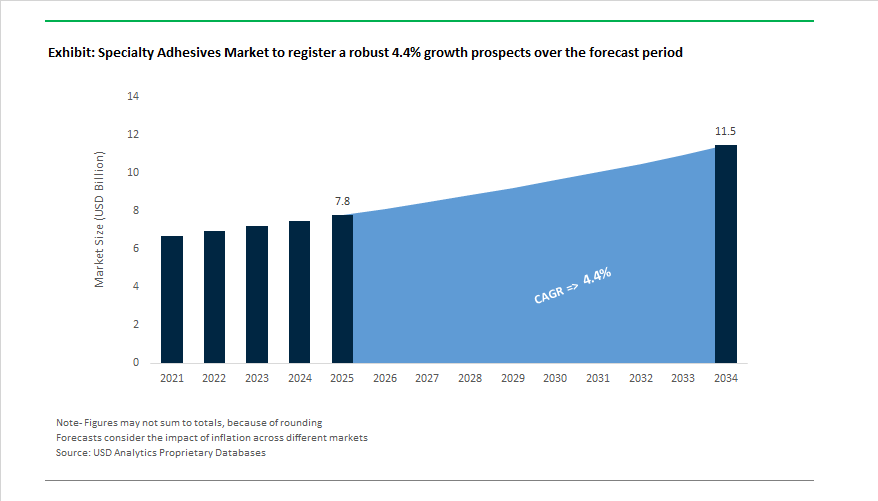

The Global Specialty Adhesives Market is projected to grow from $7.8 billion in 2025 to $11.5 billion by 2034, registering a CAGR of 4.4%. The market is driven by the rising complexity of industrial assemblies, the shift toward lightweighting and sustainable bonding, and rapid technological advances in bio-based and thermally conductive adhesive systems.

The specialty adhesives industry continues to evolve rapidly through strategic mergers, sustainable product launches, and regional expansions targeting high-margin verticals such as medical devices, advanced manufacturing, and renewable energy systems.

In October 2025, H.B. Fuller announced the appointment of a new MedTech board member, reinforcing its strategy to deepen innovation in medical-grade adhesive systems and bio-compatible technologies. The company’s focus reflects a larger trend of specialty adhesive providers targeting high-margin healthcare and life science applications, where performance and regulatory compliance dictate market success.

Avery Dennison Corporation made a significant move in August 2025 by acquiring the flooring adhesives business of Meridian Adhesives Group, expanding its reach in construction and specialty flooring applications. This acquisition underscores an ongoing wave of industry consolidation, with global players strengthening vertical integration across diverse adhesive categories—from automotive interiors to sustainable packaging laminations.

In July 2025, a leading adhesives producer launched a new range of thermally conductive polyurethane adhesives engineered for large-format display gasketing and consumer electronics. These adhesives combine superior heat dissipation with high-speed automation compatibility, meeting the miniaturization and heat management demands of next-generation electronics.

Simultaneously, APPLIED Adhesives expanded through its acquisition of BTmix (July 2025), enhancing its distribution capabilities and custom formulation network across North America. This signals a broader market shift toward regionally tailored, high-specification adhesive solutions as global manufacturers demand localized service and faster supply chain responsiveness.

H.B. Fuller also advanced sustainability goals in June 2025 with its Millennium PG-1 EF ECO2 roofing adhesive, a breakthrough formulation utilizing ECO2 Driven™ technology to replace high-GWP blowing agents with atmospheric gases—an innovation marking a new standard for low-emission construction adhesives.

Earlier, in April 2025, Dow’s waterborne barrier coating RHOBARR™ 135 earned recognitions for its repulpable and recyclable performance, offering a practical solution to plastic-free packaging adhesives. The product exemplifies Dow’s shift toward renewable chemistry and circular materials, a trend mirrored across major adhesive producers.

Geographically, the industry is experiencing robust growth in Asia-Pacific. A European specialty chemical group inaugurated a new automated adhesives plant in Southeast Asia (March 2025) to serve the electronics, hygiene, and packaging sectors, reinforcing Asia’s position as the world’s fastest-growing production hub for specialty adhesives.

Additionally, February 2025 marked a pivotal policy change with the European Union’s tightened F-gas and solvent regulations, prompting an industry-wide shift toward low-VOC and solvent-free systems. This regulatory push is accelerating investment in green chemistries, digital process controls, and sustainable raw material sourcing across the adhesive value chain.

Market Trend 1: Proliferation of Electrically and Thermally Conductive Adhesives for Advanced Electronics Packaging

The accelerating adoption of electric vehicles (EVs), 5G infrastructure, and power electronics is driving demand for specialty adhesives engineered for simultaneous thermal management, electrical conductivity, and mechanical integrity. Unlike traditional structural bonding materials, these formulations must ensure high dielectric protection and heat dissipation across miniaturized, high-power electronic systems.

WACKER Chemie AG’s 2025 showcase at The Battery Show North America exemplified the transition, introducing next-generation Thermally Conductive Adhesives (TCA) optimized for cell-to-pack (CTP) and cell-to-chassis (CTC) EV battery designs. These adhesives function as both structural and heat-transfer materials, ensuring temperature uniformity across densely packed battery arrays while enhancing mechanical rigidity.

Similarly, Dow Inc.’s DOWSIL™ EC-6601 Electrically Conductive Adhesive addresses the rising need for electromagnetic shielding in automotive radar, cameras, and 5G base stations, offering exceptional conductivity and mechanical resilience in high-frequency environments. Its success drives the growing intersection between adhesive science and electronics packaging innovation.

Complementing these advancements, WEVO-CHEMIE GmbH’s 2K silicone adhesive WEVOSIL 28015 FL—with a thermal conductivity of 1.5 W/m⋅K and initial adhesion above 2 MPa within minutes—represents a major leap for automated EV battery module assembly. Rapid curing via infrared or laser activation streamlines production, demonstrating how high-speed, thermally conductive adhesives are redefining throughput in next-generation electronics manufacturing.

Market Trend 2: Adoption of Dynamic and Reversible Bonding Technologies for Repair, Recycling, and Disassembly

The shift toward circular manufacturing and Extended Producer Responsibility (EPR) is catalyzing the rise of dynamic and reversible adhesive technologies that enable easy disassembly, repair, and recycling. These advanced bonding systems—activated by temperature, light, or specific chemical triggers—are pivotal to achieving design-for-disassembly (DfD) in industries like electronics, textiles, and consumer goods.

A 2025 Global Environment Facility (GEF) and United Nations Development Programme (UNDP) initiative in India, valued at US$120 million, emphasizes eco-design and circular business models for the electronics sector, explicitly promoting reversible adhesive adoption to recover valuable materials.

Academic studies confirm that reversible adhesives in smartphones could significantly extend product lifespans by allowing safe component replacement and modular upgrades, minimizing e-waste and enabling resource recovery.

In the fashion industry, CreateMe Technologies, in collaboration with The University of Warwick, has patented 19 innovations in thermoreversible adhesive technology that allow bonded garments to disassemble under controlled heat conditions, facilitating textile recycling and reuse at scale. These breakthroughs demonstrate that dynamic adhesive formulations are redefining sustainability, bridging the gap between industrial recycling efficiency and consumer product circularity.

Market Opportunity 1: Development of Bio-Integrated Adhesives for Next-Generation Wearable Medical Devices

The convergence of biotechnology and materials science is fueling demand for bio-integrated adhesives capable of maintaining adhesion under dynamic skin conditions while being biocompatible, breathable, and reusable. These specialty adhesives form the interface between wearable medical sensors and the human body, enabling continuous, high-fidelity physiological monitoring for chronic care and fitness applications.

Recent research introduced a self-adhesive, biocompatible organohydrogel fabricated through DLP 3D printing, engineered for flexible biosensors. The material maintains structural integrity and adhesion during prolonged skin exposure, achieving sustained wear comfort and signal accuracy.

Leading companies like Avery Dennison Medical are advancing skin-friendly silicone-based pressure-sensitive adhesives (PSAs) and perforated gel matrices for repositionable medical patches, ensuring secure yet non-irritating adhesion even after repeated use. The aligns with healthcare’s pivot toward long-term, remote monitoring solutions.

Supporting the innovation, a biomaterials review highlighted hydrogels’ superior conformability and moisture retention, making them ideal for adhesives in wearable health monitoring systems. Their capacity to conform to skin topography ensures minimal signal distortion and irritation, a crucial parameter for reliable biosignal capture.

Market Opportunity 2: Engineering of High-Strength, Rapid-Curing Adhesives for Sustainable Mass Timber Construction

As the construction industry transitions toward mass timber architecture, demand is surging for high-strength, moisture-tolerant, and rapid-curing adhesives that support sustainable, large-scale wooden structures such as Cross-Laminated Timber (CLT) and Timber-Concrete-Composites (TCC). Specialty adhesives play a pivotal role in enabling high-load, eco-friendly structural assemblies that replace traditional steel and concrete.

Research on adhesive-bonded TCC systems found that epoxy-based polymer concrete exhibited a shear strength of 16.7 ± 3.0 MPa when bonded to beech wood—over five times stronger than polyurethane-based alternatives (3.2 ± 1.7 MPa). The data drives the importance of chemically tailored specialty adhesives for achieving superior load-bearing capacity in hybrid timber structures.

In Europe, one-component polyurethane adhesives (1K PUR) dominate CLT manufacturing, prized for rapid setting, high green strength, and eco-friendly composition compatible with automated production systems. These formulations allow fast assembly cycles, crucial for large-scale timber building projects targeting LEED and BREEAM certifications.

Further advancing the segment, research into inductive heating with Curie particles in epoxy adhesives has demonstrated mechanical strengths of 6–10 MPa in small-scale lap shear tests while enabling rapid curing through localized heating. The innovation represents a breakthrough for on-site bonding, potentially cutting assembly times drastically in modular and prefabricated timber construction.

Specialty Adhesives Market Share Insights, 2025-2034

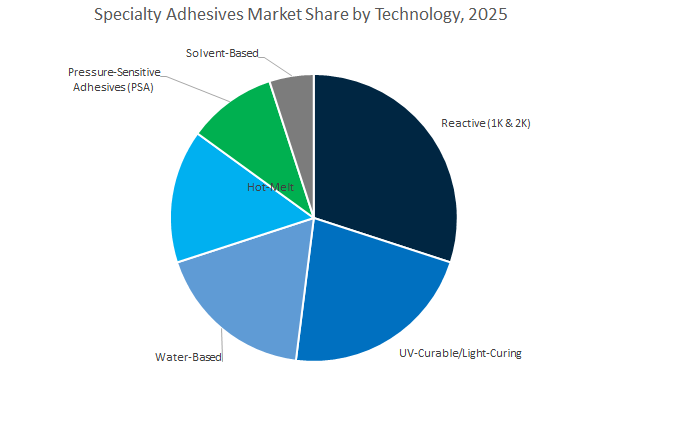

Market Share by Technology

Reactive adhesives (1K & 2K systems) lead the global specialty adhesives industry, capturing an estimated 27.4% share by 2025, owing to their unparalleled performance in structural and high-stress bonding applications. These formulations, based on epoxy, polyurethane, silicone, and acrylic chemistries, deliver exceptional mechanical strength, chemical resistance, and long-term stability, making them indispensable in aerospace, automotive, and construction sectors. The dominance of reactive systems is reinforced by their adaptability to demanding environments—where exposure to heat, moisture, and vibration can challenge conventional adhesive types. Their ability to form durable, thermoset bonds has made them the go-to choice for composite materials, EV battery module assembly, and advanced infrastructure components. The segment’s continued expansion is further fueled by the shift toward lightweight, hybrid material assemblies, where mechanical fasteners are being replaced with advanced adhesive technologies for weight reduction and improved aesthetics.

Meanwhile, UV-curable and light-curing adhesives represent the fastest-growing technology segment, driven by the electronics, optics, and medical device industries, which prioritize precision, rapid curing, and solvent-free processes. These adhesives enable instant bonding under controlled light exposure, making them ideal for automated assembly lines and high-throughput production. Water-based and hot-melt adhesives continue to gain traction across packaging, labeling, and furniture manufacturing, aligning with global sustainability goals by offering low-VOC and solvent-free formulations. These systems provide a critical balance between environmental compliance and efficient processing. Conversely, solvent-based adhesives occupy niche roles in aerospace and high-performance industrial settings, where their high initial tack and extreme environmental resistance still offer competitive advantages.

Market Share by End-Use Industry

Electronics leads the global specialty adhesives market, accounting for approximately 24.3% of the total share by 2025, driven by increasing complexity and miniaturization in modern electronic assemblies. Specialty adhesives play a vital role in smartphones, semiconductors, wearable devices, and flexible electronics, where precise bonding, thermal stability, and dielectric performance are essential. In particular, conductive and thermally dissipative adhesive systems are integral to next-generation applications like 5G infrastructure, EV power modules, and advanced sensors, enabling high reliability and long-term performance in confined environments. The continuous evolution of surface-mount technology (SMT) and microelectronic packaging ensures steady growth for high-purity, low-outgassing adhesive formulations designed for stringent electronic standards.

The automotive and transportation industry represents one of the fastest-growing end-use sectors, fueled by the electrification of vehicles, increased use of lightweight composites, and the adoption of adhesive bonding for structural integrity and noise reduction. Specialty adhesives are used extensively for battery module sealing, windshield bonding, and vibration damping, replacing traditional welding and riveting processes. Similarly, the medical and healthcare sector continues to expand its share, utilizing biocompatible and sterilization-resistant adhesives in wearable sensors, surgical instruments, and implantable devices. The aerospace and defense segment, though smaller in volume, remains a premium market, demanding adhesives that can withstand extreme temperatures, pressure differentials, and chemical exposure—particularly in composite fabrication, fuel tank sealing, and avionics assembly.

In the building & construction sector, specialty adhesives support high-performance applications such as curtain wall assembly, glass bonding, and structural reinforcement, driven by architectural trends emphasizing energy efficiency and durability. Industrial assembly applications leverage these adhesives for precision bonding in machinery, appliances, and renewable energy equipment where vibration resistance and fatigue performance are crucial. Meanwhile, traditional industries such as packaging, woodworking, and consumer/DIY retain smaller shares but remain steady contributors due to cost-effective specialty formulations offering enhanced adhesion and versatility.

The Global Specialty Adhesives Market is characterized by intense innovation, vertical integration, and sustainability-driven transformation. The top players—Henkel, H.B. Fuller, Sika, Arkema (Bostik), and Dow—are leveraging their R&D strength and global production scale to capture opportunities in emerging sectors such as EV manufacturing, aerospace composites, flexible packaging, and renewable construction.

Henkel’s Adhesive Technologies division remains a benchmark for structural bonding and UV-curing adhesive solutions across automotive, electronics, and packaging industries. Its strategic initiatives center around digital engineering tools, predictive maintenance, and robotic application systems that enable scalable industrial integration. In Q4 2024, Henkel introduced new thermal gap fillers and potting compounds optimized for EV battery thermal management, improving heat dissipation and extending component life. Its end-to-end service model, encompassing design-in support and automated dispensing systems, solidifies Henkel’s position as a full-spectrum adhesive solution provider.

H.B. Fuller stands as the largest pure-play adhesives manufacturer globally, with a diversified portfolio across medical, hygiene, packaging, and durable assembly. The company continues its transformation toward 20%+ EBITDA margins, emphasizing sustainable innovation. In Q2 2025, it advanced the Swift®melt 1850, a bio-based hot-melt adhesive designed for recyclable packaging. Additionally, the launch of its Millennium PG-1 EF ECO2 roofing adhesive showcased Fuller’s sustainability-first approach. The opening of a new plant in Cairo (Q4 2024) strengthens its distribution and manufacturing footprint in Africa and the Middle East, improving regional market responsiveness.

Sika AG continues to lead through its Strategy 2028, prioritizing growth via innovation and acquisitions in automotive and construction adhesives. Its product line includes high-performance polyurethane and epoxy-based bonding systems used in structural glazing and vehicle lightweighting. The company’s acquisition of a Qatar-based additives factory (Q1 2025) enhances its manufacturing resilience and supply stability in the Middle East. Sika reported a material margin increase to 54.5% in FY 2024, driven by an expanded share of high-value specialty adhesive systems.

Through its Bostik division, Arkema is focusing on sustainable packaging, hygiene, and transportation adhesives. Bostik’s “smart adhesives” initiative integrates features such as elastic bonding, heat resistance, and recyclability, positioning it at the forefront of eco-efficient bonding technology. With 2.7% of sales dedicated to R&D, its global centers in France, China, and the U.S. drive innovations in solvent-free PSA hot-melts and polymer-modified construction binders. Arkema’s elastic bonding technology ensures superior durability and flexibility under impact and temperature variation—crucial for EVs and structural transport applications.

Dow leverages its deep materials science expertise to develop sustainable, high-performance silicone, polyurethane, and acrylic adhesives under its DOWSIL™ brand. Its 2024 portfolio includes the RHOBARR™ 135 waterborne coating, recognized for advancing recyclable food packaging solutions. Dow’s adhesive technologies play a key role in electronics, aerospace, and defense, offering superior heat resistance, elasticity, and long-term bonding stability. Its focus on circular chemistry, repulpable coatings, and silicone-based structural adhesives underscores its leadership in sustainability-driven specialty materials innovation.

Country Analysis: Regional Drivers Powering Growth in the Global Specialty Adhesives Industry

United States (U.S.): Advancing Specialty Adhesives through Innovation, Defense Contracts, and High-Tech Manufacturing

The United States specialty adhesives market remains at the forefront of technological advancement and innovation, driven by its strong industrial base, defense-backed R&D investments, and growing demand from EV and aerospace manufacturing. In 2024, H.B. Fuller Company launched a new series of low-outgassing structural epoxy adhesives designed for advanced driver-assistance systems (ADAS) and electric vehicle (EV) battery pack assembly, addressing critical needs in thermal management and durability for next-generation vehicles. Similarly, 3M Company announced a 2025 capacity expansion at its Midwest adhesives and tapes facility, supporting high-volume medical device assembly and aerospace composite bonding applications—two segments showing robust post-pandemic recovery.

Government-driven innovation also plays a central role. The U.S. Department of Defense (DoD) awarded multi-million-dollar contracts in late 2024 to several American material science companies for the development of high-temperature polyimide adhesives tailored for hypersonic flight systems, marking a leap in defense-grade bonding materials. In parallel, the rise of UV-curable acrylic adhesives for flexible display bonding and advanced microelectronic encapsulation continues to gain momentum, supported by tech sector R&D. With growing regulatory emphasis on sustainability and low-VOC compliance, U.S. adhesive manufacturers are rapidly transitioning toward eco-friendly, solvent-free chemistries, cementing the country’s position as a global hub for high-performance specialty adhesives innovation.

Germany: Sustainability-Driven Adhesive Leadership and Advanced Automotive Integration

Germany’s specialty adhesives industry continues to thrive under the combined influence of stringent EU environmental policies, automotive electrification, and strong industrial R&D investment. In 2024, Henkel AG & Co. KGaA introduced a new line of bio-based polyurethane (PU) adhesives derived from sustainable feedstocks, specifically targeting high-volume footwear and packaging applications that must comply with the European Green Deal’s circular economy objectives. Simultaneously, BASF SE established a Structural Adhesives R&D Center in Ludwigshafen, focused on developing epoxy and methyl methacrylate (MMA) adhesives optimized for mixed-material automotive body-in-white (BIW) structures, an essential innovation for lightweight EV assembly.

Germany’s government mandates for low-VOC adhesives in public construction projects are accelerating demand for water-based and solvent-free bonding solutions, particularly in building insulation and infrastructure sealing. Moreover, major automotive OEMs and Tier 1 suppliers continue to invest heavily in electrically conductive adhesives (ECAs) and thermally conductive silicone gap fillers to enhance the safety, performance, and efficiency of EV battery systems. The country’s blend of engineering precision, sustainable chemical innovation, and rigorous environmental compliance positions Germany as the R&D nucleus of Europe’s specialty adhesives industry.

China: Expanding Specialty Adhesive Production and Application across Infrastructure and Manufacturing

China is the largest and fastest-growing producer and consumer of specialty adhesives, powered by massive infrastructure investments, government policy support, and a robust domestic manufacturing base. The government’s continued investment in high-speed rail and urban construction projects has sharply increased the demand for seismic-resistant structural adhesives and high-durability epoxy coatings, with 2024–2025 seeing record consumption across construction and civil engineering. Simultaneously, foreign and domestic players are investing in production capacity expansion, with a major European adhesive manufacturer commissioning new production lines in Eastern China in 2024 to support local demand for hot-melt adhesives in electronics and packaging.

In the electronics sector, Chinese manufacturers are rapidly integrating cyanoacrylate and UV-cured adhesives for microelectronic and wearable device assembly, prompting a wave of domestic R&D into faster-curing, precision-controlled specialty adhesives. The country’s “Made in China 2025” strategy continues to prioritize self-sufficiency in high-performance chemical materials, including silicone adhesives for renewable energy and EV battery applications. With escalating demand from construction, electronics, automotive, and renewable sectors, China remains the anchor of global specialty adhesive supply and consumption, blending scale with technological adaptation.

Japan: Precision Materials and Technological Innovation Define Specialty Adhesive Development

Japan stands as a global leader in precision-engineered specialty adhesives, driven by automotive lightweighting, electronics miniaturization, and bio-inspired material innovation. Leading automotive suppliers and chemical manufacturers are developing lightweight polyurethane and epoxy adhesives designed for multi-substrate bonding—enabling automakers to integrate carbon fiber-reinforced plastics (CFRP) and steel components to meet stringent fuel-efficiency and safety standards in 2024 and beyond.

In the electronics sector, Japanese companies are at the forefront of developing anisotropic conductive films (ACFs) and flexible film adhesives for ultra-fine pitch bonding in OLED displays, smartphones, and microelectronics. Research institutions across Japan are also pioneering bio-inspired reversible adhesives, capable of temporary bonding for cleanroom and medical applications, reflecting a focus on precision and sustainability. The healthcare industry, in particular, benefits from ongoing R&D into high-biocompatibility silicone and soft-skin adhesives for advanced wound care and wearable health monitoring devices. Japan’s deep integration of material science innovation and industrial application ensures its continued dominance in high-value specialty adhesive markets.

Switzerland: Specialty Adhesive Innovation Anchored by M&A and High-Precision Manufacturing

Switzerland continues to exert strong influence on the global specialty adhesives industry through strategic acquisitions, precision manufacturing, and sustainable materials development. In 2025, Covestro AG acquired a Swiss manufacturer of multi-layer adhesive films, reinforcing its global portfolio in specialty films and bonding technologies. Simultaneously, Sika AG, one of the world’s leading construction chemicals firms, remains a central figure in high-performance structural bonding agents and sealants designed for aerospace, automotive, and civil engineering applications.

Swiss adhesive producers emphasize precision, performance, and environmental compliance, investing in solvent-free and non-isocyanate adhesive formulations that meet the strictest European environmental and occupational safety standards. The focus aligns with Switzerland’s broader reputation for engineering excellence and sustainability leadership. As a result, Swiss companies continue to set benchmarks for reliability, clean manufacturing, and product certification in aerospace and high-load industrial bonding applications, maintaining the country’s reputation as a premium hub for specialty adhesives innovation.

India: Accelerating Specialty Adhesive Demand through Infrastructure, FMCG, and EV Growth

India’s specialty adhesives market is expanding rapidly, driven by the construction boom, packaging sector growth, and emerging EV manufacturing ecosystem. Large-scale infrastructure initiatives, including the Smart Cities Mission and industrial corridor projects, are driving demand for construction-grade adhesives, tile grouts, and waterproofing sealants. Companies like Mapei India, with new facilities in Kosi, Mathura (2022), are scaling local production capacity to support high-demand projects in both urban housing and transport infrastructure.

India’s FMCG and packaging industries continue to push the need for high-speed, durable hot-melt adhesives optimized for automated lines, ensuring efficiency and adhesion reliability. Additionally, the government’s focus on electric mobility, supported by Production-Linked Incentive (PLI) schemes, is propelling demand for thermal interface materials (TIMs) and flame-retardant structural adhesives critical to EV battery and component assembly. With both domestic and global companies strengthening R&D and distribution networks, India is emerging as a strategic hub for high-performance specialty adhesives manufacturing and export, underscoring its growing role in the Asia-Pacific adhesives value chain.

Specialty Adhesives Market Report Scope

Specialty Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.8 Billion

|

|

Market Size (2034)

|

$11.5 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Acrylic, Cyanoacrylate, Silicone, Polyolefin, Vinyl, Polyimide, Styrenic Block Copolymers, Methacrylate), By Technology (Water-Based, Solvent-Based, Hot-Melt, Reactive, UV-Curable/Light-Curing, Pressure-Sensitive), By End-Use Industry (Automotive & Transportation, Building & Construction, Packaging, Electronics, Medical & Healthcare, Aerospace & Defense, Industrial Assembly, Woodworking, Consumer/DIY), By Application (Structural Bonding, Non-Structural Bonding, Sealing & Caulking, Laminating, Tapes & Labels, Encapsulation & Potting, Fastening), By Functionality (Conductive, Flame-Retardant, High-Temperature Resistant, Flexible, High-Shear Strength, Low-Outgassing, Biocompatible

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema Group, Dow Inc., BASF SE, DuPont de Nemours, Inc., Huntsman Corporation, Illinois Tool Works Inc. (ITW), Avery Dennison Corporation, Jowat SE, Wacker Chemie AG, Covestro AG, Pidilite Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type/Chemistry

- Epoxy

- Polyurethane

- Acrylic

- Cyanoacrylate

- Silicone

- Polyolefin

- Vinyl

- Polyimide

- Styrenic Block Copolymers

- Methacrylate

By Technology

- Water-Based

- Solvent-Based

- Hot-Melt

- Reactive

- UV-Curable/Light-Curing

- Pressure-Sensitive

By End-Use Industry

- Automotive & Transportation

- Building & Construction

- Packaging

- Electronics

- Medical & Healthcare

- Aerospace & Defense

- Industrial Assembly

- Woodworking

- Consumer/DIY

By Application Type

- Structural Bonding

- Non-Structural Bonding

- Sealing & Caulking

- Laminating

- Tapes & Labels

- Encapsulation & Potting

- Fastening

By Functionality/Performance

- Conductive

- Flame-Retardant

- High-Temperature Resistant

- Flexible

- High-Shear Strength

- Low-Outgassing

- Biocompatible

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Arkema Group

- Dow Inc.

- BASF SE

- DuPont de Nemours, Inc.

- Huntsman Corporation

- Illinois Tool Works Inc. (ITW)

- Avery Dennison Corporation

- Jowat SE

- Wacker Chemie AG

- Covestro AG

- Pidilite Industries Limited

*- List not Exhaustive

Research Coverage

This comprehensive report on the Global Specialty Adhesives Market, published by USDAnalytics, investigates the technological breakthroughs, industry shifts, and performance innovations shaping the future of high-performance bonding systems across automotive, aerospace, electronics, construction, and medical industries. Through in-depth analysis reviews and data-backed insights, this report highlights the evolving dynamics of specialty adhesives, including the transition toward bio-based chemistries, advanced thermally conductive materials, and digitally integrated manufacturing systems. It thoroughly examines emerging trends such as reversible bonding for circular manufacturing, smart adhesives for wearables, and rapid-curing formulations for mass timber construction. Moreover, it explores how sustainability regulations, R&D investments, and industrial automation are redefining product design, performance standards, and supply chain competitiveness. Featuring detailed assessments of market trends, regulatory impacts, and strategic developments—including mergers, acquisitions, and product innovations—this report serves as an essential resource for industry professionals, investors, and policymakers aiming to navigate the complex specialty adhesives landscape. Backed by USDAnalytics’ robust research methodology and multidimensional evaluation framework, the report delivers actionable intelligence that enables strategic decision-making in rapidly evolving industrial and technological environments.

Scope Highlights

Segmentation:

- By Resin Type (Epoxy, Polyurethane, Acrylic, Cyanoacrylate, Silicone, Polyolefin, Vinyl, Polyimide, Styrenic Block Copolymers, Methacrylate)

- By Technology (Water-Based, Solvent-Based, Hot-Melt, Reactive, UV-Curable/Light-Curing, Pressure-Sensitive)

- By End-Use Industry (Automotive & Transportation, Building & Construction, Packaging, Electronics, Medical & Healthcare, Aerospace & Defense, Industrial Assembly, Woodworking, Consumer/DIY)

- By Application Type (Structural Bonding, Non-Structural Bonding, Sealing & Caulking, Laminating, Tapes & Labels, Encapsulation & Potting, Fastening)

- By Functionality/Performance (Conductive, Flame-Retardant, High-Temperature Resistant, Flexible, High-Shear Strength, Low-Outgassing, Biocompatible)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Historic Data: 2021–2024 | Forecast Data: 2025–2034

Companies Covered: Profiles and competitive analysis of 15+ leading global players, including Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema Group, Dow Inc., and others.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.