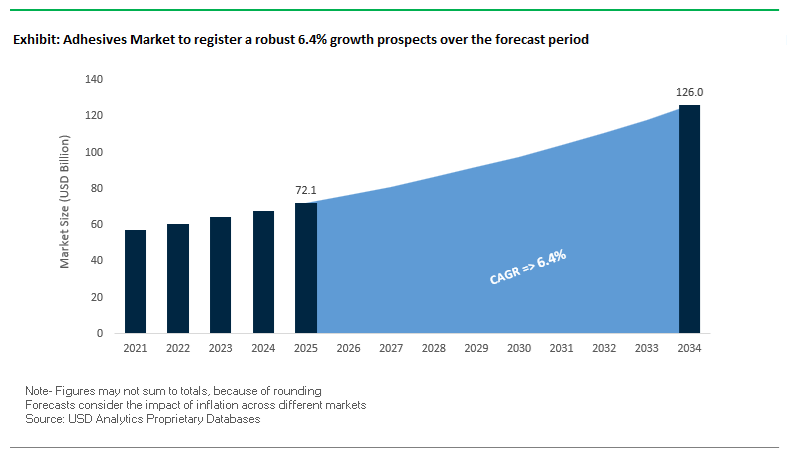

The global adhesives market is projected to grow from $72.1 billion in 2025 to $126 billion by 2034, registering a CAGR of 6.4% during the forecast period. Adhesives remain indispensable across packaging, automotive, construction, and electronics applications, driven by the accelerating shift toward lightweighting, e-mobility, and sustainable manufacturing systems., the current market structure reflects a steady pivot from solvent-based formulations to water-borne and hot-melt technologies, as environmental compliance and process efficiency become strategic imperatives.

The global adhesives market is shifting from commodity binders to engineered, low-emission chemistries and integrated bonding solutions as manufacturers scale water-borne, hot-melt and solvent-free technologies while simultaneously supporting high-value end markets such as e-mobility, advanced packaging, electronics and high-performance construction. Leading suppliers report parallel investments in ultra-thin, high-conductivity tapes and structural adhesives for EV battery assembly and thermal management (enabling tape replacements for mechanical fasteners), demonstrating how adhesive technology is migrating upstream into product design and system performance.

Sustainability and regulatory compliance determine product roadmaps: major manufacturers have publicly committed to PFAS elimination, to expand water-based and bio-balanced formulations, and to lower product embodied carbon through process and raw-material changes — moves that are reshaping formulation portfolios and buyer specifications. At the same time, manufacturers are commercializing low-VOC hot-melt and ECO2-branded adhesives for roofing and construction that reduce solvent use and lifecycle emissions.

Value is being captured not only by chemistry but by system solutions: equipment-integrated dispensing, precision metering, and Industry-4.0 enabled process control are standard selling points for adhesive manufacturers partnering with OEMs and contract assemblers to guarantee throughput, repeatability and quality in high-rate manufacturing lines (packaging, appliance, automotive gigafactories). Localized capacity builds and strategic acquisitions are tightening lead times for application-critical chemistries and enabling on-shore supply for regulated markets.

The adhesives industry is witnessing rapid transformation driven by sustainability, digitalization, and strategic consolidation. Leading players are launching green building adhesives, expanding capacity in Asia-Pacific, and pursuing M&A to strengthen construction and industrial adhesives portfolios. These developments signal a decisive move toward sustainability compliance, technological integration, and customer-oriented product innovation.

In October 2025, Henkel Adhesive Technologies announced an expanded suite of Environmental Product Declarations (EPDs) for its Ceresit construction adhesives, reinforcing its position in the green building adhesives segment and helping clients achieve LEED certification. Around the same time, Sika AG completed the acquisition of Marlon Tørmørtel A/S in Denmark, solidifying its position in the Nordic construction chemical market and enhancing its industrial sealants portfolio. In September 2025, H.B. Fuller reported a robust Q3 performance, with EBITDA margins rising by 110 basis points YoY to 19.1%, reflecting its pricing power and operational discipline across specialty adhesive segments. These actions underscore the industry’s emphasis on performance efficiency and profitability optimization.

Earlier in August 2025, Henkel AG & Co. KGaA reaffirmed its strong full-year guidance, citing momentum from e-mobility bonding and the low-carbon materials agenda, while Sika AG in July 2025 raised synergy targets for its MBCC acquisition integration, focusing on concrete admixtures and building finishing systems. During the same period, 3M Company launched 126 new adhesive products, reinforcing leadership in industrial adhesives and electronics bonding. Further, Sika’s June 2025 investment in Giatec marked a bold step toward digital construction transformation, while the March 2025 collaboration between Sika and BASF on epoxy hardeners showcased the growing momentum for joint sustainability innovation. Finally, in January 2025, Sika’s new adhesive production plants in Singapore and Xi’an, China, highlighted Asia-Pacific’s manufacturing acceleration, underscoring regional capacity buildup as a strategic growth driver.

The overarching direction of the adhesives industry in 2025–2035 identifies a balanced duality — a continued scale-up of production capacity in Asia-Pacific and a technology-led shift in Europe and North America toward eco-compliant, high-performance bonding systems. The cumulative impact of sustainability-focused R&D, vertical integration, and performance-driven acquisitions is likely to define the competitive dynamics of the global adhesives market through 2034.

A defining trend across the adhesives industry is the rapid migration from petrochemical-based feedstocks to bio-based and circular raw materials, catalyzed by global sustainability targets, regulatory tightening, and increasing consumer awareness. Adhesive manufacturers are prioritizing bio-circular chemistry, integrating renewable and recycled inputs while simultaneously addressing performance parity with synthetic formulations.

Between 2000 and 2022, the number of patents and published studies on bio-based adhesives for wood-based composite panels (WBCPs) grew nearly eightfold, from 60 to over 500 registered innovations, underscoring the industry’s expanding R&D footprint in renewable bonding technologies. The spike directly aligns with global formaldehyde-emission (FE) restrictions, which have accelerated the shift toward non-toxic, bio-derived adhesives for construction and furniture applications.

In the packaging sector, the EU Packaging and Packaging Waste Regulation (PPWR)—mandating full recyclability or reusability by 2030—is propelling demand for wash-off and recycling-compatible adhesives that allow PET and HDPE labels to detach at low temperatures (as low as 65°C). These innovations are essential to preserving high-value polymer streams during recycling, positioning adhesives as critical facilitators of the circular packaging economy.

On the corporate front, leading global manufacturers have pledged to redesign 100% of their packaging for recyclability by 2025 and to integrate over 30% post-consumer recycled content in all plastic packaging. These quantifiable sustainability goals are directly shaping adhesive formulation strategies—focusing on low-VOC, water-based, and bio-circular products that meet the evolving needs of green manufacturing and regulatory compliance.

Adhesive technology is evolving beyond traditional mechanical functions into the realm of smart materials, integrating responsiveness, conductivity, and reusability into bonded systems. The paradigm shift—spanning electronics, automotive, and industrial manufacturing—is creating an entirely new class of multi-functional adhesives that combine bonding with sensing, heat transfer, or controlled debonding features.

A notable example is the electrically released adhesive tape introduced by a leading smartphone manufacturer, capable of maintaining high-strength adhesion yet detaching cleanly when a low voltage (9–12V) is applied for approximately 60 seconds. The innovation directly supports the Right-to-Repair initiative, enabling easy battery removal, electronics recycling, and modular repairability—key principles of the circular electronics economy.

In the automotive industry, a global adhesives leader has demonstrated that thermal-activated debonding-on-demand systems can cut premium headlamp repair costs by up to 80% by allowing clean disassembly of sealed assemblies. The technological advancement not only promotes component reuse but also significantly reduces warranty and insurance expenses.

These next-generation smart adhesives—featuring thermal conductivity, reversibility, and even electrical sensing—are redefining performance expectations in sectors like EV battery bonding, semiconductor packaging, and flexible electronics. As global manufacturers integrate advanced functionalities into materials, adhesives are becoming key enablers of smarter, safer, and more sustainable product ecosystems.

The rapid industrialization of solid-state batteries (SSBs)—the next-generation power source for electric vehicles and energy storage—presents a high-value market opportunity for advanced adhesive technologies. Unlike conventional liquid-electrolyte batteries, SSBs rely on solid electrolytes that require precision bonding, stable interfacial contact, and effective heat management, making adhesives and interface materials integral to their mass production.

Thermal management is among the top engineering challenges in SSB design. Li-ion systems typically operate between 25°C and 40°C (298–313 K), with internal temperature deviations restricted to under 5 K for safety and performance. However, solid-state electrolytes exhibit lower thermal conductivity, intensifying the need for thermally conductive adhesives (TCAs) and thermal interface materials (TIMs) to maintain optimal temperature uniformity.

Equally critical is achieving a low-resistance solid-solid interface between brittle solid electrolytes and active electrodes. Researchers and engineers are developing thin adhesive buffer layers that function as both mechanical cushions and ionic bridges, mitigating stress, reducing lithium dendrite formation, and maintaining long-term electrochemical stability.

As the global energy transition accelerates, adhesives will play a pivotal role in solid-state gigafactory scale-up, enabling high-precision manufacturing while ensuring cell longevity, reliability, and safety. Manufacturers capable of developing heat-dissipative, chemically inert, and electrically compatible adhesives are strategically positioned to capture a major share of the expanding battery materials market.

The global automotive sector’s electrification drive is reshaping adhesive demand, with lightweighting emerging as a cornerstone of next-generation EV design. As automakers replace steel with aluminum, carbon fiber, and composite materials, structural adhesives are rapidly displacing welds and rivets to meet the performance and efficiency requirements of electric mobility.

Replacing mechanical fasteners in Body-in-White (BIW) assemblies with epoxy or polyurethane-based structural adhesives can cut vehicle weight by up to 25 kilograms per unit, translating into 3–7% CO₂ reduction and extended battery range. Beyond weight savings, structural adhesives provide superior load distribution, improving crash safety and stiffness by more than 30% compared to traditional welds or bolts.

Unlike conventional joining techniques, adhesive bonding allows for multi-material integration without introducing thermal distortion or galvanic corrosion—a critical benefit for combining aluminum and high-strength steels. These adhesives enhance fatigue performance, vibration damping, and long-term structural integrity, making them indispensable for EV chassis, body panels, and battery enclosure designs.

The growing emphasis on sustainable, high-efficiency automotive design ensures that the market for structural adhesives will expand significantly as global EV production scales. Manufacturers that can deliver lightweight, high-strength, corrosion-resistant adhesives tailored for automated robotic assembly will dominate the evolving high-value segment of the automotive supply chain.

Adhesives Market Share Insights, 2025-2034

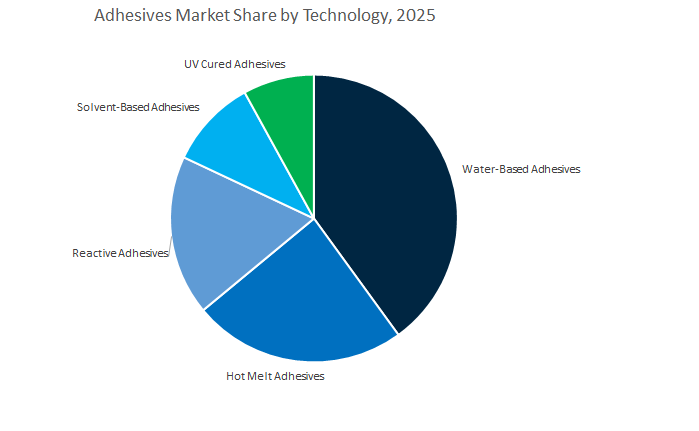

The water-based adhesives segment continues to dominate the global adhesives industry, commanding an estimated 40% market share in 2025. This dominance is anchored in its environmental sustainability, cost-effectiveness, and safety advantages compared to solvent-based systems. Water-based adhesives are widely utilized in packaging, construction, woodworking, and paper converting industries, where high-volume production and regulatory compliance are essential. Their low Volatile Organic Compound (VOC) emissions and non-flammable nature have positioned them as the go-to solution in markets governed by strict environmental standards such as EPA, REACH, and RoHS. Moreover, advancements in polyvinyl acetate (PVA), ethylene-vinyl acetate (EVA), and acrylic emulsion technologies have improved bonding strength and moisture resistance, expanding their applicability to both porous and semi-porous substrates. As industries increasingly prioritize green chemistry and worker safety, water-based adhesives have solidified their role as the sustainable workhorse of the adhesive landscape, balancing performance, processability, and environmental stewardship.

Hot melt adhesives and reactive adhesives are two of the most important growth-driving technologies in the global adhesives market, each serving distinct but complementary roles. Hot melt adhesives, accounting for around 24 percent of market share, are the fastest-growing segment due to their solvent-free formulations, instant setting speed, and compatibility with high-speed automated manufacturing, making them essential for packaging, hygiene products, woodworking, and automotive assembly, especially amid the rapid expansion of e-commerce and disposable hygiene products. In parallel, reactive adhesives represent the high-performance core of the industry, delivering exceptional strength, durability, and resistance to heat, vibration, and chemicals across automotive, aerospace, construction, electronics, and renewable energy applications. Systems such as epoxy, polyurethane, silicone, and UV-curable adhesives are increasingly critical for lightweight structures, EV battery assembly, and advanced electronics. Together, these segments highlight the industry’s shift toward faster processing, structural reliability, and next-generation manufacturing efficiency.

UV-cured adhesives, though the smallest segment by volume, play a vital role in high-precision and high-value manufacturing due to their instant curing, optical clarity, low outgassing, and solvent-free performance, making them indispensable in electronics, semiconductor packaging, display bonding, and advanced medical devices. Their adoption is rising alongside the growth of miniaturized electronics and wearable medical technologies that demand clean, accurate, and automated bonding processes. In contrast, solvent-based adhesives represent a declining segment as industries shift toward water-based, hot melt, and hybrid alternatives driven by VOC regulations and safety standards. Despite this, solvent-based systems remain relevant in niche applications such as footwear, flexible laminates, and select automotive uses where high initial tack, fast drying, and strong adhesion to low-surface-energy substrates are required.

The packaging industry dominates the global adhesives market, accounting for roughly 35% of total market share in 2025. This leadership is driven by the explosive growth of e-commerce, consumer goods, and flexible packaging sectors. Adhesives are indispensable in carton sealing, labeling, lamination, and flexible pouch fabrication, where speed, reliability, and sustainability are critical. Water-based and hot melt adhesives lead this space due to their low toxicity, recyclability, and high-speed performance. As global demand for sustainable and biodegradable packaging materials intensifies, adhesive manufacturers are developing bio-based, compostable, and repulpable solutions that align with circular economy goals. The sector’s rapid digitalization and automation—particularly in smart and tamper-evident packaging—are also redefining adhesive functionalities. Given its scale and continuous innovation, packaging remains the largest and most dynamic application segment, underpinning the adhesive industry’s global growth trajectory.

The building and construction segment, holding about 28% of market share, stands as the second-largest and most structurally vital segment. Adhesives play a central role in flooring, paneling, tile setting, insulation bonding, and waterproofing, replacing traditional fasteners and enabling modern architectural flexibility. The increasing adoption of green building standards (LEED, BREEAM), coupled with the demand for energy-efficient and durable materials, drives steady growth in this segment. Polyurethane, silicone, and hybrid adhesives dominate, providing elasticity, weather resistance, and structural stability. The rise of prefabricated and modular construction is further amplifying demand for fast-curing, high-strength bonding systems. Moreover, ongoing urbanization in Asia-Pacific and the Middle East continues to fuel large-scale infrastructure projects. As sustainability and structural performance converge, the construction segment remains a foundational pillar for long-term adhesive market expansion.

The automotive and transportation segment represents one of the most innovation-intensive areas of adhesive demand, driven by the shift toward lightweight, electric, and sustainable mobility solutions. Adhesives are fundamental to replacing welding and mechanical fasteners, offering reduced vehicle weight, improved fuel efficiency, and enhanced safety. Key applications include body panel bonding, trim attachment, battery assembly, and NVH (noise, vibration, and harshness) control. The growing production of electric vehicles (EVs) has sparked demand for thermal conductive, flame-retardant, and structural adhesives to ensure battery integrity and temperature management. Advanced reactive and hot melt formulations dominate, offering high strength and environmental resilience. As automakers prioritize multi-material design, corrosion protection, and assembly automation, adhesives are evolving into critical enablers of automotive design and performance innovation.

The electronics and electrical segment holds a high-value yet specialized position within the global adhesives market. Adhesives are indispensable for semiconductor encapsulation, display assembly, heat dissipation, and circuit protection, enabling the miniaturization and durability of modern electronics. UV-cured and reactive adhesives dominate this segment due to their precision, purity, and controlled curing behavior. The surge in 5G infrastructure, wearable technology, and EV battery electronics has propelled the adoption of adhesives with enhanced thermal conductivity, dielectric strength, and transparency. This segment’s value lies in its technological sophistication, where even small-volume adhesives deliver significant functional impact. As electronics continue to converge with automotive and healthcare technologies, this segment remains a hotbed of innovation and high-margin growth.

The global adhesives competitive landscape is dominated by a blend of innovation-driven global giants and regional specialists focused on sustainability, performance, and manufacturing scale. Leading companies such as Henkel, Sika, H.B. Fuller, 3M, and Bostik (Arkema Group) continue to reshape the market through sustainability programs, advanced R&D investments, and capacity expansion across high-demand regions like Asia-Pacific and Europe.

Henkel remains the undisputed global leader in adhesives, sealants, and functional coatings, operating through its flagship Loctite brand. The company’s 2030+ Sustainability Ambition emphasizes decarbonizing raw materials and operations to achieve net-zero emissions. Its innovation focus includes thermal management adhesives and battery assembly bonding for electric vehicles. Henkel’s functional coatings and MRO solutions further strengthen its leadership across industrial, consumer, and DIY segments, positioning it as a sustainability-first enterprise in the adhesive technologies market.

Sika continues to enhance its dominance through construction chemical innovations and strategic acquisitions like MBCC and Marlon Tørmørtel A/S, which have fortified its infrastructure solutions and building finishing systems. The company’s technological leadership extends to structural bonding, sealants, and damping solutions, powering over 1,000 data centers worldwide with Sika technology. Its 2025 capacity expansion in Singapore and China underscores its commitment to scaling Asia-Pacific manufacturing operations and meeting rising global construction demand.

As the world’s largest pure-play adhesives provider, H.B. Fuller continues to excel in specialty adhesive solutions with a focus on Durable Assembly and Engineering Adhesives. The company achieved an 19.1% EBITDA margin in Q3 2025, reflecting disciplined execution. With an expected $140 million capital investment in process improvements and innovation, H.B. Fuller is enhancing its footprint in high-margin segments while advancing its Fuller Impact philanthropic initiative to nurture future STEM talent for the adhesives industry.

3M’s R&D investment of $3.5 billion (2025–2027) demonstrates its commitment to technological leadership. Its Industrial Adhesives, Tapes, and Films division continues to deliver robust growth in electronics bonding and pressure-sensitive adhesives (PSA). With 126 new products launched in the first half of 2025, 3M outpaced its annual innovation target. The company’s plan to eliminate PFAS from all operations by 2026 highlights its proactive sustainability stance, making it a frontrunner in eco-compliant adhesive formulations.

As part of the Arkema Group, Bostik leverages backward integration into specialty materials and advanced polymers, enabling a secure supply chain for bio-based adhesives. Its Born2Bond™ portfolio specializes in precision bonding applications such as electronics assembly and EV battery manufacturing. Bostik’s innovation focus extends to thermally and electrically conductive adhesives catering to ADAS and new mobility platforms, reinforcing its position as a precision engineering adhesives pioneer within the specialty materials market.

China continues to dominate the Asia-Pacific adhesives market, supported by massive industrial investments, strong domestic demand, and a rapid shift toward localized high-performance adhesive production. With Henkel’s €60 million investment in the Adhesive Technologies Application Engineering Centre and Inspiration Center in Shanghai (2025), China is becoming a global R&D hub for smart bonding solutions. Similarly, the establishment of the South China Application Engineering Centre (SCAEC) in Dongguan demonstrates China’s rising technological maturity in future-oriented bonding applications for electronics, mobility, and packaging industries.

Strategic acquisitions are also shaping the country’s adhesive ecosystem. Henkel’s 2025 acquisition of Suzhou Boke Biotechnology has expanded its footprint in the personal care and hygiene adhesives segment, a fast-growing end-use category. Meanwhile, the strong momentum in epoxy and fast-curing adhesives is driven by China’s leadership in automotive production, electric vehicles (EVs), and industrial fabrication. Ongoing infrastructure megaprojects, from high-speed rail to residential complexes, continue to boost construction sealant consumption, reinforcing China’s dual strength as both a manufacturing hub and innovation center in the global adhesives industry.

The United States adhesives and sealants industry is undergoing a technology-driven transformation, powered by federal infrastructure spending, environmental regulation, and advanced manufacturing innovation. Construction activity remains robust — the U.S. Census Bureau reported a $2.19 trillion construction spending rate in January 2025, ensuring sustained demand for structural adhesives, waterproofing sealants, and hybrid polymer bonding systems across commercial and residential segments.

Regulatory reform continues to be a major driver. The EPA’s low-VOC standards are reshaping adhesive formulations, pushing companies toward water-based, solvent-free, and bio-based chemistries. To mitigate global supply risks, manufacturers are near-shoring the production of acrylic monomers and resin intermediates, improving supply security post-2025 tariffs. Product innovation remains vigorous — Engineered Polymer Solutions’ launch of EPS® 2133 (2023), an acrylic resin for pressure-sensitive adhesives (PSAs), exemplifies domestic innovation in packaging and industrial applications. Overall, the U.S. market continues to lead in sustainability-focused R&D and high-value adhesive technologies for sectors like aerospace, construction, and packaging.

Germany anchors the European adhesives and sealants industry, combining engineering excellence with environmental compliance under the EU’s tightening sustainability mandates. The country’s adhesive manufacturers are at the forefront of advanced material compatibility and medical-grade bonding innovation. Henkel’s 2025 launch of Loctite AA 3952 and Loctite SI 5057 — light-cure adhesives optimized for flexible medical devices and thermoplastic elastomers (TPEs) — exemplifies the integration of precision engineering with health technology.

The German automotive sector continues to advance lightweighting and structural bonding with epoxy and polyurethane-based adhesives, critical for improving EV range and crash resistance. Meanwhile, the nation’s strong R&D infrastructure is fueling industrial assembly innovation, with companies expanding hot melt and reactive adhesive production lines to enhance speed and automation. Germany’s focus on fast-curing epoxy adhesives and sustainable polymer systems ensures its continued position as the innovation and regulatory benchmark for Europe’s specialty adhesives market.

India’s adhesives industry is rapidly expanding on the back of urbanization, infrastructure megaprojects, and growing domestic manufacturing capacity. The market is seeing exponential demand in construction adhesives and sealants, driven by large-scale projects such as 12 new smart industrial cities approved by the Indian government (₹28,602 crore, December 2024). Supporting The expansion, Pidilite Industries opened a 11,000 m² tile adhesive plant in Luck(April 2024), bolstering regional access for its Roff brand in North India.

The market’s diversification is also gaining pace. Hindware Limited’s entry into tile adhesives (2023) underscores the growing competition and need for end-to-end tiling solutions in both urban and commercial construction. Rising adoption of polyurethane sealants in affordable housing projects under Pradhan Mantri Awas Yojana highlights India’s growing shift toward energy-efficient, moisture-resistant bonding systems. With its expanding industrial base, government-backed infrastructure programs, and evolving consumer preferences, India is emerging as one of the fastest-growing construction adhesives markets globally.

Japan’s adhesives industry continues to set global standards for precision manufacturing and materials innovation. The country’s electronics sector — a global hub for smartphones, semiconductors, and miniaturized devices — drives strong demand for UV-curable and high-precision adhesives designed for intricate assembly processes. As manufacturers focus on smaller, more efficient designs, UV-curable and fast-setting formulations are becoming indispensable for precision bonding.

Meanwhile, Japan’s automotive industry is driving innovation in EV battery adhesives, focusing on thermal management, flame retardancy, and vibration damping. Domestic adhesive producers are developing customized formulations for high-strength bonding and thermal dissipation, critical for the country’s EV expansion. With advanced R&D facilities, strict performance standards, and a focus on sustainable chemistry, Japan remains a technological pioneer in electronics-grade and automotive adhesives globally.

The United Kingdom adhesives and sealants market is increasingly shaped by green building standards, energy efficiency regulations, and medical device manufacturing advancements. The Future Homes Standard (FHS) and updates to Building Regulations Part L are driving a surge in low-VOC construction sealants and insulation adhesives, helping the country meet its carbon reduction commitments. Public sector projects are adopting sustainable adhesive solutions aligned with EU compliance frameworks even post-Brexit.

On the industrial front, Intertronics’ launch of the IUV101 Medical Kit (2023) demonstrates the UK’s innovation in LED UV-curable adhesive technology, offering high precision for medical device assembly. The growing intersection of construction sustainability and healthcare innovation is positioning the UK as a high-value market for energy-efficient and specialty adhesive technologies.

France plays a pivotal role in the global adhesives landscape, driven by Arkema’s Bostik division, which continues to pioneer smart, adaptive, and bio-based adhesives. The next-generation materials are engineered to self-heal, adapt to stress, and enhance performance under variable conditions, addressing demands in construction and automotive sectors. France’s leadership aligns with European Green Deal goals, emphasizing low-emission and solvent-free adhesives across industrial and consumer applications.

With major production hubs in France, Bostik is accelerating innovation in high-performance, sustainable bonding solutions that support both industrial manufacturing and building modernization. The country’s emphasis on sustainability, circular chemistry, and advanced materials science ensures France remains at the forefront of the European smart adhesives and green materials revolution.

Switzerland serves as a global innovation base for Sika AG, one of the world’s leading producers of construction adhesives and sealants. Sika’s ongoing advancements in hot melt adhesive technologies are revolutionizing construction assembly and structural bonding, offering rapid curing, high weather resistance, and superior adhesion performance. The innovations are crucial for modern façade systems, high-rise construction, and infrastructure repair applications.

Additionally, Switzerland’s strength in automotive and industrial adhesives is reflected in Sika’s commitment to interior assembly bonding, including dashboards, panels, and trims, where performance and longevity are critical. With its deep focus on durability, material versatility, and sustainability, Switzerland remains the epicenter of innovation for advanced industrial and construction adhesives on the global stage.

Adhesives Market Report Scope

Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$72.1 Billion

|

|

Market Size (2034)

|

$126 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Resin Type (Acrylic Adhesives, Polyurethane Adhesives, Epoxy Adhesives, Cyanoacrylate Adhesives, VAE/EVA Adhesives, Silicone Adhesives & Sealants, Other Resins), By Technology (Water-Based Adhesives, Hot Melt Adhesives, Reactive Adhesives, Solvent-Based Adhesives, UV Cured Adhesives), By End-Use Industry (Packaging, Building & Construction, Automotive & Transportation, Woodworking & Joinery, Consumer/DIY, Aerospace & Defense, Healthcare & Medical, Footwear & Leather, Electronics & Electrical

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema Group (Bostik), Dow Inc., BASF SE, Huntsman Corporation, Avery Dennison Corporation, Wacker Chemie AG, Pidilite Industries Ltd., Mapei S.p.A., Ashland Global Holdings Inc., DuPont de Nemours, Inc., Kuraray Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Acrylic Adhesives

- Polyurethane Adhesives

- Epoxy Adhesives

- Cyanoacrylate Adhesives

- VAE/EVA Adhesives

- Silicone Adhesives & Sealants

- Other Resins

By Technology

- Water-Based Adhesives

- Hot Melt Adhesives

- Reactive Adhesives

- Solvent-Based Adhesives

- UV Cured Adhesives

By End-Use Industry

- Packaging

- Building & Construction

- Automotive & Transportation

- Woodworking & Joinery

- Consumer/DIY

- Aerospace & Defense

- Healthcare & Medical

- Footwear & Leather

- Electronics & Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Arkema Group (Bostik)

- Dow Inc.

- BASF SE

- Huntsman Corporation

- Avery Dennison Corporation

- Wacker Chemie AG

- Pidilite Industries Ltd.

- Mapei S.p.A.

- Ashland Global Holdings Inc.

- DuPont de Nemours, Inc.

- Kuraray Co., Ltd.

*- List not Exhaustive

Research Coverage

Developed by USDAnalytics, this report investigates how sustainability mandates, e-mobility, and automation are reshaping the global adhesives market, quantifying value pools from $72.1B (2025) to $118.4B (2034) at a 6.4% CAGR. Our analysis reviews the migration from solvent-based to water-borne and hot-melt platforms, benchmarks bio-based and reactive breakthroughs, and highlights supply shifts, regional competitiveness, and procurement risk. With price–mix diagnostics, specification roadmaps, and scenario stress tests to 2034, this report is an essential resource for executives, engineers, and sourcing leaders seeking lower VOCs, higher throughput, and durable performance without cost overruns.

Scope Includes

- By Resin Type: Acrylic; Polyurethane; Epoxy; Cyanoacrylate; VAE/EVA; Silicone Adhesives & Sealants; Other Resins.

- By Technology: Water-Based; Hot Melt; Reactive; Solvent-Based; UV-Cured.

- By End-Use Industry: Packaging; Building & Construction; Automotive & Transportation; Woodworking & Joinery; Consumer/DIY; Aerospace & Defense; Healthcare & Medical; Footwear & Leather; Electronics & Electrical.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic 2021–2024; Forecast 2025–2034.

- Companies: 15+ company analyses/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.