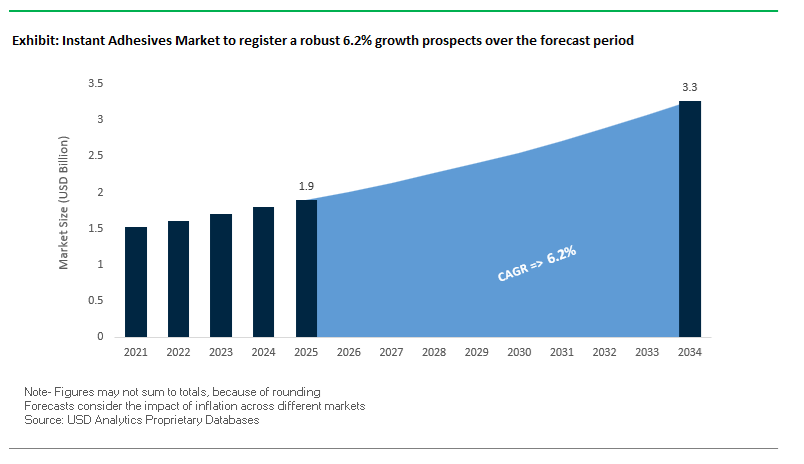

The Global Instant Adhesives Market is projected to expand from USD 1.9 billion in 2025 to USD 3.3 billion by 2034, advancing at a CAGR of 6.2%, as manufacturers across electronics, medical devices, industrial assembly, and maintenance operations re-engineer production around speed, precision, and regulatory cleanliness. Growth is structurally driven by the shift toward high-throughput automated lines and miniaturized components, where traditional curing-dependent adhesives introduce bottlenecks and variability. Cyanoacrylate-based instant adhesives, alongside emerging dual-cure hybrid systems, are increasingly specified because they deliver near-instant fixture strength—often in under 10 seconds—without heat, mixing, or complex dispensing infrastructure, directly supporting lean manufacturing and reduced cycle times.

From a materials and OEM-qualification perspective, leading manufacturers such as Henkel (Loctite), 3M, H.B. Fuller, Permabond, and Dymax have advanced instant adhesive platforms beyond basic fast bonding toward engineered performance profiles. Modern cyanoacrylates are formulated to address historical limitations related to odor, blooming, thermal resistance, and sterilization stability. Low-bloom, low-odor alkoxy-ethyl cyanoacrylates are increasingly deployed in electronics, medical, and cosmetic-device assembly, where particulate control and operator comfort are non-negotiable. At the same time, industrial-grade formulations with continuous thermal stability approaching 200°C are enabling broader adoption in automotive interiors, power tools, and aerospace maintenance environments where elevated temperatures and vibration are routine.

Medical and electronics manufacturing represent structurally important demand layers shaping product development. Instant adhesives validated for ethylene oxide (EtO), gamma irradiation, and autoclave sterilization are routinely specified for catheters, syringes, wearable sensors, and diagnostic devices, supporting regulatory approval without post-bond degradation. In parallel, UV/LED-curable cyanoacrylate hybrids are gaining traction where line-of-sight curing, positional control, and visual inspection are required; these systems allow on-demand cure triggering, color-change verification, and improved bond placement accuracy on automated lines.

The global instant adhesives industry is witnessing sustained innovation and expansion driven by formulation chemistry advancements, regional investments, and cross-sector adoption of high-performance bonding materials.

In February 2024, Henkel AG & Co. KGaA expanded its Loctite medical-grade adhesive line with the Loctite 4011S and 4061S series, purpose-built for bonding plastics, rubbers, and metals in regulated medical environments. These low-odor, low-bloom formulations were specifically engineered to enhance device assembly efficiency and meet ISO 10993 biocompatibility standards. Earlier in May 2024, 3M Company announced a $67 million investment in its Valley, Nebraska facility, adding new production lines to support its expanding portfolio of industrial adhesives and personal safety products, reflecting strong North American demand.

Permabond, a pioneer in cyanoacrylate technology, continued its innovation streak by launching UV6357, a UV-curable adhesive designed for cold-resistant industrial applications, including freezer component assembly. Previously, its 130UV and 135UV series introduced the market’s first dual-cure adhesives—combining moisture and UV cure mechanisms—offering complete cure control in shaded or inaccessible joints.

The medical and high-tech manufacturing sectors are shaping product innovation trends. Dymax Corporation introduced MD 1072-M-Z, a TPO-free, light-curable adhesive for medical device assembly, while emphasizing its Encompass® technology, enabling color-change curing for visual inspection. In parallel, Arkema (Bostik) strengthened its cyanoacrylate footprint through a joint venture with Cartell Chemical Co. (CMC) in January 2021, focusing on crackless monomer (CMC) technology for high-value engineering adhesives.

Strategic acquisitions also continue to reshape the competitive landscape. Sika AG’s acquisition of Hamatite from Yokohama Rubber Co. Ltd. (April 2021) reinforced its market position in Japan and expanded its adhesive offerings for automotive interiors and structural bonding. As a result, the instant adhesives ecosystem is evolving toward multi-chemistry integration, blending speed, precision, and sustainability across automotive, electronics, and healthcare verticals.

The market is witnessing a pronounced transition from petrochemical-based cyanoacrylates to bio-based instant adhesives as sustainability becomes central to industrial manufacturing strategies. Under the influence of global climate policies and Scope 3 emission reduction targets, adhesive manufacturers are investing heavily in renewable chemistry platforms, focusing on low-carbon feedstocks, renewable power integration, and biodegradable raw materials.

Collaborations like the Henkel–Dow partnership illustrate the shift, as the companies jointly deploy low-carbon feedstocks and renewable electricity to cut product carbon footprints (PCFs) by 20–40% across selected instant adhesive lines. Such initiatives underscore how industrial decarbonization is being driven by adhesive manufacturers aligning with global sustainability frameworks such as the European Green Deal and REACH chemical safety standards.

The trend is also visible in product innovation. A leading chemical producer recently commercialized a bio-based cyanoacrylate adhesive containing 60% renewable raw materials, derived from castor oil feedstocks, without compromising humidity and heat resistance. The milestone represents a significant achievement in sustainable formulation science, proving that renewable-sourced adhesives can match the high tensile and shear strength required in engineering-grade bonding.

Further, new medical-grade instant adhesives—engineered without CMR (Carcinogenic, Mutagenic, or Reproductive hazardous) ingredients—are being introduced to comply with stringent EU medical device and biocompatibility regulations. These innovations are redefining the market for healthcare adhesives, with sustainability an integrated performance metric alongside curing speed and reliability. Overall, the growing alignment of regulatory, consumer, and industrial priorities is pushing manufacturers to embed eco-innovation and material circularity into every phase of instant adhesive production.

The increasing complexity of electronic components and the miniaturization of devices in consumer, automotive, and 5G sectors have elevated the demand for high-performance, precision-grade instant adhesives tailored for advanced electronics assembly. These materials must combine rapid curing with thermal stability, electrical insulation, and superior mechanical retention across diverse substrates such as glass, metal, ceramics, and polyimide.

Recent product testing in the electronics adhesives segment reported a new cyanoacrylate formulation retaining 97% of its bond strength after 1,000 hours under “double 85” conditions (85°C/85% RH) and 87% retention after 168 thermal cycles (−40°C to 80°C). The durability benchmark positions instant adhesives as a viable solution for next-generation consumer electronics and power modules.

The integration of thermal management capability within adhesive systems is another key technological direction. A leading materials company recently introduced a dispersible gel-based Thermal Interface Material (TIM) with a thermal conductivity of 10 W/m·K, optimized for high-performance ASICs, FPGAs, and EV charging systems. These hybrid instant adhesives serve dual roles—mechanical bonding and efficient heat dissipation—critical for high-density, high-power applications.

In addition, low-temperature-curing, one-component instant adhesives are being engineered for optic and image sensor module assembly, where minimal heat exposure is essential to avoid component distortion. The adoption of these adhesives in semiconductor packaging and flexible electronics reflects the industry’s progression toward precision adhesives with multi-functional characteristics, a key differentiator in the competitive high-tech manufacturing landscape.

The global surge in electric vehicle (EV) production presents a major growth frontier for instant adhesives—particularly in battery cell stacking, module insulation, and thermal interface bonding. Adhesives are increasingly replacing mechanical fasteners in battery pack designs, providing lightweight structural integrity, vibration resistance, and improved safety.

Within EV systems, adhesives must simultaneously deliver high dielectric insulation and flame retardancy, adhering to rigorous certifications such as UL 94 V-0 to mitigate thermal runaway risks. Manufacturers are responding by developing flame-retardant, fast-curing cyanoacrylate and hybrid formulations that maintain structural strength while enhancing fire resistance in lithium-ion battery (LIB) modules.

Thermal management also represents a pivotal opportunity. Pressure-sensitive adhesives (PSAs)—both silicone-based (for compatibility with silicone TIMs) and acrylic-based (for non-silicone TIMs)—are being optimized for cell-to-cooling plate bonding, ensuring efficient heat transfer and preventing hotspots. These adhesives enable modular design flexibility, shorten assembly times, and improve the overall thermal stability and lifecycle performance of EV battery systems.

With the global EV battery market expected to exceed 2.5 TWh of annual capacity by 2030, the role of instant adhesives in enabling lightweight, thermally optimized, and safety-compliant EV designs will continue to expand exponentially, creating a high-margin niche for specialized adhesive manufacturers.

The rise of on-demand manufacturing and digital supply ecosystems presents a novel opportunity for instant adhesive suppliers to provide localized, just-in-time availability for high-value industries like aerospace, defense, and medical device repair. As global manufacturers pivot toward additive manufacturing (AM) and distributed production models, the demand for rapid-curing, small-batch adhesive systems optimized for maintenance, repair, and overhaul (MRO) operations is growing sharply.

Studies indicate that integrating 3D printing with local adhesive application processes can reduce lead times for custom components from several weeks to mere days, improving supply chain resilience and operational flexibility. Adhesive producers are aligning with the digital transformation by offering modular, cartridge-based packaging systems suitable for automated dispensing in additive manufacturing workflows.

Further, distributed manufacturing models reduce inventory and logistics costs, with digital design files enabling global replication of parts and local adhesive bonding for final assembly. The shift—driven by digital inventory management platforms—is transforming instant adhesives into critical enablers of decentralized, high-efficiency production ecosystems, offering both performance reliability and reduced total cost of ownership (TCO) for industrial operators.

As Industry 4.0 ecosystems mature, the integration of smart logistics, additive manufacturing, and chemical micro-distribution will open new service-based revenue streams for adhesive manufacturers, especially those that leverage data-driven forecasting, remote monitoring, and automated replenishment systems.

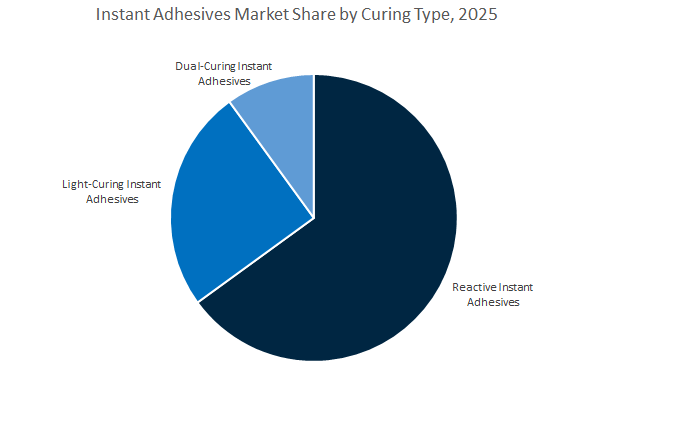

Instant Adhesives Market Share Insights, 2025-2034

Reactive instant adhesives, primarily cyanoacrylates, dominate the global instant adhesives market with an estimated 62.5% share in 2025, owing to their versatility, rapid curing, and ability to bond dissimilar materials such as metal, plastic, rubber, and composites. These adhesives polymerize instantly in the presence of surface moisture, delivering high shear strength, excellent gap filling, and long-term durability, making them indispensable in maintenance, repair, and assembly (MRO) operations across automotive, electronics, and general industrial sectors. Their simplicity—requiring no heat, mixing, or pressure—drives their widespread adoption in on-demand bonding and precision manufacturing. Manufacturers continue to advance low-bloom, odorless, and high-temperature-resistant formulations, broadening their use in medical devices and electronic assemblies where aesthetics and reliability are critical.

Light-curing instant adhesives represent the fastest-growing subsegment, fueled by their adoption in high-speed electronic, optical, and medical manufacturing lines that require precise curing control and minimal thermal stress. These adhesives cure within seconds under UV or visible light exposure, offering excellent transparency, positional accuracy, and process efficiency. Dual-curing systems, combining UV and moisture or heat activation, cater to complex geometries and shadowed bonding areas, ensuring full polymerization even in inaccessible joints. Their role is expanding in advanced electronics, automotive sensors, and hybrid assembly lines, where performance consistency and low defect rates are paramount.

The industrial assembly and maintenance, repair, and operations (MRO) segment leads the global instant adhesives market with a 30.8% share in 2025, reflecting its universal use across machinery, equipment repair, and component assembly. Instant adhesives provide rapid fixture times, high tensile strength, and ease of application, making them ideal for production lines, plant maintenance, and emergency repair work. Their reliability in bonding metals, ceramics, and plastics makes them a critical enabler of industrial uptime and operational efficiency. The segment’s dominance is reinforced by automation and lean manufacturing trends, which emphasize faster throughput and reduced adhesive waste.

The electronics assembly sector is a key growth engine, driven by miniaturization, precision bonding, and component encapsulation in smartphones, wearables, and printed circuit boards (PCBs). Light- and dual-curing instant adhesives are increasingly used for sensor encapsulation, connector bonding, and optical assembly, where clarity, low shrinkage, and electrical insulation are essential. The automotive and transportation sector continues to expand its use of instant adhesives for interior assembly, gasketing, wire harnessing, and electric vehicle (EV) components, leveraging their fast-curing and vibration-resistant properties.

In medical and healthcare applications, instant adhesives are essential for device assembly, disposable product bonding, and biocompatible instrument manufacturing, where low-toxicity, sterilization compatibility, and precision curing are required. The consumer, DIY, and craft sectors represent a large-volume, lower-margin segment, characterized by household repair, model building, and small assembly uses, supported by extensive retail availability and product accessibility. Meanwhile, packaging, labeling, and woodworking applications represent smaller but steady niches where instant adhesives offer rapid adhesion and surface versatility.

The instant adhesives market is defined by continuous product innovation, regulatory compliance adaptation, and deep technical collaboration between suppliers and OEMs. The major industry players—Henkel, Dymax, Permabond, H.B. Fuller, and 3M—are driving competitive differentiation through medical-grade formulations, dual-curing chemistries, and digital process integration.

Henkel AG & Co. KGaA: Loctite Redefines High-Speed Industrial Bonding

Henkel’s Loctite brand dominates the global instant adhesives market, with a legacy in maintenance, repair, and operations (MRO). Its solutions prevent over one million hours of unplanned downtime annually through advanced bonding and sealing technologies. The company’s instant adhesives portfolio extends beyond consumer-grade cyanoacrylates to industrial-strength solutions for metals, plastics, and composites. Loctite’s 2047 threadlocker exemplifies this specialization—engineered for large bolts requiring extreme shear and lubricity performance. Additionally, Henkel provides a turnkey system integration model, combining adhesive selection, dispensing automation, and process optimization for OEMs.

Dymax Corporation: Pioneering Dual-Cure and Medical-Grade Light-Curable Adhesives

Dymax Corporation leads in UV/LED-curable adhesive systems with its Encompass® Technology, combining color-change (See-Cure) and Ultra-Red® fluorescence for real-time process control. Its MD® 2000 series features IBOA- and TPO-free formulations designed for biocompatible, skin-proximal applications such as catheters and wearable sensors. The company’s adhesives deliver fixture strength in under 5 seconds, supporting fully automated syringe and transducer assembly lines. Dymax continues to strengthen its position in medical device bonding and electronics encapsulation, ensuring unmatched precision and regulatory compliance.

Permabond: Dual-Cure Cyanoacrylates for Industrial and Aerospace Applications

Permabond is recognized for its innovation in high-temperature and specialty industrial adhesives, including the iconic PERMABOND® 910, approved under MIL-A-46050C for aerospace-grade use. The company recently launched dual-cure cyanoacrylate/UV hybrid systems like 130UV and 135UV, providing instant bonding even in areas shielded from UV exposure. Its UV6357 formulation, engineered for cold-temperature durability, is gaining traction in refrigeration and industrial electronics. Permabond offers customized formulations with short lead times, serving demanding clients across defense, automotive, and electronics sectors.

H.B. Fuller Company: Expanding High-Performance Industrial and Medical Adhesive Platforms

H.B. Fuller leverages its extensive experience in specialty industrial adhesives to deliver solutions for lightweighting, sustainability, and precision assembly. Its cyanoacrylate portfolio complements broader adhesive systems including acrylics and epoxies, targeting automotive, electronics, and healthcare markets. The company focuses on automation-ready adhesives, offering integrated support from formulation to process implementation. With a strong global presence—particularly in Asia-Pacific—and an emphasis on bio-based innovation, H.B. Fuller continues to shape the market through sustainable and high-performance adhesive solutions.

3M Company: Investing in Next-Generation Instant Adhesive Solutions

3M combines material science with adhesive innovation to deliver single-part cyanoacrylates and activators used across automotive, electronics, and industrial sectors. Known for its reliability and product consistency, 3M’s adhesives provide rapid bonding for difficult substrates, often used in conjunction with its tapes and abrasives. Its $67 million Valley, Nebraska expansion (2024) enhances production capacity and ensures supply chain resilience. Through constant R&D, 3M continues to advance instant adhesive durability and performance, supporting next-generation EV component assembly and electronics manufacturing.

China dominates the global instant adhesives market, powered by its massive consumer electronics, electric vehicle (EV), and industrial manufacturing base. The country's emphasis on automation and high-speed production lines is accelerating the adoption of high-throughput instant bonding systems that combine adhesives with micro-dispensing and robotic precision equipment. Major electronics and automotive manufacturers are utilizing surface-insensitive cyanoacrylates (CAs) for bonding diverse substrates—such as flexible displays, foldable screens, and battery pack components—where rapid fixture and clean curing are essential.

The rapid EV industry growth, supported by government incentives and a robust domestic supply chain, has intensified demand for high-strength, thermally stable cyanoacrylates for lightweight bonding of sensors, battery housings, and interior modules. Additionally, the national “Green Manufacturing Transformation Plan” has prioritized low-VOC, solvent-free adhesives, creating opportunities for eco-friendly, fast-setting instant formulations. Global adhesive giants, including Henkel, have expanded R&D operations in Shanghai to address local miniaturization, performance, and sustainability requirements. With strong government policy backing and robust R&D infrastructure, China stands as the largest and most advanced market for industrial-grade instant adhesives in Asia.

The United States Instant Adhesives Market leads in innovation for premium performance adhesives tailored for e-mobility, aerospace, and healthcare applications. U.S.-based manufacturers are at the forefront of light-curing cyanoacrylates (UV-CAs) that combine instant bonding with rapid curing under UV light, drastically reducing assembly time in aerospace, electronics, and industrial component production. Companies such as 3M and Henkel are expanding capacity and product portfolios—3M’s expansion of its Valley, Nebraska facility (May 2024) underscores increasing U.S. demand for advanced instant bonding solutions across industrial and consumer markets.

The medical adhesives segment is witnessing strong momentum, with new biocompatible and sterilization-resistant cyanoacrylate formulations introduced for medical sensors, diagnostic kits, and wound closure systems. Meanwhile, the push for EV battery safety and durability is prompting manufacturers to invest in high-temperature-resistant CAs that perform reliably under thermal stress. The Department of Energy’s (DOE) support for clean mobility initiatives continues to boost adhesive innovation in electric drive systems. Combined with strict EPA sustainability standards, U.S. manufacturers are steering the market toward low-emission, high-performance instant adhesives engineered for precision and reliability.

Germany remains a critical hub for precision industrial adhesives in Europe, shaped by a strong regulatory focus and the country’s deep expertise in engineering and materials science. Under the influence of EU REACH regulations and carbon neutrality goals, German manufacturers such as DELO Industrial Adhesives are pioneering low-VOC, bio-based, and odorless instant adhesives for high-sensitivity applications across consumer electronics, optics, and medical devices.

Recent advancements include directional conductive adhesives designed as solder-free alternatives for MiniLED and MicroLED production, optimizing reliability in high-density electronics. DELO’s 2025 innovations, including dual-cure instant adhesives for camera lens bonding in high-resolution optical modules, represent Germany’s leadership in next-generation precision bonding technology. Furthermore, the domestic automotive sector’s demand for high-strength, thermally resilient CAs complements the ongoing shift toward lightweight electric mobility platforms. Germany’s emphasis on bio-compliance, low emissions, and industrial durability positions it as the benchmark market for sustainable instant adhesive development in Europe.

South Korea’s position as a global electronics and semiconductor powerhouse drives demand for high-precision, low-viscosity instant adhesives tailored for micro-dispensing in miniaturized devices. Local manufacturers and research institutions are focusing on dual-cure cyanoacrylate systems, combining UV and moisture curing mechanisms, to ensure rapid bonding in both exposed and shadowed areas—an essential feature for intricate wearable and medical device assemblies.

The market is also seeing strong adoption of elastic-bonding CAs, offering flexibility and stress absorption in flex-circuit and plastic-rubber hybrid materials, vital for advanced consumer electronics. South Korea’s ongoing innovation in semiconductors, display panels, and healthcare devices is sustaining consistent demand for ultra-fast, reliable instant bonding solutions. As part of the country’s “Digital and Green New Deal” initiative, adhesive manufacturers are also investing in environmentally conscious formulations to meet sustainability mandates while supporting high-tech, precision-driven industries.

Japan continues to lead the global market in micro-component bonding and aerospace-grade instant adhesive applications, reflecting its unmatched focus on reliability, precision, and miniaturization. Following Sika AG’s 2021 acquisition of Hamatite, Japan’s industrial adhesives sector has witnessed increased integration of high-strength instant and structural bonding technologies for both automotive and construction sectors.

Japanese manufacturers are pioneering low-viscosity cyanoacrylates and precision dispensing adhesives for microelectronics and optical instruments, ensuring stable performance under temperature and vibration extremes. The country’s advanced aerospace and robotics industries demand adhesives capable of maintaining bond integrity in extreme thermal environments, driving R&D toward high-temperature-resistant CAs with exceptional shear and impact strength. With its emphasis on performance stability, long-term reliability, and high-purity chemistry, Japan remains a global hub for advanced instant adhesive R&D and niche high-value applications.

The Brazilian Instant Adhesives Market is gaining momentum as industrial modernization and infrastructure development create new demand for rapid bonding and repair solutions. Global leaders like Henkel operate regional R&D and production centers in Itapevi, São Paulo, developing adhesive systems specifically suited for South American industrial maintenance, automotive, and construction environments.

Brazil’s position as Latin America’s largest automotive manufacturing base supports continuous consumption of instant adhesives in vehicle assembly, component repair, and aftermarket maintenance. The applications often require high-strength, temperature-stable cyanoacrylates for quick, reliable bonding on metals, plastics, and composites. Combined with expanding investment in localized adhesive production, Brazil is emerging as a strategic hub for instant bonding technologies across the region.

India’s instant adhesives market is witnessing rapid expansion fueled by the dual engines of industrial infrastructure development and domestic manufacturing growth. The government’s “Make in India” and PLI (Production Linked Incentive) initiatives are attracting significant foreign direct investment in automotive, electronics, and consumer goods sectors, leading to a surge in demand for high-performance, fast-curing cyanoacrylates.

Local leaders like Pidilite Industries dominate the market through its flagship brand Fevikwik, while also expanding into industrial-grade CA formulations catering to electronics assembly, wood bonding, and structural repair. Rapid urbanization and e-commerce growth are increasing consumption of instant adhesives for packaging, assembly, and maintenance applications. India’s growing focus on import substitution, cost-efficient manufacturing, and sustainability-driven adhesives positions it as a key emerging market for instant adhesive production and export in Asia.

Instant Adhesives Market Report Scope

Instant Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$3.3 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Chemistry (Cyanoacrylate Adhesives, Epoxy Adhesives, Other Chemistries), By Technology (Reactive Instant Adhesives, Light-Curing Instant Adhesives, Dual-Curing Instant Adhesives), By Substrate (Metals Bonding, Plastics Bonding, Rubber Bonding, Composites Bonding, Wood & Veneer Bonding, Glass/Ceramics Bonding, Porous Materials Bonding), By End-Use Industry (Electronics Assembly, Automotive & Transportation, Medical & Healthcare, Industrial Assembly & MRO, Packaging & Labeling, Woodworking & Furniture, Consumer/DIY & Crafts), By Form (Liquid Adhesives, Gel Adhesives, Solvents-Free Adhesives, Low-Viscosity Adhesives, High-Viscosity Adhesives

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Arkema Group, Sika AG, Huntsman Corporation, DELO Industrial Adhesives, Wacker Chemie AG, Pidilite Industries Limited, Permabond Engineering Adhesives, Ashland Inc., Avery Dennison Corporation, Panacol-Elosol GmbH, Dymax Corporation, Hubei Huitian New Materials Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Cyanoacrylate Adhesives

- Epoxy Adhesives

- Other Chemistries

By Technology/Curing Type

- Reactive Instant Adhesives

- Light-Curing Instant Adhesives

- Dual-Curing Instant Adhesives

By Substrate

- Metals Bonding

- Plastics Bonding

- Rubber Bonding

- Composites Bonding

- Wood & Veneer Bonding

- Glass/Ceramics Bonding

- Porous Materials Bonding

By End-Use Industry

- Electronics Assembly

- Automotive & Transportation

- Medical & Healthcare

- Industrial Assembly & MRO

- Packaging & Labeling

- Woodworking & Furniture

- Consumer/DIY & Crafts

By Form

- Liquid Adhesives

- Gel Adhesives

- Solvents-Free Adhesives

- Low-Viscosity Adhesives

- High-Viscosity Adhesives

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Arkema Group

- Sika AG

- Huntsman Corporation

- DELO Industrial Adhesives

- Wacker Chemie AG

- Pidilite Industries Limited

- Permabond Engineering Adhesives

- Ashland Inc.

- Avery Dennison Corporation

- Panacol-Elosol GmbH

- Dymax Corporation

- Hubei Huitian New Materials Co. Ltd.

*- List not Exhaustive

Research Coverage

Purpose-built for engineers, sourcing leaders, and product managers, the USDAnalytics study on the Instant Adhesives Market delivers a decision-ready narrative that connects speed-to-assembly with compliance and total cost of ownership: this report investigates how ultra-fast fixture, dual-cure photoinitiation, and sterilization-ready grades are reshaping line design in electronics, medical, automotive, and MRO; benchmarks durability under heat/humidity and chemical exposure; and traces specification shifts toward low-odor, low-bloom, IBOA/TPO-free portfolios. It documents commercialization breakthroughs in UV/LED hybrids, heat-resistant cyanoacrylates, and inspection-ready color-change systems; analysis reviews investments, partnerships, and capacity adds that de-risk supply; and highlights process KPIs—open time control, substrate latitude, and first-pass yield—that compress takt times without compromising biocompatibility or optical clarity. With scenario forecasts tied to automation intensity and device miniaturization, this report is an essential resource for OEMs, converters, and investors seeking resilient, regulation-aligned bonding strategies, etc……

Scope Highlights

Segmentation

- By Chemistry: Cyanoacrylate Adhesives; Epoxy Adhesives; Other Chemistries

- By Technology/Curing Type: Reactive Instant Adhesives; Light-Curing Instant Adhesives; Dual-Curing Instant Adhesives

- By Substrate: Metals; Plastics; Rubber; Composites; Wood & Veneer; Glass/Ceramics; Porous Materials

- By End-Use Industry: Electronics Assembly; Automotive & Transportation; Medical & Healthcare; Industrial Assembly & MRO; Packaging & Labeling; Woodworking & Furniture; Consumer/DIY & Crafts

- By Form: Liquid; Gel; Solvents-Free; Low-Viscosity; High-Viscosity

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analyses/profiles (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.