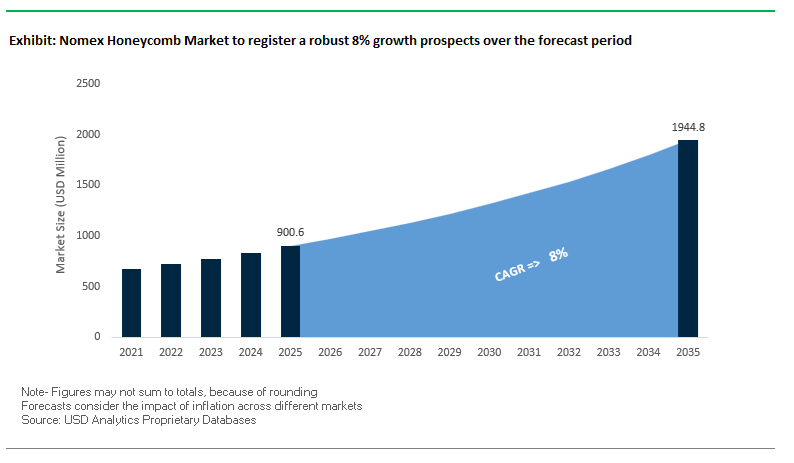

The Nomex Honeycomb Market, valued at USD 900.6 million in 2025, is projected to reach USD 1,944.3 million by 2035, registering a strong CAGR of 8% during 2025–2035. Growth is fueled by advanced aerospace programs, the rise of eVTOL/UAM aircraft, next-generation railway interiors, and a structural shift toward high-specific-stiffness composite sandwich panels with stringent FST (Fire, Smoke, Toxicity) compliance requirements.

The Nomex Honeycomb Market is undergoing rapid transformation driven by aerospace production rate increases, next-generation propulsion systems, and UAM platform certification programs. In November 2025, Hexcel introduced its Flex-Core® HRH-302 BMI-coated Mid-Temperature core, a critical advancement enabling Nomex honeycomb to withstand elevated temperatures in engine nacelles and hot-zone fairings. The shift toward BMI resin systems signals a rising need for aramid cores that can survive demanding thermal gradients in hybrid-electric propulsion and next-gen commercial aircraft architectures.

In September 2025, Hexcel substantially expanded its Americas Aerospace Distribution Network for HexWeb® aramid paper cores, anticipating increased production rates for the A320neo and 737 MAX programs. The move supports OEM backlog reduction and strengthens supply chain resilience amid persistent industry headwinds. Earlier in August 2025, the U.S. GAO identified aerospace-grade Nomex honeycomb as a top three supply-chain constraint for Boeing and Airbus—underscoring the strategic importance of securing qualified core suppliers with uninterrupted material flow. The elevated dependency on few raw-material producers, particularly DuPont’s meta-aramid paper, intensifies competitive leverage within the supply chain.

DuPont’s structural repositioning in June 2025, splitting into two publicly traded companies, confirmed that the New DuPont will retain its Performance Materials & Protection segment, ensuring long-term continuity for the Nomex® brand within aerospace, defense, and industrial composites. Meanwhile, Tier 1 suppliers continue to reinforce market expansion. In March 2025, The Gill Corporation secured a supply contract with Sonaca for Gillcore® aramid honeycomb on multiple Airbus aircraft, strengthening its presence in critical flight-control components. The emerging Urban Air Mobility (UAM) sector, as of January 2025, reported a 60% increase in composite R&D investment, driving demand for ultra-light Nomex honeycomb optimized for battery endurance, noise control, and energy efficiency.

Innovation momentum also stems from Europe. In late 2024, Euro-Composites rolled out its 3-Dimensional formable Nomex® honeycomb, featuring rectangular cells that dramatically reduce manufacturing cost and time for complex curved surfaces including railway interiors, lavatories, and fuselage interiors. Concurrently, Plascore received renewed qualification emphasis for its PN1 Commercial Grade Aramid Honeycomb, which delivers 10-year shelf life and compatibility with a wide range of resin systems, expanding adoption in marine, industrial, and radome applications. Together, these developments emphasize a global market pivot toward specialty Nomex honeycomb solutions with enhanced formability, higher heat resistance, sustainability value, and multi-sector adaptability.

For composite engineers and procurement leaders, Nomex honeycomb is assessed based on ultra-low density, shear anisotropy, compatibility with CFRP skins, and guaranteed FAA flammability performance. Buyers also focus on raw-material availability, forming performance for curved panels, and qualification to Airbus/Boeing material specs.

- Ultra-low density benchmark (1.5 PCF / 24 kg/m³): Enables highest specific stiffness for interior panels and lightweight airframe sections.

- FST leadership: Phenolic-coated Nomex honeycomb maintains dominance with 66.78% share of commercial aircraft floor panels (2024) due to industry-leading fire resistance.

- Zero galvanic corrosion: Meta-aramid composition eliminates galvanic interaction with CFRP, supporting its adoption in primary and secondary carbon composite structures.

- Orthotropic shear performance: L-direction shear modulus is 1.5–2× higher than W-direction—critical for load paths in leading edges, nacelle panels, and floor systems.

- Raw-material volatility: DuPont Nomex paper shipments grew 27% (Jun 2024–May 2025), reflecting persistent demand and contributing to market tightness and elevated pricing.

Advanced Hybridization, Structural Displacement Dynamics, and Sustainability Pathways Shape the Nomex Honeycomb Market

Trend 1 - Hybrid Nomex Honeycomb Panels and Evolving Resin Systems Gain Priority in Next-Generation Aircraft Interiors

Aerospace manufacturers are accelerating their transition toward multi-material hybrid Nomex honeycomb panels, driven by stricter Fire, Smoke, and Toxicity (FST) compliance requirements and the industry-wide push for lighter, thinner, and more durable interior components. Nomex honeycomb inherently satisfies the stringent flammability standards defined in FAR 25.853, making it the foundation for sandwich structures in sidewalls, ceilings, galley panels, and partitions.

The shift toward hybridization is fueled by composite suppliers pairing standard phenolic or epoxy Nomex cores with reinforced thermoplastic laminates (RTL). These hybrid panels unlock superior surface quality, greater impact durability, and improved aesthetics without compromising FST performance. This evolution supports the growing demand for visually refined aircraft cabin interiors while preserving structural efficiency.

Customization flexibility remains a central differentiator. Aerospace-grade Nomex cores, typically ranging from 29 kg/m³ to 64 kg/m³, enable weight-optimized design depending on component duty-ranging from ultra-lightweight sidewalls to mechanically demanding floor structures. Furthermore, the aramid paper and phenolic resin system in Nomex Honeycomb withstand continuous service temperatures up to 180°C (356°F), ensuring reliable operation in thermally stressed regions near ducts, lavatory modules, and air-conditioning routing zones.

As regulatory and OEM-driven FST requirements tighten, the rising adoption of hybrid Nomex sandwich systems is setting a new benchmark for performance, weight efficiency, and durability in aircraft interiors.

Trend 2 - Nomex Faces Competitive Substitution from PMI Foam and Aluminum Cores in Structural Aerospace Applications

While Nomex Honeycomb dominates aircraft interiors, it faces growing competition in structural and semi-structural aerospace components where compression strength, moisture resistance, and thermal conductivity are key differentiators. In ultra-lightweight applications, Nomex retains an edge with a density of about 0.029 g/cm³, which is considerably lower than most PMI (Polymethacrylimide) foams, reinforcing its dominance in sidewalls, fairings, and non-load-bearing panels.

However, PMI foams offer superior compressive strength and damage tolerance, making them attractive for applications requiring higher structural performance. Meanwhile, aluminum honeycomb cores are being adopted for components in high-impact, high-temperature, or thermally conductive environments such as engine cowls, flaps, and exhaust fairings. Aluminum cores offer an advantageous balance of cost, rigidity, conductivity, and mechanical strength, especially in secondary structural applications.

One of the key trade-offs influencing market substitution is Nomex’s lower compressive strength-often around 0.8 MPa for the lightest grades-compared with PMI or aluminum solutions. As aircraft structures evolve toward higher load-bearing multifunctional components, designers increasingly evaluate performance-to-cost ratios, prompting selective displacement of Nomex in specific areas of next-generation aerostructures.

Despite this competitive landscape, Nomex Honeycomb maintains an irreplaceable role in applications where ultra-low weight, flame resistance, and acoustic damping outweigh compressive strength requirements.

Opportunity 1 - Nomex Honeycomb Penetrates EV and High-End Automotive Structures Through Lightweighting and Thermal Safety Advantages

As Electric Vehicle (EV) manufacturers face mounting pressure to maximize battery efficiency and reduce overall mass, high-performance Nomex Honeycomb structures are emerging as viable candidates for advanced automotive components. Their adoption builds on Nomex’s long heritage in motorsport, where its exceptional stiffness-to-weight ratio and impact absorption have been used in composite monocoques and crash structures.

In premium OEM and low-volume EV production, Nomex cores are now incorporated into floors, interior body panels, crash management systems, and structural energy absorbers. Their ability to significantly reduce vehicle weight directly improves driving range-one of the highest priorities in EV engineering.

A critical advantage lies in Nomex’s fire resistance and superior electrical insulation properties, which position it favorably for applications in battery enclosures, thermal barriers, and high-voltage component insulation. Nomex paper, the foundational material for honeycomb cores, is already widely used in motor windings and power electronics because of its resistance to thermal degradation and dielectric breakdown.

As EV architectures transition toward more complex multi-material platforms, Nomex Honeycomb offers OEMs a pathway to combine safety, mechanical robustness, and lightweighting in next-generation vehicle design.

Opportunity 2 - Advancements in Recyclable and Bio-Based Aramid Paper Unlock Sustainable Honeycomb Core Manufacturing

Sustainability-driven regulatory shifts in aerospace, automotive, and composite manufacturing are accelerating R&D into recyclable and bio-based Nomex Honeycomb alternatives. This marks a fundamental industry pivot toward circular materials, aligning with global carbon reduction goals and OEM sustainability mandates.

Manufacturers are investing in technologies that incorporate recycled aramid fibers and bio-based resin binders into aramid paper production to reduce environmental impact without sacrificing performance. These initiatives parallel broader industry movements to reduce thermoset waste, improve core recyclability, and enable end-of-life reclamation of fiber materials as composite waste volumes rise globally.

Research pipelines include development of thermoplastic fiber papers and bio-based polymer core sheets, which promise enhanced recyclability versus traditional thermoset-impregnated cores. Patent literature highlights the potential for these new materials to be used in hybrid honeycomb panels, maintaining stiffness and FST performance while offering improved environmental compatibility.

This wave of innovation offers suppliers a lucrative opportunity to differentiate through sustainable material portfolios, especially as aerospace OEMs intensify focus on climate-neutral manufacturing and circular supply chain frameworks.

Nomex Honeycomb Market Share Analysis

Market Share by Density: Low-Density Nomex Honeycomb Leads Through Maximized Lightweighting and Compliance with Aerospace Interior Requirements

Low-density Nomex honeycomb cores (≤2.0 lb/ft³) command a dominant 55% share of the Nomex Honeycomb Market, driven by their unparalleled ability to deliver extreme lightweighting while maintaining the structural integrity necessary for aircraft interior components. In commercial aircraft cabins—where Nomex honeycomb is most widely used—the primary engineering objective is to achieve the lowest possible mass without compromising performance or safety. Low-density cores excel in this role because their hexagonal cell geometry delivers high specific stiffness and sufficient shear strength for secondary structural elements such as sidewalls, ceiling panels, bulkheads, luggage bins, and galley structures. These are areas where bending loads are modest but weight reduction is critical, making low-density Nomex the default material choice. With densities at or below 2.0 lb/ft³, these cores ensure that finished sandwich panels consist largely of “air,” producing dramatic reductions in component mass and yielding substantial improvements in aircraft fuel efficiency. Their dominance is further reinforced by their broad certification history and the fact that interior applications—where lightweight cores are standard—represent the largest cumulative surface area inside commercial aircraft. As aircraft manufacturers continue prioritizing cabin modernization, fuel burn reduction, and sustainability across fleets, low-density Nomex cores remain indispensable, securing their leading market share across global aerospace production programs.

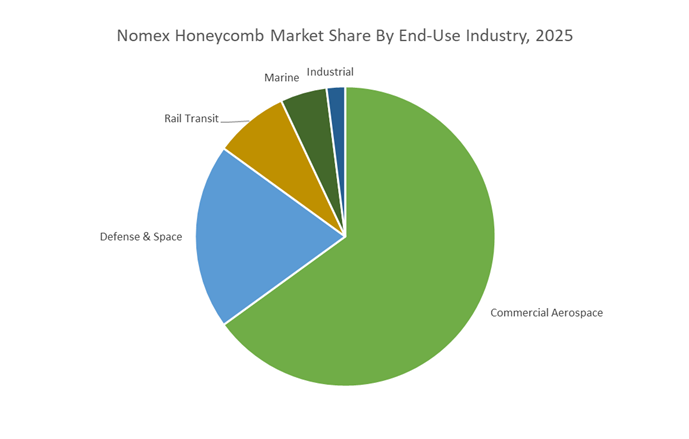

Market Share by End-Use Industry: Commercial Aerospace Dominates Through Stringent Flammability Standards and High-Volume Interior Panel Demand

Commercial Aerospace holds the leading 65% share in the Nomex Honeycomb Market, reflecting the material’s essential role in meeting the highly regulated performance and fire safety requirements governing aircraft interiors. Nomex honeycomb, manufactured from aramid paper and phenolic resin, is uniquely engineered to comply with FAR 25.853 flammability, heat release, and smoke emission standards, making it the material of record for virtually all OEM cabin applications. Its inherent fire resistance, self-extinguishing properties, and low smoke toxicity ensure it satisfies aviation authorities’ most demanding criteria—requirements that alternative core materials often fail to meet. This regulatory compatibility underpins its widespread deployment across more than 60% of interior aircraft components, including flooring systems, seat structures, monuments, overhead bins, and integrated panel assemblies. The sheer production volume of commercial aircraft—from single-aisle narrowbodies to widebody long-haul jets—creates a large, recurring demand pool, as every aircraft requires thousands of square feet of Nomex-based panels.

Additionally, the long-term operational benefits reinforce adoption: lightweight Nomex honeycomb contributes directly to reduced fuel consumption, with each pound of weight reduction saving an estimated $10,000+ over an aircraft’s 20–30 year lifecycle. This economic rationale makes the premium cost of Nomex honeycomb a strategically justified investment for OEMs and airlines alike. As global air travel markets expand and fleet renewal accelerates, particularly with next-generation composite-intensive aircraft platforms, the Commercial Aerospace segment is positioned to retain its dominant share in the Nomex honeycomb industry.

Country Analysis: Global Nomex Honeycomb Development Hubs

United States: High-Thermal Nomex® Honeycomb Engineering Driven by Aerospace, UAM, and Defense Programs

The United States continues to dominate the Nomex® Honeycomb Market through its unrivaled aerospace and defense industrial base, advanced composite manufacturing capabilities, and strong investment in next-generation thermal and acoustic core materials. The U.S. remains the central hub for high-performance Nomex® aramid honeycomb development, driven by rising demand from commercial aviation, Urban Air Mobility (UAM), and military platforms requiring lightweight cores with exceptional thermal resistance, flame retardancy, and dimensional stability. In 2025, Hexcel Corporation introduced the Flex-Core® HRH-302 Mid-Temperature Nomex® Honeycomb, engineered for service temperatures up to 450°F. This positions the material directly for high-thermal-demand applications such as future propulsion systems, electric aircraft, and UAM vehicles. Additionally, the HexWeb® HRH-10 NOMEX® line remains a benchmark for formability, enabling manufacturers to shape cores into highly complex contours—ducts, nacelle structures, leading edges—while reducing anticlastic curvature and lowering total manufacturing costs.

Acoustic efficiency is another domain where the U.S. leads. Technologies such as HexWeb® Acousti-Cap® enable designers to integrate broadband sound-absorbing capabilities into nacelles and engine housings without adding structural weight, supporting FAA and OEM initiatives to reduce aircraft noise signatures. Defense applications continue to accelerate adoption, as meta-aramid honeycomb cores provide ballistic resistance, flame retardancy, and lightweight structural support in UAVs, naval vessels, and next-generation airborne platforms. Supply chain reliability is also a strategic U.S. strength: in September 2025, Hexcel expanded its Americas Aerospace Distribution Network, reinforcing material availability for Tier 1 suppliers and ensuring consistent supply continuity for mission-critical programs across aerospace and defense markets.

Europe (France/Germany): Nomex® Honeycomb Innovations Aligned With FST Compliance and Airbus Interior Programs

Europe—particularly France and Germany—forms a critical development hub for FST-compliant Nomex® Honeycomb, sustained by rigorous EU transportation safety standards and the high production rates of Airbus commercial aircraft. The region’s regulatory framework, especially the EN 45545-2 standard, dictates material behavior under fire for all rail vehicles and strengthens requirements for flammability, smoke toxicity (T12), and heat release. These regulations directly influence the design and manufacturing of Nomex® honeycomb cores and bonded composite panels across both aerospace and rail interiors. Academic and OEM-funded studies confirm that carbon/Nomex® honeycomb composites used in ceiling panels demonstrate extremely low heat release rates and delayed ignition times under high heat flux conditions (e.g., 40 kW/m²), underscoring their suitability for confined passenger cabin environments.

Europe’s manufacturing leadership is reinforced by specialized facilities from Euro-Composites S.A., Hexcel, and other suppliers that mass-produce aramid honeycomb cores for Airbus programs—including galleys, lavatories, bulkheads, and cabin walls. These materials must maintain dimensional stability, phenolic resin durability, and long-term fatigue resistance under fluctuating cabin humidity and thermal environments. Ongoing European R&D is refining phenolic dipping and bonding systems to enhance the performance of Nomex® honeycomb paper, targeting tighter tolerances, more consistent stiffness, and extended service life. This ecosystem of regulatory rigor, aerospace interior demand, and advanced materials science establishes Europe as a premier FST-oriented Nomex® honeycomb innovation hub.

China: High-Speed Rail Expansion and Domestic Aramid Honeycomb Substitution Strategy

China’s surging High-Speed Rail (HSR) expansion and growing domestic aircraft manufacturing sector have positioned the country as a major consumer and emerging producer of aramid paper honeycomb structures. In China’s HSR network—the largest globally—Meta-aramid Nomex-equivalent honeycomb cores are increasingly used in interior components such as ceilings, luggage racks, cabin frames, and doors, where flame retardancy and low smoke/low toxicity properties are essential for passenger safety. Domestic suppliers highlight the material’s performance advantage, noting that aramid honeycomb’s specific strength can reach up to 27× that of aluminum honeycomb, enabling significant vehicle weight reduction and improved energy efficiency across high-speed rail operations.

China is also strategically focused on reducing reliance on imported Nomex® materials. Domestic producers of aramid paper—including manufacturers of Metastar®-type materials—are expanding capacity and promoting local honeycomb core substitution for transportation, aerospace, and defense applications. With China intensifying its investment in aviation programs such as COMAC and expanding urban rail infrastructure, demand for fire-retardant, lightweight composite interior materials is expected to accelerate sharply. This domestic material push, supported by national manufacturing incentives and large-scale transportation programs, firmly positions China as a rising force in the Nomex® honeycomb market.

Japan: Aramid Fiber Precursor Leadership Supporting Ultra-High-Performance Honeycomb Structures

Japan plays a foundational role in the global Nomex® Honeycomb Market due to its leadership in manufacturing aramid fiber precursors, advanced reinforcements, and high-reliability composite materials used in honeycomb sandwich panels. Companies such as Toray Industries supply critical para-aramid and advanced composite fiber inputs required for producing both Nomex®-type honeycomb paper and high-performance composite skins, ensuring exceptional material fidelity and mechanical consistency. These precursor materials are essential for achieving aerospace-grade honeycomb characteristics, including high tensile strength, low density, and superior fatigue resistance.

Japanese manufacturers emphasize extreme quality control, minimizing microdefects that could compromise structural integrity in applications such as aircraft interiors, rotorcraft components, and precision industrial assemblies. Japan’s strengths in high-precision processing and specialty material science also support the production of honeycomb panels for electronics, robotics, and specialty industrial equipment requiring low dielectric loss, flame retardancy, and dimensional stability. Through its role as a vital upstream materials supplier, Japan continues to underpin global production of ultra-reliable Nomex® honeycomb composites.

Competitive Landscape: Leading Nomex Honeycomb Manufacturers & Strategic Capabilities

A handful of specialized composite core manufacturers dominate the Nomex Honeycomb Market, backed by strong aerospace qualifications, proprietary resin systems, and extensive material certifications. Competition revolves around core density control, forming technologies, resin impregnation quality, thermal stability, and ability to deliver build-to-print precision-machined cores for OEM assembly.

Hexcel remains the industry benchmark through its HexWeb® HRH-10/36 and premium aramid honeycomb ranges designed for aircraft secondary structures requiring high shear, compressive strength, and thermal resistance. Its vertical integration—producing its own phenolic and epoxy resin systems—enables precise control of cell wall impregnation and final core performance. The Flex-Core® product line allows heat-forming of simple curves, lowering labor time in interior monuments and panel assemblies. Hexcel’s ongoing R&D is centered on introducing recyclable thermoplastic honeycomb systems, a strategic shift aimed at long-term substitution in non-FST-critical sectors while preserving Nomex dominance in aviation.

DuPont holds a raw-material monopoly as the sole manufacturer of Nomex® meta-aramid paper, the precursor used by nearly all honeycomb converters. Its production facilities operated at high utilization through 2024–2025, with localized outages amplifying supply chain pressures and price volatility. DuPont’s strategic efforts focus on supply chain resilience, domestic capacity reinforcement, and price stabilization mechanisms to support aerospace OEMs and converters. Ongoing research initiatives include next-generation Nomex variants with improved moisture resistance and acoustic damping characteristics—critical attributes for aircraft cabin noise reduction and next-gen interior panel architecture.

Euro-Composites maintains a leading footprint in Europe’s aerospace and rail industries with its ECA® core family, offering densities from 24–200 kg/m³ and cell sizes from 3.2–19.2 mm. Its ECA-3D rectangular-cell core significantly enhances formability, enabling efficient manufacturing of curved aircraft lavatories, galleys, and train interiors. With strong involvement in producing finished sandwich panels and prefabricated composite kits, Euro-Composites acts as a turnkey supplier to Tier 1 integrators. Its deep product breadth supports customized solutions for both low-density interior panels and high-strength regional jet components.

Plascore extends Nomex honeycomb into diverse end-use sectors—including military vehicles, marine structures, radomes, and motorsport composites—leveraging the material’s superior creep resistance and fatigue behavior. Its PN1 Commercial Grade honeycomb meets stringent long-term storage requirements (10+ years) and offers over-expanded configurations ideal for simple-curve rotary-wing structures. Plascore’s specialized Machined Core business unit manufactures build-to-print precision core components that enter OEM assembly lines directly, ensuring tight tolerance control. Its phenolic-based production provides excellent dielectric properties for antenna fairings and radar systems.

The Gill Corporation differentiates itself through its Gillcore® HK para-aramid honeycomb, delivering improved performance in fatigue, strength, and weight reduction compared to standard Nomex meta-aramid cores. Gillcore® products are approved under critical aerospace specifications, including Boeing BMS 8-124 and Airbus AIMS 11-01-004, enabling deployment in flaps, ailerons, and other exterior aerodynamic structures. Its 2023 contract with Sonaca strengthens its position as a major Tier 1 supplier for Airbus composite structures. With a wide geometry portfolio—hexagonal and over-expanded cores with ribbon widths up to 1,651 mm and transverse dimensions up to 3,658 mm—The Gill Corporation is equipped to supply both narrow-body and wide-body aircraft markets.

Nomex Honeycomb Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$900.6 Million

|

|

Market Size (2035)

|

$1944.3 Million

|

|

Market Growth Rate

|

8%

|

|

Segments

|

By Aramid Paper Type (Meta-Aramid Paper, Para-Aramid Paper, Hybrid Aramid), By Resin Impregnation (Phenolic Resin, Polyimide Resin, Epoxy Resin), By Cell Geometry (Hexagonal Cell, Over-Expanded Cell, Flex-Core), By Density (Low-Density Cores, Medium-Density Cores, High-Density Cores), By End-Use Industry (Commercial Aerospace, Defense & Space, Rail Transit, Marine, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hexcel Corporation, DuPont de Nemours Inc., Euro-Composites S.A., Toray Advanced Composites, Teijin Limited, The Gill Corporation, Plascore Inc., Advanced Honeycomb Technologies, Safran S.A., TenCate Advanced Composites, Dolan Precision Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nomex Honeycomb Market Segmentation

By Aramid Paper Type

- Meta-Aramid Paper

- Para-Aramid Paper

- Hybrid Aramid

By Resin Impregnation

- Phenolic Resin

- Polyimide Resin

- Epoxy Resin

By Cell Geometry

- Hexagonal Cell

- Over-Expanded (OX) Cell

- Flex-Core®

By Density

- Low-Density Cores (≤2.0 lb/ft³)

- Medium-Density Cores (2.0–4.0 lb/ft³)

- High-Density Cores (>4.0 lb/ft³)

By End-Use Industry

- Commercial Aerospace

- Defense & Space

- Rail Transit

- Marine

- Industrial

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Nomex Honeycomb Manufacturers

- Hexcel Corporation

- DuPont de Nemours, Inc.

- Euro-Composites S.A.

- Toray Advanced Composites

- Teijin Limited

- The Gill Corporation

- Plascore, Inc.

- Advanced Honeycomb Technologies

- Safran S.A.

- TenCate Advanced Composites

- Dolan Precision, Inc.

*- List not Exhaustive