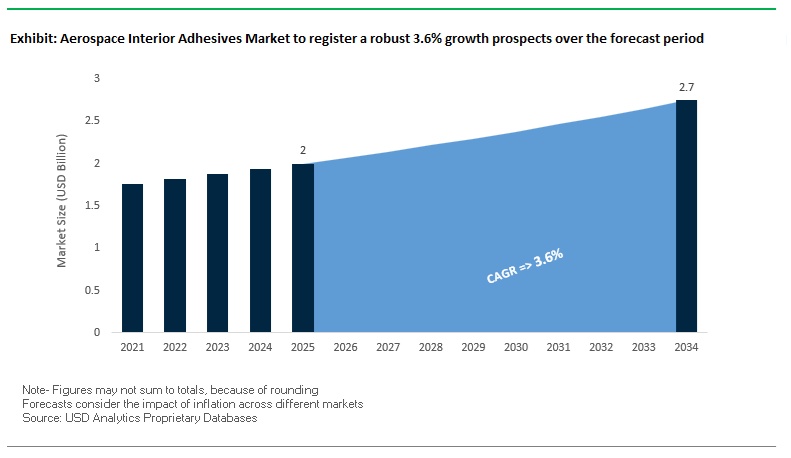

The global aerospace interior adhesives market is projected to increase from $2 billion in 2025 to $2.7 billion by 2034, registering a CAGR of 3.6%. This steady expansion is attributed to the increasing emphasis on FAR 25.853-compliant fire-retardant materials, lightweight composite integration, and advancements in epoxy, phenolic, and polyurethane-based bonding technologies. Industry professionals are focusing on adhesives that balance structural performance, flame retardancy, and low-VOC emissions, addressing the stringent safety and environmental standards governing aircraft interiors.

The adoption of Carbon Fiber Reinforced Polymer (CFRP) structures across aircraft interiors is reshaping adhesive specifications, with epoxy film adhesives and syntactic paste adhesives emerging as core solutions for honeycomb panel bonding and lightweight assembly. Maintenance, Repair, and Overhaul (MRO) operations depend heavily on room-temperature curing (RTC) adhesives, field repair kits, and flexible sealing compounds. Meanwhile, seat assembly, lavatory units, galleys, and stowage bins are key applications demanding rapid cure adhesives to meet high-rate production targets.

Compliance with Federal Aviation Regulation (FAR) 25.853 remains the cornerstone of aerospace interior manufacturing, mandating low flammability, limited heat release (OSU 65/65), and low smoke density (NBS testing). As OEMs and Tier-1 suppliers transition toward halogen-free, FST-compliant formulations, adhesive manufacturers are accelerating R&D in water-borne, bio-based, and non-solvent chemistries. Simultaneously, the introduction of digital and automated adhesive dispensing systems ensures bond-line thickness control and process consistency, critical for high-throughput aircraft manufacturing.

The global aerospace interior adhesives industry is entering a critical phase characterized by innovation in flame-retardant adhesives, regulatory compliance, and material science advancements. In June 2026, Henkel AG & Co. KGaA launched a new generation of Loctite structural adhesives designed for cabin interiors. These adhesives offer 30% faster curing times, optimizing multi-material bonding efficiency across high-throughput production lines and marking a pivotal move toward sustainable, rapid-cure epoxy technologies.

In May 2026, the U.S. Federal Aviation Administration (FAA) released an advisory circular outlining updated best practices for thermoplastic composite panel repair—a policy that effectively boosts demand for certified aerospace thermoplastic bonding agents. Shortly after, Huntsman Corporation announced a major R&D expansion in Texas (April 2026), reinforcing its investment in Araldite® epoxy systems engineered for flame-retardant interior panels. These developments underline a broader trend: adhesive manufacturers are prioritizing compliance, speed, and sustainability to meet OEM cabin certification standards.

On the innovation front, PPG Industries (March 2026) introduced PRC® low-density polysulfide sealants using SEMCO® SEMKIT® packaging, reducing cure times for cabin floor and pressurization seals during MRO operations. In February 2026, Airbus set a new procurement precedent by mandating halogen-free, FST-compliant adhesives for all interior suppliers, effectively reshaping supply chain chemistry standards. Meanwhile, 3M Aerospace (January 2026) achieved OEM certification for its Scotch-Weld™ adhesive films, expanding its role in secondary structural bonding across next-generation narrow-body programs.

Innovation partnerships have also emerged as a key growth vector. In December 2025, LG Chem partnered with a European airframe manufacturer to co-develop polyurethane-based acoustic adhesives, enhancing cabin soundproofing performance. Similarly, Solvay (November 2025) finalized the divestiture of its SolvaLite® prepreg and structural adhesive unit, which will focus exclusively on composite bonding for aerospace and defense. Meanwhile, Lufthansa Technik (October 2025) implemented PPG ARE™ 3D-printed gaskets for cabin pressurization, symbolizing the integration of additive manufacturing and aerospace sealing technologies.

This sequence of developments highlights a distinct market trajectory — one defined by material innovation, fire safety mandates, and manufacturing automation. The industry’s core growth drivers are centered on lightweighting, rapid curing, PFAS-free compliance, and smart adhesive application technologies that enable both OEM assembly and MRO efficiency.

The aerospace sector is witnessing a decisive shift toward Fire, Smoke, and Toxicity (FST)-compliant adhesives, driven by evolving safety mandates from aviation regulatory bodies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA). The foundational requirement under FAR 25.853 and Appendix F compels all interior components—including wall panels, flooring, and insulation systems—to meet strict flame spread, smoke density, and heat release criteria. The move directly supports enhanced passenger survivability, extending escape times by an estimated 2–4 minutes in post-crash fuel fire scenarios, underscoring the life-critical importance of advanced adhesive technologies.

In response, manufacturers are reformulating adhesives with non-halogenated epoxy and phenolic chemistries to replace older halogenated flame-retardant systems. These next-generation formulations not only pass Boeing’s BSS 7238 (low smoke density) and BSS 7239 (low toxicity) tests but also align with environmental and occupational safety goals. Major aerospace adhesive producers have launched high-performance bonding systems tailored for laminated panels, galley modules, and lavatory assemblies, combining stringent FST compliance with long-term durability and chemical resistance.

Beyond compliance, the trend represents a shift in aircraft material philosophy. As OEMs integrate composite and thermoplastic interior materials with lower ignition potential, adhesive systems must provide thermal stability, low VOC emissions, and compatibility across mixed substrates. The performance trifecta—fire resistance, low toxicity, and mechanical endurance—is the baseline for approval in new cabin programs and retrofit applications.

Fuel efficiency remains a central pillar of aviation economics, and the cabin interior segment plays a crucial role in the equation. The adoption of lightweight composite and honeycomb sandwich structures has accelerated dramatically, with OEMs like Airbus reporting approximately 15% reductions in cabin weight in select programs through the use of adhesive-intensive bonding methods. The evolution reduces both operational fuel consumption and lifecycle maintenance costs, while expanding design flexibility for modular cabin layouts.

The market is seeing a surge in epoxy-based void fillers and core reinforcement adhesives with densities as low as 0.35 g/cm³, optimized for honeycomb sandwich panels, stowage bins, and galley modules. These high-performance materials replace traditional mechanical fasteners, reducing the number of attachment points and further lowering assembly weight.

In addition, cyclic durability and chemical resistance have become critical testing parameters. Aircraft interiors are routinely exposed to disinfectants, cleaning solvents, and humidity fluctuations; hence, adhesive systems must sustain long-term shear strength and creep resistance under such conditions. Advanced formulations, including elastomer-toughened epoxy and urethane hybrid adhesives, are increasingly preferred for their ability to absorb vibration and resist degradation during prolonged service cycles.

The shift aligns directly with the modular design movement in aerospace interiors. Airlines are opting for reconfigurable cabin modules, such as interchangeable lavatory and galley systems, which rely on quick-curing, high-strength adhesives to facilitate rapid installation and maintenance without structural compromise. These adhesive solutions underpin the industry’s drive toward lighter, faster, and more efficient interior manufacturing processes.

Sustainability has emerged as a central strategic focus in cabin design, creating a substantial innovation opportunity for eco-compatible aerospace adhesives. Airlines and OEMs are increasingly substituting traditional petrochemical-based composites with bio-based resins, recycled thermoplastics, and natural fiber composites (such as flax and hemp) for non-structural interior elements like partitions, seat shells, and trim components. However, these new substrates present adhesion challenges due to their diverse surface energy profiles, necessitating specialized adhesive systems that can bond effectively without compromising FST compliance.

To meet the demand, leading chemical groups are developing water-based, low-VOC, and solvent-free adhesive formulations specifically engineered for next-generation cabin materials. A top aerospace adhesives manufacturer’s parent group announced a $10 million R&D investment (2022–2023) aimed at scaling water-based polymer systems that simultaneously meet low smoke, low toxicity, and high adhesion requirements. The investment responds to growing airline mandates for cabin sustainability and improved indoor air quality—both during manufacturing and operation.

Further, the Air Transport Action Group (ATAG) and major aerospace consortiums are pushing for carbon-neutral cabin materials by 2050. Adhesive solutions enabling recyclable or disassemblable bonding between biocomposites and thermoplastics will be vital in meeting these targets, creating a new frontier for green-certified bonding technologies.

A robust and expanding Maintenance, Repair, and Overhaul (MRO) market is driving consistent aftermarket demand for aerospace interior adhesives, particularly as airlines seek to modernize cabin aesthetics and optimize fleet utilization post-pandemic. Aging wide-body aircraft, including the Boeing 777 and Airbus A330, continue to represent a significant portion of active global fleets, generating recurring demand for interior refurbishment adhesives used in panel overlays, galley reconstruction, and IFE (In-Flight Entertainment) integration.

The post-2022 recovery in long-haul traffic has accelerated the retrofit cycle, with many airlines advancing full-cabin reconfigurations every 7–10 years to align with passenger experience and branding goals. The cyclic refurbishment market fuels high-volume consumption of fast-curing structural epoxy systems, repair-grade adhesives, and decorative film bonding agents optimized for on-wing or hangar-based maintenance operations.

In addition, the rising focus on VIP and private jet completions is opening lucrative, high-margin niches for aesthetic-grade interior adhesives that combine structural performance with aesthetic compatibility—critical for bonding luxury veneers, composite furniture, and decorative laminates. The MRO segment’s demand for certified, easy-to-apply, and reworkable adhesive systems will remain a stable revenue stream as fleet extension policies and airline interior modernization programs continue globally.

Aerospace Interior Adhesives Market Share Insights, 2025-2034

The liquid and paste adhesives segment dominates the global aerospace interior adhesives industry, accounting for an estimated 35% market share in 2025. This leadership stems from their exceptional versatility, proven bonding performance, and adaptability across a wide range of substrates, including aluminum, thermoplastics, composites, and foams. These adhesives—primarily two-part epoxies and polyurethanes—are the backbone of interior assembly applications, from panel bonding and seat frame attachment to flooring and insulation systems. Their ability to meet the aerospace industry’s stringent flammability, smoke, and toxicity (FST) standards makes them indispensable for both OEM and MRO use. The formulation flexibility of liquid/paste adhesives allows manufacturers to tailor viscosity, cure speed, and thermal resistance for specific processes such as brush, spray, or automated bead application, improving efficiency and precision. Additionally, the increasing adoption of low-VOC and solvent-free adhesive systems aligns with the aviation industry’s sustainability and cabin air quality goals. As aircraft interiors evolve toward lightweight composite structures and multi-material assemblies, liquid and paste adhesives will continue to be the primary enablers of structural integrity and design innovation within the cabin environment.

The film adhesives segment, with a projected 25% share, holds a critical position in high-performance interior panel manufacturing. Film adhesives—typically epoxy-based and B-staged (partially cured)—are favored for their clean handling, controlled thickness, and consistent bond-line uniformity, which are essential for aerospace-quality production. They are primarily used in bonding composite skins to honeycomb cores for sidewalls, ceilings, galleys, lavatories, and partitions, forming the structural foundation of lightweight cabin monuments. The aerospace industry’s increasing emphasis on weight reduction and automated composite layup processes has further boosted film adhesive adoption, as they integrate seamlessly into autoclave and out-of-autoclave (OOA) curing systems. Their void-free bonding capability, resistance to thermal cycling, and superior mechanical properties make them indispensable in both commercial and business jet interiors. Moreover, leading adhesive manufacturers are advancing low-temperature-curing film technologies that reduce energy consumption while maintaining aerospace-grade reliability. As aircraft OEMs adopt modular, composite-intensive cabin architectures, film adhesives will remain the preferred technology for precision interior bonding and large-panel fabrication.

The pressure-sensitive adhesives (PSAs) and hot melt adhesives segments serve specialized but rapidly growing niches within the aerospace interior adhesives landscape. PSAs are integral to trim attachment, wire harnessing, insulation mounting, and quick-install applications, offering immediate adhesion without curing time—a key advantage for both OEM and MRO environments. They are particularly valuable for maintenance operations, where removable, reworkable tapes and films streamline assembly and repair. Hot melt adhesives, on the other hand, dominate textile bonding, carpeting, and sound-damping assemblies, where fast-setting and high-throughput production are essential. With innovations in thermoplastic polyolefin and reactive hot melt (PUR) formulations, these adhesives are achieving higher heat resistance and improved flexibility, extending their use beyond decorative applications. Meanwhile, void and edge fillers, as well as potting compounds, are indispensable for reinforcing honeycomb core edges, structural voids, and crash zones, ensuring mechanical stability and compliance with aerospace safety regulations. These products, often based on epoxy or polyurethane chemistries, are seeing rising adoption due to composite-intensive cabin structures and stringent crashworthiness requirements.

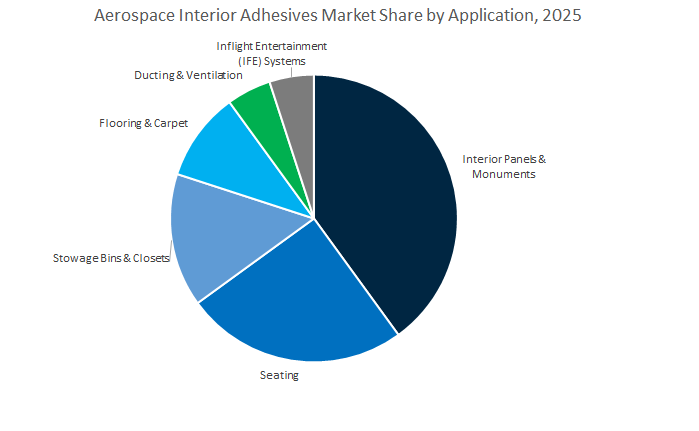

The interior panels and monuments segment represents the largest share of the aerospace interior adhesives market, accounting for roughly 40% of global demand in 2025. This dominance reflects the sheer surface area and material complexity of aircraft cabins, where nearly every visible structure—from sidewalls and partitions to lavatories, galleys, and ceiling panels—is bonded using advanced adhesive systems. The industry’s migration toward lightweight honeycomb-core composites has further intensified demand for film and paste adhesives that ensure strong, durable, and FST-compliant bonds. These adhesives provide the essential structural stiffness and vibration resistance required to withstand the rigors of pressurization cycles and passenger use over decades. With aircraft OEMs increasingly standardizing modular cabin configurations for faster customization and maintenance, adhesives are replacing mechanical fasteners to improve aesthetics and weight efficiency. Additionally, the development of low-density and thermally stable bonding systems supports the integration of new composite interior materials, driving continuous growth in this foundational segment.

The seating segment, holding an estimated 25% market share, stands as the second-largest and most innovation-intensive application area in the aerospace interior adhesives industry. Aircraft seating presents a uniquely demanding adhesive environment—requiring solutions that can bond composite seat frames, foam cushioning, fire-blocking layers, and upholstery fabrics, all while maintaining lightweight, flexibility, and FST compliance. Adhesives used in seating must endure constant load cycles, temperature fluctuations, and vibration throughout the aircraft’s service life. Polyurethane and epoxy-based adhesives dominate this application due to their impact resistance, acoustic insulation properties, and strong adhesion to dissimilar materials. The aviation trend toward thinner, lighter, and ergonomic seating designs has further intensified demand for low-density structural and sprayable adhesive systems. Additionally, cabin reconfiguration and retrofit programs—particularly in commercial and business jets—are creating steady MRO-driven demand for quick-curing, reworkable, and solvent-free adhesives that streamline seat assembly and repair. The segment’s continued growth aligns closely with the broader industry shift toward passenger comfort, energy efficiency, and modernized cabin interiors.

The stowage bins and flooring applications represent another key pillar of aerospace interior adhesive demand, reflecting the need for durability, structural integrity, and safety in high-traffic areas. Overhead bins, closets, and cargo compartments require tough, fatigue-resistant adhesives capable of bonding composite shells, hinge mounts, and latch mechanisms that endure repeated mechanical stress. Flooring and carpet bonding applications, meanwhile, depend on adhesives that provide long-term shear strength, fire resistance, and flexibility to accommodate aircraft vibration and thermal expansion. Hot melt and contact adhesives dominate carpet and insulation attachment, while two-part polyurethanes are used in multi-layer flooring constructions to ensure lasting adhesion under compressive loads. With airlines prioritizing cabin noise reduction and acoustic insulation, specialized sound-damping adhesives are gaining traction in flooring systems.

The ducting, ventilation, and in-flight entertainment (IFE) systems segments, while smaller in global market share, represent high-value, specialized niches that demand precision bonding and environmental resilience. Ducting and ventilation components rely on adhesives capable of withstanding temperature cycling, humidity variations, and continuous airflow vibration, making silicone and epoxy formulations the materials of choice. On the other hand, IFE systems require electrically non-conductive, low-outgassing adhesives for screen mounting, cable management, and component encapsulation. The rapid integration of wireless connectivity, touch-screen displays, and smart cabin systems has expanded adhesive use in IFE assembly and maintenance. These high-precision, electronics-compatible adhesives are tailored to minimize electromagnetic interference while maintaining reliability during flight. As the industry continues to prioritize passenger experience, noise control, and energy efficiency, adhesives for ducting, ventilation, and IFE systems will remain critical to enabling next-generation cabin functionality and modular design flexibility.

The global aerospace interior adhesives market is dominated by technologically advanced manufacturers including 3M Company, Henkel AG & Co. KGaA, Huntsman Corporation, PPG Industries, Hexion Inc., and Sekisui Aerospace Group. Each of these companies leverages a combination of certified product lines, sustainable chemistry innovation, and automation technologies to meet evolving industry demands for flame-retardant, low-VOC, and lightweight bonding solutions.

3M Company leads in structural adhesives and sealants through its well-established Scotch-Weld™ and VHB™ product lines. Core offerings include AF 131 and AF 147 adhesive films and AC-380 polysulfide sealants for critical sealing in aircraft interiors and fuel systems. The company’s R&D efforts center on low-density and fast-cure adhesives, aligning with aircraft weight-reduction goals. Widely used in primary and secondary bonding, 3M’s products enhance production efficiency while maintaining mechanical strength. The brand’s focus on two-part acrylic and epoxy systems supports quick fixture bonding in MRO repairs, reinforcing its leadership in aircraft structural bonding technologies.

Henkel, the global leader in adhesives, has established a strong foothold in interior structural bonding through its Loctite® and Bonderite® lines. Its liquid and paste epoxy adhesives are engineered for floor panel, stowage bin, and bulkhead bonding applications, offering exceptional fatigue resistance and strength. The company integrates Loctite® dispensing systems to automate bonding in aircraft seat and panel production. Henkel’s R&D strategy focuses heavily on bio-based and low-emission adhesives, supporting OEM sustainability goals. The company’s commitment to halogen-free and low-VOC systems is setting benchmarks in FST-compliant interior assembly.

Huntsman specializes in Araldite® and Aradur® epoxy systems, optimized for fire-resistant, high-temperature applications within aircraft interiors. Its Cascophen® phenolic resin systems remain integral to honeycomb sandwich panels used in galleys and lavatories. The company’s innovation focus includes lightweight, high-strength adhesives compatible with advanced engineering plastics, enabling modular, weight-optimized interiors. Huntsman’s newest epoxy systems offer faster processing and lower cure temperatures, reducing manufacturing energy consumption while maintaining FAR 25.853 compliance and mechanical integrity.

PPG Industries remains a key player in aerospace sealants and coatings, with renowned brands such as PRC®, Pro-Seal™, and SEMCO®. Its adhesives portfolio covers cabin pressurization seals, window assemblies, and fuel system interfaces, offered through the SEMKIT® cartridge system for efficient application. Recent innovations include epoxy syntactic paste adhesives (ESPA) engineered for honeycomb core filling and reinforcement, ensuring high mechanical performance at minimal weight. PPG’s automation-ready SEMCO® dispensing systems enhance bond-line control and material efficiency, making it a leader in aerospace MRO adhesives.

Hexion Inc. is a global leader in phenolic and resorcinol-formaldehyde resins used for fire-retardant interior panels. Its Cascophen® product line underpins the construction of FST-compliant laminates used in galleys, lavatories, and flooring systems. Hexion’s adhesives deliver dimensional stability, moisture resistance, and low smoke emission, supporting compliance with FAR 25.853 fire safety standards. The company continues to reformulate its resins to meet low-formaldehyde and low-emission regulations, maintaining leadership in fire-safe bonding solutions for aircraft interiors.

Sekisui Aerospace Group integrates adhesive expertise within its composite manufacturing operations, focusing on film adhesives, prepregs, and thermoplastic bonding. Operating more than 50 automated production lines, the company uses advanced adhesive technologies to assemble stowage bins, seat shells, and lavatory modules. Its internal adhesive systems ensure precise bond-line control and efficient curing cycles, enabling high-rate production of lightweight structures. Sekisui’s expertise in CFRP-to-thermoplastic bonding supports the industry’s drive for lighter, modular, and sustainable cabin interiors.

The United States aerospace interior adhesives market leads globally, driven by a strong regulatory framework, expanding OEM programs, and robust defense investments. The Federal Aviation Administration (FAA) introduced updated fire resistance and low-VOC guidelines (2025) for aircraft cabin materials, compelling adhesive manufacturers to focus R&D on FST-compliant epoxy and polyurethane systems. The adhesives, engineered for low smoke emission and non-toxicity, are increasingly vital in cabin interiors, including sidewalls, lavatories, and floor panels.

The country’s major OEMs, particularly Boeing, have amplified adhesive consumption. Its 787 Dreamliner interior modernization program (2025) has increased the adoption of lightweight, high-performance structural adhesives by over 10%, according to industry reports. Meanwhile, PPG Industries’ $380 million North Carolina facility investment (2025) is expanding the U.S. domestic supply chain for aerospace coatings, sealants, and bonding solutions used in cabin assembly and refurbishment. On the defense front, sustained FY2025 RDT&E allocations exceeding $143 billion ensure ongoing procurement of advanced bonding systems for stealth platforms, cockpit modules, and avionics encapsulation.

Germany remains at the forefront of the European aerospace interior adhesives market, recognized for its precision polyurethane systems and sustainability-focused formulations. German chemical producers are investing heavily in low-density polyurethane foaming systems used for honeycomb sandwich panels, a core structural component of aircraft galleys, sidewalls, and monuments. The adhesives contribute significantly to weight reduction and acoustic performance in cabin manufacturing.

Regulatory drivers, particularly EASA’s REACH and VOC directives (2025), are pushing aerospace suppliers toward waterborne and 100% solids adhesive systems that improve indoor air quality during aircraft assembly. German firms are also pioneering two-component epoxy potting compounds for securing mechanical inserts and fasteners in cabin panels—ensuring enhanced vibration resistance and longevity. Supported by Germany’s strong industrial R&D infrastructure and proximity to Airbus’s major European production sites, the country continues to dominate in the development of eco-friendly, high-durability aerospace interior adhesives.

France remains a critical hub for aerospace interior adhesive manufacturing and innovation, driven by its position as Airbus’s central production base. The ongoing Airbus single-aisle program ramp-up has sharply increased demand for rapid-cure core splice adhesives and automated dispensing systems for assembling aircraft cabin panels and ceiling structures. French aerospace suppliers are leveraging automation and robotics to achieve faster production cycles while maintaining precision bonding integrity.

France’s adhesives industry is also advancing in FST-certified thermoplastic bonding technologies, ensuring compliance with EASA CS-25 fire safety regulations. Leading manufacturers are working on low-flammability and low-smoke adhesives to enhance passenger safety and cabin air quality. Historical strategic consolidations, such as Hexcel’s acquisition of Structil, have strengthened France’s expertise in aerospace film adhesives and composite bonding for both interior and structural applications. Additionally, the nation’s continued focus on sustainable chemistry and smart adhesives underlines its leadership in next-generation aerospace cabin bonding solutions.

China’s aerospace interior adhesives market is rapidly expanding in alignment with the government’s “Made in China 2025” policy, which emphasizes domestic manufacturing of certified aerospace-grade materials. The COMAC C919 program continues to be a major growth driver, creating large-scale demand for fire-retardant cabin adhesives in galleys, lavatories, sidewalls, and overhead storage bins. Chinese adhesive companies are scaling up production capacity for FST-compliant epoxy and polyurethane systems to support COMAC’s growing aircraft output.

Simultaneously, China’s fast-developing Maintenance, Repair, and Overhaul (MRO) sector is boosting the need for high-reliability epoxy repair kits and sealants, particularly for commercial aircraft refurbishments. Government funding for aviation infrastructure and materials self-sufficiency is fostering collaborations between local manufacturers and international chemical companies to improve formulation quality. With continued investments in flame-resistant, low-density bonding systems, China is solidifying its position as Asia-Pacific’s leading aerospace interior adhesives manufacturing hub.

India’s aerospace interior adhesives sector is gaining momentum as the country strengthens its domestic aircraft manufacturing ecosystem under the “Make in India” initiative. The establishment of new aerospace component plants and joint ventures with foreign OEMs is driving localized production of laminate adhesives, core-fill compounds, and void-filling materials for cabin interiors. The transition is reducing import dependency while ensuring a steady supply chain for civil and defense aircraft assembly.

The Indian government’s efforts to streamline aerospace certification and testing processes are enabling domestic chemical manufacturers to develop products aligned with EASA and FAR specifications. Local R&D centers are prioritizing FST-compliant adhesive systems and PU-based structural bonding materials for aircraft flooring, panels, and seating. As India increases investment in MRO infrastructure, demand is also surging for lightweight epoxy bonding solutions that meet global aviation standards, positioning the country as an emerging aerospace interior adhesive innovation hub in South Asia.

Japan’s aerospace interior adhesives market benefits from its leadership in advanced composites and materials engineering. Japanese manufacturers specialize in co-curable adhesive films for carbon fiber-reinforced cabin panels, essential for reducing overall aircraft weight. The high-precision adhesives ensure strong, flexible bonding while meeting stringent FST and temperature resistance requirements.

Automation is a key theme in Japan’s aerospace adhesive applications. Local aerospace firms are deploying robotic dispensing systems for consistent application of two-part epoxy and core splice adhesives, enhancing production throughput and reducing waste. Japan’s expertise in resin chemistry, precision dosing, and automation control allows it to meet the growing global demand for lightweight, high-durability cabin bonding systems.

Spain has emerged as a strategic production hub within the European aerospace adhesives market, largely due to Henkel’s major expansion of its Montornès del Vallès facility. The site, which produces LOCTITE and BONDERITE aerospace adhesives and sealants, significantly enhances Europe’s supply of high-performance bonding materials for aircraft interiors and MRO applications. The expansion enables Henkel to support both major OEM programs and aftermarket repair operations, ensuring timely supply across Airbus assembly lines and related subcontractors.

The United Kingdom aerospace interior adhesives market is advancing rapidly through focused research on lightweight thermoplastic bonding materials. Specialized firms and R&D institutions are developing low-density epoxy adhesives and FST-certified thermoplastics aimed at improving performance in seating structures, inflight entertainment (IFE) enclosures, and decorative laminates. The innovations align with the UK’s commitment to carbon reduction and material circularity within aerospace manufacturing.

The integration of thermoplastic composites and next-generation adhesives in cabin assembly offers faster processing times, recyclability, and reduced emissions. Such developments place the UK among the key European centers driving sustainable and high-efficiency interior bonding technologies for future aerospace applications.

Aerospace Interior Adhesives Market Report Scope

Aerospace Interior Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$2.7 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Resin Type (Epoxy Adhesives, Polyurethane Adhesives, Silicone Adhesives, Cyanoacrylate Adhesives, Acrylic Adhesives, Others), By Product Technology (Film Adhesives, Liquid/Paste Adhesives, Hot Melt Adhesives, Pressure Sensitive Adhesives (PSA Tapes/Foils), Void/Edge Fillers and Potting Compounds, Primers and Surface Pre-treatments), By Application Type (Interior Panels, Monuments, Seating, Stowage Bins & Closets, Flooring & Carpet, Inflight Entertainment (IFE) Systems, Ducting & Ventilation), By Aircraft Type (Narrow-Body Aircraft, Wide-Body Aircraft, Regional Jets (RJs) and Turboprops, General Aviation (GA), Military Aircraft), By End-Use (OEMs, MRO

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Huntsman Corporation, PPG Industries, Inc., Solvay S.A., Sika AG, Arkema S.A. (Bostik), Dow Inc., Master Bond Inc., Permatex, Lord Corporation, DELO Industrial Adhesives, Hexcel Corporation, Adhetec

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type (Chemical Composition)

- Epoxy Adhesives

- Polyurethane Adhesives

- Silicone Adhesives

- Cyanoacrylate Adhesives

- Acrylic Adhesives

- Others

By Product Technology/Form

- Film Adhesives

- Liquid/Paste Adhesives

- Hot Melt Adhesives

- Pressure Sensitive Adhesives (PSA Tapes/Foils)

- Void/Edge Fillers and Potting Compounds

- Primers and Surface Pre-treatments

By Application Type (Aircraft Interior Sub-segment)

- Interior Panels

- Monuments

- Seating

- Stowage Bins & Closets

- Flooring & Carpet

- Inflight Entertainment (IFE) Systems

- Ducting & Ventilation

By Aircraft Type

- Narrow-Body Aircraft

- Wide-Body Aircraft

- Regional Jets (RJs) and Turboprops

- General Aviation (GA)

- Military Aircraft

By End-Use

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Huntsman Corporation

- PPG Industries, Inc.

- Solvay S.A.

- Sika AG

- Arkema S.A. (Bostik)

- Dow Inc.

- Master Bond Inc.

- Permatex

- Lord Corporation

- DELO Industrial Adhesives

- Hexcel Corporation

- Adhetec

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Aerospace Interior Adhesives Market with granular sizing, pricing corridors, and specification adoption across cabin systems; our analysis reviews regulatory momentum (FAR 25.853/FST), composite integration, supply risk, and qualification lead times, and highlights innovation vectors such as halogen-free chemistries, low-density syntactics, and automation-ready dispensing. Mapping certification pathways and buyer criteria (bond strength, cure speed, VOC limits, OSU/NBS scores), we benchmark leaders, track capex and M&A, and quantify retrofit and MRO pull through 2034. Incorporating technology roadmaps and procurement playbooks, this report is an essential resource for OEM, Tier-1, and MRO decision-makers aligning materials strategy to safety, sustainability, and throughput breakthroughs across interiors.

Scope Includes

- By Resin Type (Chemical Composition): Epoxy; Polyurethane; Silicone; Cyanoacrylate; Acrylic; Others

- By Product Technology/Form: Film Adhesives; Liquid/Paste Adhesives; Hot Melt Adhesives; Pressure-Sensitive Adhesives (PSA Tapes/Foils); Void/Edge Fillers & Potting Compounds; Primers & Surface Pre-treatments

- By Application (Interior Sub-segment): Interior Panels; Monuments; Seating; Stowage Bins & Closets; Flooring & Carpet; In-Flight Entertainment (IFE) Systems; Ducting & Ventilation

- By Aircraft Type: Narrow-Body; Wide-Body; Regional Jets & Turboprops; General Aviation; Military Aircraft

- By End-Use: OEMs; MRO

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Horizon: Historic 2021–2024 and Forecast 2025–2034.

- Companies: 15+ company analysis/profiles, including strategy, certifications, product lines, and recent developments.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.