globally in aerospace-grade polymers, thermal interface adhesives, and lightweight automotive bonding systems. A surge in R&D investments by key manufacturers and government agencies is fueling breakthroughs in thermal management materials (TMMs), self-healing composites, and ultra-high-temperature ceramics (UHTCs) for next-generation defense and mobility systems.

Henkel Adhesive Technologies expanded its Brandon, South Dakota facility with a $30 million investment in 2025, boosting production of thermal management materials (TMMs) for EV battery packs and electronics, enhancing North America’s domestic supply resilience. 3M Company continues to dominate the aerospace and advanced materials segment with new structural epoxy systems engineered for lightweight composite bonding and multi-material assemblies in aircraft and defense vehicles.

In high-temperature ceramics, Aremco Products, Inc. is advancing its Ceramabond™ series, capable of withstanding up to 3200°F (1760°C)—ideal for aerospace sensor housings, refractory bonding, and high-vacuum furnaces. Meanwhile, Master Bond’s Supreme 46HTQ epoxy offers exceptional adhesion across metals, ceramics, and composites with cryogenic to +500°F (260°C) temperature stability, making it a top choice for aerospace and oilfield electronics.

The U.S. defense sector, particularly NASA and DARPA, is driving large-scale programs in UHTC-based bonding systems that can endure temperatures beyond 2500°C for hypersonic and reusable vehicle applications. In electronics, Dymax Corporation’s UV-curable Multi-Cure® series introduces hybrid curing technology combining UV/Visible and heat activation for faster throughput in semiconductor and EV electronics assembly.

Germany’s high-temperature adhesives and sealants industry is driven by its leadership in automotive electronics, industrial power systems, and engineering simulation technologies. The nation’s manufacturers are aligning their adhesive innovations with Europe’s Green Deal, emphasizing low-VOC, solvent-free, and recyclable materials that comply with stringent EU chemical safety regulations.

Henkel AG & Co. KGaA continues to advance automotive-grade thermal management and EMI shielding adhesives, including its new electromagnetic interference (EMI) shielding film—a cost-efficient, sustainable alternative to metal housings in complex vehicle electronics. The company’s UL-certified Loctite Stycast US 8000AB potting system demonstrates high thermal stability and durability, ideal for industrial power electronics in extreme environments.

Germany’s R&D centers are leading in digital material validation and simulation, employing digital twin modeling to accelerate adhesive development cycles and predict long-term thermal fatigue in structural bonding applications. Furthermore, Henkel’s eco-efficiency initiatives recovered 435 metric tons of materials and 16,500 drums in 2025, showcasing progress toward circular manufacturing practices for specialty adhesives.

The combination of precision material science, digital innovation, and sustainable process engineering solidifies Germany’s reputation as the European hub for high-temperature adhesive excellence, catering to automotive, electronics, and heavy industrial applications.

China represents the largest Asia-Pacific market for high-temperature adhesives, bolstered by state-led industrial policy, massive EV battery output, and a rapidly expanding semiconductor ecosystem. The Made in China 2025 initiative continues to emphasize materials independence, driving significant investment in silicone, polyimide, and thermally conductive adhesives for both domestic and export markets.

In the aerospace sector, China’s push for indigenous aircraft manufacturing has accelerated the use of polyimide and silicone-based adhesives for composite bonding, nacelle structures, and thermal shielding. The materials are essential for meeting the temperature endurance requirements of domestic programs such as COMAC C919.

The EV battery sector, accounting for 60% of global production in 2023, demands advanced thermally conductive adhesives (TCAs) and gap fillers with high heat dissipation ratings (≥2 W/mK) to optimize battery-to-cooling-plate bonding. Local champions such as CATL and BYD are investing in vertically integrated supply chains for adhesive resins and thermal interface compounds.

China’s rapidly scaling semiconductor and display manufacturing industry drives strong demand for high-temperature die-attach adhesives and encapsulants, which ensure reliability under thermal cycling during reflow soldering. Additionally, the nation’s solar PV expansion fuels the use of UV- and heat-resistant silicone adhesives for panel lamination and junction box sealing, reinforcing China’s dominance in high-temperature adhesive innovation for renewable energy and electronics manufacturing.

Japan remains a global frontrunner in high-temperature adhesive technologies for miniaturized electronics, semiconductor packaging, and flexible displays. Japanese manufacturers are perfecting ultra-thin bond-line adhesives, polyimide-integrated films, and precision dispensing technologies for highly compact and thermally demanding devices.

The trend toward 3D semiconductor packaging has amplified the demand for ultra-thin, thermally conductive materials capable of withstanding high reflow temperatures without delamination. Companies are integrating polyimide (PI) film-based adhesives into flex circuits, under-hood automotive sensors, and display panels, balancing heat tolerance and electrical insulation.

Japanese leaders like Toyo Ink Group’s Toyo-Morton and Nitto Denko Corporation focus on PI and epoxy resin systems designed for flexible printed circuit boards (FPCBs) and wearable microelectronics, where both thermal stability and mechanical flexibility are vital. Furthermore, Japan’s precision dispensing equipment manufacturers are revolutionizing low-viscosity adhesive application for micro-scale assembly, supporting the country’s ongoing leadership in electronics miniaturization and high-temperature packaging technologies.

South Korea’s high-temperature adhesive market is evolving in tandem with its dominance in EV battery production, OLED displays, and advanced electronic materials. The nation’s EV industry, spearheaded by Hyundai Motor Group, LG Energy Solution, and Samsung SDI, relies on flame-retardant epoxy and polyurethane adhesives to ensure battery module stability and thermal propagation resistance in high-voltage assemblies.

The high-performance structural adhesives are essential in securing module-to-pack interfaces while maintaining mechanical strength under thermal shock. Additionally, the country’s OLED and flexible display fabrication ecosystem—led by Samsung Display and LG Display—drives demand for UV-curable, low-outgassing adhesives that can endure high lamination temperatures without yellowing or delamination.

Government-led initiatives in polymeric composites and hydrogen energy components further emphasize heat-resistant and flame-retardant adhesive research, ensuring South Korea maintains its competitive edge in energy-efficient, high-performance adhesive technologies for next-generation electronics and mobility.

France remains a pivotal center for aerospace-grade and high-temperature composite adhesives, driven by Airbus-led projects and a broader European focus on lightweight, thermally stable bonding systems. High-performance epoxy and bismaleimide (BMI) film adhesives are widely used in carbon fiber reinforced polymer (CFRP) structures, enabling superior load-bearing capacity at elevated operational temperatures.

The French market also emphasizes fire-retardant adhesives for rail and transport infrastructure, aligned with EN 45545-2 safety standards. Major suppliers such as Huntsman Corporation and Arkema provide certified phenolic and epoxy systems for rail interior bonding and flooring applications, ensuring compliance with EU fire protection directives.

France’s commitment to industrial decarbonization and advanced composite materials reinforces its role as a European hub for structural adhesives, particularly those designed for high-temperature aerospace, automotive, and rail applications requiring long-term thermal endurance and environmental safety.

High Temperature Adhesives Market Report Scope

High Temperature Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.2 Billion

|

|

Market Size (2034)

|

$14.9 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Resin Type (Silicone Adhesives, Epoxy Adhesives, Polyurethane Adhesives, Polyimide Adhesives, Bismaleimide Adhesives, Ceramic Adhesives, Acrylic Adhesives, Phenolic Adhesives, Cyanacrylate Adhesives), By Technology (Solvent-Based Adhesives, Water-Based Adhesives, Hot Melt Adhesives, Reactive Adhesives, Pressure-Sensitive Adhesives), By Application Method (Liquid Adhesives, Paste/Gel Adhesives, Film Adhesives, Tape Adhesives, Potting and Encapsulation Compounds), By End-Use Industry (Aerospace and Defense, Automotive and Transportation, Electronics and Electrical, Industrial, Power Generation, Building and Construction

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Sika AG, Huntsman Corporation, Master Bond Inc., Dymax Corporation, LORD Corporation, Aremco Products, Inc., The Dow Chemical Company, Permabond LLC, DELO Industrial Adhesives, Shin-Etsu Chemical Co., Ltd., DuPont de Nemours, Inc., BASF SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry/Resin Type

- Silicone Adhesives

- Epoxy Adhesives

- Polyurethane Adhesives

- Polyimide Adhesives

- Bismaleimide Adhesives

- Ceramic Adhesives

- Acrylic Adhesives

- Phenolic Adhesives

- Cyanacrylate Adhesives

By Technology

- Solvent-Based Adhesives

- Water-Based Adhesives

- Hot Melt Adhesives

- Reactive Adhesives

- Pressure-Sensitive Adhesives

By Application Method

- Liquid Adhesives

- Paste/Gel Adhesives

- Film Adhesives

- Tape Adhesives

- Potting and Encapsulation Compounds

By End-Use Industry

- Aerospace and Defense

- Automotive and Transportation

- Electronics and Electrical

- Industrial

- Power Generation

- Building and Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Sika AG

- Huntsman Corporation

- Master Bond Inc.

- Dymax Corporation

- LORD Corporation

- Aremco Products, Inc.

- The Dow Chemical Company

- Permabond LLC

- DELO Industrial Adhesives

- Shin-Etsu Chemical Co., Ltd.

- DuPont de Nemours, Inc.

- BASF SE

*- List not Exhaustive

Research Coverage

Designed for materials leaders and application engineers, the USDAnalytics study on the High Temperature Adhesives Market connects technology choices with mission-critical performance at ≥250 °C: this report investigates where polyimide, silicone, epoxy, ceramic and hybrid systems deliver structural fidelity, dielectric stability, and oxidation resistance in aerospace, EV battery packs, turbines, and high-reliability electronics; maps breakthroughs in ceramic-filled/inorganic chemistries, thermally conductive bonding, and fast-cycle UV/thermal cures; analysis reviews regulatory momentum (REACH/VOC), qualification pathways, and cost-of-ownership levers from cure speed and line productivity; and highlights design-for-safety in thermal runaway mitigation, reflow endurance to 280 °C, and IP-rated sealing for harsh environments—aligning materials science with real factory constraints. Built for strategy, sourcing, QA, and R&D roadmaps, this report is an essential resource for CTOs, process engineers, converters, and investors seeking defensible choices on reliability, compliance, and lifecycle economics, etc……

Scope Highlights

Segmentation

- By Chemistry / Resin Type: Silicone; Epoxy; Polyurethane; Polyimide; Bismaleimide; Ceramic; Acrylic; Phenolic; Cyanoacrylate

- By Technology: Solvent-Based; Water-Based; Hot Melt; Reactive; Pressure-Sensitive

- By Application Method: Liquid; Paste/Gel; Film; Tape; Potting & Encapsulation Compounds

- By End-Use Industry: Aerospace & Defense; Automotive & Transportation; Electronics & Electrical; Industrial; Power Generation; Building & Construction

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.