Market Overview: High-Specific-Strength, FST-Compliant Aramid Honeycomb Is Becoming A Structural Enabler For Next-Generation Aerospace Platforms

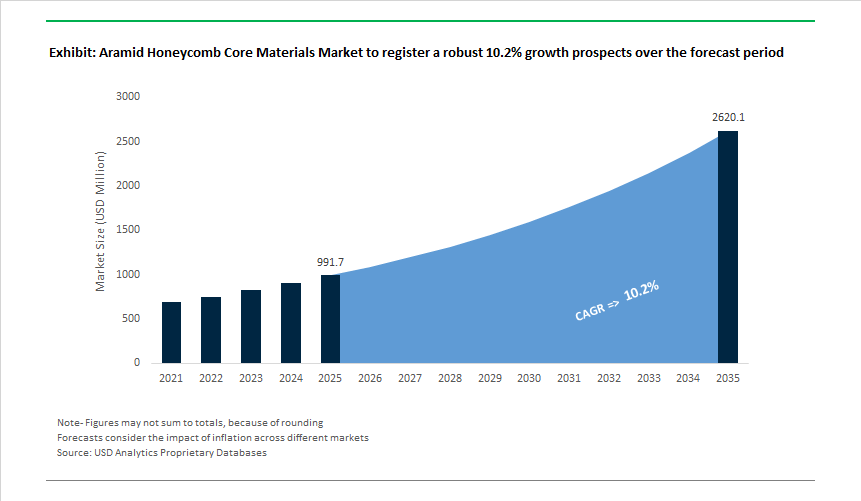

The Aramid Honeycomb Core Materials Market (USD 991.7 million in 2025; projected to reach USD 2,619.4 million by 2035 at a 10.2% CAGR) is expanding as aerospace OEMs and tier-one suppliers structurally redesign aircraft and advanced air mobility platforms around lightweight, fire-safe, sandwich composite architectures. Aramid honeycomb has become a critical enabler in this shift, offering exceptional specific strength and stiffness at ultra-low densities while meeting stringent FAR 25.853 flame, smoke, and toxicity (FST) requirements that govern both civil and military aircraft interiors. In weight-sensitive programs, these attributes translate directly into lower fuel burn, higher payload margins, and simplified certification pathways compared with metallic or foam core alternatives.

From a system-level perspective, aramid honeycomb enables load-bearing panels at densities that are materially unattainable with aluminum honeycomb, while avoiding the corrosion, galvanic interaction, and fatigue concerns associated with metallic cores. Commercially available aramid honeycomb products routinely deliver compressive strengths at or above 270 psi across a wide density spectrum, allowing designers to tune stiffness and impact resistance without over-engineering skins. Leading manufacturers position aramid honeycomb as a mature, certifiable solution for cabin floors, sidewalls, galleys, monuments, nacelles, control surfaces, and radomes, where predictable performance under fire exposure and long-term cyclic loading is non-negotiable.

Over the forecast period, demand will be shaped as much by program risk management and supply-chain resilience as by material performance. Aircraft OEMs, defense primes, and emerging eVTOL developers are increasingly locking in multi-year sourcing strategies for aramid paper and honeycomb core materials to de-risk production ramps and certification timelines. The ability of suppliers to offer consistent cell geometry, tight dimensional tolerances, and complex-curvature forming - while maintaining FST compliance across customized density grades - is becoming a key differentiator.

Market Analysis: Aerospace Supply Chain Expansions and Material Innovations Reshaping Aramid Honeycomb Demand

The past two years brought significant acceleration in aerospace-grade aramid honeycomb manufacturing, product innovation, and supply chain reinforcement. The momentum began in December 2024, when Boeing Commercial Airplanes recognized a key aramid honeycomb supplier for achieving 100% quality and delivery performance over 24 months, reaffirming the material’s critical role in sustaining commercial aircraft production rates. In January 2025, Euro-Composites secured a major government defense contract focused on high-density aramid honeycomb for radomes and military shelters, leveraging the material’s excellent dielectric transparency and structural stability. Manufacturers intensified efforts toward productivity enhancements, reflected in March 2025 when Schütz launched pre-cut, numbered aramid honeycomb kits designed to reduce waste and accelerate assembly in aircraft interior monument manufacturing lines.

Upstream raw material security came into focus in May 2025, with DuPont announcing expanded capacity for Nomex® aramid paper to stabilize supply for honeycomb producers addressing rising global aerospace demand. Structural segment growth continued in July 2025, when Hexcel entered a multi-year supply partnership with a leading UAV/eVTOL manufacturer, embedding HexWeb® honeycomb cores into fuselage and wing architectures for Urban Air Mobility applications. The consolidation wave strengthened in September 2025, as Advanced Honeycomb Technologies (AHT) rebranded under the Axiom Honeycomb umbrella following an acquisition, signaling a commitment to scale aerospace-grade manufacturing at its new California facility. In October 2025, Plascore announced major investments in automated slicing and machining systems to meet expanding Airbus A320 family requirements, indicating rising high-volume needs for precision-machined aramid cores. Innovation continued with Toray’s November 2025 launch of a new Nomex® honeycomb grade offering enhanced acoustic damping properties, addressing next-generation wide-body cabin noise reduction objectives.

Aramid Honeycomb Core Materials Market Trends and Opportunities

High-Flow Aramid Honeycomb Grades Enabling Out-of-Autoclave Aerospace Production

Aerospace OEMs are under mounting pressure to eliminate the capital and operating costs associated with autoclave curing, which can account for a disproportionate share of composite program CAPEX and energy consumption. This has accelerated the adoption of Vacuum Bag Only (VBO) and resin infusion processes—creating a strong pull for aramid honeycomb cores engineered with high-flow cell geometries that enable uniform resin distribution without weight penalties.

A critical validation milestone was reached in December 2025 when Toray Advanced Composites completed NCAMP qualification for its Cetex® TC1225 LMPAEK thermoplastic system. This dataset, now accessible across the aerospace supply chain, formally validates OoA/VBO processing for primary structures and materially lowers certification friction for aramid-cored sandwich panels.

From a manufacturing perspective, late-2024 introductions of dip-coated meta-aramid grades have demonstrated up to 15% lower resin uptake versus traditional phenolic-dipped cores. For programs such as the Airbus A321XLR—where every kilogram directly impacts range—this translates into tangible aircraft-level economics. Industry disclosures at the 2025 Paris Air Show further indicate that switching to OoA-compatible aramid honeycomb can cut cycle times by 25–40%, allowing Tier-1 suppliers to scale production without parallel investment in high-pressure autoclave infrastructure.

Low-Smoke, Fire-Retardant Aramid Cores for Rail, Marine, and Aviation Safety

As fire-safety regulation tightens globally, aramid honeycomb’s inherent flame resistance—derived from its meta-aramid paper base—is becoming a decisive advantage over aluminum and polymer foam cores. The full enforcement of EN 45545-2 in 2025 has pushed European rail OEMs to standardize aramid honeycomb in floors, partitions, and bulkheads, where its dual role as a structural core and thermal barrier helps preserve evacuation windows during fire events.

In commercial aviation, aramid honeycomb has effectively become the default core material for interiors. By 2025, over 60% of new aircraft cabin components—including flooring, seating, and monuments—utilize meta-aramid cores to meet FAA and EASA flammability requirements, while delivering ~20% weight reduction compared with legacy aluminum or balsa constructions.

Fire containment has emerged as a particularly strategic use case. In 2024–2025, European Union Aviation Safety Agency and the Federal Aviation Administration intensified research under LOKI-PED programs focused on lithium battery thermal runaway. Aramid honeycomb panels are now being integrated into onboard containment systems and flight-deck stowage, having demonstrated resistance to localized temperatures exceeding 400 °C without generating toxic smoke—an increasingly non-negotiable requirement as battery-powered aviation scales.

Aramid Honeycomb as a Structural Core for Urban Air Mobility and eVTOL Aircraft

Urban Air Mobility (UAM) and eVTOL platforms represent the fastest-accelerating opportunity for aramid honeycomb materials. Unlike conventional fixed-wing aircraft, eVTOL designs must balance extreme weight sensitivity with crashworthiness and energy absorption for low-altitude vertical operations.

By 2025, more than 80% of leading UAM developers, including Joby Aviation and Archer, have incorporated Nomex® or Kevlar® honeycomb into airframe, sub-floor, and rotor blade structures. The specific energy absorption (SEA) characteristics of aramid honeycomb make it particularly effective in protecting occupants during hard landings, positioning it as the reference core material for Category A certification pathways.

From an operational standpoint, lightweight aramid-cored bulkheads and floors are enabling eVTOL manufacturers to partially offset the mass of high-density battery packs—still the primary constraint on urban range and payload economics. Defense and space applications further reinforce this opportunity: approximately 55% of tactical drones and small-satellite platforms now utilize para-aramid honeycomb for its stiffness retention and damage tolerance under high-vibration launch and recovery cycles.

Long-Span Wind Turbine Blades and Hybrid Core Architectures

Beyond aerospace, aramid honeycomb is gaining strategic relevance in next-generation offshore wind turbines, where blade lengths exceeding 115 meters impose severe fatigue and shear-loading demands on core materials. Traditional balsa wood and PET foam cores face well-documented challenges—moisture ingress, fatigue degradation, and thickness limitations—particularly in offshore environments.

By 2025, meta-aramid honeycomb is increasingly specified in root sections and shear webs of ultra-long blades, where its corrosion-proof nature and high shear modulus support operational lifetimes beyond 25 years. This shift is not occurring in isolation: blade manufacturers are adopting hybrid architectures that combine aramid honeycomb cores with carbon fiber spar caps, enabling thinner aerofoils that can capture 10–15% more energy in low-wind regimes—directly improving project ROI.

Supply chain dynamics underscore this opportunity. In late 2024, DuPont announced a significant expansion of its global Nomex® paper capacity to address tightening availability as aerospace and offshore wind demand converge. This investment reflects a broader industry consensus that aramid honeycomb is transitioning from a niche interior material to a load-critical core technology across mobility, energy, and defense applications.

Market Share Analysis: Aramid Honeycomb Core Materials Market

Market Share by Material Type: Nomex® Honeycomb Establishes the Aerospace Cost–Safety Benchmark

Nomex® honeycomb accounts for approximately 80% of the global aramid honeycomb core materials market, reflecting its entrenched position as the default structural core for certified lightweight sandwich panels. This dominance is not driven by peak mechanical performance alone, but by Nomex’s ability to sit at the optimal intersection of weight reduction, fire safety compliance, processing compatibility, and lifecycle economics. In aerospace-grade structures, replacing aluminum or solid laminate cores with Nomex® honeycomb delivers up to 20% component-level weight reduction, a saving that compounds across fuselage interiors, floor panels, and control surfaces to materially lower fuel burn and emissions. Critically, Nomex® meets FAR 25.853 smoke, flame, and toxicity regulations without secondary fire-retardant additives, eliminating costly design iterations and certification risk—an advantage para-aramid alternatives struggle to match at scale. From a manufacturing standpoint, its ability to withstand continuous cure temperatures around 180°C allows seamless integration with carbon-fiber prepregs used in next-generation composite skins, avoiding thermal mismatch failures. Long service life further reinforces market share: aerospace-certified Nomex® cores demonstrate durability beyond 20,000 flight hours even in humid or corrosive environments, where aluminum cores face galvanic corrosion when paired with carbon fiber. When procurement teams assess total cost of ownership—including certification, maintenance, and replacement cycles—Nomex® consistently outperforms both metallic and exotic aramid substitutes, cementing its role as the economic and regulatory anchor of the aramid honeycomb market.

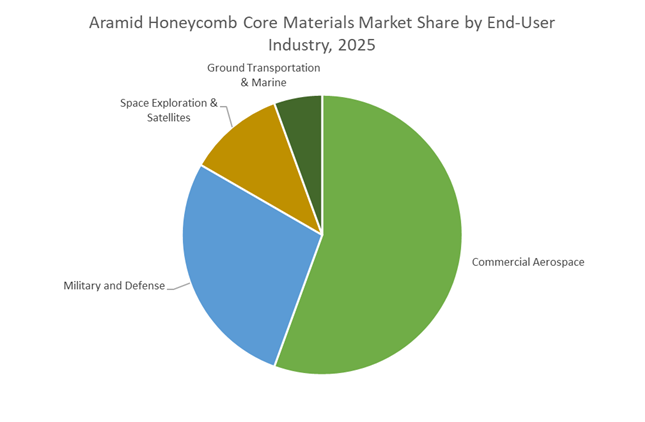

Market Share by End-Use Industry: Commercial Aerospace Drives Structural Volume and Design Lock-In

Commercial aerospace represents roughly 50% of total demand for aramid honeycomb core materials, making it the single most influential end-use segment shaping product specifications and production scale. This leadership is structurally linked to the fact that modern aircraft platforms are now approximately 50% composite by weight, creating sustained, program-long demand for lightweight cores that can be certified once and deployed across thousands of aircraft. Nomex® honeycomb has achieved deep design lock-in, with over 70% of cabin interior components—including sidewalls, ceilings, galleys, monuments, and flooring—built around aramid honeycomb sandwich constructions. Market share is further reinforced by the rapid shift toward advanced sandwich architectures, as OEMs pursue aggressive payload-to-fuel optimization; every kilogram removed from the cabin translates directly into higher revenue payload or extended range. Passenger comfort has become an additional demand lever, with acoustically tuned honeycomb cores now delivering up to 35% cabin noise reduction, supporting airlines’ premium-cabin differentiation strategies. On the production side, aerospace backlogs have pushed Tier-1 suppliers to adopt formable “Flex-Core” geometries, enabling complex curved structures without cell buckling and reducing fabrication waste—an efficiency gain that directly supports higher build rates at Boeing and Airbus. As long as commercial aircraft remain composite-intensive and certification-driven, aerospace will continue to anchor volume demand and technological direction for the aramid honeycomb core materials market.

Competitive Landscape: Global Leaders Advancing Aerospace-Grade Aramid Honeycomb Technologies

The competitive ecosystem is shaped by aerospace-certified manufacturers specializing in high-temperature honeycomb cores, over-expanded architectures, precision-machined parts, and integrated prepreg-core solutions. Companies focus heavily on AS9100-certified production, phenolic resin coating uniformity, dielectric-compatible grades for defense, and formable honeycomb variants to address complex curvature requirements in nacelles, flight-control surfaces, radomes, and aircraft interiors. Their strategies revolve around multi-site manufacturing footprints, R&D on acoustic-damping cores, and secure access to Nomex® aramid paper during periods of heightened aerospace demand.

Hexcel Corporation: Industry Leader in High-Temperature, Acoustic-Optimized Aramid Honeycomb

Hexcel offers the renowned HexWeb® CR and HRH series, engineered for outstanding thermal stability up to 180°C-particularly suited for nacelle structures and engine environments. The company is well known for HexWeb® Acousti-Cap®, a patented septum-reinforced honeycomb technology that delivers superior acoustic attenuation in engine inlets and exhaust systems. Hexcel’s integration of aramid honeycomb with HexPly™ prepregs and HexFlow® resins provides OEMs with a single-source composite solution. Its extensive AS9100-certified global manufacturing footprint supports all major aircraft programs, ensuring consistent supply reliability.

Toray Advanced Composites: Integrated Core-Prepreg Solutions With Curvature Flexibility

Toray maintains substantial aramid core processing capabilities in Europe, co-located strategically with prepreg manufacturing to offer Toray Nomex® honeycomb kits tailored for aerospace and high-performance automotive customers. Its Nomex® Flexible Core systems enable forming parabolic or compound curves without mechanical property loss, making them ideal for radomes and flight-control surfaces. Toray’s aramid honeycomb grades operate at temperatures up to 180°C, ensuring suitability for high-speed aircraft. The company also caters to cost-sensitive sectors by offering commercial-grade honeycomb for marine and transportation applications.

Euro-Composites S.A.: High-Volume, Defense-Ready Aramid Honeycomb Manufacturing

Euro-Composites operates some of the world’s largest automated aramid honeycomb production lines across Europe and the U.S., supplying Airbus, Boeing, and global Tier-1 integrators. Its advanced phenolic resin coating processes yield uniform cell compression strength with <5% variability, supporting stringent aerospace repeatability requirements. The company provides specialized honeycomb for military shelters and radomes, capitalizing on the material’s dielectric transparency. With broad AS9100 and Nadcap certifications, Euro-Composites serves both primary and secondary aerospace structures with high reliability.

Plascore, Inc.: Precision-Machined Aramid Honeycomb For Aerospace and Rail

Plascore expanded significantly after its 2023 acquisition of Argosy’s honeycomb division, strengthening its product range and military-grade supply capability. The company offers Nomex® and Kevlar® honeycomb, supporting applications requiring tailored flame resistance and impact tolerance. Its machining expertise delivers contoured and cut-to-spec core components with slicing tolerances as tight as ±0.006 inches, reducing OEM fabrication times. Plascore is also a prominent supplier to high-speed rail interiors, focusing on fire protection and corrosion-resistant lightweight panels.

The Gill Corporation: Specialist in Aircraft Interiors and Over-Expanded Honeycomb

The Gill Corporation is well established in the aircraft interior segment, supplying aramid honeycomb bonded panel systems that meet stringent FST and aesthetic requirements for cabin modules. Its Over-Expanded (OX) honeycomb variants provide exceptional drapeability for complex cabin ceiling geometries and interior curved panels. The firm integrates aramid honeycomb with its proprietary Gillfab™ pre-laminated face sheets, enabling plug-and-play composite panel solutions. It also offers high-density grades (≥8 PCF) for localized structural loads in aircraft flooring and interior support points.

The United States continues to function as the global anchor market for para-aramid honeycomb core materials, driven by defense reshoring priorities, aerospace certification depth, and digitally enabled composite manufacturing. In 2025, federal policy alignment with advanced materials has indirectly strengthened the aramid honeycomb ecosystem, particularly for FST-compliant sandwich panels used in military aviation, satellites, and next-generation commercial aircraft cabins. The January 2025 allocation of USD 285 million under the CHIPS and Science Act by the U.S. Department of Commerce—while semiconductor-focused—extends into digital twin–based optimization of composite substrates, accelerating defect reduction and yield stability for honeycomb cores used in UAVs and space systems. This convergence of digital manufacturing and structural materials is reshaping U.S. supplier competitiveness.

On the industrial front, Hexcel Corporation expanded its Americas Aerospace Distribution Network in October 2025, materially reducing lead times for HexWeb® aramid honeycomb supplied to Tier 1 and Tier 2 aerospace suppliers supporting Boeing production ramps. Parallel to commercial aviation, the U.S. Department of Defense intensified funding for high-temperature aramid-reinforced cores designed to withstand acoustic fatigue and thermal cycling in hypersonic flight profiles, reinforcing the country’s strategic edge in defense-grade honeycomb technologies.

China: C919 Localization, MIIT Standards & Export-Driven Rail Applications

China’s aramid honeycomb core materials market is undergoing a structural shift from import dependence toward full domestic aerospace-grade capability, tightly coupled with the industrialization of the C919 program. In 2025, COMAC enforced a localized-first procurement framework, triggering accelerated capacity expansion among domestic meta-aramid paper producers. Suppliers such as Yantai Metastar Special Paper and Shenghe Tech scaled flame-resistant aramid paper output tailored for narrow-body cabin interiors, signaling China’s intent to control the full honeycomb value chain—from paper to finished core blocks.

Regulatory momentum further strengthened this trajectory when the Ministry of Industry and Information Technology (MIIT) finalized national standards for high-end structural composites in September 2025. These standards incentivize manufacturers achieving tight cell-size tolerances (down to 200 mm large-format precision), directly improving China’s competitiveness in wide-format honeycomb panels. Beyond aerospace, CRRC integrated aramid honeycomb flooring into export-oriented high-speed trains to meet EN 45545-2 fire safety requirements, enabling Chinese suppliers to penetrate European-regulated transport markets.

Germany: Thermoplastic Honeycomb, Circular Composites & Green Aviation Leadership

Germany leads Europe’s aramid honeycomb core materials market through its integration of thermoplastic welding technologies, sustainability mandates, and high-rate aerospace manufacturing. A defining milestone in early 2025 was the success of the Multi-Functional Fuselage Demonstrator (MFFD) program, involving Airbus and Fraunhofer institutes. The project demonstrated induction-welded thermoplastic aramid honeycomb panels capable of eliminating thousands of mechanical fasteners, reducing fuselage weight by approximately 10%—a decisive advantage for next-generation narrow-body aircraft.

Industrial momentum remains strong, with Germany reporting composite-sector growth of 9.2% in 2025. Euro-Composites, operating across the German–Luxembourg corridor, introduced perforated aramid honeycomb cores for vented space-grade panels without mechanical property loss. Under the EU Green Deal, German OEMs are now required to track lifecycle carbon footprints, structurally favoring aramid honeycomb over aluminum cores in aircraft such as the A320neo family.

Japan: Para-Aramid Dominance Powering Future Mobility & Hydrogen Systems

Japan’s strategic strength in para-aramid fiber production positions it as a leader in honeycomb applications beyond aerospace, particularly in future mobility and hydrogen infrastructure. In October 2025, Toray Group entered a strategic partnership with Hyundai Motor Group to develop lightweight, crash-resistant aramid honeycomb sandwich structures for special purpose mobility and advanced EV platforms. This signals a decisive shift toward structural honeycomb use in automotive architectures.

Manufacturing innovation further differentiates Japan, with breakthroughs in robotic Automated Fiber Placement (AFP) enabling precise lamination of complex-curved honeycomb panels and reducing material waste by 22% versus manual processes. Simultaneously, Teijin Limited is prioritizing aramid-reinforced composites for high-pressure hydrogen storage tanks, embedding honeycomb technologies into Japan’s long-term green energy roadmap.

France: Aerospace Lifecycle Management & Platform Benchmarking

France remains the global benchmarking arena for aramid honeycomb materials, reinforced by its role in aerospace lifecycle innovation and platform-level decision-making. At the June 2025 Paris Air Show, Toray Group, Daher, and Tarmac Aerosave launched a joint End-of-Life recycling program focused on recovering high-value thermoplastic aramid composites from retired aircraft—addressing circularity without compromising material performance.

France also advances novel aerospace platforms. In mid-2025, Flying Whales selected Hexcel as the primary composite supplier for its LCA60T heavy-lift airship, underscoring aramid honeycomb’s dominance in low-carbon logistics. Concurrently, the French Ministry of the Armed Forces expanded procurement of aramid-core shelters for mobile defense units, citing superior energy absorption and acoustic insulation in operational environments.

India: MRO Localization, Space Programs & Aerospace Clusters

India is emerging as a strategically important node in the aramid honeycomb core materials market, driven by MRO localization, defense indigenization, and space-sector demand. Under the Semicon India and Aatmanirbhar Bharat initiatives, Tata Electronics and global partners have begun integrating aramid composite manufacturing into the Gujarat aerospace cluster, expanding domestic capabilities beyond assembly into structural materials.

In 2025, the Indian government committed ₹4,500 crore (USD 540 million) to modernize aerospace infrastructure, including clean-room bonding lines for repairing Nomex honeycomb floor panels used by Air India and IndiGo fleets. On the space front, Indian Space Research Organisation increased domestic sourcing of para-aramid honeycomb for satellite solar array substrates, targeting a 14% reduction in launch mass for upcoming constellation missions—positioning India as a credible secondary manufacturing hub.

2025 Strategic Summary: Aramid Honeycomb Core Materials by Country

Aramid Honeycomb Core Materials Matrix

|

Country

|

Primary Technical Focus

|

Key 2025 Development

|

Structural Market Advantage

|

|

United States

|

Military hypersonics & digital manufacturing

|

USD 285M Digital Twin institute; HexWeb® distribution expansion

|

Defense-grade certification depth

|

|

China

|

Narrow-body aerospace & rail exports

|

MIIT composite standards; C919 localization

|

Self-sufficient aramid paper supply

|

|

Germany

|

Thermoplastic welding & circular composites

|

MFFD fuselage success; EU Green Deal alignment

|

Lightweighting leadership in Europe

|

|

Japan

|

Future mobility & hydrogen systems

|

Toray–Hyundai pact; AFP automation

|

Para-aramid fiber dominance

|

|

France

|

Aircraft lifecycle & novel platforms

|

Recycling consortium; LCA60T airship

|

Global aerospace benchmarking hub

|

|

India

|

MRO & space substrates

|

₹4,500 Cr aerospace modernization

|

Cost-efficient secondary manufacturing base

|

Aramid Honeycomb Core Materials Market Report Scope

Aramid Honeycomb Core Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$991.7 Million

|

|

Market Size (2035)

|

$2619.4 Million

|

|

Market Growth Rate

|

10.2%

|

|

Segments

|

By Material Type (Nomex® Honeycomb, Kevlar® Honeycomb, Other Aramid Hybrids), By Application (Aerostructures, Cabin Interiors, Transportation, Defense & Space, Industrial & Other), By End-User Industry (Commercial Aerospace, Military & Defense, Space Exploration, Ground Transportation, Marine & Sporting Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hexcel Corporation, DuPont de Nemours Inc., Toray Industries Inc., Euro-Composites S.A., The Gill Corporation, Plascore Inc., Gurit Holding AG, Teijin Limited, Schütz GmbH & Co. KGaA, Argosy International Inc., EconCore N.V., Shenghe New Material Technology, TRB Lightweight Structures Ltd., Yantai Tayho Advanced Materials Co., Ltd., Showapylat

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aramid Honeycomb Core Materials Market Segmentation

By Material Type

- Nomex® Honeycomb

- Kevlar® Honeycomb

- Other Aramid Hybrids

By Application

- Aerostructures

- Cabin Interiors

- Transportation

- Defense and Space

- Industrial and Other Applications

By End-User Industry

- Commercial Aerospace

- Military and Defense

- Space Exploration

- Ground Transportation

- Marine and Sporting Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aramid Honeycomb Core Materials Market

- Hexcel Corporation

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Euro-Composites S.A.

- The Gill Corporation

- Plascore, Inc.

- Gurit Holding AG

- Teijin Limited

- Schütz GmbH & Co. KGaA

- Argosy International Inc.

- EconCore N.V.

- Shenghe New Material Technology

- TRB Lightweight Structures Ltd.

- Yantai Tayho Advanced Materials Co., Ltd.

- Showapylat (Showalight)

*- List not Exhaustive