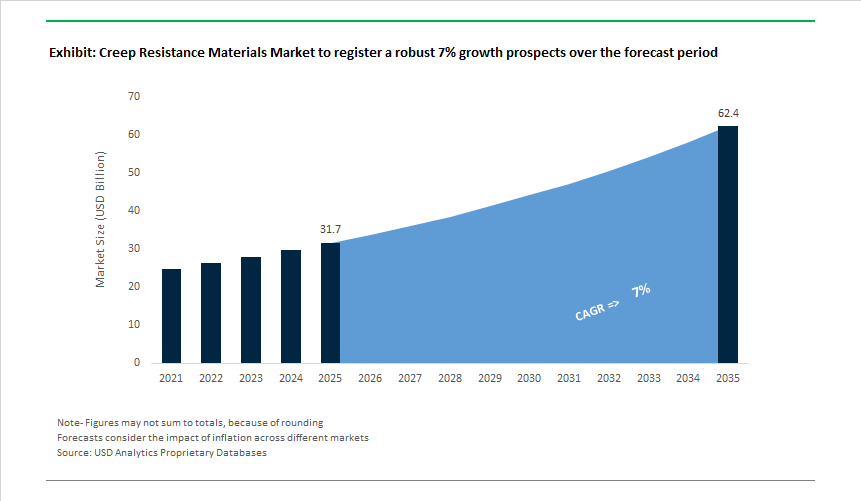

Creep Resistance Materials Market To Generate USD 62.4B (2035) With High-Temperature Alloys Powering Turbines & Ultra-Supercritical Plants

The Creep Resistance Materials Market is valued at USD 31.7 billion in 2025 and is projected to reach USD 62.4 billion by 2035, expanding at a 7.0% CAGR. Growth is being accelerated by the widespread adoption of nickel-based superalloys, ferritic-martensitic steels, and oxide-dispersion-strengthened (ODS) alloys proven to retain mechanical integrity during long-duration exposure at 600-1,100°C. OEMs such as GE, Mitsubishi Power, and Siemens Energy continue qualifying alloys like Inconel 740H, Haynes 282, Alloy 617, and Mar-M247 for advanced turbine sections because they maintain creep rupture life under stress levels exceeding 100 MPa at ≥700°C, enabling higher turbine firing temperatures and improved cycle efficiencies. In ultra-supercritical and A-USC power plants, commercially deployed materials such as T91, T92, Super 304H, HR6W, and Sanicro 25 demonstrate engineering lifetimes of 100,000 hours with ≤1% creep strain, forming the backbone of next-generation boiler tubes, headers, and steam piping.

Rapid adoption is also influenced by CSP receiver manufacturers, who require alloys able to withstand cyclic thermal shocks and creep deformation under molten-salt exposure, where alloys like Haynes 230 and Inconel 625 exhibit superior structural retention. In HPHT oil and gas environments, nickel alloys such as Inconel 718 and 725 continue to dominate wellhead, completion, and subsea hardware due to their ability to resist sulfidation, chloride-induced cracking, and time-dependent deformation at elevated pressures and temperatures. Parallelly, additive manufacturing OEMs have validated creep-resistant AM alloys-CMSX-4, Hastelloy X, and IN718 AM-grade-with post-HIP processing, enabling rotor-grade mechanical properties suitable for combustor liners, shrouds, and high-pressure turbine components.

Market Analysis: Consolidation, Ultra-High-Temp Alloys & Manufacturing Scale

The creep resistance materials sector recorded strategic expansions, product launches, and policy-driven funding that collectively accelerate demand for advanced superalloys and processing capacity. In December 2024, Bodycote completed an expansion of its Hot Isostatic Pressing (HIP) capacity in Europe, markedly increasing densification throughput for large additively manufactured superalloy components destined for aerospace and industrial gas turbines. The early months of 2025 saw policy and partnership moves: in March 2025, the U.S. Department of Energy released funding guidelines prioritizing materials for supercritical CO₂ power cycles, explicitly requiring alloys capable of creep resistance above 700°C at high pressures - a clear demand signal for both nickel-base alloys and advanced Cr-Mo steels.

Throughout 2025, product and capability announcements highlighted both material innovation and manufacturing scale-up. In May 2025, Siemens Energy partnered with university consortia to build Digital Twin models and sensor-driven methodologies to predict in-service creep damage for gas turbine blades - linking materials science with predictive asset management. Materials innovation accelerated in July 2025 when Haynes International launched HAYNES® 233®, a Ni-Co-Cr-Mo-Al alloy demonstrating superior creep strength and oxidation resistance to ~1,149°C, expanding applicability toward ultra-high temperature components. Industrial capacity followed: in September 2025, an Asian power generation firm commissioned a USD 150 million casting facility focused on high-grade Cr-Mo-V rotor components, underpinning supply security for advanced steam turbines. In October 2025, aerospace OEM integration of CMC manufacturers signalled a strategic shift toward ceramic matrix hot-Section components for the hottest zones, complementing superalloy use in rotating hardware. Finally, November 2025 saw leading superalloy producers introduce cobalt-based alloys for CSP receivers operating around 650°C, emphasizing corrosion resistance to molten salts and widening the market for creep-resistant specialty alloys.

The developments show the market moving in parallel on three tracks: high-temperature alloy chemistry (γ′ engineering and novel Co-based systems), production & post-processing scale (HIP expansions and dedicated casting plants), and digital/materials integration (Digital Twins and sensor analytics) -to meet the long life, high-temperature, and traceability requirements of modern power and aerospace assets.

Creep Resistance Materials Market: Trends and Opportunities

Coated Superalloys and Refractory Metal Composites Enable Higher Turbine Inlet Temperatures

The creep resistance materials landscape is being reshaped by the relentless push to raise turbine inlet temperatures (TIT) beyond 1,200°C in both aviation and industrial gas turbines, where even marginal efficiency gains translate into material performance becoming mission-critical. The focus has shifted from incremental alloy tuning to multi-layered material systems, combining advanced superalloys with protective coatings that suppress creep, oxidation, and grain-boundary degradation simultaneously. A defining inflection point occurred in December 2025 when NASA advanced its GRX-810 oxide-dispersion-strengthened (ODS) superalloy toward industrial licensing. GRX-810 demonstrated roughly 2× higher strength and nearly 1,000× longer creep life at ~1,093°C versus conventional nickel-based alloys by stabilizing grain boundaries against sliding—one of the dominant high-temperature creep mechanisms.

Parallel progress is evident in coating technologies. GE Aerospace has disclosed the deployment of next-generation Environmental Barrier Coatings (EBCs) incorporating rare-earth silicates, enabling metallic substrates to operate in environments approaching 1,315°C. These coatings act as diffusion barriers to oxygen and water vapor, which otherwise accelerate sub-surface oxidation and creep damage. At the alloy level, research presented during Superalloys 2024/2025 confirmed that newly developed wrought Ni-based systems with stable TiC and γ′ precipitates can suppress microstructural “rafting” at ~800°C, extending component life in exhaust and hot-section hardware. Comparative benchmarking in 2025 further showed that Ta-containing IN 792 forms more stable oxide scales than Rene 80 at ~1,050°C, data now being used to justify extended inspection intervals for high-pressure turbine blades in widebody engines such as the GEnx.

Enhanced Ferritic–Martensitic Steels Qualified for Generation IV Nuclear Systems

Creep-resistant materials are also central to the commercialization of Generation IV nuclear reactors, where components must survive decades of combined thermal stress, neutron irradiation, and cyclic loading. Enhanced ferritic–martensitic (FM) steels—particularly Grade 91 and 92—are emerging as anchor materials for reactor pressure boundaries and heat transport systems operating up to ~700°C. At the November 2025 technical meeting hosted by the International Atomic Energy Agency, ongoing qualification work highlighted how optimized nitrogen and vanadium additions in 9Cr-1Mo steels create fine precipitate “pinning” sites that inhibit dislocation climb, directly improving long-term creep rupture resistance.

Commercial validation is already underway. China’s HTR-PM at Shidaowan—now fully operational—demonstrates how creep-resistant steels and graphite enable sustained outlet temperatures near 750°C in high-temperature gas-cooled architectures. Looking beyond fission, fusion programs are accelerating materials testing. The International Fusion Materials Irradiation Facility is evaluating Reduced Activation Ferritic–Martensitic (RAFM) steels engineered to retain >100 MPa creep rupture strength after 10,000 hours at ~550°C, while minimizing long-lived radioactivity. Importantly, regulatory frameworks are evolving in parallel: 2025 updates to ASME III-NH and RCC-MRx codes formally integrated creep–fatigue interaction diagrams, allowing designers to quantify life expectancy in Gen IV components where steady-state creep and thermal cycling coexist.

Additive Manufacturing Unlocks Complex, Actively Cooled Creep-Resistant Components

Additive manufacturing (AM) is opening a structurally new opportunity for creep resistance materials by enabling geometry-driven thermal management rather than relying solely on alloy capability. Technologies such as Laser Powder Bed Fusion (L-PBF) and Laser Metal Deposition (LMD) allow the fabrication of transpiration-cooled and lattice-reinforced components with internal channels that would be impossible to machine conventionally. To support this shift, AM platform providers have co-developed alloys optimized for rapid solidification. Velo3D and EOS have qualified γ′-strengthened superalloy powders that remain weldable during printing, avoiding liquation cracking that historically limited AM adoption for high-temperature parts.

The operational payoff is already visible in service. Through CFM International, GE Aerospace has deployed additively manufactured fuel nozzles and combustor components in LEAP engines, where integrated cooling geometries deliver 15–20% improvements in thermal management, directly reducing creep-driving thermal gradients. In space propulsion, NASA Glenn Research Center is applying the GRCop-42 copper alloy in AM rocket engine liners, combining high thermal conductivity with creep resistance under cyclic regenerative cooling. Beyond new-build parts, aerospace OEMs are adopting “digital warehouse” strategies: in 2025, multiple defense contractors began using LMD for additive remanufacturing of worn turbine blade tips, restoring creep-resistant microstructures at roughly 40% of replacement cost, fundamentally changing spare-parts economics.

Hydrogen Combustion Drives Demand for H₂-Tolerant High-Temperature Materials

The transition toward hydrogen-fired gas turbines introduces a new materials frontier, as 100% hydrogen combustion produces higher flame temperatures, elevated water vapor content, and increased risk of hydrogen-induced cracking. These conditions amplify creep, oxidation, and grain-boundary degradation, forcing a rethink of hot-section materials. In 2025, Mitsubishi Power advanced validation of its H-25 and JAC-class turbines at the Takasago Hydrogen Park, requiring combustor liners and first-stage vanes fabricated from alloys capable of tolerating higher moisture-driven oxidation and flame velocities.

Alloy selection is converging around systems that combine creep strength with hydrogen tolerance. Haynes 282 has emerged as a leading candidate for hydrogen combustors, demonstrating stable creep performance up to ~1,000°C and resistance to steam-induced grain boundary depletion. Public funding is reinforcing this trajectory. In 2025, the U.S. Department of Energy expanded ARPA-E programs targeting hydrogen-tolerant high-temperature materials designed to block atomic hydrogen diffusion into metal lattices under pressure. Field validation is progressing incrementally: in June 2025, Mitsubishi Power Americas and Georgia Power completed 50% hydrogen blend testing at Plant McDonough-Atkinson, confirming that existing creep-resistant alloy architectures can accommodate high hydrogen fractions with limited hardware modification. These results position advanced creep resistance materials as a gating factor—not a bottleneck—in the path toward full hydrogen combustion by the end of the decade.

Creep Resistance Materials Market Share Analysis

Market Share by Alloy Chemistry: Chromium-Containing Alloys Form the Industry’s Thermal Backbone

Chromium-containing alloys account for approximately 35% of the global Creep Resistance Materials Market, reflecting their indispensable role in applications where long-term exposure to high temperatures and oxidative environments is unavoidable. This segment’s dominance is anchored in chromium’s ability to form a self-healing chromia (Cr₂O₃) oxide layer, which acts as a continuous protective shield against oxidation, scaling, and surface degradation—key mechanisms that accelerate creep deformation and premature failure. Unlike strength-only alloying elements, chromium directly enhances operational survivability, enabling components to retain dimensional and mechanical stability over decades of service. In power generation and industrial thermal systems, high-chromium alloys are routinely specified because they deliver predictable creep-rupture performance over operating lifetimes exceeding 100,000 hours, aligning with the long capital cycles of utilities and heavy industry. Market share is further reinforced by chromium’s cost-to-performance advantage, as chromium-rich alloys achieve the majority of the thermal and oxidation resistance benefits of exotic superalloys without the price volatility associated with scarcer elements such as niobium or molybdenum. Dimensional stability at elevated temperatures also plays a strategic role, as low thermal expansion reduces seal failures, bolt loosening, and mechanical distortion in turbines and pressure systems. Together, these attributes position chromium-containing alloys as the default material choice for mid-to-high temperature creep-critical environments, securing their leading share across power, industrial, and aerospace-adjacent applications.

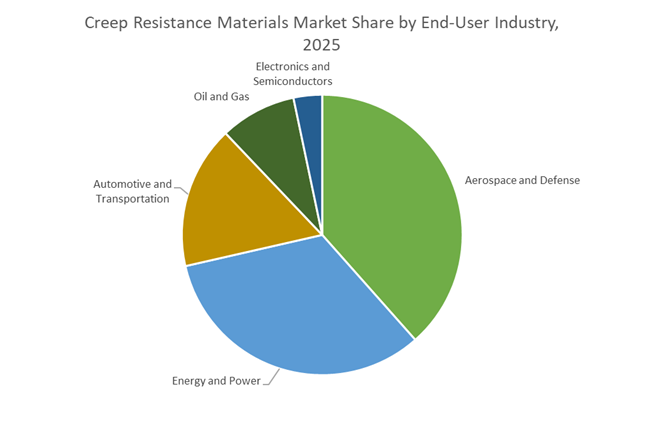

Market Share by End-User Industry: Aerospace and Defense Set the Performance Ceiling for Creep Resistance

The aerospace and defense sector represents roughly 35% of total demand in the Creep Resistance Materials Market, making it the single largest and most technologically demanding end-use industry. This leadership position is driven by a direct and uncompromising relationship between operating temperature, engine efficiency, and fuel economics, where higher thermal thresholds translate into measurable performance gains. Modern jet engines rely heavily on creep-resistant alloys, which now constitute a substantial portion of engine mass, particularly in hot-section components such as combustors and turbine blades where failure is not an option. Incremental improvements in creep resistance enable engines to operate at higher temperatures, delivering step-change fuel efficiency gains that compound across global airline fleets and defense aviation platforms. The market share of aerospace applications is further reinforced by the sector’s emphasis on predictable material behavior, as precisely modeled creep rates allow manufacturers and defense operators to implement condition-based maintenance strategies. This predictability reduces unplanned downtime, extends inspection intervals, and improves mission readiness—critical decision criteria for both commercial and military procurement programs. As aerospace OEMs continue to push thermal and efficiency boundaries, the sector remains the primary driver of demand for advanced creep-resistant materials, anchoring its dominant share in the global market.

Competitive Landscape: Alloy Makers, Integrators, and Thermal-Processing Specialists Driving Creep Performance

The competitive ecosystem for creep-resistant materials combines specialist alloy producers, fully integrated turbomachinery OEMs, high-purity melt processors, and global thermal-processing service providers. Differentiation hinges on proprietary alloy chemistries (γ′-engineered), advanced melting routes (VIM/VAR/ESR), HIP and heat-treatment capacity, AM qualification support, and domain expertise in corrosive/HPHT environments. Buyers prioritize suppliers who can demonstrate validated creep test data, traceable processing (including HIP and LCF screening), and in-service monitoring partnerships.

Haynes International - Proprietary Γ′-Strengthened Alloys For Ultra-High-Temperature Environments

Haynes International offers a family of high-performance alloys (notably HAYNES® 230® and the recently launched HAYNES® 233®) engineered for exceptional creep strength and oxidation resistance up to ~1,149°C. The company’s portfolio targets industrial gas turbines, CSP receivers, and corrosive processing environments where sulfidation and molten salt exposure are concerns. Haynes’ R&D focus on γ′-strengthened chemistries and wrought superalloy forms positions it as a go-to supplier for components requiring a balance of creep life and oxidation resistance, while its application support helps customers qualify alloys across demanding service conditions.

Siemens Energy - In-House Metallurgy and Digital Twin Integration For Turbine Life Extension

Siemens Energy combines proprietary high-creep-strength nickel alloys and advanced coating systems with digital engineering capabilities to optimize hot-Section component life. The company’s investment in Digital Twin modeling and sensor analytics enables predictive creep damage assessment, informing material selection and condition-based maintenance strategies for multi-decade turbine lifespans. Siemens’ hydrogen-ready turbine roadmap further demands creep-optimized geometries and internal cooling designs-areas where Siemens’ integrated metallurgy, design, and service capabilities provide competitive advantage to utilities and OEM partners.

ATI Inc. (Allegheny Technologies) - Integrated Melting and Forging For Aerospace-Grade, Low-Creep Superalloys

ATI is a vertically integrated specialty metals producer with advanced melting (VIM/VAR/ESR) and forging capabilities that produce high-purity nickel, titanium, and cobalt superalloys for rotating discs, shafts, and critical aero engine components. Its control over thermomechanical processing enables tailored microstructures that resist creep under combined high temperature and centrifugal stress. ATI’s product formats-ingots, billets, and precision forgings-are essential to OEMs requiring verified creep performance and minimal defect populations in high-stress rotating components.

Bodycote Plc - Global HIP and Heat-Treatment Network That Maximizes Creep Life Of AM and Cast Parts

Bodycote operates a global network of more than 150 facilities providing HIP and specialized heat treatments essential for densifying additively manufactured superalloy parts and improving stress-rupture/LCF properties. Its Powdermet® integration of AM with HIP enables near-net-shape production of isotropic, creep-resistant superalloy components. Bodycote’s expanded HIP capacity and process know-how are critical enablers for manufacturers seeking to qualify large, complex geometries for long service lives in aerospace and power generation, while its service model supports traceability and certification needs for safety-critical parts.

India’s creep resistance materials market is being structurally reshaped by the third round of the Production Linked Incentive scheme (PLI 1.2), which explicitly prioritizes superalloys, titanium alloys, and advanced specialty steels for defense, aerospace, and space applications. By channeling fiscal incentives toward high-temperature and stress-tolerant materials, the policy is shifting India away from dependence on imported nickel-based superalloys toward localized production and metallurgy know-how. Investment traction from earlier PLI rounds has already translated into capacity build-out, skilled employment, and technology transfer across the domestic alloy ecosystem. A critical inflection point in 2025 was the successful development of Titan 31 ELI and cobalt-free maraging steel by Mishra Dhatu Nigam Limited, materials engineered to retain mechanical integrity under sustained thermal and mechanical loads. This positions India as an emerging hub for creep-resistant alloys tailored to launch vehicles, gas turbines, and advanced propulsion systems.

United States’ Energy Security Agenda and Defense-Grade Superalloy Supply Chains

The United States creep resistance materials market is increasingly aligned with national energy security and defense preparedness. Federal funding streams under the Bipartisan Infrastructure Law are supporting high-temperature material processing for advanced transmission systems and next-generation turbines, directly expanding demand for nickel-based superalloys, refractory metals, and oxide dispersion strengthened alloys. The inclusion of rhenium, tungsten, and related superalloy constituents on the Department of Defense’s 2025 Critical Minerals List underscores a strategic emphasis on materials capable of withstanding extreme thermal stress in jet engines and hypersonic platforms. On the industrial front, ATI (Allegheny Technologies) is expanding aerospace- and defense-focused capacity, reflecting strong downstream pull from turbine manufacturers and defense OEMs. The U.S. market is therefore characterized by premium-grade, domestically sourced creep-resistant materials rather than volume-led growth.

China’s “New Materials” Sovereignty and Scale-Driven Capability Expansion

China remains a dominant force in creep resistance materials through a coordinated push for self-sufficiency under the concluding 14th Five-Year Plan. Government-backed investment into “New Materials” R&D centers is accelerating breakthroughs in ultra-pure non-ferrous metals, nickel-based superalloys, and refractory alloys for nuclear reactors, aerospace propulsion, and maritime engineering. Industrial policy emphasizes replacement of legacy capacity with high-tech production lines capable of tighter microstructural control, essential for long-term creep resistance at elevated temperatures. By targeting sustained annual growth in non-ferrous metals while embedding smart manufacturing systems, China is strengthening its ability to supply both domestic mega-projects and export markets with high-performance creep-resistant materials.

European Union (Germany & Spain): Decarbonization-Driven Alloy Innovation

Across the European Union, creep resistance materials development is tightly coupled with decarbonization and energy-efficiency goals. Reforms to the Research Fund for Coal and Steel are increasing funding availability for high-temperature alloy research that enables turbines to operate at higher efficiencies and lower emissions. Germany’s industrial base is leveraging this framework to integrate hydrogen-ready steelmaking and advanced alloy design, while Spain has emerged as a research hotspot for microstructural optimization of superalloys. Notably, work at IMDEA Materials Institute has demonstrated scalable methodologies to control grain structure in nickel-based superalloys, directly improving creep performance in additively manufactured components. Europe’s competitive edge lies in coupling materials science innovation with climate policy compliance.

South Korea’s MPE Roadmap and Localized High-Temperature Alloys

South Korea’s creep resistance materials market is being driven by its Materials, Parts, and Equipment (MPE) roadmap, which aims to localize critical technologies across aerospace, medical, and defense supply chains. Substantial planned investment through 2030 is accelerating R&D into special carbon steels and superalloys capable of meeting stringent thermal stability requirements. By integrating AI-driven material discovery with localized production, South Korea is reducing dependence on imported high-temperature alloys while positioning itself as a supplier of precision-engineered creep-resistant materials for advanced industrial applications.

Japan’s Materials DX Platform and Data-Driven Extreme-Environment Materials

Japan continues to lead in precision metallurgy through the expansion of its Materials Research DX Platform, which combines data science, simulation, and experimental metallurgy. The 2025 focus on materials that remain stable under extreme temperatures aligns with Japan’s long-term “Society 5.0” and carbon-neutral objectives. By targeting ultra-wide-bandgap semiconductors, high-temperature dielectrics, and thermally stable alloys, Japan is strengthening its role as a developer of next-generation creep-resistant materials for advanced electronics, power systems, and aerospace components. The market emphasis is on reliability, predictability, and long lifecycle performance rather than rapid capacity expansion.

National Strategic Development Matrix: Creep Resistance Materials Market (2025)

Creep Resistance Materials Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

Key 2025 Policy or Investment Trigger

|

Core Application Focus

|

|

India

|

PLI-led self-reliance

|

PLI 1.2 incentives for superalloys

|

Space, defense, high-temperature turbines

|

|

United States

|

Energy & defense security

|

DOE funding and Critical Minerals List

|

Aerospace engines, power infrastructure

|

|

China

|

New materials sovereignty

|

14th Five-Year Plan R&D expansion

|

Nuclear, aerospace, maritime engineering

|

|

EU (Germany & Spain)

|

Decarbonization & efficiency

|

RFCS reform and alloy R&D grants

|

Turbines, low-emission power systems

|

|

South Korea

|

MPE localization

|

2026–2030 MPE investment roadmap

|

Aerospace and defense components

|

|

Japan

|

Materials DX leadership

|

Data-driven metallurgy platforms

|

Extreme-environment electronics & alloys

|

Creep Resistance Materials Market Report Scope

Geopolymers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.6 Billion

|

|

Market Size (2035)

|

$138 Billion

|

|

Market Growth Rate

|

28.1%

|

|

Segments

|

By Raw Material Type (Fly Ash-Based, Slag-Based, Metakaolin-Based, Natural Aluminosilicate-Based, Hybrid Systems), By Product Form (Geopolymer Binders, Geopolymer Concrete, Precast Elements, Mortars & Grouts, Coatings & Adhesives), By Application (Building & Construction, Infrastructure & Transportation, Marine Structures, Repair & Rehabilitation, Industrial, Oil & Gas & Mining, Composites, Art & Decoration), By Curing Method (Ambient Curing, Heat Curing)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Schlumberger Limited, CEMEX S.A.B. de C.V., Wagners Holding Company, Imerys S.A., Tata Steel Limited, PCI Augsburg GmbH, Zeobond Pty Ltd., Geopolymer Solutions LLC, banah UK Ltd., Heidelberg Materials AG, Milliken & Company Inc., Coromandel International Limited, Corning Incorporated

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Creep Resistance Materials Market Segmentation

By Material Type

- Metals and Alloys

- Nickel-Based Superalloys

- Cobalt-Based Superalloys

- Iron-Based Superalloys

- Refractory Metals

- Titanium Alloys

- Ceramics and Composites

- Polymers

By Alloy Chemistry

- Chromium-Containing Alloys

- Niobium-Strengthened Alloys

- Titanium/Aluminum-Strengthened Alloys

- Molybdenum-Containing Alloys

By Application Temperature

- Low Temperature

- Medium Temperature

- High Temperature

- Ultra-High Temperature

By End-User Industry

- Aerospace and Defense

- Energy and Power

- Automotive and Transportation

- Oil and Gas

- Electronics and Semiconductors

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Creep Resistance Materials Market

- Haynes International, Inc.

- Carpenter Technology Corporation

- ATI Inc.

- Precision Castparts Corp.

- AMETEK, Inc.

- VDM Metals GmbH

- Kyocera Corporation

- CoorsTek, Inc.

- General Electric Company

- Tata Steel Limited

- Morgan Advanced Materials plc

- Aperam S.A.

- Doncasters Group

- Avicennna Co., Ltd.

*- List not Exhaustive