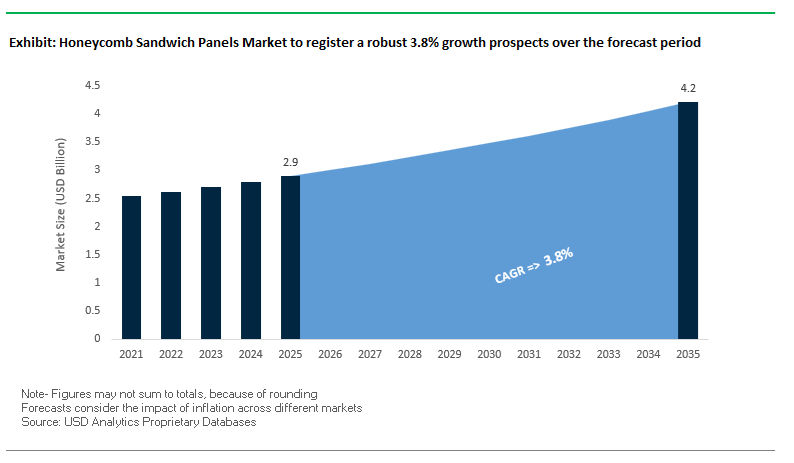

The global Honeycomb Sandwich Panels Market is projected to grow from USD 2.9 billion in 2025 to USD 4.2 billion by 2035, registering a CAGR of 3.8% (2025–2035). For aerospace OEMs, rail vehicle builders, marine yards, and architectural façade contractors, the key buying decision is not just cost per square meter but specific stiffness, FST compliance, and structural efficiency under stringent weight and safety constraints.

Recent developments in the honeycomb sandwich panels market underline a shift toward thermoplastic composites, circularity, and high-rate aerospace production. In December 2025, Toray Advanced Composites completed NCAMP qualification for its LMPAEK™ TC1225/T300 thermoplastic composite, a milestone that de-risks the use of thermoplastic skins and cores for aerospace honeycomb structures and supports faster, out-of-autoclave manufacturing cycles. In November 2025, the EuReComp consortium showcased the ROCCA cabin demonstrator at K-Messe, placing circular composites and end-of-life recycling at the center of future interior panel designs and directly influencing how honeycomb core materials will be specified for recyclability, repairability, and reduced lifecycle emissions.

Strategic collaborations are reinforcing honeycomb adoption in next-generation mobility. In October 2025, Hyundai Motor Group and Toray announced a strengthened partnership to develop advanced composite materials for future mobility platforms, signaling broader deployment of aluminum and thermoplastic honeycomb sandwich structures in electric vehicles, autonomous shuttles, and new urban air mobility concepts. Earlier, in June 2025, Toray, Daher, and TARMAC launched an End-of-Life Aerospace Recycling Program for commercial aircraft, focusing on thermoplastic composites and catalyzing the development of recyclable PP and PEI honeycomb cores. The aligns with OEM decarbonization roadmaps and pushes panel suppliers to offer full lifecycle traceability and recycling solutions for cores and skins alike.

On the materials innovation side, Hexcel introduced Flex-Core® HRH-302 mid-temperature honeycomb in May 2025, designed to withstand service temperatures up to 450°F and bridge the cost–performance gap between standard phenolic honeycombs and high-temperature specialty cores. The enables expanded use in engine nacelles and hot-zone structures where higher service temperatures and FST compliance are critical. Strategically, Hexcel reinforced its role in high-rate aerospace composites at the Carbon Fiber 2024 Conference (October 2024) by emphasizing vertical integration across honeycomb, prepregs, and carbon fiber—essential for upcoming OEM build-rate ramps. Parallelly, Gurit’s H1 2025 restructuring, which delivered an adjusted operating margin of 5.7% (up from 5.4% in H1 2024), shows that core material suppliers are tightening their portfolios around profitable wind energy and marine structural core applications, where “honeycomb-like” core architectures compete with PVC, PET, and balsa.

Innovation is also happening at the form factor level. In late 2024, Euro-Composites highlighted its 3-dimensional formable Nomex® honeycomb, enabling complex, non-flat geometries for aircraft bulkheads and curved structural elements, reducing assembly steps and manual forming. The complements Plascore’s and others’ growing focus on specialized polypropylene and polycarbonate honeycomb cores for resin infusion, industrial, and architectural applications. Overall, the market is transitioning from commodity sandwich panels to highly engineered, application-specific honeycomb systems that combine FST compliance, recyclability, thermoplastic integration, and high-rate manufacturability.

Honeycomb sandwich panels deliver a stiffness-to-weight ratio 40–50% higher than conventional foam cores or solid laminates, making them the default solution in aircraft floor panels, cabin interiors, railway bulkheads, and high-performance transport structures. Engineers increasingly specify aramid/Nomex® honeycomb or aluminum honeycomb cores that balance shear modulus, core weight fraction, and compatibility with carbon fiber skins to meet demanding deflection, vibration, and fire performance targets.

Current technical benchmarks show that standard aerospace-grade aramid honeycomb achieves shear modulus levels around 6 ksi (41 MPa) in the L-direction, while optimized core weight fractions of 50–66.7% of finished panel weight deliver maximum flexural rigidity. For long-life CFRP structures, non-metallic aramid cores eliminate galvanic corrosion risk and account for over half of non-metallic aerospace composite core usage, strengthening the business case for multi-decade service in harsh environments.

- High specific strength and stiffness: Honeycomb panels deliver 40–50% higher stiffness-to-weight ratio than foam or solid laminates, enabling aggressive mass reduction in aerospace, high-speed rail, and marine structures.

- Aerospace-grade shear performance: Typical Nomex®/aramid honeycomb (1/8", 3.0 PCF) offers a plate shear modulus of 6 ksi (41 MPa) in the L-direction, supporting stringent deflection criteria for aircraft floors and cargo liners.

- FST and flammability compliance: Aluminum honeycomb sandwich panels for aircraft cabins are engineered to comply with FAA CFR 25.853 Appendix F requirements, ensuring flame, smoke, and toxicity (FST) performance for commercial aviation.

- Optimized core-to-skin weight ratio: For maximum flexural efficiency, the core typically contributes 50–66.7% of total panel weight, guiding core density and skin thickness selection for weight-critical designs.

- Corrosion-free integration with CFRP skins: Nomex®/aramid cores provide full galvanic corrosion resistance against carbon fiber skins, supporting their use in over 50% of non-metallic aerospace composite applications in marine, aerospace, and defense environments.

Honeycomb Sandwich Panels Market Share Analysis

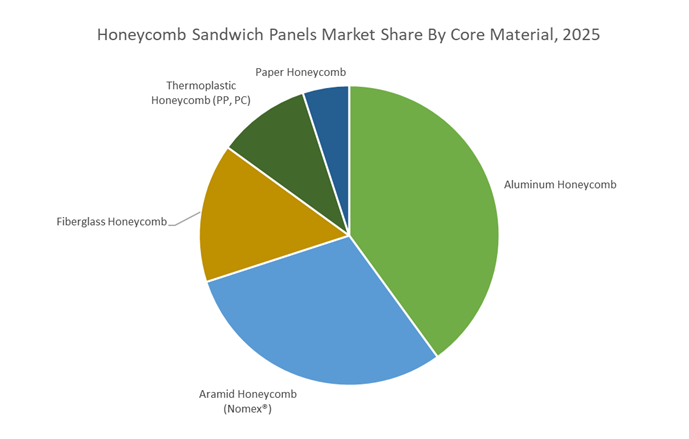

Market Share by Core Material: Aluminum Honeycomb Dominates Through Exceptional Strength-to-Weight Efficiency and Multi-Functional Performance

Aluminum honeycomb maintains the highest 40% share in the Honeycomb Sandwich Panels Market due to its unmatched balance of structural performance, low density, and multifunctional physical properties that are indispensable across aerospace, transportation, marine, and industrial applications. The inherent geometry of the hexagonal honeycomb structure allows aluminum cores to behave like a network of miniature I-beams, resulting in extraordinarily high specific stiffness and strength-to-weight ratios that far exceed those of polymeric or paper-based cores. This performance advantage enables panels to endure substantial compressive and shear loads while keeping weight to an absolute minimum—an essential requirement in sectors where mass reduction drives energy efficiency and payload optimization. Aluminum honeycomb’s dominance is further reinforced by its non-combustibility and corrosion resistance, with alloys such as 5052 and 5056 meeting stringent fire regulations, including certain A2 classifications in European building standards. Its superior thermal and electrical conductivity, which polymeric cores cannot replicate, makes it indispensable for applications where heat spreading, thermal management, or EMI mitigation is required—such as satellite structures, avionics enclosures, electronic heat sinks, and high-performance industrial equipment. These combined attributes—mechanical reliability, fire resistance, heat dissipation capability, and broad design flexibility—solidify aluminum honeycomb as the most widely adopted and strategically essential core material in the global honeycomb sandwich panel ecosystem.

Market Share by End-Use Industry: Aerospace & Defense Leads Through Critical Lightweighting Demands and Structural Safety Requirements

Aerospace & Defense commands a dominant 50% market share, reflecting the industry’s unmatched reliance on honeycomb sandwich panels to achieve mission-critical performance objectives in aircraft, spacecraft, and defense structures. Weight reduction is a core engineering priority: lowering the empty weight of an aircraft by even a few hundred kilograms can yield significant improvements in fuel efficiency, payload capacity, range, and CO₂ emissions reduction. Honeycomb sandwich panels—used extensively in flooring systems, bulkheads, nacelles, wings, stabilizers, and control surfaces—enable these gains by providing exceptional rigidity at a fraction of the mass of solid materials. Their very high torsional stiffness is particularly important for aerodynamic components such as flaps, ailerons, and wing edges, where insufficient stiffness can trigger aerodynamic flutter, a phenomenon that can escalate into catastrophic structural failure at high airspeeds.

In defense applications, honeycomb structures play an equally strategic role. Aluminum honeycomb cores can be engineered to undergo controlled crushing during high-impact or crash events, providing highly effective energy absorption and enhancing occupant protection in military vehicles, unmanned platforms, and protective housings. Their predictable failure modes and high specific energy absorption make them ideal for safeguarding sensitive avionics, munitions, or mission systems. With aerospace OEMs targeting aggressive lightweighting goals, expanding composite-airframe platforms, and rising defense modernization programs globally, honeycomb sandwich panels remain a foundational material technology—ensuring this segment continues to lead market share with strong long-term growth momentum.

Country Analysis: Global Honeycomb Sandwich Panel Development Hubs

United States: Aerospace-Grade Honeycomb Innovation Accelerating Military, Commercial, and Space Applications

The United States remains the global epicenter for aerospace-grade Honeycomb Sandwich Panels due to its concentration of major OEMs—including Boeing, Lockheed Martin, and Northrop Grumman—and a deeply integrated supply chain for Nomex®, aluminum, and advanced non-metallic cores. The sector continues to benefit from strong innovation activity. In 2025, Hexcel Corporation introduced the Flex-Core® HRH-302 Mid-Temperature Honeycomb Core, designed for complex curvature and thermal stability in aircraft interiors, flight structures, and high-performance aerostructures. This development reflects the industry's shift toward high-formability, lightweight composite cores that reduce component count and enhance manufacturability for next-generation aircraft.

Defense and space programs are further advancing U.S. honeycomb core demand. In December 2024, Hexcel partnered with Boeing to test specialized honeycomb materials for the MQ-25 Stingray unmanned tanker, reinforcing the strategic importance of impact-resistant, lightweight structural cores in high-stress defense platforms. Additionally, acoustic technology is emerging as a major differentiator: Hexcel’s HexWeb® Acousti-Cap® technology integrates acoustic-dampening structures into honeycomb panels to reduce engine noise without compromising structural integrity—an essential requirement for commercial and military aircraft. U.S. suppliers are also scaling global production lines for aluminum and aramid (Nomex®) cores to support long-term contracts across aerospace, defense, and space. Honeycomb cores are increasingly deployed in launch vehicle structures, solar array panels, and satellite modules, where ultra-high strength-to-weight ratios are mandatory. These capabilities firmly position the U.S. as the most technically advanced honeycomb materials hub worldwide.

China: High-Speed Rail Growth and Expanding Aluminum Honeycomb Capacity Driving Mass-Market Adoption

China is rapidly emerging as one of the world’s largest consumers of aluminum honeycomb sandwich panels, supported by unparalleled investment in High-Speed Rail (HSR) networks, domestic aircraft programs, and urban infrastructure development. The country’s rail transit segment is the single highest-volume consumer of aluminum honeycomb panels, driven by regulatory mandates requiring 15–25% weight reduction across train cars to enhance energy efficiency, minimize track wear, and increase operational life. Honeycomb panels are widely used for flooring, bulkheads, wall partitions, and luggage racks, replacing traditional sheet metal while improving fire resistance, mechanical stability, and crash-energy absorption.

China’s urban expansion is also accelerating the use of honeycomb materials in architectural cladding, building facades, ceilings, and interior panels, where lightweight fire-resistant materials are prioritized for safety and longevity. Manufacturers are scaling production capacity to offer high-volume composite aluminum honeycomb panels that meet national requirements for thermal insulation, flame retardancy, and structural rigidity. In parallel, government green-building incentives are increasing the adoption of energy-efficient honeycomb panels in commercial and public infrastructure. With strong localization policies, expanding production lines, and aggressive growth in EV, rail, and aerospace industries, China is consolidating its role as the world’s largest mass-market producer of aluminum honeycomb sandwich structures.

Europe (Germany/France): Aramid/Nomex® Honeycomb Leadership Supported by Strict FST Standards and Recyclable Thermoplastic Innovations

Europe—particularly Germany and France—remains a global center of excellence for aramid-based (Nomex®) honeycomb cores, driven by the region’s strict Fire, Smoke, and Toxicity (FST) regulations for aviation and public transport. European aerospace OEMs such as Airbus specify phenolic-bonded Nomex® honeycomb cores to comply with FAR 25.853 and other stringent flame-resistance requirements for aircraft interiors, including galleys, ceilings, sidewalls, and floor panels. These requirements create a stable, high-value market for aramid honeycomb suppliers.

Sustainability-driven innovation is reshaping the European market. In September 2024, Diab Group launched a fully recyclable thermoplastic honeycomb sandwich panel, engineered for high mechanical strength, superior fire performance, and reduced weight—designed specifically for next-generation aerospace cabin structures. This aligns with new EU mandates emphasizing recyclability, circular materials, and reduced environmental footprint in transportation manufacturing. Beyond aerospace, European high-speed rail operators continue to adopt aluminum honeycomb interiors to enhance passenger comfort through sound insulation and improved durability at speeds exceeding 300 km/h.

Europe also benefits from highly advanced manufacturing capabilities. Industry leaders such as Euro-Composites S.A. and Hexcel operate state-of-the-art facilities for producing precision-machined Nomex® honeycomb components, supplying major Airbus programs. This ecosystem of precision manufacturing, FST compliance expertise, and thermoplastic recyclability leadership ensures Europe’s continued role as a top-tier innovation hub for honeycomb sandwich panel technologies.

Canada: Niche Leadership in Custom Honeycomb Structures and Specialized Composite Applications

Canada plays a strategic role in the honeycomb sandwich panels market through its focus on custom-engineered composite structures serving aerospace, defense, and specialized transportation. Canadian manufacturers frequently produce customized honeycomb configurations using Kevlar®, Nomex®, and aerospace-grade aluminum, engineered for high-load-bearing applications such as military vehicle armor, UAV airframes, helicopter components, and ruggedized transport systems. These solutions cater to customers requiring bespoke mechanical performance, enhanced durability, and superior impact resistance, distinguishing Canada as a premium niche supplier rather than a volume producer.

Academic institutions and research organizations—including those funded by the National Research Council of Canada (NRC)—actively support the market with advanced R&D in bonding technologies, adhesive formulations, delamination resistance, and fatigue performance. Research collaborations are exploring improved core–skin adhesion, environmental durability, and manufacturing methods for honeycomb panels used in extreme environments such as Arctic climates, offshore platforms, and military field operations. This combination of customized production capabilities and research-intensive innovation positions Canada as a specialist hub for high-performance honeycomb sandwich panels across defense, aerospace, and critical infrastructure markets.

Competitive Landscape: Leading Honeycomb Sandwich Panel and Core Material Suppliers

The competitive landscape of the Honeycomb Sandwich Panels Market is characterized by a small group of vertically integrated aerospace composite majors and specialized honeycomb/core producers. These players differentiate themselves through material breadth (Nomex®, Kevlar®, glass, carbon, aluminum, PP, PC), global manufacturing scale, NCAMP and FAA qualification portfolios, and value-added services including core kitting, ready-to-install panels, and recycling programs. Hexcel Corporation remains a benchmark in aerospace honeycomb materials, while Euro-Composites, Plascore, Toray Advanced Composites, Gurit, and Collins Aerospace address complementary niches spanning rail, space, wind energy, marine, industrial, and aircraft interiors.

Hexcel offers one of the broadest honeycomb core portfolios in the market, including HexWeb® Nomex® and HexWeb® aluminum cores (3003, 5052, 5056 alloys) that support virtually every major commercial and military aircraft program. Its competitive edge comes from vertical integration, spanning carbon fiber, prepregs, and honeycomb production, enabling unified material data, NCAMP qualification, and consistent performance across the sandwich structure value chain. The launch of Flex-Core® HRH-302 in May 2025 targets mid-temperature aerospace applications, with service temperatures up to 450°F, making it ideal for engine nacelles and near-hot-zone structures that must still achieve stringent FST compliance. Hexcel also provides specialized products including HexWeb CR III crush-core for energy absorption in crash structures and rotor blade protection, reinforcing its leadership in energy-absorbing and structural honeycomb composites.

Euro-Composites operates from three key locations in Luxembourg, Germany, and the USA, with a combined production area of over 54,800 m², serving the rail, space, and aviation markets. The company manufactures honeycomb cores in five distinct materials—Nomex®, Kevlar®, glass fiber, carbon fiber, and aluminum (3003, 5052, 5056)—allowing engineers to tailor weight, stiffness, and environmental resistance to specific applications. A strategic >USD 80 million supply contract with EFW (Airbus/ST Engineering), announced in February 2023, underpins long-term supply of honeycomb products for Airbus floor panels and freighter conversion programs. Euro-Composites also operates a large panel press capable of producing sandwich panels up to 15,000 mm (590 inches) in length, giving it a strong competitive position in large-format rail car, aircraft, and infrastructure structures.

Plascore is expanding its aerospace and industrial honeycomb business, supported by a USD 6 million investment in a 73,500-square-foot facility in Zeeland, Michigan, to meet rising demand for aramid honeycomb cores. The company differentiates itself with advanced polypropylene honeycomb products, including PP Infusion Grade cores engineered specifically for Lite RTM and resin infusion processes, capable of achieving low resin uptake (400 g/m²) and resulting in exceptionally lightweight marine and truck body panels. Plascore is also a major supplier of aluminum honeycomb cores used in laser cutting tables, flow straighteners, and clean room ceilings, leveraging aluminum’s high compressive strength and thermal conductivity. Additionally, it is one of the few producers of polycarbonate (PC) honeycomb cores, widely used in lighting diffusion, wind tunnels, and architectural skylights, strengthening its footprint in non-structural and optical honeycomb applications.

Toray Advanced Composites focuses on high-performance thermoplastic and thermoset prepregs, including Torayca™ P2302 carbon fiber systems, which are frequently co-cured or bonded with honeycomb cores to produce certified aerospace sandwich panels. The company’s LMPAEK™ TC1225/T300 thermoplastic system achieved NCAMP qualification in December 2025, enabling OEMs to deploy out-of-autoclave (OOA) and high-rate processing for honeycomb structures—critical for urban air mobility (UAM) and next-generation aircraft. Toray is also a key participant in End-of-Life aerospace recycling initiatives launched in June 2025 alongside Daher and TARMAC, aimed at closing the loop on thermoplastic composites and driving development of recyclable honeycomb cores. Its strategic collaboration with Hyundai Motor Group (October 2025) further extends honeycomb and composite adoption into automotive and future mobility platforms, emphasizing lightweight, high-specific-strength sandwich solutions.

Gurit is a recognized leader in structural core materials—including PVC, PET, and balsa—supplying “honeycomb-like” sandwich solutions for large rotor blades, marine hulls, and industrial structures. While its core emphasis is on foam-based cores rather than classic hexagonal honeycomb, the company competes directly in the lightweight sandwich panel market, particularly for wind energy and marine composites where large, integrated core kits are required. Following a strategic restructuring, Gurit delivered an adjusted operating profit margin of 5.7% in H1 2025, up from 5.4% in H1 2024, signaling improved focus on high-margin core materials and specialized core kits. Its Core Kit Solutions, which include pre-cut, marked, and packaged cores (including aramid honeycomb where specified), can reduce customer material waste and labor by up to 30%, reinforcing its value proposition in lean manufacturing and automated lay-up environments.

Collins Aerospace is a major Tier 1 supplier of honeycomb sandwich panels for aircraft interiors, marketed under brands including aeroMETAL™ aluminum and Nomex-based honeycomb panels. These panels are widely used in aircraft flooring, galleys, lavatories, and cabin monuments, where tight tolerances, FST compliance, and weight control are essential. Collins manufactures large-format panels up to 60 × 144 inches with thickness tolerances as tight as ±0.010 inches, enabling efficient integration into high-rate airframe assembly lines with minimal shimming and rework. The company also integrates honeycomb cores with in-house composite skins to supply ready-to-install sandwich structures, reducing integration complexity for OEMs. Backed by extensive FAA and EASA Part 21 certifications for composite repair and overhaul, Collins Aerospace offers a full lifecycle solution for design, production, and MRO of honeycomb-based aircraft components.

Honeycomb Sandwich Panels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2035)

|

$4.2 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Core Material (Aluminum Honeycomb, Aramid Honeycomb, Fiberglass Honeycomb, Thermoplastic Honeycomb, Paper Honeycomb), By Skin Material/Facing (Aluminum Sheets/Foil, CFRP, GFRP, Stainless Steel, High-Pressure Laminate, Natural Stone/Veneer), By End-Use Industry (Aerospace & Defense, Transportation, Construction & Infrastructure, Marine, Wind Energy), By Panel Function (Structural Panels, Non-Structural/Decorative Panels, Acoustic Panels, Fire-Resistant Panels, Energy Absorption Components), By Product Form (Flat Panels, Contour/Curved Panels, Engineered Core Blocks, Ready-to-Bond Kits)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hexcel Corporation, Toray Advanced Composites, Euro-Composites S.A., The Gill Corporation, Plascore Inc., Schweiter Technologies AG (3A Composites), Diab Group, EconCore N.V., Foshan Liming Honeycomb Composite Material Co. Ltd., Safran S.A., Encocam Ltd., Toray Industries Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Honeycomb Sandwich Panels Market Segmentation

By Core Material

- Aluminum Honeycomb

- Aramid Honeycomb

- Fiberglass Honeycomb

- Thermoplastic Honeycomb (PP, PC)

- Paper Honeycomb

By Skin Material (Facing)

- Aluminum Sheets/Foil

- Carbon Fiber Reinforced Polymer (CFRP)

- Glass Fiber Reinforced Polymer (GFRP)

- Stainless Steel

- High-Pressure Laminate (HPL)

- Natural Stone/Veneer

By End-Use Industry

- Aerospace & Defense

- Transportation (Rail, Automotive)

- Construction & Infrastructure

- Marine

- Wind Energy

By Panel Function

- Structural Panels

- Non-Structural / Decorative Panels

- Acoustic Panels

- Fire-Resistant Panels

- Energy Absorption Components

By Product Form

- Flat Panels

- Contour / Curved Panels

- Engineered Core Blocks

- Ready-to-Bond Kits

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Honeycomb Sandwich Panel Manufacturers

- Hexcel Corporation

- Toray Advanced Composites

- Euro-Composites S.A.

- The Gill Corporation

- Plascore, Inc.

- Schweiter Technologies AG (3A Composites)

- Diab Group

- EconCore N.V.

- Foshan Liming Honeycomb Composite Material Co. Ltd.

- Safran S.A.

- Encocam Ltd.

- Toray Industries, Inc.

*- List not Exhaustive