Market Overview: Lightweight Sandwich Structures and Multi-Material Adoption Propel the Global Honeycomb Core Materials Market

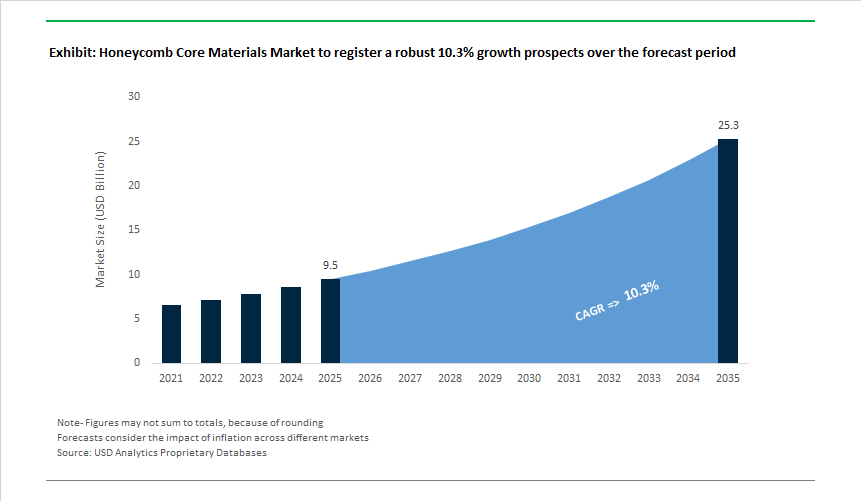

The Honeycomb Core Materials Market is valued at USD 9.5 billion in 2025 and is projected to reach USD 25.3 billion by 2035, expanding at a 10.3% CAGR as lightweight sandwich construction becomes a design default rather than a weight-saving option across aerospace, rail, automotive, and emerging electric mobility platforms. Honeycomb cores are increasingly specified not only for mass reduction, but for their ability to deliver high bending stiffness, predictable energy absorption, acoustic damping, and manufacturability at scale, all of which directly influence system performance and regulatory compliance.

Material choice continues to define value concentration. Aluminum honeycomb remains the backbone of the market, supported by decades of qualification in commercial and military aerospace, where stiffness-to-weight efficiency, thermal stability, and long-term durability under cyclic loading are non-negotiable. Its continued dominance reflects the risk profile of aircraft programs, where certified materials with known fatigue and damage-tolerance behavior remain preferred. At the same time, thermoplastic honeycomb structures - particularly polypropylene-based systems - are gaining rapid traction in ground transportation, rail interiors, and EV battery enclosures. Their recyclability, moisture resistance, and compatibility with circular-economy design frameworks are increasingly aligned with OEM sustainability mandates and end-of-life regulations.

Manufacturing dynamics are evolving alongside application requirements. Expansion-based honeycomb fabrication continues to account for the majority of global output, underpinned by its cost efficiency and suitability for large-format panels. However, automated continuous thermoplastic processing and additive manufacturing approaches are maturing for applications that require complex geometries, variable cell architectures, and rapid design iteration. These newer processes enable localized reinforcement, integrated features, and shorter development cycles, making them attractive for automotive platforms and modular interior systems where customization and volume coexist.

Beyond structural performance, functional integration is becoming a key differentiator. Honeycomb cores with engineered permeability and acoustic septa are increasingly specified to meet tightening noise and vibration regulations, particularly in aircraft engine nacelles, cabin panels, and high-speed rail interiors. This shift reflects a broader trend toward multifunctional core materials that combine structural support with NVH mitigation, fire performance, and thermal management. As lightweighting targets intensify and sustainability criteria harden, honeycomb core materials are evolving from passive structural fillers into engineered platforms central to next-generation mobility and infrastructure design.

Market Analysis: Product Launches, JV Scale-Ups and Aerospace/Automotive Partnerships Shaping Demand Outlook

Recent development activity highlights both supply-side scaling for aerospace programs and a diversification into thermoplastic, automotive and space markets. In December 2022 Hexcel and Toray launched a joint venture to shore up Europe’s aerospace-grade honeycomb supply, a move aimed at improving supply-chain resilience for OEMs. March 2023 brought automotive-focused innovation when Teijin Automotive Technologies introduced Hexacore for lightweight vehicle structures, signalling early traction for fiber-compatible cores in mass-market mobility. Through 2024 the market saw both capacity and product expansion: May 2024 EconCore licensed continuous thermoplastic honeycomb production targeting EV floors and transit panels; July 2024 Hexcel released high-temperature aluminum honeycomb variants for next-gen engines and military aerospace; and August 2024 Toray and Hyundai strengthened collaboration to integrate advanced core materials into future EV and high-performance vehicle programs.

Financial and capacity signals continued into late 2024-2025: September 2024 Hexcel reported strong aerospace segment growth tied to single-aisle production ramps; December 2024 Toray expanded carbon fiber honeycomb capacity for defense and motorsports segments; and December 2025 Toray Advanced Composites signed a long-term supply agreement to provide advanced core products for mega-constellation satellite solar arrays, underlining diversification into space-grade applications. These events show three concurrent market dynamics: (1) steady aerospace volume underpinning near-term demand, (2) thermoplastic and automated production scaling to address high-volume transport and EV use cases, and (3) product innovation to meet thermal, acoustic and high-temperature requirements across aerospace, defense and new space markets.

Honeycomb Core Materials Market Trends and Opportunities

Qualification of Thermoplastic and Sustainable Cores for High-Rate Aerospace Manufacturing

Aerospace OEMs are rapidly moving beyond phenolic and thermoset honeycomb systems toward thermoplastic composite (TPC) cores, driven by the need to eliminate autoclaves, shorten takt times, and enable recyclability. Thermoplastic honeycomb sandwich structures now align directly with next-generation single-aisle and regional aircraft production strategies.

A major inflection point occurred in December 2025, when Toray Advanced Composites completed NCAMP qualification for its Cetex® TC1225 LMPAEK thermoplastic system. This milestone allows OEMs to bypass individual material allowables testing, accelerating the certification of thermoplastic honeycomb panels for primary and secondary aerostructures.

Manufacturing economics are equally compelling. In 2025, Collins Aerospace demonstrated that transitioning from thermoset to thermoplastic integrated sandwich structures can reduce production cycle times by up to 80%, primarily by removing autoclave cure steps. Weight reductions of 20–50% have been documented in cabin doors, floor panels, and interior bulkheads—directly improving payload efficiency and fuel burn.

End-of-life considerations are now embedded in material selection. In June 2025, Toray, Daher, and Tarmac Aerosave launched a joint recycling program for retired thermoplastic composite aircraft structures. The initiative supports the EU Circular Economy Action Plan by reprocessing high-performance honeycomb cores into secondary automotive and industrial components—an advantage thermosets cannot match.

Metal and Hybrid Honeycomb Cores for Satellite and UAV Thermal Stability

The expansion of mega-constellation satellites and high-speed UAVs is driving renewed demand for metal honeycomb cores, particularly aluminum 5052/5056 and titanium, where thermal conductivity and dimensional stability under vacuum are decisive. Unlike polymeric cores, metal honeycombs maintain stiffness and flatness across extreme orbital temperature gradients.

In July 2025, Toray Advanced Composites signed a long-term supply agreement with Airborne Aerospace for satellite solar array substrates. These platforms rely on aluminum honeycomb to manage rapid hot–cold orbital transitions without inducing panel warpage, directly protecting photovoltaic efficiency.

Defense programs are pushing material limits further. At the 2025 Paris Air Show, multiple hypersonic and high-speed UAV platforms showcased titanium honeycomb cores capable of continuous service above 600 °C—a regime where aramid and conventional aluminum cores lose modulus. This capability is critical for reusable high-Mach vehicles and long-loiter ISR drones operating in severe aerodynamic heating environments.

Corrosion resistance has also advanced. To meet updated MIL-SPEC requirements, aerospace aluminum honeycombs now employ phosphoric acid anodizing (PAA) and chrome-free conversion coatings. These treatments extend service life by ~35% in maritime patrol UAVs operating in high-salinity conditions, materially lowering lifecycle maintenance costs.

Honeycomb Cores as Crash-Critical Structures in Urban Air Mobility (UAM) and eVTOL Platforms

Urban air mobility represents one of the most structurally demanding growth avenues for honeycomb cores. Unlike conventional aircraft, eVTOLs prioritize specific energy absorption (SEA) and crashworthiness to protect occupants during vertical operations and off-nominal landings.

Research published in February 2025 demonstrates that auxetic (negative Poisson’s ratio) honeycomb cores reduce blade and floor deflection to ~55.6% of conventional cores under extreme loading. This stiffness-to-weight advantage is becoming decisive for Category A-certified eVTOLs developed by Joby Aviation and Archer Aviation.

Battery safety further reinforces honeycomb adoption. UAM OEMs increasingly specify aramid (Kevlar) honeycomb in battery enclosures, where its high crush energy absorption acts as a structural “crumple zone,” mitigating cell intrusion and reducing the probability of thermal runaway after hard landings.

Policy and infrastructure signals are aligning with this trend. At the Dubai Airshow 2025, the UAE unveiled a national Skyport infrastructure plan built around eVTOL fleets featuring >30% composite content by weight, creating a direct pipeline for honeycomb core suppliers into high-volume urban air taxi production.

Large-Format Honeycomb Cores for Ultra-Long Offshore Wind Blades

Offshore wind turbine scaling beyond 15 MW is exposing the structural limits of balsa wood and PET foam cores, particularly in shear webs and root sections of blades exceeding 115 m. This is opening a material substitution window for large-cell aluminum and thermoplastic honeycomb cores.

Modeling data released in 2025 by Sinoma Science & Technology shows that honeycomb-filled shear webs reduce maximum blade stress by ~22%, enabling longer blades without compromising fatigue life. This stress reduction directly supports 25-year offshore service requirements under cyclonic loading.

Capacity is following demand. In June 2025, Sinoma announced a $25.2 million investment in a new wind blade manufacturing facility in Uzbekistan, designed for automated assembly of large composite structures targeting Central Asian and European offshore markets.

A further differentiator is digital integration. Through an EU-funded program, Corex Honeycomb and TWI Ltd embedded early-failure crack detection sensors directly into honeycomb cores of a 9.7 m rotor blade. Real-time structural health monitoring from within the core has demonstrated the potential to reduce offshore O&M costs by ~15% by preventing catastrophic blade failure.

Market Share Analysis: Honeycomb Core Materials Market

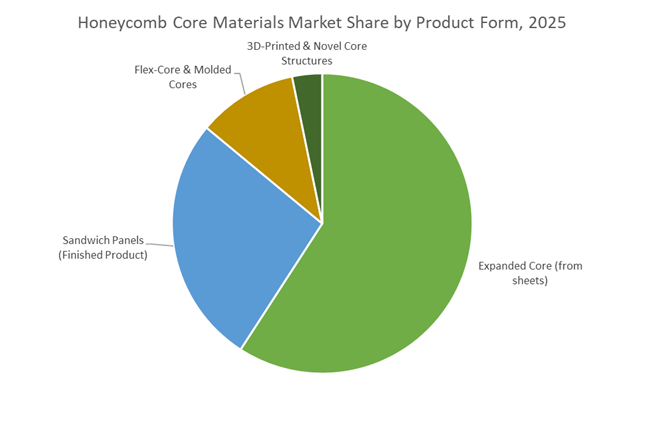

Market Share by Product Form: Expanded Honeycomb Core as the Cost–Performance Backbone of Lightweight Structures

Expanded honeycomb core accounts for approximately 55% of total market share because it delivers the most scalable and economically defensible route to achieving ultra-high stiffness-to-weight ratios across aerospace, defense, and transportation platforms. Its dominance is not driven by material novelty, but by manufacturing physics and logistics efficiency. The 40:1 expansion ratio fundamentally reshapes supply-chain economics—OEMs and Tier-1 suppliers can ship compact HOBE blocks instead of volumetric finished cores, cutting freight costs, warehouse space, and carbon footprint per square meter of installed structure. At the fabrication stage, 2025-grade expanded cores have crossed a critical quality threshold: zero-burr CNC machinability at ±0.010-inch tolerances allows direct integration into high-precision bonded assemblies without secondary edge finishing, reducing labor hours and rework risk in nacelles, radomes, and satellite panels. Further, expanded core technology offers the widest usable density spectrum in the market (≈1–55 lb/ft³), enabling engineers to fine-tune strength, acoustic damping, and impact resistance using a single core architecture rather than switching materials. This design flexibility—combined with continuous service stability up to 350°F for advanced phenolic systems—locks expanded honeycomb into long-cycle programs where qualification costs are high and material changes are economically unattractive. As a result, expanded core maintains structural share leadership not through price competition, but through system-level cost minimization, qualification inertia, and production scalability.

Market Share by End-Use Industry: Aerospace & Defense as the Structural Demand Anchor

Aerospace & Defense represents roughly 50% of total honeycomb core demand, reflecting the sector’s structural dependence on sandwich construction rather than cyclical procurement behavior. Modern commercial aircraft are effectively engineered around honeycomb architectures, with expanded cores embedded in ≈80% of aircraft flooring systems and more than 70% of cabin interior components, making them a non-substitutable material class rather than a discretionary input. The value proposition is fundamentally fuel-driven: every kilogram removed from a narrow-body airframe translates into lifetime fuel savings that far exceed the cost of premium core materials, anchoring long-term demand even during aerospace downturns. In parallel, 2025 design priorities—noise reduction, cabin comfort, and durability—are reinforcing honeycomb adoption through acoustic-optimized cell geometries capable of reducing cabin noise by up to 30%, a metric airlines now monetize in premium branding. Defense demand further stabilizes market share, as UAVs, naval aviation, and surveillance platforms increasingly specify corrosion-resistant, PAA-treated aluminum expanded cores to ensure bond integrity in salt-spray and high-humidity environments. With aircraft backlogs at historic highs and UAV production accelerating, Aerospace & Defense continues to function as the volume anchor and qualification gatekeeper for the Honeycomb Core Materials Market, structurally reinforcing its dominant share through long program lifecycles and stringent certification barriers.

Competitive Landscape: Established Aerospace Leaders Expanding Into Thermoplastic and Space Markets While Licensing New Manufacturing Platforms

The honeycomb core competitive set centers on legacy aerospace suppliers and specialist innovators that combine material breadth (aluminum, aramid/Nomex®, fiberglass, thermoplastic PP), certified processing (NADCAP/AS9100), CNC engineered-core capabilities, and licensing/automation partnerships for high-volume markets. Companies differentiate via acoustic cores, high-temperature aluminum grades, continuous thermoplastic production licenses and turnkey sandwich panel offerings for transit and marine.

Hexcel Corporation - World Leader in Aluminum and Engineered Acoustic Honeycomb For High-Rate Aerospace Programs

Hexcel’s HexWeb® portfolio (700+ core variants) dominates commercial aerospace, supplying aluminum, aramid and fiberglass cores qualified on major Airbus and Boeing programs. Hexcel pioneered acoustic solutions (Acousti-Cap®) that integrate permeable septa for 5-10 dB nacelle noise reduction and operates engineered-core facilities offering CNC machining and pre-formed assemblies for engine/nacelle applications-making it a preferred supplier for high-rate single-aisle production and mission-critical thermal/structural core demands.

Toray Advanced Composites - Integrated Thermoset/Thermoplastic Core Supplier Expanding Into Space and High-Performance Mobility

Toray bundles prepregs and specialized honeycomb cores to streamline supply chains for aerospace and automotive Tier-1s. Toray’s European processing capacity and recent December 2025 long-term supply agreement for satellite solar arrays show strategic diversification into space applications. The company’s expanded carbon fiber honeycomb capacity (Dec 2024) and sustainability collaborations (end-of-life aircraft recycling for thermoplastics) position it to serve both defense/motorsports niche markets and large EV/mobility programs.

Euro-Composites S.A. - Independent Global Supplier Focused On Aircraft Interiors and FST-Qualified Cores

Euro-Composites is a major independent producer of Nomex®, aluminum and fiberglass cores tailored for aircraft interiors-flooring, galley modules and overhead bins-with strict FAR 25.853 FST compliance. The company’s aluminum 5052/5056 alloy cores are specified for corrosion resistance and primary structural locations on regional jets, while its Poly Shape and other novel core formats enable curved and marine applications, delivering breadth for interiors and secondary structures.

Plascore, Inc. - Versatile Metallic and Thermoplastic Core Specialist Serving Transit, Marine and Clean-Room Sectors

Plascore supplies metallic (aluminum, stainless) and non-metallic (Nomex®, polypropylene) honeycomb cores and turnkey sandwich panel systems for mass transit, marine hulls and clean-room construction. Its PP honeycomb cores are particularly suited for moisture-resistant, cost-sensitive marine and transit interiors, and Plascore’s NADCAP certification for non-metallic processing plus in-house panel integration make it a practical partner for OEMs seeking ready-to-install composite assemblies.

The United States honeycomb core materials market continues to anchor global demand in 2025, supported by defense modernization programs and accelerating narrow-body aircraft production. Growth is particularly strong in aramid honeycomb cores used in fighter aircraft, rotorcraft, space launch vehicles, and next-generation UAVs. Hexcel Corporation reported 13.3% year-on-year growth in its Defense & Space segment in Q3 2025, reflecting higher throughput of HexWeb® aramid and aluminum honeycomb cores for U.S. and allied military platforms.

Industrial policy is reinforcing localization. Under updated USMCA origin rules, bonding and finishing of composite sandwich panels are increasingly being localized within North America, enabling tariff-free movement of qualified aerospace structures. In parallel, Plascore Inc. completed the full operationalization of its 73,500-sq-ft Zeeland, Michigan expansion in 2025, effectively doubling aerospace-grade aramid honeycomb capacity. This expansion directly targets rising demand from commercial aviation interiors and Advanced Air Mobility (AAM) platforms transitioning into certification.

China: COMAC Scaling and “New Materials” Sovereignty

China’s honeycomb core materials market is being reshaped by aerospace indigenization and green manufacturing mandates under the final phase of Made in China 2025. By 2025, the government achieved 70% domestic content in core basic materials, including aluminum honeycomb panels and aramid paper, reducing reliance on imported aerospace cores for the COMAC C919 and upcoming C929 programs.

Beyond aviation, policy spillover into transportation is accelerating adoption. In January 2025, the National Development and Reform Commission (NDRC) enhanced incentives for public transport renewal, driving the use of honeycomb sandwich panels in new-energy buses and high-speed rail interiors. Industrial clusters in Guangdong and Jiangsu have emerged as supply hubs for fire-retardant and FKM-coated honeycomb cores, serving both building façades and mass-transit applications—cementing China’s position as a volume-driven but increasingly sophisticated core producer.

Germany: Circular Honeycomb Engineering under the Clean Industrial Deal

Germany leads Europe in low-carbon and recyclable honeycomb core development, aligning advanced composites with the Clean Industrial Deal and EU circular-economy mandates. At K 2025, German majors including Evonik and Schütz Composites showcased thermoplastic honeycomb cores engineered for rapid thermoforming. These recyclable structures are gaining traction in EV battery enclosures, where impact resistance, thermal insulation, and end-of-life recyclability are simultaneously required.

Aviation decarbonization remains a parallel driver. German research institutes, working with Airbus, are piloting bio-based resin systems for honeycomb cores in 2025 to meet stringent life-cycle carbon accounting for aircraft interiors. Meanwhile, robotized bonding and assembly lines introduced this year are improving dimensional accuracy for large-format aluminum honeycomb panels used in architectural façades and marine superstructures—areas where Germany maintains a precision-engineering advantage.

Luxembourg: Space-Grade Honeycombs and Complex Aerostructures

Luxembourg occupies a strategic niche in high-end aerospace and space-qualified honeycomb cores, anchored by Euro-Composites. In December 2025, the company strengthened long-term supply agreements with major European aerospace OEMs, focusing on perforated aramid honeycombs that allow controlled venting in vacuum environments—an essential requirement for satellites and launch systems.

Portfolio expansion is equally important. During 2025, Euro-Composites broadened its offerings to include 3D-formable Nomex® and Kevlar® honeycombs, enabling complex curved aerostructures without inducing mechanical stress. This capability is increasingly critical for lightweight space panels and next-generation aircraft fuselage sections, positioning Luxembourg as a technology-intensive rather than volume-driven core supplier.

India: Aatmanirbhar Push and Infrastructure-Led Demand

India’s honeycomb core materials market is transitioning rapidly from import dependence to localized commercial production, supported by defense programs, rail modernization, and component incentives. In 2025, domestic players such as Kineco Limited and HONYLITE expanded output of aluminum and paper honeycomb cores, supplying defense vehicles, UAV structures, and architectural panels.

Policy tailwinds are strong. The 2025 Union Budget emphasized light engineering and component manufacturing, extending tax incentives to structural core materials used in automotive and construction sectors. Utilization is most visible in rail: India’s Vande Bharat train program significantly increased consumption of honeycomb-core flooring and partitions in 2025, leveraging weight reduction to support higher operating speeds and improved energy efficiency.

Japan: Advanced Air Mobility, 6G Hardware, and Bio-Attributed Cores

Japan is leveraging its leadership in high-performance fibers and electronics integration to advance the honeycomb core market into next-generation mobility and telecommunications. In 2025, METI fast-tracked certification pathways for eVTOL platforms, driving demand for ultralight aramid and carbon-fiber-reinforced honeycomb cores that maximize battery endurance and structural stiffness.

Electronics applications are emerging in parallel. Japanese firms are piloting honeycomb-structured EMI shielding for 6G signal reflectors, combining mechanical rigidity with controlled electromagnetic transparency for smart-city infrastructure. Sustainability innovation rounds out the picture: research published in December 2025 highlighted PLA-based 3D-printed honeycomb cores for non-structural interiors, offering a markedly lower carbon footprint and reinforcing Japan’s role in bio-attributed composite engineering.

2025 Strategic Matrix: Honeycomb Core Materials by Country

Honeycomb Core Materials Matrix

|

Country

|

Primary Development Focus

|

2025 Strategic Milestone

|

Core Material Leadership

|

|

United States

|

Defense & AAM

|

Hexcel Q3 2025 +13.3% Defense & Space

|

Aramid & HexWeb® cores

|

|

China

|

Aerospace indigenization

|

MIC 2025 70% self-sufficiency

|

Aluminum & paper honeycomb

|

|

Germany

|

Circular composites

|

K 2025 thermoplastic cores

|

Recyclable thermoplastic honeycomb

|

|

Luxembourg

|

Space systems

|

Euro-Composites perforated cores

|

3D-formable aramid

|

|

India

|

Rail & defense

|

Budget 2025 component incentives

|

Aluminum structural panels

|

|

Japan

|

eVTOL & 6G

|

METI fast-track certification

|

Carbon-fiber honeycomb

|

Honeycomb Core Materials Market Report Scope

Honeycomb Core Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.5 Billion

|

|

Market Size (2035)

|

$25.3 Billion

|

|

Market Growth Rate

|

10.3%

|

|

Segments

|

By Core Material Type (Aluminum Honeycomb, Aramid Honeycomb, Thermoplastic Honeycomb, Paper Honeycomb, Stainless Steel & Specialty Alloys), By Product Form (Expanded Core, Sandwich Panels, Flex-Core, 3D-Printed Core Structures), By Manufacturing Technology (Expansion, Corrugation, Extrusion, Additive Manufacturing), By Application (Structural Components, Interior Fit-outs, Thermal & Acoustic Insulation, Energy Absorption, Precision Platforms), By End-User Industry (Aerospace & Defense, Automotive & Transportation, Construction & Infrastructure, Packaging & Logistics, Sports & Consumer Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hexcel Corporation, Euro-Composites S.A., Plascore Inc., Argosy International Inc., The Gill Corporation, EconCore N.V., Toray Industries Inc., Schütz GmbH & Co. KGaA, Corex Honeycomb, HONYLITE, Packaging Corporation of America, Tubus Baer GmbH, RelCore Composites Inc., Avic Composite Establishment, Axxor

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Honeycomb Core Materials Market Segmentation

By Core Material Type

- Aluminum Honeycomb

- Aramid Honeycomb

- Thermoplastic Honeycomb

- Paper Honeycomb

- Stainless Steel & Specialty Alloys

By Product Form

- Expanded Core

- Sandwich Panels

- Flex-Core

- 3D-Printed Core Structures

By Manufacturing Technology

- Expansion Process

- Corrugation Process

- Extrusion

- Additive Manufacturing / 3D Printing

By Application

- Structural Components

- Interior Fit-outs

- Thermal & Acoustic Insulation

- Energy Absorption

- Precision Platforms

By End-User Industry

- Aerospace & Defense

- Automotive and Transportation

- Construction & Infrastructure

- Packaging & Logistics

- Sports & Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Honeycomb Core Materials Market

- Hexcel Corporation

- Euro-Composites S.A.

- Plascore, Inc.

- Argosy International Inc.

- The Gill Corporation

- EconCore N.V.

- Toray Industries, Inc.

- Schütz GmbH & Co. KGaA

- Corex Honeycomb

- HONYLITE

- Packaging Corporation of America (PCA)

- Tubus Baer GmbH

- RelCore Composites Inc.

- Avic Composite Establishment

- Axxor

*- List not Exhaustive