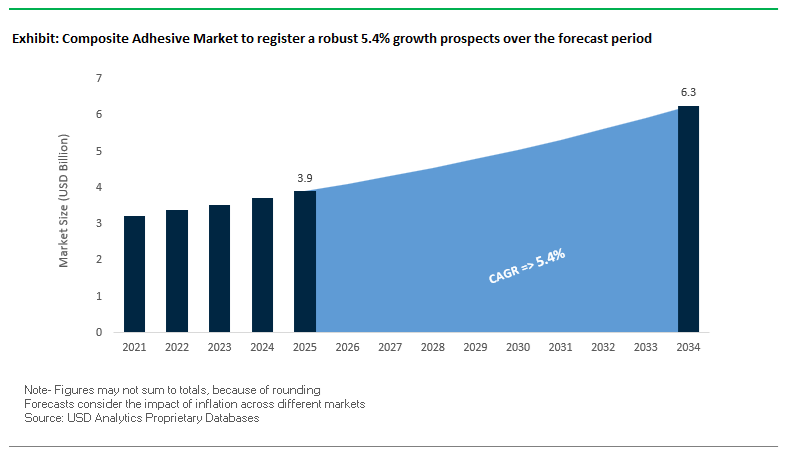

The Global Composite Adhesive Market is projected to grow from $3.9 billion in 2025 to $6.3 billion by 2034, registering a CAGR of 5.4%. Growth is anchored by the accelerated adoption of epoxy, polyurethane, and acrylic resin systems across aerospace, automotive, wind energy, and industrial assembly applications. The demand surge is driven by the industry’s ongoing pursuit of lightweight, high-strength materials, coupled with a growing emphasis on fast-curing, energy-efficient, and sustainable adhesive formulations for composite bonding.

Epoxy adhesives are supported by their superior tensile strength, chemical resistance, and thermal stability. These are critical in aerospace fuselage assembly, marine structures, and oil & gas pipelines, where mechanical reliability is non-negotiable. Meanwhile, the automotive and EV segments are rapidly embracing acrylic and methacrylate-based composite adhesives due to their rapid cure profiles and compatibility with multi-material bonding of carbon fiber, metals, and thermoplastics—essential for battery housing and structural modules in electric vehicles.

The Aerospace & Defense sector remains a premium consumer of composite adhesives, driven by the sector’s focus on lightweighting, high fatigue resistance, and thermal integrity under extreme stress. Furthermore, one-component adhesive systems have emerged as a preferred choice due to their automation-ready application, improved storage stability, and reduced mixing waste, perfectly aligning with Industry 4.0 production environments.

The composite adhesive market has entered a strategic growth phase characterized by corporate consolidation, manufacturing expansions, and sustainability-driven R&D. A wave of mergers and acquisitions since 2023 has reshaped the supply landscape, aligning adhesive producers with high-performance composite applications in aerospace, automotive, and renewable energy.

In November 2024, INX Group Limited completed the acquisition of Coatings & Adhesives Corporation, forming INX International Coatings & Adhesives, expanding its footprint into specialty adhesive products for advanced composite assembly. Similarly, Nippon Paint Holdings Co., Ltd. (NPHD) strengthened its composite materials portfolio in October 2024 through the acquisition of AOC, a leading supplier of composite resins used in construction, transportation, and marine sectors, reinforcing Japan’s presence in global structural bonding solutions.

In August 2024, ATP Adhesive Systems established a new North American production facility in South Carolina, marking a significant investment to serve the growing lightweight bonding needs of automotive and transportation manufacturers, particularly EV assembly plants. Henkel AG & Co. KGaA, in February 2024, continued advancing digital manufacturing via collaboration with the International Centre for Industrial Transformation (INCIT), leveraging analytics to accelerate fast-cure adhesive commercialization and sustainable production.

Sustainability remains a defining market driver. Mitsui Chemicals Inc. achieved ISCC PLUS certification in May 2023 for its epoxy resin chain, demonstrating commitment to biomass-based phenolic feedstocks that reduce reliance on petrochemical inputs. Likewise, 3M’s launch in March 2023 of the Scotch-Weld DP6310NS composite urethane adhesive expanded options for multi-material structural bonding in transportation and industrial machinery, highlighting innovation toward impact-resistant and flexible adhesive systems.

On a macro level, India’s 2023 Union Budget allocation of ₹35,000 crore toward net-zero mobility has accelerated domestic EV manufacturing, propelling composite adhesive demand for battery housing, chassis, and structural lightweighting applications. The trend is reinforced globally by Tesla’s expansion in Markham, Canada, announced in early 2022, where the facility’s focus on EV battery equipment manufacturing underpins regional demand for epoxy and acrylic composite adhesives.

The aerospace sector is at the forefront of adhesive innovation, with a strong focus on high-temperature composite adhesives that can perform reliably under extreme thermal and mechanical stresses. As the next generation of fuel-efficient aircraft and hypersonic vehicles demands higher operational temperatures, bismaleimide (BMI) and toughened epoxy adhesive systems are being rigorously qualified for primary CFRP bonding applications.

Empirical studies have demonstrated that BMI structural adhesive films designed for BMI-based CFRP substrates can achieve a glass transition temperature (Tg) of 208.6°C with an impressive shear strength retention of 17.3 MPa at 200°C. These metrics underscore the adhesive’s resilience in maintaining structural integrity under high-temperature exposure, validating their integration into wing skins, fuselage joints, and engine nacelle structures. Further, toughened BMI resin systems, particularly those reinforced with IM7 carbon fibers, have shown exceptional Compression-After-Impact (CAI) strength retention, even under large damage zones—proving essential for damage-tolerant design in primary load-bearing CFRP assemblies.

Conversely, comparative data on conventional epoxy adhesive systems report a critical performance limitation: mechanical strength reductions of up to 85% at 70°C, emphasizing the need for high-Tg structural adhesives. The drives ongoing R&D into hybrid thermoset formulations capable of withstanding prolonged exposure above 200°C while maintaining cohesive strength. The qualification of these high-modulus epoxy and BMI formulations by major aerospace OEMs not only elevates structural safety but also sets a new benchmark for thermo-mechanical performance in composite bonding systems used in aviation and defense.

The global automotive industry’s pivot toward electric mobility and lightweighting is transforming adhesive design priorities. Modern vehicle architectures rely on multi-material assemblies—combining carbon fiber, glass composites, thermoplastics, and aluminum—to achieve optimal weight reduction and crash durability. As a result, the industry is witnessing widespread adoption of fast-curing composite adhesives that can integrate seamlessly into high-speed assembly lines, replacing slower, heat-cure systems.

Automotive OEMs are increasingly deploying two-part structural adhesives compatible with spot induction curing, a technology that allows for ultra-fast “lock-up” times during Body-in-White (BiW) production. The technique significantly reduces cycle times compared to traditional welding or oven-based curing, aligning with the EV industry’s demand for efficient, low-energy manufacturing. In addition, the use of structural polyurethane and methacrylate adhesives in joining composite-metal interfaces provides superior modal frequency response and weight optimization, as proven in light rail and electric vehicle chassis applications.

With automotive platforms integrating more lightweight polymer and CFRP panels, these advanced adhesives enhance structural integrity, NVH (Noise, Vibration, and Harshness) performance, and design freedom. The transition toward rapid-setting, multi-material adhesives represents a strategic leap toward achieving EV range efficiency, manufacturing productivity, and long-term durability, establishing a dominant growth avenue for the automotive composite adhesive market.

The rapid expansion of the global wind energy market, particularly in offshore installations, has created a massive demand for structural composite adhesives tailored for turbine blade manufacturing and repair. These applications require adhesives with long pot life, high toughness, and environmental resilience, capable of bonding massive epoxy/fiberglass laminates under varying temperature and humidity conditions.

Performance tests (per ASTM D3163) confirm that certain two-component epoxy structural adhesives designed for wind turbine assembly consistently exhibit substrate failure before adhesive failure, proving exceptional bonding strength and load-bearing capacity. Such adhesives are pivotal in achieving aerodynamic efficiency and fatigue resistance in turbine blades exceeding 100 meters in length. Further, two-part methacrylate adhesives are gaining traction for up-tower and field repair operations due to their ability to snap-cure at ambient temperatures and require minimal surface preparation. These features significantly reduce downtime and maintenance costs for wind operators, directly improving the economic viability of renewable installations.

As turbine designs scale up in size, the demand for lightweight, weather-resistant, and high-elongation composite adhesives will surge, reinforcing the sector’s importance as one of the most profitable growth frontiers for composite adhesive manufacturers catering to the renewable energy market.

The global shift toward a circular composite economy has opened significant opportunities for sustainable and recyclable adhesive systems that enable the disassembly and recycling of composite components at end-of-life. Regulatory initiatives—such as the EU Green Deal, REACH, and carbon reduction mandates—are compelling manufacturers to adopt bio-based feedstocks and debonding technologies that align with lifecycle assessment (LCA) criteria and carbon-neutral production goals.

Breakthrough academic research has validated the recyclability of bio-based epoxy adhesives through mild acid-catalyzed disassembly processes, which allow for the recovery of thermoplastic polymers without structural degradation. In parallel, the development of cleavable hardeners that selectively break C–N bonds during low-temperature (∼90°C) solvent-based recycling has enabled the full recovery of high-value carbon fibers and epoxy oligomers, representing a major step toward closed-loop recycling of CFRP structures.

Such innovations directly address the end-of-life challenge of composite materials in aerospace, automotive, and wind energy applications, providing economic and environmental incentives for adoption. The push for recyclable thermoset adhesives, bio-derived bonding systems, and cleavable curing chemistries marks a critical transformation in composite manufacturing, ensuring that sustainability becomes a built-in feature rather than an afterthought.

Composite Adhesive Market Share Insights, 2025-2034

Paste adhesives hold the leading share in the global composite adhesive industry, commanding approximately 42.4% of the projected 2025 market. Their dominance stems from their exceptional versatility, ease of handling, and superior mechanical performance across a wide range of substrates and geometries. Paste adhesives—typically based on epoxy, polyurethane, or methyl methacrylate (MMA) chemistries—are preferred for bonding complex composite structures where gap-filling, high peel strength, and robust adhesion are essential. They are heavily utilized in wind turbine blade manufacturing, automotive component assembly, rail interiors, and marine structures, where joints must withstand high mechanical stress, vibration, and environmental exposure. Their thixotropic nature enables easy application on vertical or contoured surfaces without sagging, while their compatibility with both manual and automated dispensing systems supports modern, high-throughput production lines. The segment continues to grow, driven by the surge in electric vehicle (EV) lightweighting initiatives and modular composite architecture adoption across industries. Paste adhesives also provide advantages in repair and maintenance, offering structural integrity without the need for heat curing—making them an indispensable workhorse in the composite bonding ecosystem.

Film adhesives represent the highest-performance class within the composite adhesives market, widely used in aerospace, defense, and wind energy applications. These pre-catalyzed, B-staged epoxy-based adhesives offer controlled bond-line thickness, uniform stress distribution, and consistent mechanical properties—qualities essential in high-specification structures such as aircraft fuselage panels, rotor blades, and composite wings. The precise nature of film adhesives minimizes voids and ensures long-term durability under fatigue, thermal cycling, and environmental extremes. Aerospace OEMs such as Boeing and Airbus have standardized film adhesives in critical structural assemblies to meet stringent FAA and EASA compliance standards. Their use is also expanding into the automotive and urban air mobility (UAM) sectors, where consistent performance and weight reduction are critical for next-generation vehicles. Although more expensive and requiring specialized handling (typically heat and pressure curing), film adhesives’ contribution to mechanical reliability, surface uniformity, and repeatable performance makes them indispensable in safety-critical composite applications.

Liquid and powder-based composite adhesives form specialized niches within the global market, catering to unique manufacturing processes such as resin infusion, pre-preg consolidation, and thermoplastic bonding. Liquid adhesives—typically low-viscosity epoxies or acrylics—are used where wet layup or vacuum infusion methods require deep substrate penetration and even distribution. They are vital in wind energy blade assembly, automotive composites, and pipe rehabilitation projects where large bonding areas or complex geometries are involved. Powder adhesives, though niche, are gaining relevance in thermoplastic composite welding and powder-coated bonding systems due to their solvent-free formulation and recyclability benefits. These dry systems enable precise control of deposition and are compatible with automated powder-coating lines, making them attractive for future lightweight composite fabrication.

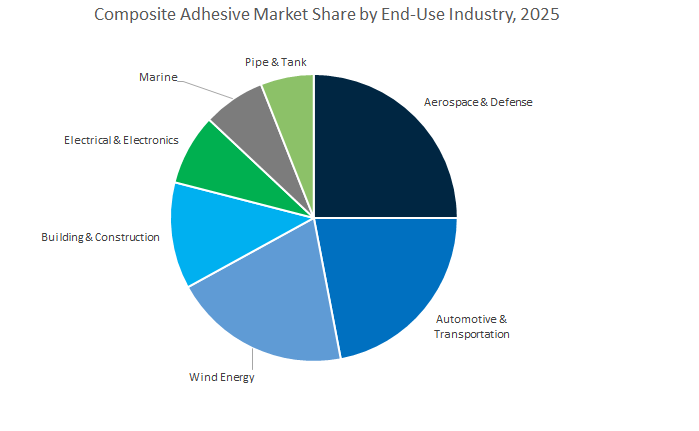

The Aerospace & Defense sector holds the largest market share within the composite adhesives industry, accounting for approximately 25.9% of global demand by 2025. This dominance reflects the sector’s reliance on lightweight structural bonding technologies to replace rivets and fasteners, enabling improved fuel efficiency, structural integrity, and weight savings. Composite adhesives are critical for bonding primary and secondary aircraft structures, including fuselage panels, wings, nacelles, and control surfaces. Adhesives in this sector must meet exceptionally high standards of thermal stability, fatigue resistance, and chemical resilience, often verified through rigorous aerospace certification. Film adhesives dominate in this sector, particularly for co-curing and assembly of carbon fiber-reinforced components, while paste epoxies and polyimides are used for repair and assembly of metallic-composite hybrid joints. The continuous push toward next-generation materials (carbon fiber, ceramic matrix composites) and sustainable aviation initiatives ensures steady demand for innovative adhesive formulations with lower VOCs, improved durability, and recyclability.

The Automotive & Transportation segment, representing around 22.3% of the global market, is a critical driver of adhesive innovation and volume consumption. Composite adhesives are pivotal to vehicle lightweighting strategies, enabling the bonding of dissimilar materials such as aluminum, CFRP, and thermoplastics in car bodies, EV battery enclosures, and chassis structures. High-performance paste and liquid adhesives allow for noise reduction, vibration damping, and structural integrity without the need for heavy mechanical joints. The Wind Energy sector, while slightly smaller in share, is one of the fastest-growing in volume, using large amounts of epoxy-based adhesives to assemble and repair turbine blades exceeding 80 meters in length. These applications demand adhesives that combine high toughness, fatigue endurance, and long-term weatherability, positioning the wind energy sector as a key growth frontier.

In the Building & Construction, Marine, and Industrial composite segments, demand for adhesives is centered on durability, environmental resistance, and mechanical robustness. Building and construction use composite adhesives for panel lamination, architectural cladding, and modular construction, where they enhance both aesthetic and structural performance. In the marine sector, adhesives are indispensable for bonding fiberglass hulls, decks, and interior fittings, providing watertight, corrosion-resistant, and fatigue-resistant bonds in harsh marine conditions. Industrial applications such as pipe and tank manufacturing rely on adhesive systems for joining and repairing composite materials used in chemical plants, desalination facilities, and wastewater infrastructure. These applications prioritize chemical resistance, flexibility, and long service life, solidifying adhesives as a structural necessity. Moreover, the integration of low-VOC and solvent-free technologies is accelerating adoption, aligning with the industry’s sustainability and environmental compliance objectives.

The Electrical and Electronics segment represents a technically sophisticated but smaller share of the global composite adhesives market. These adhesives are used for potting, encapsulation, and substrate bonding in components exposed to thermal cycling, high voltages, and vibration. Composite adhesives enable lightweight enclosures and structural elements for electronic devices and renewable energy components such as battery housings and power inverters. As devices continue to miniaturize and power densities increase, thermally conductive and electrically insulating adhesives are gaining traction. The segment’s growth is being amplified by the electrification of vehicles and expansion of energy storage systems, where composite bonding supports thermal management and mechanical protection. The sector is strategically important for technology convergence and next-generation material development, linking the composite adhesives industry to high-growth fields like EVs, aerospace electronics, and renewable energy infrastructure.

The global composite adhesive market is characterized by a high level of technological differentiation and strategic integration across resin systems, curing technologies, and end-use industries. The competitive ecosystem is dominated by companies like Henkel, 3M, Sika, Huntsman, Arkema (Bostik), and H.B. Fuller, all focusing on high-strength structural adhesives, sustainability, and automation-ready systems for composite assembly in aerospace, automotive, construction, and energy sectors.

Henkel remains a global front-runner in industrial adhesive technologies, leveraging its Loctite brand portfolio to deliver epoxy, acrylic, and polyurethane composite adhesives for lightweighting and high-speed structural assembly. The company’s digital transformation partnership with INCIT aims to enhance smart manufacturing and R&D efficiency, enabling faster development of bio-based and low-VOC formulations. Henkel’s deep integration with automated dispensing systems gives it a unique advantage in high-volume composite assembly lines across EV and aerospace sectors.

3M continues to pioneer multi-material bonding solutions under its Scotch-Weld brand, offering epoxy and urethane adhesives engineered for aerospace, defense, and transportation. The 2023 launch of DP6310NS reinforced 3M’s innovation leadership, addressing the need for high-impact, fast-curing adhesives suitable for bonding dissimilar substrates like carbon fiber composites and aluminum. With a strong reputation for pressure-sensitive and structural adhesives, 3M supports customers through application-ready forms such as films and cartridges, optimizing productivity and precision in complex manufacturing processes.

Sika AG stands out for its expertise in polyurethane and epoxy-based composite adhesives, supporting structural bonding in construction, wind turbine blades, and automotive body assembly. Its strategic acquisitions have strengthened its global reach in industrial adhesives and sealants, particularly for electric vehicle manufacturing and renewable energy components. Sika’s adhesives, such as the Sikadur® and Sikaflex® series, are engineered for high dynamic loads, chemical resistance, and thermal cycling durability, making them indispensable in infrastructure and mobility applications.

Huntsman delivers cutting-edge thermoset and epoxy adhesive chemistries under its flagship ARALDITE® brand, recognized globally for aerospace, industrial, and transportation composite bonding. The company’s R&D focuses on high-temperature performance and thermal stability, essential for flight-critical and high-load environments. Huntsman’s custom polymer formulation services allow clients to develop application-specific adhesives, reinforcing its position as a technical leader in the composite materials supply chain.

Through its Bostik division, Arkema Group has become a powerhouse in advanced acrylic, SMP, and polyurethane adhesive systems for automotive and industrial composites. The $1.65 billion acquisition of Ashland’s Performance Adhesives division significantly strengthened its presence in fast-curing, high-strength formulations tailored for EV battery bonding and lightweight assembly. The company’s R&D centers focus on low-VOC, solvent-free adhesives and hybrid chemistries, aligning with the shift toward eco-friendly composite manufacturing.

H.B. Fuller maintains a strong focus on industrial composite adhesives, offering a broad portfolio including epoxy, polyurethane, and hot melt systems. The company’s innovation strategy emphasizes bespoke formulations for aerospace, packaging, and durable goods assembly, ensuring superior mechanical strength and ease of application. Its entry into MRO-grade structural adhesives extends the brand’s reach into aftermarket and maintenance segments, supporting modular construction and composite repairs.

Composite Adhesive Market Report Scope

Composite Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$6.3 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Epoxy, Acrylic, Polyurethane, Cyanoacrylate, Polyimide, Others), By Component (One-Component (1K), Two-Component (2K)), By Form (Liquid, Paste, Film, Others), By Application (Automotive & Transportation, Aerospace & Defense, Wind Energy, Construction & Infrastructure, Marine, Electrical & Electronics, Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, Huntsman Corporation, H.B. Fuller Company, Arkema Group, Dow Inc., LORD Corporation, Ashland Global Holdings Inc, Permabond LLC, PPG Industries, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Composite Adhesive Market Segmentation

By Product Type / Resin

- Epoxy

- Acrylic

- Polyurethane

- Cyanoacrylate

- Polyimide

- Others

By Component

- One-Component (1K)

- Two-Component (2K)

By Form

By Application

- Automotive & Transportation

- Aerospace & Defense

- Wind Energy

- Construction & Infrastructure

- Marine

- Electrical & Electronics

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top companies in Composite Adhesive Market

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- Huntsman Corporation

- H.B. Fuller Company

- Arkema Group

- Dow Inc.

- LORD Corporation

- Ashland Global Holdings Inc

- Permabond LLC

- PPG Industries, Inc.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Composite Adhesive Market as lightweight manufacturing, automation-ready application, and high-strength resin systems redefine structural bonding across aerospace, automotive/EV, wind energy, marine, electronics, and infrastructure. It delivers analysis reviews of demand drivers, certification pathways, and multi-material joining strategies; highlights processing advances in one- and two-component platforms, film precision bonding, and rapid-cure assembly; and tracks breakthroughs in epoxy, polyurethane, acrylic/methacrylate, and emerging bio-based chemistries that elevate thermal stability, fatigue resistance, and recyclability. With clear comparisons of bondline control, cure kinetics, and durability under vibration/thermal cycling, the study links engineering performance to plant productivity and sustainability outcomes—making this report an essential resource for materials leaders, design engineers, manufacturing strategists, and procurement teams tasked with delivering safer, lighter, and greener products at scale.

Scope Highlights

Segmentation:

- By Product Type/Resin: Epoxy; Acrylic; Polyurethane; Cyanoacrylate; Polyimide; Others.

- By Component: One-Component (1K); Two-Component (2K).

- By Form: Liquid; Paste; Film; Others.

- By Application: Automotive & Transportation; Aerospace & Defense; Wind Energy; Construction & Infrastructure; Marine; Electrical & Electronics; Others.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data (2021–2024) and forecast (2025–2034).

Companies: Analysis/profiles of 15+ companies covering strategies, innovation pipelines, capacity moves, and product benchmarking.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.