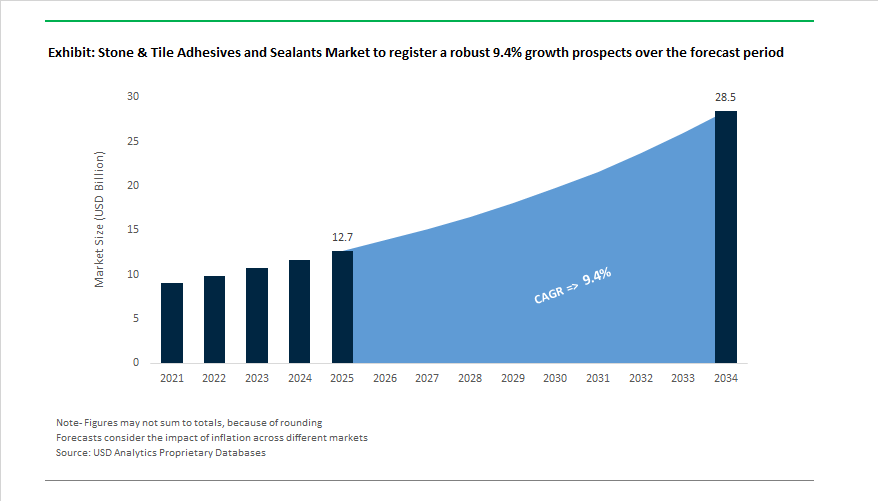

The Global Stone and Tile Adhesives and Sealants Market is projected to grow from USD 12.7 billion in 2025 to USD 28.5 billion by 2034, expanding at a robust CAGR of 9.4%. This double-digit growth trajectory reflects the escalating demand for high-performance, polymer-modified adhesives and flexible sealants in commercial construction, residential renovation, and infrastructure modernization projects. Industry professionals increasingly favor next-generation C2S1/C2S2 adhesives, high-movement sealants, and low-VOC, CO₂-neutral building materials, as developers and contractors pursue faster installation, enhanced durability, and compliance with sustainable building standards.

Modern tiling projects are evolving beyond traditional substrates, with large-format porcelain tiles, natural stone slabs, and façade installations requiring superior bond strength, deformability, and weather resistance. Global construction trends—particularly in data centers, airports, and smart urban infrastructure—are fueling adoption of specialized adhesive systems offering rapid-curing capability and structural flexibility. Further, the integration of digital construction technologies is driving a new generation of smart adhesive formulations that combine speed with structural integrity.

- Rapid-curing formulations (C2F adhesives) deliver adhesion strength exceeding 1.0 N/mm² within 6 hours, minimizing project downtime.

- High-movement sealants (±25% movement, ISO 9047) provide superior flexibility for exterior façades and structural applications.

- High-polymer modified mortars (C2S1/C2S2) ensure reliable bonding for low-porosity porcelain and natural stone materials.

- Sustainability leadership: Mapei’s CO₂-offset ‘Zero Line’ products neutralized 300,000 tonnes of emissions in 2024, marking a significant milestone in green construction chemistry.

- Growth in Asia-Pacific and Middle East regions continues to dominate demand, driven by rapid urbanization and government infrastructure programs.

The industry’s competitive dynamics reveal an aggressive phase of product innovation, capacity expansion, and sustainability transformation. In July 2024, Sika AG introduced SikaCeram-50 BH, a high-resistance, one-pack cementitious tile adhesive engineered for fast and precise ceramic installations. This innovation underscored Sika’s focus on ease of application and consistent performance across large-scale commercial projects. Earlier in April 2024, Sika expanded its adhesive manufacturing footprint across Indonesia and China, reinforcing its commitment to Asia-Pacific growth and ensuring localized supply for emerging construction markets. By January 2024, Sika’s integration of MBCC Group accelerated synergy realization, enhancing its leadership in construction adhesives, sealants, and waterproofing systems. Additionally, the company’s April 2024 investment in data center construction adhesives highlighted a strategic move toward high-spec industrial applications demanding thermal resistance and longevity.

Meanwhile, Mapei Group continues to demonstrate sustainability leadership. In February 2025, it was recognized as a Sustainability Champion 2024/25 for its comprehensive approach to low-carbon and eco-certified product lines. The company’s October 2025 acquisitions in Saudi Arabia, Bahrain, and Chile mark a calculated expansion into emerging high-growth markets, reinforcing its internationalization strategy. The expansion of the ‘Zero Line’ portfolio in 2024, covering 230 fully offset products, demonstrates Mapei’s long-term dedication to green construction and CO₂-neutral adhesives.

Henkel, through its Ceresit brand, focused on low-VOC interior solutions in July 2024, aligning its adhesive portfolio with evolving indoor air quality standards. Arkema’s December 2023 acquisition of Arc Building Products strengthened its construction polymer base, while LATICRETE’s June 2025 campaign for its 1 System platform showcased the company’s technological innovation in simplifying professional installation through integrated, high-performance systems.

Market Trend 1: Shift Towards Rapid-Curing, High-Performance Thin-Bed Mortars for Large-Format Tile and Slab Installation

The increasing adoption of large-format tiles (LFTs) and porcelain slabs—often exceeding 15 inches on one side—has redefined adhesive performance standards. Traditional thick-bed mortars are being replaced by thin-bed, polymer-modified, rapid-curing adhesives that deliver higher flexural strength, reduced shrinkage, and faster installation cycles.

Modern formulations comply with ANSI A118.15F standards, setting benchmarks for improved high-performance fast-setting cement mortars. In fact, premium-grade adhesives are engineered to reach required shear strength on impervious porcelain within just 4 hours, compared to the industry-standard 28-day curing period. The dramatic reduction translates into shorter project timelines and reduced labor costs, especially for large commercial projects like airports, malls, and hotels where every hour of downtime impacts profitability.

Flatness tolerance has become another key determinant of adhesive choice. The Tile Council of North America (TCNA) specifies a maximum variation of 1/8 inch over 10 feet for large-format installations. The pushes demand for non-slump, high-build, and deformable thin-bed adhesives that can level minor substrate imperfections while maintaining a minimum 95% mortar coverage, especially critical in wet and exterior applications.

Further, innovations such as Controlled Cure Technology™ have revolutionized installation speed and reliability. These adhesives achieve early high strength, allowing grouting in just three hours and full commercial traffic in under 24 hours. Such performance advantages are particularly valued in time-sensitive renovation projects, including retail, hospitality, and public infrastructure, where downtime costs are significant.

Market Trend 2: Proliferation of Low-Dust, Ready-to-Use Adhesive Mortars for Renovation and DIY Markets

The post-pandemic renovation boom and surge in DIY remodeling have accelerated the market’s shift toward ready-to-use and low-dust adhesive systems. Contractors and consumers alike are prioritizing health, safety, and ease of use—factors that have become critical differentiators in tile adhesive innovation.

Leading producers in Europe and North America have introduced Low-Dust Technology for cementitious adhesives, significantly reducing airborne particles during mixing and pouring. Independent testing confirms that these formulations cut airborne dust exposure by over 90%, drastically improving job-site air quality and ensuring safer installation environments—particularly in occupied spaces like hospitals, schools, and retail outlets.

In parallel, manufacturers are tapping into the DIY and light-commercial markets with pre-mixed, ready-to-use tile adhesive mortars. These bucket-packaged systems eliminate the complexity of on-site mixing, while proprietary polymer blends match or exceed the bond strength of cementitious mortars, even in high-moisture or vertical applications. Such innovation directly broadens consumer access, enabling non-professionals to achieve professional-grade results with minimal tools and expertise.

Sustainability is also shaping purchasing decisions. Adhesives carrying UL GREENGUARD and LEED-compatible certifications are seeing rising adoption in green construction projects. These products guarantee low VOC emissions and safer indoor air quality—critical benchmarks for institutional and healthcare developments pursuing LEED, WELL, or BREEAM certifications.

Market Opportunity 1: Development of Crack-Isolation and Uncoupling Membranes Integrated with Self-Leveling Adhesives

As flooring systems become more complex—integrating radiant heating, hybrid subfloors, and flexible building materials—the demand for integrated adhesive-membrane systems is rising sharply. These multi-functional adhesives combine waterproofing, crack-isolation, and leveling functions, drastically simplifying floor preparation and reducing the risk of substrate failure.

Advanced liquid-applied membranes formulated with polymer-modified elastomers are emerging as industry game-changers. These single-component, self-curing systems act simultaneously as waterproofing barriers and anti-fracture membranes, capable of curing within 2 hours before flood testing. The speed reduces downtime for installers, cutting the total installation cycle time by up to 40% compared to multi-step waterproofing systems.

Technology convergence is evident with the emergence of color-change cure indicators, which visually signal full cure readiness. The innovation eliminates uncertainty in flood-testing schedules, allowing contractors to proceed confidently with subsequent installation steps, such as tile setting and grouting, in as little as 12 hours.

These integrated solutions are especially advantageous for wet environments—including bathrooms, steam showers, and exterior decks—where performance reliability and waterproof integrity are paramount. The evolution of self-leveling adhesives that merge flexibility, moisture tolerance, and structural bonding marks a new phase of efficiency in professional tiling systems.

Market Opportunity 2: Formulation of Advanced Photocatalytic Grout Sealants with Self-Cleaning and Air-Purifying Properties

The future of grout and sealant technology lies in the convergence of hygiene, sustainability, and air purification, with photocatalytic coatings at the forefront. The integration of titanium dioxide (TiO₂) nanoparticles into sealant and grout formulations introduces self-cleaning and air-purifying functionalities that align with global green building and wellness initiatives.

Scientific research confirms that TiO₂ can catalyze the breakdown of nitrogen oxides (NOx) and volatile organic compounds (VOCs) into harmless end-products when exposed to light. The reaction not only keeps grout lines and tiles visibly cleaner but also actively contributes to improved indoor air quality—an innovation highly relevant for hospitals, schools, and premium residential projects.

Historical applications, such as the Cité des Arts et de la Musique in Chambéry, France, demonstrated the viability of photocatalytic mortars in large-scale construction. Modern advances extend the capability to grout and sealant products, offering consumers the benefit of low-maintenance, hygienic, and eco-active surfaces in interior spaces.

In addition, photocatalytic sealants help reduce the frequency and cost of cleaning cycles by promoting oxidation and decomposition of soiling deposits. The translates into long-term facility management savings, particularly for porous surfaces prone to discoloration. As building owners prioritize sustainability and operational efficiency, such photoactive functional sealants are expected to gain rapid commercial traction in both new construction and renovation markets.

Competitive Landscape: Strategic Profiles of Global Leaders

The global stone and tile adhesives and sealants market is consolidated around a few major players — Sika AG, Mapei Group, Henkel AG & Co. KGaA, LATICRETE International, and Tenax S.p.A. — each driving innovation, regional expansion, and sustainable transformation. These companies differentiate themselves through specialized chemistries, vertical integration, and smart construction systems that meet the performance and environmental demands of modern infrastructure.

Sika AG remains a cornerstone in the global adhesive and sealant ecosystem. With its Strategy 2028 targeting 6–9% annual growth and EBITDA margins of up to 23%, Sika combines aggressive geographic expansion with strong technological diversification. In 2024, the company expanded facilities in Singapore, Xi’an, and Morocco, boosting supply resilience. Its SikaCeram-50 BH cementitious adhesive reinforced its leadership in tile fixing solutions, while successful MBCC integration created a more synergized and comprehensive portfolio across tiling, waterproofing, and infrastructure repair systems. Sika’s targeted expansion into data center construction adhesives underscores its focus on specialized, durable, and high-margin applications.

Mapei Group continues to dominate through its four-pillar strategy—internationalization, specialization, R&D, and sustainability. Its Zero Line carbon-offset range, covering 230 eco-neutral products, positioned it as a benchmark for sustainable adhesive chemistry. Operating across 42 countries, Mapei ensures localized responsiveness and global consistency. Its participation in the restoration of Notre-Dame Cathedral and the Colosseum attests to the long-term durability of its formulations. Additionally, the company’s C-ADD segment in construction additives broadens its impact beyond adhesives, promoting a holistic construction solutions ecosystem.

Henkel leverages its global dominance in Adhesive Technologies through high-impact R&D investments and market-leading product innovation. The CERESIT brand anchors its construction portfolio, offering durable, waterproof tile adhesives optimized for wet rooms and structural bonding. Henkel’s ongoing Debonding-on-Demand adhesive development exemplifies its commitment to circular economy principles, enabling recyclability in construction components. By aligning with sustainable construction trends and smart manufacturing processes, Henkel continues to set the standard for industrial-grade adhesive innovation.

With over six decades of legacy, LATICRETE has built its reputation on complete installation systems that simplify workflows for contractors and designers. Its LATICRETE 1 System, featuring MULTIMAX™ 1 and SPECTRALOCK® 1, represents a new standard in efficiency and performance. Offering comprehensive substrate preparation, adhesive, and grout solutions, LATICRETE caters to architectural, exterior, and high-traffic applications. Its ANYCOLOR™ program adds a design dimension, offering custom-colored grouts and sealants that meet both aesthetic and structural requirements.

Tenax S.p.A. distinguishes itself through deep specialization in natural stone adhesives and restoration systems. Its product lineup includes epoxy and polyester mastics for marble, granite, and quartz, addressing the nuanced bonding requirements of dense and decorative stones. Tenax’s innovation in clear and color-matched stone adhesives meets the visual demands of high-end installations. With a strong global distribution network, Tenax supports fabricators and stone craftsmen with material science expertise and application-specific technical guidance, ensuring precision and durability across the stone value chain.

Country Analysis: Regional Developments in the Global Stone and Tile Adhesives and Sealants Industry

China – Expanding Urbanization and Technological Upgrades Drive Demand for Advanced Tile Adhesive Systems

China remains the epicenter of the Asia-Pacific stone and tile adhesives market, propelled by its record-breaking urbanization, infrastructure megaprojects, and industrial manufacturing ecosystem. Under the 14th Five-Year Plan, the Chinese government has allocated over USD 4.2 trillion toward transportation and urban renewal projects, directly boosting the consumption of cementitious tile adhesives, epoxy grouts, and high-flex bonding systems in both residential and commercial construction. Despite anti-dumping duties on ceramic exports to the EU (February 2024), the robust domestic demand and active trade with Southeast Asia have sustained high growth in low-VOC, polymer-modified tile adhesive production.

The shift toward large-format porcelain slabs and engineered stones has driven significant R&D in C2 S2 deformable adhesives and polymer-modified mortars engineered for extreme thermal and substrate stress. Furthermore, digital procurement platforms are revolutionizing the B2B distribution of high-performance adhesives and sealants, increasing supply chain efficiency across regional construction hubs. The ongoing regulatory tightening under China’s green building codes is accelerating the introduction of eco-certified, water-resistant adhesives and façade sealants that meet global durability benchmarks for exterior cladding and insulation systems.

United States – Innovation and Sustainability Reinforce the Market for Premium Tile Adhesives and Sealants

The United States stone and tile adhesives market is evolving rapidly, fueled by strong housing demand, sustainability regulations, and a surge in home renovation spending. The U.S. residential remodeling trend, coupled with the increasing shift from hardwood to porcelain and natural stone flooring, is boosting the consumption of quick-set, polymer-modified, and high-bonding tile adhesives. The acquisition of DriTac’s flooring adhesives business by Sika AG has strengthened its North American market reach, aligning with the rising preference for interior finishing, wood-floor bonding, and large-tile installation applications.

Regulatory initiatives—especially in states like California and Washington—are pushing the industry toward low-VOC, water-based formulations that comply with Green Building Council and LEED standards. At the same time, product innovation is intensifying, with major U.S. chemical firms investing in C2 S1 and C2 S2 deformable adhesives for radiant heat flooring and high-traffic commercial spaces. The combination of robust construction spending, advanced building codes, and consumer demand for sustainable materials firmly positions the U.S. as a leading hub for next-generation tile adhesive technologies and performance sealants designed for moisture control and long-term adhesion.

Germany – Engineering Excellence and Regulatory Compliance Drive Advanced Tile Adhesive Solutions

Germany remains a benchmark for construction quality and adhesive technology in Europe, supported by the European Standard EN 12004 framework and the country's strict environmental policies. Leading chemical and construction brands, including Wacker Chemie AG and Omnicol, are pioneering polymer-enriched C2 and R2 adhesives for improved durability and adhesion strength. The launch of Omnicol’s S2 tile adhesive in 2024 marks a notable advancement—reducing curing time by 70% and enhancing flexibility for large-format tile installations on heated subfloors and cement screeds.

Germany’s construction ecosystem heavily prioritizes energy-efficient building materials, driving increased demand for thermal façade sealants, flexible cladding adhesives, and dispersion-based D2 adhesives for renovation work. Moreover, the Flexmortar certification system ensures that adhesives meet or exceed C2/S1 standards, guaranteeing superior freeze-thaw resistance and elasticity. The integration of low-VOC raw materials and solvent-free polymer modifiers continues to position Germany as a leader in eco-compliant, high-performance tile adhesives that cater to both renovation and high-rise applications in Europe’s green construction landscape.

India – Infrastructure Acceleration and Professional Tiling Standards Transform the Market

India’s stone and tile adhesive market is undergoing rapid modernization, shifting from traditional sand-cement mixtures toward polymer-modified and epoxy-based tiling solutions. The launch of Fosroc’s “Nitotile” range (2023) underscores The transition, offering high-performance adhesives and grouts designed for professional and large-scale applications. Domestic major Pidilite Industries, through its Roff brand, continues to strengthen its regional footprint—introducing Master Fix Adhesives and waterproof epoxy grouts suitable for high-humidity environments like kitchens, pools, and façades.

The adoption of vitrified tiles, imported marble, and granite in luxury residential and infrastructure projects has driven the use of C2-class polymer mortars and epoxy sealants, particularly in metro, airport, and commercial real estate developments. Government initiatives such as the Smart Cities Mission and regulatory emphasis on structural durability are pushing the market penetration of specialized adhesives from 25% to nearly 50% by 2030. As consumer awareness and installation standards rise, the Indian market is rapidly evolving into a major growth engine for certified, durable tile adhesive systems and chemical-resistant grouting technologies tailored to local climatic conditions.

Italy – Design Innovation and Industry Integration Define Advanced Tile Adhesive Development

Italy, the historic heart of the global ceramic tile industry, remains at the forefront of adhesive and grout innovation to match evolving design aesthetics and performance needs. Mapei S.p.A., the industry’s leading manufacturer, continues to drive advancements in polymer-modified mortars and epoxy-based grouts. Its Ultracolor Plus and Kerapoxy Easy Design systems, launched with improved pigment uniformity and workability, cater to precision tile installations demanding minimal grout lines and superior stain resistance.

The close collaboration between Italy’s ceramic tile manufacturers and adhesive producers fosters continuous innovation in deformable S1/S2 adhesives, essential for complex substrates and renovation projects involving tile-over-tile applications. R&D also focuses on stone-safe bonding systems that prevent discoloration or efflorescence on delicate materials such as Carrara marble. Furthermore, compliance with EN 12004 standards and growing export activity ensure Italy maintains its leadership in eco-friendly, highly deformable, and design-oriented adhesives for luxury interiors and architectural installations.

South Korea – High-Density Urban Construction and Technological Adoption Accelerate Market Expansion

South Korea’s stone and tile adhesives and sealants market is advancing rapidly, supported by urban infrastructure development, high-rise construction, and smart building integration. The government’s continuous investment in urban renewal projects has spurred demand for fast-setting (C2F) and rapid-curing adhesives that enable accelerated project completion without compromising performance. The country’s automated construction systems increasingly rely on hybrid polyurethane adhesives and high-modulus silicone sealants, engineered for seismic resilience and long-term façade bonding.

Domestic manufacturers are investing in low-VOC dispersion adhesives and flexible mortars to comply with stringent indoor air quality regulations. The use of lightweight cladding and advanced façade systems in new high-rise developments necessitates high-strength silicone and polyurethane sealants designed for Korea’s variable weather conditions. As sustainability and construction efficiency gain prominence, South Korea continues to evolve as a technologically advanced hub for high-performance tiling adhesives, grouts, and sealant systems optimized for next-generation urban architecture.

Stone & Tile Adhesives and Sealants Market Report Scope

Stone & Tile Adhesives and Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.7 Billion

|

|

Market Size (2034)

|

$28.5 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Chemistry (Cementitious, Polymer-Modified Cementitious, Dispersion, Reaction Resin, Specialized Sealants), By Application Type (Ceramic Tiles, Porcelain Tiles, Natural Stone, Mosaic & Glass Tiles, Façade & External Cladding), By End-User (Residential, Commercial, Institutional, Industrial), By Construction Type (New Construction, Repairs & Renovation), By Formulation (Powder, Liquid/Paste, Two-Component), By Technology (Water-Based, Solvent-Based, 100% Solid/Reactive), By Performance Classification (Normal, Improved, Additional Characteristics

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, Mapei S.p.A., Henkel AG & Co. KGaA, Arkema Group, Laticrete International, Inc., ARDEX Group, Saint-Gobain Weber, BASF SE, H.B. Fuller Company, Pidilite Industries Limited, Fosroc International Limited, The Dow Chemical Company, Wacker Chemie AG, 3M Company, Terraco Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Cementitious

- Polymer-Modified Cementitious

- Dispersion

- Reaction Resin

- Specialized Sealants

By Application Type

- Ceramic Tiles

- Porcelain Tiles

- Natural Stone

- Mosaic & Glass Tiles

- Façade & External Cladding

By End-Use Sector

- Residential

- Commercial

- Institutional

- Industrial

By Construction Type

- New Construction

- Repairs & Renovation

By Formulation/Form

- Powder

- Liquid/Paste

- Two-Component

By Technology

- Water-Based

- Solvent-Based

- 100% Solid/Reactive

By Performance Classification

- Normal

- Improved

- Additional Characteristics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Stone and Tile Adhesives and Sealants Market

- Sika AG

- Mapei S.p.A.

- Henkel AG & Co. KGaA

- Arkema Group

- Laticrete International, Inc.

- ARDEX Group

- Saint-Gobain Weber

- BASF SE

- H.B. Fuller Company

- Pidilite Industries Limited

- Fosroc International Limited

- The Dow Chemical Company

- Wacker Chemie AG

- 3M Company

- Terraco Group

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Stone and Tile Adhesives and Sealants Market, translating polymer-modified mortar and flexible sealant breakthroughs into clear competitive advantage for contractors, distributors, and specification teams. Our analysis reviews how rapid-curing thin-bed systems, large-format tile/slab installation needs, façade/weather-exposed assemblies, and low-VOC/CO₂-neutral solutions are reshaping jobsite productivity, durability, and compliance. It also highlights the impact of digital construction workflows, substrate preparation standards, and premium grout/sealant chemistries on lifecycle performance and risk mitigation—from commercial fit-outs to infrastructure modernization. Built for procurement leaders, estimators, and technical sales, this report is an essential resource to benchmark performance envelopes, de-risk material transitions, and align portfolios with evolving codes and green-building certifications without sacrificing speed or finish quality.

Scope Highlights

Segmentation:

- By Chemistry: Cementitious; Polymer-Modified Cementitious; Dispersion; Reaction Resin; Specialized Sealants

- By Application Type: Ceramic Tiles; Porcelain Tiles; Natural Stone; Mosaic & Glass Tiles; Façade & External Cladding

- By End-Use Sector: Residential; Commercial; Institutional; Industrial

- By Construction Type: New Construction; Repairs & Renovation

- By Formulation/Form: Powder; Liquid/Paste; Two-Component

- By Technology: Water-Based; Solvent-Based; 100% Solid/Reactive

- By Performance Classification: Normal; Improved; Additional Characteristics

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies, including Sika AG; Mapei S.p.A.; Henkel AG & Co. KGaA; Arkema Group; Laticrete International, Inc.; ARDEX Group; Saint-Gobain Weber; BASF SE; H.B. Fuller Company; Pidilite Industries Limited; Fosroc International Limited; The Dow Chemical Company; Wacker Chemie AG; 3M Company; Terraco Group.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.