Market Overview: Urethane Adhesives Evolve into Core Structural Enablers Across Mobility, Construction, and Industrial Assembly

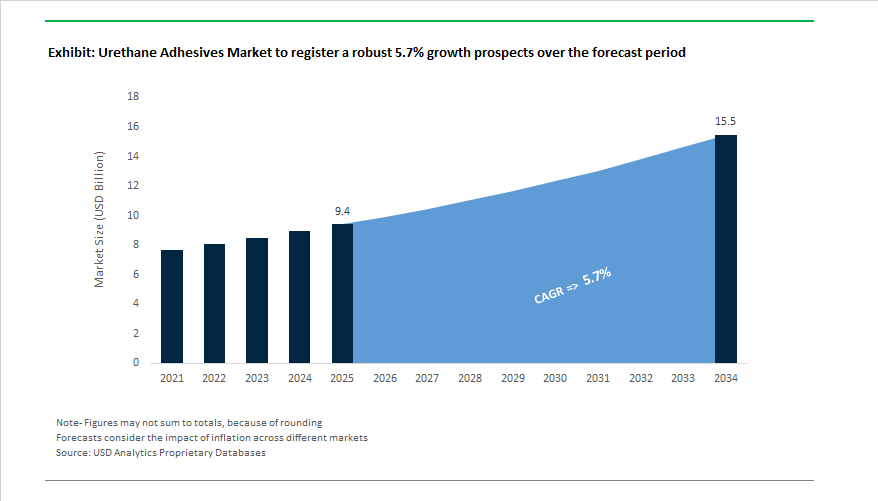

The Global Urethane (Polyurethane) Adhesives Market is expected to grow from USD 9.4 billion in 2025 to USD 15.5 billion by 2034, at a CAGR of 5.7%, as polyurethane chemistries consolidate their role as load-bearing, fatigue-resistant, and regulation-ready bonding systems rather than general-purpose adhesives. Demand is increasingly shaped by OEM specifications in automotive glazing, EV battery assembly, insulated construction panels, and industrial equipment—applications where elastic recovery, moisture tolerance, and long-term durability directly influence safety, performance, and lifecycle cost. Growth is therefore being driven less by end-use breadth and more by technical qualification depth, platform standardization, and global regulatory alignment.

From a technology standpoint, leading manufacturers have materially re-engineered polyurethane platforms to meet tightening safety and sustainability thresholds without compromising performance. Sika’s Purform® platform, Henkel’s low-monomer TEROSON® and LOCTITE® PU systems, and Arkema/Bostik’s next-generation SMP-PU hybrids have established <0.1% free monomer benchmarks to comply with REACH Annex XVII while retaining high elongation and adhesion to glass, coated metals, and composites. In automotive glazing alone, OEM-approved one-component PU adhesives routinely deliver drive-away times below 60 minutes, tensile strengths above 6–8 MPa, and elongation exceeding 400%, making them indispensable for windshield bonding, panoramic roofs, and ADAS camera stability. These systems are now engineered alongside primers and surface activators as validated bonding packages, raising switching costs and reinforcing supplier lock-in.

In construction and industrial assembly, polyurethane adhesives are increasingly specified as functional layers within building envelopes and modular assemblies, not just joining agents. Manufacturers such as H.B. Fuller and Dow have expanded portfolios of moisture-curing and two-component PU adhesives optimized for sandwich panels, roofing membranes, and façade elements, where movement accommodation and long-term watertightness are critical. Typical construction-grade PU adhesives now meet EN 204 D4 water resistance, maintain elasticity across wide temperature swings, and are compatible with automated bead application in offsite manufacturing. At the same time, water-based polyurethane dispersions (PUDs) are gaining share in interior applications and flexible lamination, supported by producers like Covestro and BASF, who are integrating bio-attributed polyols and mass-balance feedstocks to support Scope 3 reduction targets.

Manufacturing and supply-chain considerations are also reshaping the market. Polyurethane adhesives are favored for their process robustness—tolerating variable surface conditions, curing under ambient humidity, and bridging gaps without brittle failure. This makes them particularly attractive in high-mix, high-throughput environments such as appliance assembly, modular construction, and industrial equipment fabrication. To support these use cases, suppliers are pairing product innovation with application engineering, dispensing optimization, and regional capacity expansion, particularly across Asia-Pacific. New production and technical centers in China, Southeast Asia, and India are shortening qualification cycles and aligning local formulations with global OEM standards.

The 2025-2026 period is defined by sustainability initiatives, portfolio sharpening, and supply-side restructuring that directly shape urethane adhesive strategies.

- Technology & Sustainability Push. In June 2025, H.B. Fuller reported that 60% of its new product development is aimed at improving the sustainability of customers’ end products, spanning recyclable packaging and energy-efficient building materials, many enabled by specialized urethane formulations. Also in June 2025, H.B. Fuller launched Millennium PG-1 EF ECO2, a high-performance roofing adhesive utilizing ECO2 Driven™ technology that replaces high-GWP blowing agents—a direct lever for low-carbon construction.

- Raw-Material & Energy Transitions. S&P Global in April 2025 updated its review on electrified reforming for low-carbon hydrogen and methanol, key polyol/isocyanate feedstocks, signaling a future PCF reduction pathway for urethane supply chains. By September 2025, S&P Global spotlighted the IMO’s 2025 Net-Zero Framework, raising scrutiny on the carbon footprint of chemicals, including MDI/TDI value chains.

- Corporate Realignment & Margin Discipline. Huntsman in February 2025 announced strategic options for its European maleic anhydride business and closure of certain downstream PU facilities, reflecting subdued EU demand and high energy costs, while realigning around core, higher-return assets. In February 2025, Sika reported a material margin of 54.5% for 2024, supported by sustainable innovations such as Purform® low-monomer PU technology.

- Application Expansion & Fire-Safe Composites. In October 2025, Teijin Automotive Technologies and Aeronautical Service S.r.l. formed a strategic alliance to deliver next-gen fireproof composites, with urethane adhesives positioned as critical bonding agents in composite structures for automotive and aeronautics.

- Additives & Water-Based Systems. Ashland’s November 2024 strategy update emphasized focus on specialty ingredients, including HEUR rheology modifiers crucial for water-based urethane adhesives, supporting VOC reduction without sacrificing application rheology.

Market Trend 1: Accelerated Adoption of Moisture-Curing, Single-Component Urethane Adhesives for Automotive Direct Glazing and Composite Bonding

The automotive sector is rapidly shifting toward 1K moisture-curing polyurethane (PUR) adhesives for applications such as direct glazing, body panel assembly, and composite bonding, driven by the demand for high strength, simplified operations, and compatibility with mixed-material vehicle designs. The transformation drives the increasing reliance on structural-grade urethanes that combine flexibility with extreme tensile and tear resistance.

Recent performance benchmarks highlight that modern single-component urethane systems can achieve tensile strengths of up to 13.3 MPa and tear strengths of 54.7 kN/m, outperforming older low- to mid-grade formulations (5 MPa). Such superior mechanical properties ensure bond integrity in advanced vehicle structures—particularly those using lightweight composites, aluminum, and panoramic glass assemblies in electric and luxury vehicles.

Fast-curing 1K urethane systems for Auto Glass Replacement (AGR) have further advanced, with specialized adhesives passing the FMVSS 212 crash test in as little as 4 hours under standard humidity and temperature conditions (72°F/55%RH). The capability dramatically reduces vehicle downtime during repair or assembly. Additionally, the application efficiency of single-component systems—offering 10–15 minutes of work time at standard factory conditions—provides a distinct operational advantage over traditional two-component alternatives. These adhesives deliver consistent cure rates, simplified logistics, and enhanced productivity on high-throughput assembly lines across global OEM facilities.

Market Trend 2: Reformulation Towards Amine-Free and Low-Isocyanate Systems for Enhanced Workplace and Environmental Safety

As the global regulatory landscape tightens around isocyanate use and amine emissions, manufacturers are pivoting toward amine-free and low-isocyanate urethane adhesive formulations to safeguard occupational health and ensure compliance with environmental standards.

Under the European Union Regulation (EU) No. 10/2011, the allowable limit for primary aromatic amines (PAAs) in food contact materials is capped at an extremely low 0.01 mg/kg, necessitating the elimination of hazardous monomers from polyurethane adhesive compositions. The shift is particularly critical in sectors such as food packaging, consumer goods, and healthcare, where safety and regulatory conformity dictate material selection.

Industry reports also report that workers exposed to isocyanate-based coatings—especially in automotive refinishing—face up to an 80-fold higher risk of occupational asthma than the general workforce. In response, chemical manufacturers are engineering low-monomer diisocyanate (DI) prepolymers with monomer content below 0.2%, substantially reducing exposure risk while maintaining bonding performance. These new-generation adhesives allow safer usage in confined or high-exposure environments such as vehicle assembly lines, industrial laminating, and flooring installations, enabling compliance with both EU REACH and OSHA occupational exposure standards.

Market Opportunity 1: Development of Rapid-Curing, Flexible Urethanes for On-Site Wind Turbine Blade Repair

The global renewable energy boom, particularly in the wind energy sector, is creating significant opportunities for high-performance urethane adhesives engineered for on-site composite blade repair and bonding. As turbine downtime directly impacts energy production revenue, rapid-cure urethane systems have emerged as a preferred solution for structural repairs that demand both speed and mechanical resilience.

Newly developed urethane hybrid repair adhesives demonstrate fixture times as short as 12–15 minutes, a dramatic improvement over traditional epoxy-based systems that can require several hours of curing. These adhesives are specifically formulated for field conditions, providing reliable bonding performance across fluctuating temperatures and humidity levels.

In terms of structural capability, commercial structural urethanes for composite repair have achieved lap shear strengths of 17.2–24.1 MPa (2500–3500 psi) post-cure, ensuring durability against fatigue, wind stress, and weather exposure. Their inherent elasticity enables damage-tolerant bonding that absorbs vibrational stress—crucial for maintaining aerodynamic performance and long-term structural stability of rotating blades. The performance profile makes them indispensable for wind turbine OEMs and maintenance contractors seeking to optimize turbine uptime and extend lifecycle efficiency.

Market Opportunity 2: Engineering of Bio-Based Polyols for Sustainable Footwear and Packaging Laminates

Sustainability initiatives and corporate carbon-reduction mandates are unlocking lucrative avenues for bio-based urethane adhesives derived from renewable feedstocks such as natural oils, starches, and CO₂-based polyols. The innovation directly aligns with the circular economy and decarbonization strategies of industries like footwear, packaging, and automotive interiors.

Research and commercialization efforts have led to bio-based polyester polyols used in reactive hot-melt polyurethane (HMPUR) adhesives that are manufactured using 100% renewable monomers for the polyol component. These formulations drastically lower lifecycle emissions while maintaining strong mechanical performance in footwear lamination, fabric bonding, and flexible packaging applications.

A key case study highlights CO₂ utilization in polyol synthesis, where up to 15% of the polyol weight is composed of chemically fixed carbon dioxide, transforming greenhouse gases into functional feedstocks for urethane adhesive production. These CO₂-derived polyols not only reduce petrochemical dependence but also demonstrate chemical stability, adhesion reliability, and process compatibility with existing hot-melt urethane systems.

The fusion of bio-based chemistry and CO₂ valorization positions sustainable urethane adhesives as a cornerstone of low-carbon manufacturing. For brand owners and CPG companies, adopting these adhesives supports eco-label certifications and carbon-neutral product portfolios, providing both environmental and market differentiation advantages.

Urethane Adhesives Market Share Insights, 2025-2034

Market Share by Resin Type

The Thermoset Polyurethane segment overwhelmingly dominates the global urethane adhesives market, accounting for a projected 78.4% share in 2025. This segment’s leadership stems from the material’s exceptional bonding strength, thermal stability, and chemical resistance, which make it indispensable in high-stress, load-bearing, and long-term structural applications. Thermoset urethane adhesives cure irreversibly into a cross-linked matrix, forming durable bonds that maintain mechanical integrity even under extreme temperature and chemical exposure. These properties have made them the adhesive of choice for construction, automotive, wind energy, and industrial manufacturing applications, where reliability and resistance to fatigue, vibration, and moisture are essential. In the construction sector, thermoset urethanes are widely utilized for structural glazing, curtain walls, flooring, and insulation systems, providing elasticity and long-term weatherproof performance.

On the other hand, Thermoplastic Polyurethane (TPU) adhesives represent a smaller but increasingly strategic segment of the urethane adhesives market, valued for their re-meltable nature, excellent flexibility, and impact resistance. Unlike thermosets, TPU adhesives soften with heat, allowing for reworkability and heat-activated bonding, which is highly beneficial in footwear manufacturing, textile lamination, and flexible film packaging. Their high elasticity and abrasion resistance also make them ideal for dynamic applications like sportswear, technical fabrics, and flexible electronics.

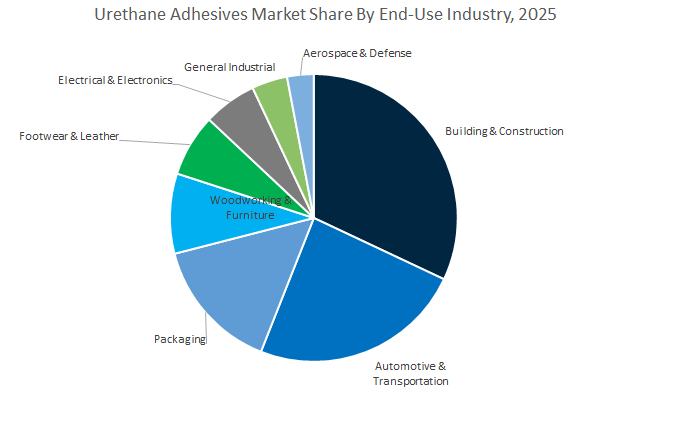

Market Share by End-Use Industry

The Building & Construction sector holds the leading position in the global urethane adhesives industry, accounting for an estimated 32.6% market share in 2025. Urethane adhesives have become integral to the modern construction landscape due to their versatility, weather resistance, and strong adhesion to diverse substrates like glass, concrete, metals, and composites. They are critical for structural glazing, curtain walls, roofing membranes, flooring systems, and insulation bonding, providing long-term flexibility and resilience against environmental stress. The increasing adoption of green building materials, prefabrication methods, and energy-efficient structures further drives demand for high-performance urethane adhesives, particularly those offering low VOC content and long open times for complex installations. The segment’s dominance is reinforced by global infrastructure investments and urbanization trends, particularly in Asia-Pacific and the Middle East, where construction volumes are expanding rapidly.

The Automotive & Transportation segment ranks as the second-largest and fastest-growing end-use market, underpinned by the industry’s shift toward lightweight vehicle architectures, electric mobility, and sustainable manufacturing. Urethane adhesives play a crucial role in composite bonding, glass attachment, trim assembly, and battery encapsulation, offering high mechanical strength with flexibility to absorb vibration and impact. The growth of the electric vehicle (EV) market has notably intensified the demand for urethane systems with enhanced thermal conductivity and dielectric insulation properties, which are essential for battery module assembly and electronic component bonding. Beyond these dominant sectors, several other industries collectively shape the market’s diversity. The Packaging sector leverages urethane adhesives in flexible laminations and barrier film bonding, ensuring performance under high-speed production conditions and food safety compliance. Woodworking & Furniture applications benefit from the adhesive’s strong yet flexible bonds suitable for edge-banding, veneering, and assembly, while Footwear & Leather remains one of the most traditional and consistent consumers due to urethane’s unmatched adhesion to synthetic and natural materials. Additionally, Electrical & Electronics, General Industrial, and Aerospace & Defense segments represent advanced, specification-driven markets. In these domains, urethane adhesives are utilized for encapsulation, potting, vibration resistance, and high-precision assembly, where performance reliability under extreme mechanical and thermal conditions is non-negotiable.

Overview. Competitive differentiation hinges on chemistry breadth (1K/2K PUR, hybrids), worker-safety advances (low-monomer, low-VOC), EV/glazing structural approvals, and global technical support for automated dispensing and on-line quality control. Vendors combining hot-melt PUR (HMPUR), moisture-cure 1K, and 2K structural PUs—plus adjacent coatings/sealants—are best placed to capture system-sell opportunities across mobility, construction, packaging, and electronics.

Henkel’s Technomelt PUR hot-melts deliver high bond strength, heat/chemical resistance, and throughput for applications such as RV panels and headlamp bonding. Its adhesive portfolio appears across thousands of aerospace specifications, underscoring high-reliability urethane and composite bonding credentials. With 1K and 2K PU structural systems, Henkel balances humidity resistance and cohesive strength at diverse line speeds. Strategically, the company is doubling down on e-mobility, supplying materials that accelerate EV battery and structural assembly while supporting sustainability roadmaps.

Sika’s Purform® platform (<0.1% free monomeric diisocyanate) elevates worker safety and REACH compliance without sacrificing performance. The company’s windshield bonding leadership showcases PU’s structural function in vehicles, and its portfolio spans industrial high-strength through construction-grade flexible sealants/adhesives. Execution against sustainable innovation targets—highlighted in 2024 results—positions Sika to capture share as OEMs and contractors standardize on low-monomer systems.

H.B. Fuller aligns 60% of new product development with customer sustainability outcomes, ranging from recyclable packaging to energy-efficient buildings. The Millennium PG-1 EF ECO2 launch (June 2025) replaces high-GWP blowing agents with atmospheric gases, cutting climate impact while maintaining adhesion and foam performance. Fuller’s offerings include bio-content polyurethane hot-melts (e.g., Swift®melt 1850), and its Customer Innovation Awards highlight lightweight auto lighting and triple-IGU glazing enabled by tailored PU chemistries.

Dow integrates polyurethane, silicone, and hybrid chemistries to deliver durable bonding, sealing, and gasketing solutions across mobility and advanced buildings, plus electronics protection. In packaging, Dow emphasizes high-performance, lower-VOC hot-melts that improve surface wetting and line efficiency. The firm’s mobility focus supports battery protection and structural integrity in EVs, pairing adhesives with sealant and encapsulant know-how to deliver system performance.

Huntsman is a major supplier of MDI—the core building block of high-performance PUs—and operates across elastomers and adhesive systems for footwear, insulation, and industrial uses. In February 2025, the company announced European PU restructuring (including facility closures) to restore cost competitiveness amid weak regional demand. Its integration and global technical centers support custom PU systems for large-span structures and harsh-environment assemblies, aligning supply security with application engineering.

Ashland supplies HEUR (hydrophobically modified ethoxylated urethanes) and Aquaflow™ polymers that thicken and stabilize water-based urethane adhesives, improving sag resistance, cohesion, and workability while meeting VOC limits. Its November 2024 update reaffirmed portfolio focus on high-margin specialty additives, including bio-resistant cellulose ethers (Natrosol™) to extend shelf-life and performance stability in PU adhesive formulations—vital for construction and industrial customers migrating to water-borne systems.

Country Analysis: Regional Advancements Shaping the Global Urethane Adhesives Industry

United States – Infrastructure Expansion and EV Growth Fueling High-Performance PU Adhesive Demand

The United States urethane adhesives market continues to gain momentum, supported by national infrastructure spending, evolving environmental regulations, and growing adoption across the automotive, aerospace, and construction industries. The Infrastructure Investment and Jobs Act (IIJA)—allocating $1.2 trillion—is a central driver, stimulating large-scale consumption of polyurethane adhesives for bridge bonding, road insulation, and structural maintenance applications. The initiative has prompted leading producers to expand domestic production capacities. For example, H.B. Fuller has diversified into new markets through acquisitions such as Adhezion Biomedical, enhancing its product portfolio in medical-grade and high-performance polyurethane adhesives.

In the automotive sector, OEMs are increasingly shifting to one-part and two-part polyurethane structural adhesives for lightweighting, crash-durable bonding, and EV battery assembly, leveraging rapid-curing and vibration-resistant formulations. Similarly, the aerospace industry is adopting advanced PU-based flexible adhesives for non-structural interior applications, emphasizing shock and vibration absorption. Meanwhile, the EPA’s stringent VOC regulations have accelerated the transition to hot melt polyurethane (HMPUR) and water-based adhesives, particularly in flooring, furniture, and green building applications. Trade barriers and petrochemical import tariffs are also pushing U.S. producers toward bio-based PU formulations, marking a significant step toward sustainable adhesive chemistry.

China – Localized Production and EV Boom Strengthen Urethane Adhesive Leadership

China continues to assert dominance in the Asia-Pacific urethane adhesives market, driven by rapid urbanization, an expanding EV manufacturing base, and large-scale infrastructure investments. Global leaders such as Sika AG and local producers have intensified their “local-for-local” strategies, commissioning new manufacturing facilities in mid-2025 to meet surging demand for construction-grade polyurethane adhesives and sealants. The rapid urbanization trend, coupled with government-driven green building mandates, has elevated the adoption of low-emission, high-bond PU adhesives for prefabricated structures, wood composites, and insulation panels.

China’s EV revolution is another cornerstone of adhesive demand. Manufacturers are deploying fire-resistant and thermally conductive polyurethane adhesives for battery pack encapsulation, gap filling, and module assembly, ensuring both safety and long-term performance. For the construction sector, Sika’s rapid-set External Insulation Finishing Systems (EIFS) adhesives are gaining traction, offering faster curing times and greater productivity on large-scale projects. Moreover, the government’s emphasis on VOC reduction and sustainability standards has accelerated domestic R&D in solvent-free PU formulations and recyclable polymer adhesives, reinforcing China’s role as a global hub for high-performance urethane bonding solutions.

Germany – Technological Advancement and REACH-Compliant Polyurethane Formulations

Germany remains the European nucleus for advanced urethane adhesive production, propelled by strong regulatory frameworks and precision manufacturing in the automotive, packaging, and construction sectors. In 2024–2025, Henkel AG & Co. KGaA announced a $21–23 million investment in its Bopfingen adhesives facility, scaling up production of hot melt and polyurethane adhesives for wood, packaging, and furniture applications. Meanwhile, the introduction of REACH-compliant Purform® PU technologies by Sika AG has revolutionized the market by significantly reducing monomeric diisocyanate emissions (<0.1%), ensuring safer application and long-term occupational compliance.

Complementing The, Dow Inc. recently completed a new production line in Ahlen, increasing output tenfold for its VORATRON™ polyurethane gap fillers and structural adhesives, directly supporting the European EV battery manufacturing ecosystem. Concurrently, Wacker Chemie AG is pioneering silane-modified polyurethane (SPUR) adhesives, delivering solvent-free, high-flexibility solutions for next-generation construction and industrial applications. Germany’s consistent emphasis on low-emission, high-durability adhesive systems solidifies its status as a leader in sustainable, REACH-compliant polyurethane technology across Europe.

India – Urban Infrastructure Growth Accelerating PU Adhesive Demand

India’s urethane adhesives market is on a high-growth trajectory, propelled by infrastructure expansion, smart city initiatives, and the government’s strong focus on local manufacturing. Large-scale national programs such as Smart Cities Mission and PM Awas Yojana are driving unprecedented demand for polyurethane sealants and construction adhesives in housing, transport, and commercial projects. Henkel’s Phase III facility expansion in Kurkumbh (Pune), completed in July 2024, exemplifies The momentum—featuring Industry 4.0 automation to optimize production of automotive and industrial-grade PU adhesives.

Global entrants are also strengthening their domestic presence. Soudal India, following its full acquisition in 2022, has expanded local manufacturing of PU foams, sealants, and adhesives, targeting the furniture, façade, and general construction markets. Meanwhile, Pidilite Industries Ltd. continues to lead in innovation, introducing urethane-based adhesives for the footwear, furniture, and consumer goods sectors, addressing both performance and cost efficiency. As infrastructure spending and housing projects surge, India is rapidly evolving into a strategic manufacturing and consumption hub for high-performance polyurethane adhesives across Asia.

Japan – High-Precision Urethane Adhesives for Electronics and Automotive Applications

Japan remains a key innovator in advanced urethane adhesive formulations, driven by its leadership in electronics miniaturization, automotive lightweighting, and flexible display technologies. The country’s electronics and semiconductor sectors rely heavily on reactive urethane adhesives offering thermal stability, high flexibility, and excellent insulation for smartphones, computers, and display components. Companies such as LINTEC Corporation and Toagosei Group are spearheading investments in polyurethane-based adhesive films optimized for flexible and high-temperature electronics, aligning with the global shift toward next-generation consumer electronics and EV applications.

The automotive industry continues to expand its use of crash-durable polyurethane structural adhesives, particularly in lightweight vehicle body and chassis assembly, ensuring compliance with Japan’s rigorous safety and fuel-efficiency standards. Ongoing research partnerships are focusing on low-emission reactive urethane formulations, balancing bonding strength, heat resistance, and long-term elasticity. Japan’s precision-driven adhesive market underscores its global role as a supplier of premium, high-reliability polyurethane adhesives for specialized, high-value applications.

South Korea – Advanced Polyurethane Adhesives Powering Electronics and EV Manufacturing

South Korea has emerged as a high-innovation hub for urethane adhesives, fueled by its robust display, semiconductor, and EV manufacturing ecosystems. The government’s semiconductor industrial policy and private-sector investment surge have created substantial demand for high-purity, low-outgassing polyurethane adhesives, essential for ensuring cleanroom compatibility and precision bonding. The materials play a pivotal role in semiconductor encapsulation, optical protection, and thermal interface applications.

The country’s rapidly expanding EV and battery sector also drives intensive R&D in thermally conductive and flame-retardant polyurethane adhesives, enhancing battery safety, energy efficiency, and lifecycle durability. Local manufacturers are introducing electrically insulating PU encapsulants tailored for battery management systems (BMS) and high-voltage assemblies. South Korea’s strategic focus on eco-friendly and energy-efficient adhesive production positions it as a regional powerhouse for advanced urethane adhesive technologies, particularly in electronics, mobility, and renewable energy applications.

Urethane Adhesives Market Report Scope

Urethane Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.4 Billion

|

|

Market Size (2034)

|

$15.5 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Chemistry (Reactive, Hot Melt, Water-Based, Solvent-Based), By Resin Type (Thermoset, Thermoplastic), By End-Use Industry (Building & Construction, Automotive, Packaging, Woodworking, Footwear, Electrical, Aerospace, General Industrial), By Application Type (Structural, Non-Structural

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, Dow Inc., H.B. Fuller Company, Arkema Group, 3M Company, Huntsman Corporation, BASF SE, Wacker Chemie AG, RPM International Inc., Illinois Tool Works Inc., Jowat SE, Pidilite Industries Ltd., Mapei S.p.A., Soudal Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Reactive

- Hot Melt

- Water-Based

- Solvent-Based

By Resin Type

By End-Use Industry

- Building & Construction

- Automotive

- Packaging

- Woodworking

- Footwear

- Electrical

- Aerospace

- General Industrial

By Application Type

- Structural

- Non-Structural

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Urethane Adhesives Market-

- Henkel AG & Co. KGaA

- Sika AG

- Dow Inc.

- H.B. Fuller Company

- Arkema Group

- 3M Company

- Huntsman Corporation

- BASF SE

- Wacker Chemie AG

- RPM International Inc.

- Illinois Tool Works Inc.

- Jowat SE

- Pidilite Industries Ltd.

- Mapei S.p.A.

- Soudal Group

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Urethane (Polyurethane) Adhesives Market, unifying demand-side drivers (EV glazing/assemblies, building envelopes, industrial assembly) with supply-side shifts in low-VOC and low-monomer technologies; our analysis reviews the pace of 1K moisture-cure adoption, the resilience advantages of polyether PU, and the manufacturing localization underway across APAC; it synthesizes recent breakthroughs in rapid fixture, elastic structural bonding, and fire-safe composite integration, and highlights how regulatory tightening (REACH/EHS), decarbonized feedstocks, and automated dispensing are redefining specifications, cycle times, and total installed cost—making this report an essential resource for engineers, procurement leaders, and product managers aligning strength, flexibility, and durability with compliance and throughput, etc……

Scope Highlights

Segmentation:

- By Chemistry: Reactive; Hot Melt; Water-Based; Solvent-Based

- By Resin Type: Thermoset; Thermoplastic

- By End-Use Industry: Building & Construction; Automotive; Packaging; Woodworking; Footwear; Electrical; Aerospace; General Industrial

- By Application Type: Structural; Non-Structural

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered (analysis/profiles of 15+): Henkel AG & Co. KGaA; Sika AG; Dow Inc.; H.B. Fuller Company; Arkema Group; 3M Company; Huntsman Corporation; BASF SE; Wacker Chemie AG; RPM International Inc.; Illinois Tool Works Inc.; Jowat SE; Pidilite Industries Ltd.; Mapei S.p.A.; Soudal Group.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.