Market Overview: Intrinsic Flame Resistance and Electrical Reliability Are Locking Meta-Aramid Fibers Into Safety-Critical Systems

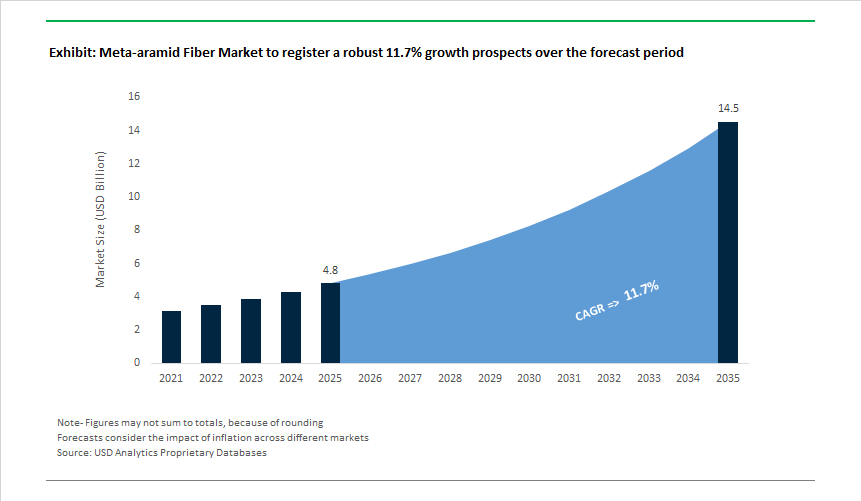

The Meta-aramid Fiber Market is valued at USD 4.8 billion in 2025 and is projected to reach USD 14.5 billion by 2035, expanding at an 11.7% CAGR as industries increasingly design around materials that cannot fail under heat, flame, or electrical stress. Unlike performance fibers that rely on coatings or additives, meta-aramids are specified for their intrinsic, non-melting fire resistance and long-term thermal stability, making them structurally embedded in applications where regulatory compliance, worker safety, and system reliability outweigh raw tensile strength.

A major share of demand is anchored in electrical infrastructure and power equipment, where meta-aramid papers and nonwovens function as insulation systems rather than commodity fibers. In transformers, generators, and high-voltage components, aramid paper is selected because it maintains dielectric integrity under sustained thermal and electrical loading. Densified meta-aramid papers deliver dielectric strengths in the range of ~18-40 kV/mm, enabling compact insulation designs while supporting higher operating temperatures and longer asset lifetimes. As grids modernize, renewable integration rises, and power density increases, insulation materials that tolerate prolonged exposure around ~220°C over multi-decade service lives become essential design enablers.

Fire protection and thermal barrier applications represent a second structural demand pillar. Meta-aramid fibers exhibit Limiting Oxygen Index (LOI) values ≥30%, meaning they are inherently self-extinguishing in atmospheric conditions without halogenated flame retardants. This characteristic underpins their use in firefighter turnout gear, industrial protective clothing, and high-temperature filtration media, where compliance with flame, smoke, and toxicity standards is non-negotiable. Unlike treated fabrics, meta-aramids retain performance after repeated heat exposure, laundering, and mechanical stress, supporting predictable lifecycle economics for institutional buyers.

In aerospace and mass-transport interiors, meta-aramid materials are valued less for headline strength and more for certification survivability and weight efficiency. Meta-aramid honeycomb papers are widely specified as core materials in interior panels, floor systems, and partitions because they combine exceptional strength-to-weight performance with compliance to stringent fire, smoke, and toxicity requirements. This allows OEMs to reduce structural mass while meeting regulatory fire scenarios that rule out many polymeric alternatives. As aircraft production rates rise and rail and urban mobility platforms adopt aerospace-derived safety standards, meta-aramid cores remain difficult to substitute.

Market Analysis: Capacity Growth, Product Innovation and Policy Shifts

The market dynamics reveal a dual trend: technology-led product improvements (lighter, dyeable, solvent-efficient processes) alongside capacity and regulatory moves that accelerate demand in APAC and defense/aerospace segments. February 2025 saw Toray Industries introduce a next-generation meta-aramid filament yarn engineered for high-temperature sewing threads and hot-gas filtration, designed to preserve >90% knot strength after 500 hours at 200°C - a clear signal of use-case specialization (industrial filtration and sewn assemblies). In April 2025, DuPont formed a strategic partnership with a North American PPE manufacturer to co-develop dyeable meta-aramid fabrics, addressing a long-standing market gap for colored flame-resistant workwear without sacrificing FR performance. Product launches and sustainability moves continued through November-December 2025 with Teijin Aramid (Nov 2025) introducing an eco-friendlier solvent system to cut hazardous chemical usage (~20%), and DuPont launching Nomex® Xtreme FR (Dec 2025) - a 3D-woven, static-dissipative apparel line that raises Thermal Protective Performance (TPP) for industrial users.

Capacity and procurement changes are reshaping supply balances. October 2025 brought Yantai Tayho’s final capacity expansion phase, strengthening Asia-Pacific supply for electrical insulation and filtration media and lowering lead times for regional converters. Regulatory and procurement updates such as the U.S. DLA’s November 2024 requirement to increase minimum meta-aramid content in military combat uniforms reinforce institutional demand for higher-performance blends. On the other hand, Kermel (Sept 2025) pivoted R&D toward lighter, moisture-managing meta-aramid blends for wildland firefighting, reflecting a sectoral push for weight reduction plus retained tensile strength (>85% post-flame). Historic production upticks like HUVIS’ July 2024 output growth also underscore steady market absorption in Europe and Asia. Taken together, these product, capacity and policy developments point to accelerated commercialization of specialty grades (dyeable, solution-dyed, filament yarns) and more resilient regional sourcing strategies.

Meta-aramid Fiber Market Trends and Opportunities

Trend 1: Capacity Expansion for High-Purity Yarns in EV Battery Safety

Global producers are accelerating capacity additions for high-purity meta-aramid yarns tailored specifically for lithium-ion battery safety architectures. By late 2025, industry disclosures indicate global installed capacity approaching ~69,000 tons per year, with China accounting for ~55% of this total. Crucially, much of the incremental capacity is not commodity-grade fiber, but battery-specific formats—including calendered papers, short-cut fibers, and needle-punched nonwovens—engineered for electrical insulation and thermal event containment.

In high-voltage EV platforms, particularly 800V systems, thermal propagation speed is the dominant safety risk. Meta-aramid fibers retain structural integrity up to ~232°C (450°F) without melting or dripping, providing a critical delay window during thermal runaway events. OEM-facing developments by Teijin Aramid and DuPont increasingly focus on composite insulation stacks rather than standalone fabrics, integrating meta-aramid layers with mica and ceramic coatings to meet next-generation pack-level abuse tests.

At the component level, short-cut meta-aramid fibers (≈2.2 dtex) are gaining traction in wetlaid processes to produce high-dielectric insulation papers. These materials are now standard in EV transformer gaskets, busbar insulation, and cell-to-pack separators, where they outperform glass fiber and polyester in arc resistance, flame retardancy, and dimensional stability under cycling heat loads.

Trend 2: Development of Hybrid Fabrics with Basalt and Carbon Fiber

The market is rapidly shifting from mono-material meta-aramid textiles to hybrid fabric architectures that combine aramid’s ductility with the stiffness of carbon fiber and the cost-efficiency of basalt. This trend reflects a broader engineering logic: optimize energy absorption per unit weight rather than maximize single-property performance.

Empirical research published in early 2025 demonstrates that aramid–basalt hybrid laminates can absorb ~26% more impact energy than basalt-only systems and nearly double the energy absorption of pure aramid laminates. This performance gain stems from staggered failure modes—basalt contributing compressive stiffness, aramid dissipating energy through fibrillation—making these hybrids particularly attractive for aerospace fire-blocking layers, ballistic armor, and multi-hit protection systems.

From a mechanical standpoint, hybridization materially improves flexural performance. Introducing basalt into carbon/aramid stacks has been shown to raise flexural modulus into the 18–25 GPa range, while improving cost–performance efficiency by roughly 40% versus carbon-dominant designs. In aircraft interiors, meta-aramid honeycomb cores paired with carbon skins are now standard for partitions, floors, and sidewalls—delivering 40–60% weight reductions while maintaining FAA/EASA smoke, flame, and toxicity (FST) compliance.

Opportunity 1: Thermal Runaway Protection for Energy Storage Systems (ESS)

Grid-scale energy storage is emerging as one of the highest-value growth vectors for meta-aramid fibers, driven almost entirely by regulation. The NFPA 855 (2026 Edition) and harmonized UL 9540A large-scale fire testing protocols are transforming fire barriers from optional safeguards into mandatory system components.

Under the new Large-Scale Fire Testing (LSFT) framework, ESS developers must demonstrate that full combustion of a battery enclosure does not trigger thermal runaway in adjacent units. Meta-aramid fabrics—integrated into REI 90 to REI 120 fire-rated assemblies—are becoming essential to achieve these two-hour containment thresholds. Operators are also adopting “controlled burn-out” design philosophies under the International Fire Code (IFC 2024), which rely on aramid-based blankets and internal barriers to prevent explosion propagation in dense urban installations.

Regionally, implementation is accelerating. In mid-2025, India’s Central Electricity Authority issued draft safety guidelines for 100 MWh-class BESS projects, mandating fire-resistant fencing and enclosure materials. This alone creates a substantial addressable market for weatherproof, UV-stable meta-aramid systems across one of the world’s fastest-growing grid storage regions.

Opportunity 2: Lightweight, High-Temperature Filtration for Industrial Processes

Industrial decarbonization is opening a second, structurally durable opportunity for meta-aramid fibers in high-temperature filtration. Cement, steel, and chemical producers are upgrading dust collection systems to meet tighter particulate matter (PM) and emissions standards—conditions where conventional polyester or polypropylene filters fail.

Advanced meta-aramid needle felts (typically ~500 g/m²) are now engineered for continuous operation at ~204°C with short-term excursions up to 240°C, while maintaining alkali resistance and dimensional stability. In cement kilns and steel furnaces, these properties allow sustained filtration of hot flue gases without fiber shrinkage, melting, or loss of airflow—directly supporting zero-emission compliance strategies.

A notable secondary opportunity is emerging in mechanically recycled meta-aramid fibers. In 2025, recycled grades are increasingly used in non-critical filtration and secondary protective layers, retaining inherent flame resistance while offering a lower-cost, circular-economy alternative for industrial operators seeking to reduce material intensity without compromising safety.

Market Share Analysis: Meta-aramid Fiber Market

Market Share by Grade: Standard Grade Meta-aramid as the Backbone of Volume and Compliance

Standard grade meta-aramid fibers command approximately 65% of total market share because they represent the most economically and functionally efficient solution for large-scale fire-protection and thermal insulation requirements. Unlike specialty high-tenacity variants that are optimized for niche aerospace or ballistic uses, standard grades deliver the core value proposition of meta-aramids: inherent flame resistance, long-term durability, and textile-level comfort at scale. Their ability to withstand degradation only beyond 370–400°C, without melting or dripping, makes them structurally superior to flame-retardant treated cotton, whose protection erodes with laundering and chemical exposure. From a procurement standpoint, the 300–400 mN/tex tenacity range is a critical sweet spot—strong enough for industrial garments, filtration fabrics, and insulation felts, yet flexible enough to avoid stiffness-related wearer fatigue, which directly impacts adoption in utilities, oil & gas, and manufacturing environments. Additionally, a Limiting Oxygen Index above 28% ensures self-extinguishing behavior under real-world fire scenarios, aligning with increasingly strict 2025 OSHA and EU workplace safety mandates. The segment’s dominance is further reinforced by its exceptional radiation resistance, allowing standard-grade fibers to serve dual roles in nuclear facilities and medical environments where material degradation is unacceptable. Collectively, these attributes explain why standard grade meta-aramid remains the default, high-volume choice across global safety-driven industries.

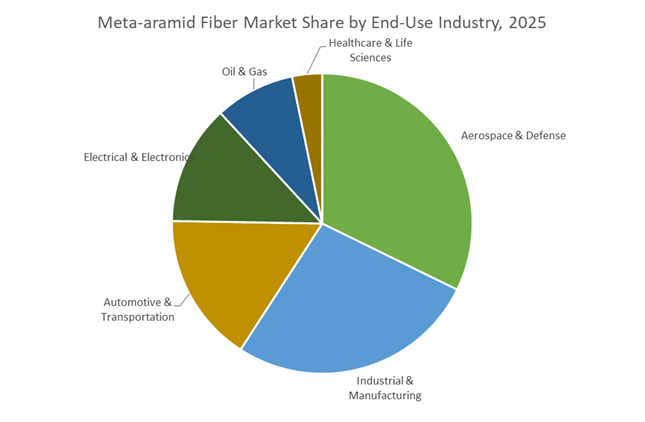

Market Share by Application: Aerospace & Defense Driving High-Value Meta-aramid Demand

Aerospace & Defense accounts for around 30% of total meta-aramid fiber demand, making it the largest single application segment by value, if not volume. This leadership position is anchored in the aerospace industry’s structural transition toward lighter, all-composite aircraft interiors, where fire safety, weight reduction, and long service life are mission-critical. Meta-aramid honeycomb cores—used in roughly 80% of modern commercial aircraft interiors—form the internal skeleton of flooring, ceilings, and sidewalls, delivering unmatched stiffness-to-weight ratios that reduce interior mass by 15–20% compared to aluminum alternatives. In parallel, defense and next-generation aerospace platforms increasingly rely on meta-aramid electrical insulation that retains around 95% of dielectric strength after prolonged exposure to 200°C, a requirement driven by the electrification of aircraft subsystems and hybrid-electric propulsion concepts. For military procurement, the 10-year, zero-degradation flame resistance of meta-aramid flight suits represents a clear lifecycle cost advantage over treated fabrics that require frequent replacement. Beyond fire protection, the material’s low dielectric constant (below 2.0) positions it as a strategic enabler for radomes and UAV structures, where radar transparency is non-negotiable. These converging performance, safety, and lifecycle economics factors firmly anchor Aerospace & Defense as the most strategically influential application segment in the meta-aramid fiber market.

Competitive Landscape: Differentiated Technical Platforms and Application Playbooks

The meta-aramid supplier landscape is led by vertically integrated technology leaders and regional scale producers. Winners combine material science (sulfone/imidic chemistries, solution dyeing), validated performance data (LOI, long-term thermal retention, dielectric tests) and a range of product formats (staple fiber, filament, pulp, paper) to serve PPE, electrical insulation, filtration and aerospace cores.

Dupont (Nomex®) Remains the Benchmark For Electrical Paper and Firefighter Textiles

DuPont’s Nomex® brand is the originator and continues to dominate mission-critical segments. Nomex® 410 paper is the global benchmark for medium- and high-voltage dry-type transformers with >95% market penetration; Nomex fibers and fabrics are widely used in firefighter turnout gear and aerospace interiors. DuPont’s product strategy blends lighter-weight constructions (3D weaving, finer deniers) to improve wearer comfort (~15% weight reduction) while preserving TPP, and its Nov/Dec 2024-2025 initiatives (dyeable fabric partnership; Nomex® Xtreme FR in Dec 2025) expand use cases into colorable PPE and electrostatic-safe protective apparel. Nomex’s depth in electrical, thermal and regulatory validation (long history of application data) remains a powerful market moat.

Teijin (Teijinconex®) Pairs Meta-Aramid Filament Innovation with Hybrid Aramid Systems

Teijin leverages a dual aramid portfolio - Teijinconex® (meta) and Twaron® (para) - enabling bespoke hybrid solutions that balance thermal stability and tensile strength. Teijin’s dope-dyed and neo grades deliver permanent color fastness and laundering UV stability, addressing professional workwear needs. The company’s Feb 2025 filament launch for high-temp sewing threads and hot-gas filtration emphasizes thread and filter reliability under prolonged heat. Teijin also invests in chemical-recycling and resource-efficiency R&D to support circularity for end-of-life aramid products, notably in industrial protective textiles and engineered nonwovens.

Kermel Positions Its Polyamide-Imide Meta-Aramid for Extreme Thermal and Chemical Environments

Kermel® (polyamide-imide classified as meta-aramid) differentiates on solution dyeing and enhanced chemical resistance (notably to cold acids/solvents). Kermel grades report LOI and extreme short-term thermal integrity up to very high temperatures and are optimized for firefighter turnout gear and hot-gas filtration systems. With product blends like V50/V70 (with Lenzing FR) the company improves wearer moisture management (moisture regain ≈7%), targeting user comfort in prolonged operations. Kermel’s focus on blends and filtration reflects a strategic niche in high-temperature, chemically aggressive service environments.

Yantai Tayho Scales APAC Supply with Full-Form Meta-Aramid Product Lines At Competitive Cost

Yantai Tayho (Newstar®) has expanded capacity (final phase completed Oct 2025) and emphasizes large-scale staple fiber, filament yarn and pulp production to serve cost-sensitive industrial markets across Asia. Its portfolio addresses nonwovens, aramid paper and reinforcement markets (>80% of local manufacturing needs) and targets export growth into Europe/North America via international certifications. Yantai’s scale provides price competitiveness for applications such as automotive hose reinforcement, gaskets and general PPE, making it a go-to supplier where cost and regional supply security are decisive.

South Korea has emerged as one of the most technology-integrated production hubs in the global meta-aramid fiber market, combining smart manufacturing with EV-driven demand. In 2025, Hyosung Advanced Materials completed a landmark expansion that doubled its meta-aramid capacity to 15,310 metric tons, embedding AI-enabled quality control and eco-efficient spinning processes. This upgrade has materially improved fiber uniformity and thermal stability—critical parameters for EV tire cords, turbocharger hoses, and flame-resistant industrial textiles.

Parallel to capacity growth, Kolon Industries has reoriented its aramid portfolio toward meta-aramid paper for electrical insulation, targeting global transformer grids and hybrid traction motors. South Korea’s battery ecosystem further amplifies demand: domestic suppliers are now embedding meta-aramid thermal barriers into high-capacity battery packs for LG Energy Solution and SK On, addressing thermal runaway risks as energy densities rise.

China: Volume Leadership, Dual-Use Controls, and Filtration Demand

China continues to dominate global volumes while pivoting toward precursor self-reliance and export governance. Yantai Tayho Advanced Materials Group, producer of the Metastar brand, reported $518 million in trailing 12-month revenue (as of September 30, 2025), underscoring financial resilience as it integrates spandex and meta-aramid lines to optimize protective apparel economics.

Regulatory oversight intensified in November 2025, when Ministry of Commerce of the People's Republic of China (MOFCOM) expanded dual-use export monitoring to high-tenacity synthetic fibers, directly affecting aerospace-grade meta-aramids. Domestically, environmental mandates under the 14th Five-Year Plan are driving a surge in high-temperature filtration media; production of meta-aramid filter bags for cement and steel plants delivered ~5.6% YoY growth in 2025, anchoring steady internal consumption despite export controls.

Japan: Digital Product Passports and GX 2040 Sustainability

Japan leads on traceability, sustainability, and premium-grade differentiation in the meta-aramid fiber market. In April 2025, Teijin Limited became the first major aramid producer to deploy Digital Product Passports (DPP) across its meta-aramid portfolio, using blockchain-enabled traceability to verify material origin, recycling pathways, and compliance with Europe’s ESPR requirements.

This digital leap aligns with Japan’s GX 2040 Vision (Cabinet-approved January 18, 2025), which channels R&D subsidies toward carbon-neutral aramid grades. Capacity expansion is reinforcing supply: Toray Industries advanced its dry-spinning meta-aramid program at the Gumi Plant via its Korean subsidiary, lifting capacity to ~3,000 tons per year in 2025 to serve high-temperature industrial workwear and filtration applications.

United States: Defense Modernization and Tariff-Led Reshoring

The U.S. meta-aramid fiber market is being reshaped by defense procurement priorities and trade-driven localization. While para-aramids dominate ballistic use, DuPont has set a benchmark for multi-risk protection through its Kevlar® EXO™ ecosystem—integrating meta-aramid flame resistance into next-generation protective gear for North American law enforcement and military users.

In Spring 2025, tariff escalations on imported synthetic textiles accelerated reshoring of meta-aramid paper for smart grid insulation and aerospace interiors. Concurrently, FAA and DoD 2025 procurement guidelines tightened domestic content requirements for honeycomb cores used in military aircraft, directly benefiting U.S.-based producers of meta-aramid paper substrates with verified local supply chains.

France: EU-REACH Leadership and Firefighter Protection

France functions as Europe’s specialized hub for compliant, high-durability meta-aramid fibers, particularly for personal protective equipment (PPE). In December 2025, Kermel unveiled advanced UV-stable meta-aramid fibers engineered to retain >90% tensile strength after prolonged UV exposure, a decisive advantage for outdoor military, utility, and firefighter applications.

French producers are also at the forefront of ESPR compliance (effective July 2024), transitioning to closed-loop solvent recovery and low-emission processing by 2025. Public-sector demand reinforces scale: France’s 2025–2027 safety roadmap allocates substantial funding to upgrade FR garments for national firefighters and armed forces using meta-aramid blends, locking in multi-year procurement visibility.

India: PLI-Fueled Export Growth and Industrial Compliance

India is rapidly ascending as a cost-competitive exporter of meta-aramid-based technical textiles under strong policy support. In 2025, the ₹10,683 crore (~$1.3 billion) PLI scheme for technical textiles enabled several domestic firms to commission aramid-reinforced fabric plants, strengthening India’s position in protective apparel and industrial filtration.

Demand is reinforced by regulation and exports. India’s defense exports reached ₹23,622 crore in FY 2024–25, with meta-aramid uniforms and safety equipment gaining traction across Middle Eastern and African markets. At home, tighter CPCB emission norms (2025) are catalyzing large-scale adoption of meta-aramid high-temperature filter bags across power, cement, and chemical plants—creating a stable domestic demand floor alongside export growth.

2025 Strategic Matrix: Meta-aramid Fiber Development

Meta-aramid Fiber Development Matrix

|

Country

|

Primary Technical Focus

|

2025 Strategic Milestone

|

Key Material Grade

|

|

South Korea

|

Smart manufacturing & EV safety

|

Hyosung capacity doubled to 15.3k tons

|

EV-grade meta-aramid

|

|

China

|

Export controls & filtration

|

MOFCOM dual-use licensing (Nov 2025)

|

Metastar aramid paper

|

|

Japan

|

Sustainability & traceability

|

Teijin DPP launch (Apr 2025)

|

Recycled meta-aramid pulp

|

|

United States

|

Defense reshoring

|

Spring 2025 tariff adjustments

|

FR honeycomb substrates

|

|

France

|

Personal protection & compliance

|

Kermel UV-stable fiber innovation

|

Multi-risk FR fabrics

|

|

India

|

Industrial compliance & exports

|

₹23.6k Cr defense export milestone

|

High-temp filter media

|

Meta-aramid Fiber Market Report Scope

Meta-aramid Fiber Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2035)

|

$14.5 Billion

|

|

Market Growth Rate

|

11.7%

|

|

Segments

|

By Product Form (Filament, Staple Fiber, Paper, Pulp), By Grade (Standard Grade, High-Performance / High-Tenacity Grade, Sustainability Grade), By Application (Protective Clothing, Electrical Insulation, Hot Gas Filtration, Honeycomb Cores, Automotive, Thermal Barriers), By End-Use Industry (Aerospace & Defense, Automotive & Transportation, Electrical & Electronics, Industrial & Manufacturing, Oil & Gas, Healthcare & Life Sciences)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours Inc., Teijin Limited, Yantai Tayho Advanced Materials, Toray Industries Inc., Huvis Corporation, Kermel S.A., Kolon Industries Inc., X-FIPER New Material, Hyosung Advanced Materials, Aramid HPM, Shanghai Sino-Arid Fiber, SRO Group (China), Jstar (Chengdu) New Material

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Meta-aramid Fiber Market Segmentation

By Product Form

- Filament

- Staple Fiber

- Paper

- Pulp

By Grade

- Standard Grade

- High-Performance / High-Tenacity Grade

- Sustainability Grade

By Application

- Protective Clothing

- Electrical Insulation

- Hot Gas Filtration

- Honeycomb Cores

- Automotive

- Thermal Barriers

By End-Use Industry

- Aerospace & Defense

- Automotive & Transportation

- Electrical & Electronics

- Industrial & Manufacturing

- Oil & Gas

- Healthcare & Life Sciences

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Meta-aramid Fiber Market

- DuPont de Nemours, Inc

- Teijin Limited

- Yantai Tayho Advanced Materials Co., Ltd

- Toray Industries, Inc

- Huvis Corporation

- Kermel S.A

- Kolon Industries, Inc.

- X-FIPER New Material Co., Ltd.

- Hyosung Advanced Materials

- Aramid HPM

- Shanghai Sino-Arid Fiber Co., Ltd.

- SRO Group (China) Limited

- Jstar (Chengdu) New Material Co., Ltd.

*- List not Exhaustive