Medical Adhesives Market Overview: Device Integration, Wearable Expansion, and Sterilization Standards Reshape Medical Adhesives Demand

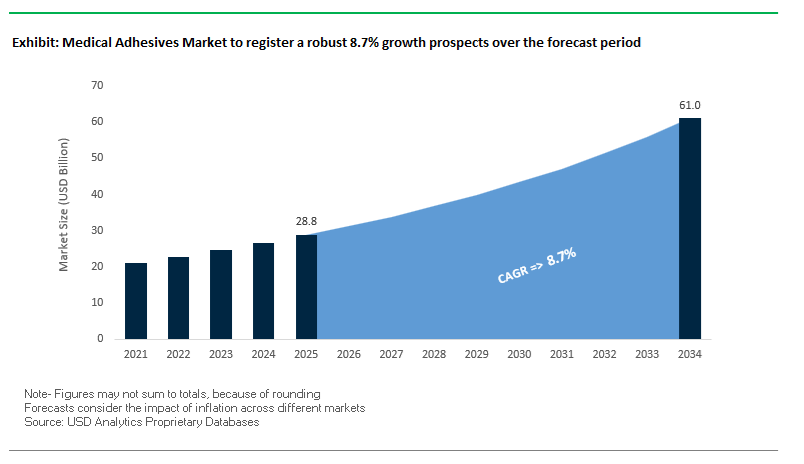

The Global Medical Adhesives Market is projected to expand from USD 28.8 billion in 2025 to USD 61 billion by 2034, advancing at a CAGR of 8.7%, as medical adhesives become core enablers of device integration, patient mobility, and regulatory clearance rather than ancillary consumables. Growth is structurally driven by the rapid proliferation of wearable medical devices, reusable surgical instruments, and minimally invasive therapies, all of which impose stringent requirements on adhesive biocompatibility, sterilization durability, and long-term bond stability. As healthcare delivery shifts beyond hospitals into homecare and remote monitoring, adhesive performance increasingly determines device reliability, patient compliance, and product lifecycle economics.

From an OEM qualification and regulatory standpoint, medical adhesives are now governed by non-negotiable biocompatibility thresholds. More than 90% of adhesives used in implantable Class II and Class III devices must comply with ISO 10993-5 and ISO 10993-10, elevating cytotoxicity and sensitization testing to gatekeeping criteria for market access. Manufacturers are responding by advancing UV-curable medical acrylics, bioresorbable systems, fibrin sealants, and silicone and polyurethane PSAs, engineered to maintain adhesion under physiological exposure while supporting sterilization and repeat handling. Mechanical performance remains equally decisive: next-generation UV-curable acrylic adhesives achieving tensile shear strengths above 2,000 psi are enabling high-speed bonding of catheters, tubing, and precision surgical components on automated assembly lines.

Application dynamics further differentiate demand. In surgical environments, fibrin sealants such as Baxter’s TISSEEL, validated across 15+ surgical specialties including cardiac and hepatic procedures, continue to anchor demand for predictable hemostasis and tissue sealing where mechanical fixation is impractical. In parallel, the fastest growth is emerging from wearable and continuous-monitoring devices, where polyurethane and silicone-based pressure-sensitive adhesives are expanding at 18–22% annually, supporting long-wear durations of up to 14 days without skin irritation or bond failure. These applications place unique stress on adhesives, requiring a balance between gentle skin interaction and resistance to sweat, motion, and repeated removal.

Sterilization resilience has become a defining procurement criterion. More than 75% of newly launched medical adhesives are now qualified to withstand three or more autoclave or ethylene oxide (EtO) sterilization cycles, ensuring bond integrity for reusable instruments and reducing total device replacement costs. This requirement is pushing suppliers to optimize polymer backbones, crosslink density, and cure mechanisms to avoid degradation under heat, moisture, and chemical exposure.

The medical adhesives industry is undergoing rapid transformation fueled by technological innovation, regulatory modernization, and strategic collaborations across the MedTech ecosystem. In October 2025, Henkel’s Loctite brand launched a new series of LED-curable adhesives (Loctite AA 3951/AA 3961) designed to meet the needs of smaller, more sophisticated medical device assemblies. These products enhance flexibility, improve curing speed, and address biocompatibility demands for emerging device miniaturization trends. Similarly, in January 2025, Henkel also unveiled Loctite AA 3952 and SI 5057, engineered specifically to bond TPE substrates—a critical innovation amid the industry’s shift away from DEHP-containing PVC materials under new EU MDR safety frameworks.

In September 2025, Baxter International secured FDA approval for an updated TISSEEL Fibrin Sealant protocol, expanding its validated application range to pediatric surgeries (over one month of age). This regulatory milestone strengthens Baxter’s leadership in surgical hemostasis and tissue sealing solutions. Meanwhile, a July 2025 innovation introduced an MPEG-PCL hydrogel-based sealant for minimally invasive procedures, marking a step forward in bioresorbable adhesion and internal wound repair. Complementing this, a May 2025 academic breakthrough achieved a protein-based tissue adhesive with bonding strength comparable to surgical sutures but 60% faster application time, aligning with clinical goals of reduced operative durations.

Strategic movements continued through March 2025, when 3M’s Medical Solutions Division completed the acquisition of a European startup specializing in flexible substrate bonding for low-trauma skin adhesives. The deal enhances 3M’s leadership in wearable technologies and continuous glucose monitoring (CGM) adhesive systems. Earlier in November 2024, H.B. Fuller announced a €25 million investment in expanding its Medical Adhesive Technologies R&D and manufacturing operations in Europe, focusing on cyanoacrylate and hydrogel innovation for wound care. Concurrently, Ethicon (Johnson & Johnson) presented 12-month clinical data (October 2024) demonstrating a 40% reduction in wound dehiscence for its DERMABOND PRINEO Skin Closure System, validating adhesive-based closures as superior alternatives to sutures.

Regulatory frameworks continue to shape market direction, as seen in September 2024, when the EU MDR transition prompted the withdrawal of legacy medical adhesives, compelling manufacturers to reinforce biocompatibility documentation and ISO testing protocols.

Market Trend 1: Emergence of Soft, Skin-Conformal, and Electrically Conductive Adhesives for Next-Generation Wearable Sensors

The surge in remote patient monitoring and wearable medical electronics has made skin-conformal, conductive adhesives one of the most rapidly growing segments within the global medical adhesives market. Recent academic research drives the pivotal role of nanomaterials in enhancing electrical conductivity, mechanical strength, and electron transfer efficiency in adhesive matrices. These materials increase effective surface area and enable faster signal processing, vital for next-generation biosensors that continuously monitor physiological parameters like ECG, glucose, and hydration levels.

On the materials front, silicone gels and hydrogel adhesives have gained prominence due to their atraumatic removal characteristics, ensuring comfort and safety for sensitive skin. Medical-grade silicone and hydrogel systems minimize Medical Adhesive Related Skin Injury (MARSI), an increasing concern in long-term wearable use. Top manufacturers are intensifying R&D to create low-irritation, biocompatible skin adhesives that maintain secure adhesion over extended periods while allowing easy removal, a critical feature for devices worn continuously for 14–28 days.

From a technology integration perspective, the convergence of 5G and IoT connectivity in medical wearables is driving the demand for flexible, electrically conductive adhesives (ECAs) that act as efficient interconnects. Unlike rigid solder, ECAs provide superior mechanical flexibility and thermal stability, essential for miniaturized, high-frequency health devices. As a result, electrically conductive medical adhesives are becoming a key enabler of smart medical patches, diagnostic biosensors, and AI-integrated health systems, directly influencing the future trajectory of digital healthcare technology.

Market Trend 2: Growing Shift Toward Biodegradable and Hemostatic Tissue Adhesives for Minimally Invasive Surgery

The global movement toward minimally invasive and rapid-recovery surgical techniques is accelerating adoption of biodegradable and hemostatic medical adhesives designed to replace sutures and staples. Advanced synthetic sealants offer rapid bleeding control, secure tissue approximation, and full resorption—eliminating the complications associated with foreign materials.

A recent study on GelMA-based microneedle arrays hybridized with silicate nanoplatelets demonstrated a 92% reduction in bleeding in in vivo rat liver models and a dramatic decrease in clotting time from over 11 minutes to approximately 1.3 minutes. Such data confirms the efficacy of bio-inspired hemostatic materials in promoting immediate coagulation and tissue adhesion. Additionally, innovative milk casein–polyacrylamide (PAAm) adhesives have exhibited a maximum peeling force of 378 N/m and fracture stress of 180 kPa, achieving strong adhesion on vital organs like the liver and heart without inflammatory response—an important benchmark for next-generation internal tissue adhesives.

On the regulatory side, the U.S. FDA’s Class III classification for synthetic absorbable adhesives reflects the rigorous safety and clinical validation these devices must meet. The classification ensures that biodegradable tissue sealants entering the market adhere to the highest standards for performance and biocompatibility. The clinical push for absorbable hemostatic and closure materials aligns with broader surgical trends favoring faster recovery, reduced infection risk, and minimal post-operative intervention, reinforcing the as one of the most strategic innovation zones in the medical adhesives industry.

Market Opportunity 1: Expanding Application of Rapid-Closure Adhesives in Ambulatory Surgery Centers (ASCs)

The exponential rise of Ambulatory Surgery Centers (ASCs) is opening new growth corridors for fast-curing surgical adhesives that streamline procedural efficiency and reduce hospitalization costs. ASCs are revolutionizing outpatient care by offering surgeries 35%–50% cheaper than inpatient facilities, translating into $684 average savings per procedure and an annual U.S. healthcare cost reduction exceeding $40 billion.

Efficiency is a key driver in the segment. Studies report that procedures in ASCs take up to 25% less time compared to hospital outpatient departments (HOPDs), creating sustained demand for rapid-closure adhesives that eliminate the time-consuming nature of suturing. In clinical trials, 2-octyl cyanoacrylate adhesives demonstrated significantly faster closure times—217.2 seconds vs. 383.3 seconds for sutures—while providing equivalent wound integrity and superior cosmetic outcomes.

Manufacturers are developing ready-to-use, sterile applicator systems optimized for high patient throughput in outpatient surgical environments. With procedure volumes in ASCs growing by 6–7% annually, particularly across orthopedics, spine, and cardiovascular specialties, the demand for bioabsorbable, time-efficient adhesives will remain robust. The shift marks a fundamental change in the surgical adhesives supply chain, as product design increasingly focuses on speed-to-hemostasis and ease of use for cost-sensitive, high-volume settings.

Market Opportunity 2: Advancements in Bioactive Adhesive Dressings for Chronic Wound Management

The global chronic wound epidemic—especially diabetic foot ulcers (DFUs) and venous leg ulcers—is driving rapid market expansion for bioactive adhesive dressings that deliver antimicrobial and regenerative therapy. Chronic wounds affect roughly 2% of the population, costing the U.S. healthcare system more than $50 billion annually. These conditions demand innovative adhesive wound dressings that not only protect but also actively accelerate healing.

A randomized controlled trial found that bioactive adhesive dressings reduced wound size by 45% within one month, compared to 30% reduction for passive dressings, demonstrating superior healing efficiency. Current R&D emphasizes hydrogel-based adhesive dressings capable of carrying therapeutic agents such as magnesium-doped bioactive glass vesicles, achieving an 8.2-fold increase in macrophage cellular uptake—a critical mechanism for promoting angiogenesis and tissue repair.

In addition, adhesives incorporating natural antimicrobial polymers like chitosan have shown exceptional clinical outcomes. Long-term studies indicate that bioactive wound dressings based on chitosan derivatives not only enhance healing rates but also reduce surgical debridement requirements and lower amputation risks in diabetic patients. As hospitals and wound care centers adopt these advanced bioadhesive systems, the segment’s growth is expected to accelerate, bridging medical adhesives with regenerative medicine and bioactive therapeutics.

Medical Adhesives Market Share Analysis

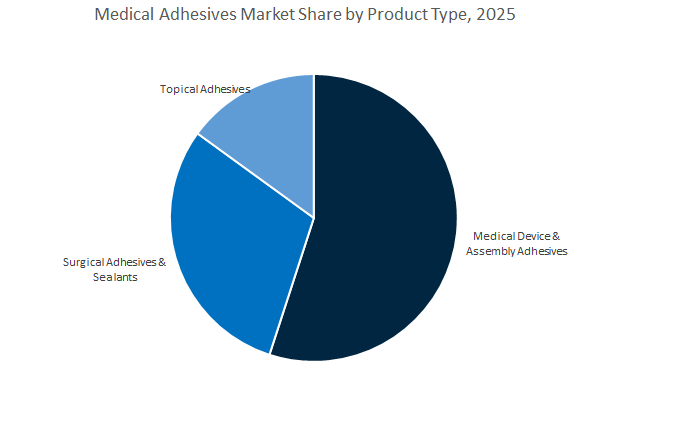

Market Share by Product Type

The medical device and assembly adhesives segment dominates the global medical adhesives market, accounting for a projected 53.6% share in 2025, underscoring its critical role in the mass production of disposable and complex medical equipment. This segment’s dominance is driven by the surge in single-use medical devices, diagnostic instruments, catheters, tubing, and surgical tools, which demand high-precision bonding solutions that ensure mechanical stability, biocompatibility, and sterilization resistance. The global shift toward minimally invasive medical devices and micro-scale assembly has further accelerated the use of advanced cyanoacrylate, UV-curable, and epoxy-based medical adhesives that support fine-tolerance assembly with rapid cure times and controlled viscosity. These adhesives are essential for maintaining device integrity under sterilization processes such as autoclaving, gamma irradiation, and ethylene oxide exposure. Moreover, regulatory requirements from agencies such as the FDA and EMA have pushed manufacturers to develop low-toxicity, ISO 10993-compliant, and solvent-free formulations, ensuring patient safety while optimizing production efficiency.

The surgical adhesives and sealants segment represents a high-value market niche characterized by increasing adoption in internal tissue repair, hemostasis, and wound closure. As healthcare systems pivot toward sutureless surgeries and laparoscopic interventions, surgical adhesives are rapidly replacing traditional sutures and staples. Formulations based on fibrin, polyethylene glycol (PEG), cyanoacrylate, and albumin-glutaraldehyde polymers are enabling precise tissue adhesion with biodegradable and hemostatic properties, reducing postoperative complications and healing time. Meanwhile, the topical adhesives segment plays a pivotal role in external wound care, surgical draping, and skin-applied medical wearables, emphasizing skin-friendly formulations with balanced adhesion and removability. These adhesives cater to the growing market for advanced wound care products and long-wear biosensors, particularly in chronic disease management and remote patient monitoring.

Market Share by Application

The medical device and equipment assembly segment dominates the global medical adhesives market, holding a projected 48.9% share in 2025, driven by the continuous rise in high-volume manufacturing of diagnostic, surgical, and therapeutic devices. These adhesives enable precise assembly of components in syringes, infusion sets, catheters, endoscopes, and implantable systems, where mechanical stability, clarity, and sterilization compatibility are essential. The growing integration of automation and micro-dispensing systems in device production lines has increased reliance on UV-curable and reactive adhesives that allow fast, clean, and automated bonding processes. Additionally, the expansion of wearable and connected medical technologies—such as continuous glucose monitors (CGMs) and biosensing patches—continues to drive adhesive innovation focused on biocompatibility, hypoallergenic properties, and long-term wear comfort. The trend toward miniaturization and multifunctional medical devices has reinforced the need for adhesives that combine optical clarity, dielectric insulation, and flexibility, enhancing both device functionality and patient safety.

External medical applications remain a key growth segment, encompassing wound dressings, transdermal patches, and wearable health monitors. This category is witnessing strong momentum as home healthcare, telemedicine, and self-care markets expand globally. Adhesives used in these products must exhibit gentle skin adhesion, moisture management, and long-wear performance, enabling products to remain effective for extended use without causing irritation. Silicone, hydrocolloid, and polyurethane-based systems dominate this area, offering superior conformability and breathability. The internal medical applications segment, though smaller in share, represents the most technologically sophisticated domain, requiring bioabsorbable, non-toxic, and tissue-compatible adhesives for surgical procedures and implant fixation. This category is being reshaped by the development of biodegradable cyanoacrylates and bio-inspired tissue adhesives, which support wound healing and controlled degradation post-implantation.

The competitive environment of the global medical adhesives market is defined by technological depth, regulatory compliance, and diversified product innovation. Market leaders such as 3M Company, Ethicon (Johnson & Johnson), Baxter International, Henkel AG & Co. KGaA, and H.B. Fuller Company dominate through strategic R&D, acquisitions, and material advancements that enhance clinical efficacy, manufacturing efficiency, and patient comfort.

3M leads the global medical adhesives space with over 1,200 Pressure Sensitive Adhesives (PSAs) tailored for skin contact applications. The company’s adhesive portfolio underpins medical tapes, wound dressings, and wearable monitoring systems, designed for multi-day use without causing Medical Adhesive-Related Skin Injury (MARSI). Its continued investment in 2024 to expand Asia-Pacific production facilities underscores its focus on scalable wound care materials. 3M’s strategic emphasis on digital health integration and remote patient monitoring cements its role as an essential enabler of the global wearable MedTech revolution.

Ethicon’s DERMABOND line of cyanoacrylate-based topical skin adhesives remains a benchmark for surgical wound management. Used globally in millions of procedures, these products form a microbial barrier that reduces Surgical Site Infections (SSIs) while enhancing cosmetic outcomes. The DERMABOND PRINEO System integrates a self-adhering mesh providing strength equivalent to a 4-0 suture, ideal for long incisions. Leveraging Johnson & Johnson’s clinical network and education programs, Ethicon is continually expanding its adhesive technologies across hospitals and surgical centers worldwide.

Baxter’s TISSEEL Fibrin Sealant remains the industry’s most clinically proven biological adhesive, with over 15 million surgical applications. It replicates the body’s natural clotting mechanism and provides precise hemostatic control during complex cardiac and hepatic surgeries. With innovations like the DUPLOSPRAY System, Baxter delivers enhanced control for open and laparoscopic procedures. The company’s R&D focus extends to bioabsorbable sealants and anti-adhesion barriers, reinforcing its strategic objective of improving recovery time and minimizing post-surgical complications.

Henkel, through its Loctite brand, commands a global leadership position in medical device assembly adhesives, offering over 40 ISO 10993-certified products. Its UV and LED-curable technologies enable rapid processing and durability under sterilization. The launch of Loctite AA 3952 and SI 5057 represents a critical innovation for TPE and flexible substrates, addressing evolving EU MDR standards. Henkel also provides comprehensive equipment integration solutions, combining adhesives, dispensing, and curing systems, which improve OEM productivity and regulatory compliance.

H.B. Fuller’s leadership in cyanoacrylate and hydrogel-based adhesives positions it as a key supplier to global MedTech OEMs. Its Cybond line delivers rapid, structural bonding for single-use medical devices with superior substrate compatibility. Following a €25 million investment in late 2024, Fuller enhanced its European R&D and cleanroom production capabilities, driving sustainability through solvent-free and low-waste adhesive systems. The company’s emphasis on eco-conscious formulation and high-purity materials aligns with global trends toward greener medical manufacturing and circular economy integration.

Country Analysis: Global Medical Adhesives Industry

United States: Regulatory Approvals and Smart Adhesive Expansion Strengthen Market Leadership

The United States medical adhesives industry continues to lead global innovation, backed by the FDA’s robust regulatory framework, advanced R&D infrastructure, and a strong medtech manufacturing base. In October 2024, the FDA approved the expansion of use for VISTASEAL, a plasma-protein-based fibrin sealant distributed by Johnson & Johnson, for pediatric surgical bleeding control, signaling increasing adoption of biological hemostats across diverse surgical segments.

R&D activity remains intense, focusing on advanced cyanoacrylate chemistries, antimicrobial surgical adjuncts, and next-generation tissue approximation adhesives designed for rapid curing and controlled degradation. Manufacturers are increasingly pursuing 510(k) and PMA pathways to secure regulatory clearance for products supporting both open and minimally invasive surgeries.

Investment trends show a strong focus on Ambulatory Surgical Centers (ASCs), where demand for single-use, room-temperature-stable medical adhesive systems is rising. Additionally, the booming market for wearable healthcare technologies, including continuous glucose monitoring (CGM) and remote patient monitoring (RPM) devices, is fueling the use of skin-friendly silicone and acrylic adhesives that ensure long-term adhesion without skin irritation. The combination of regulatory progress, funding for bioresorbable polymers, and clinical adoption trends positions the U.S. as a global epicenter for advanced surgical adhesives and smart wearable bonding solutions.

Germany: Engineering Precision and Polymer Science Drive Next-Generation Surgical Adhesive Development

Germany stands as a European powerhouse for medical adhesives and sealants, leveraging its precision engineering, polymer chemistry expertise, and compliance with EU MDR standards. The German company Adhesys Medical strengthened its global position after receiving U.S. FDA approval in 2021 for its surgical adhesive HEMIGLUE, marking a critical milestone in biocompatible, high-strength wound closure technologies.

Collaborations between German medtech manufacturers, research institutes, and government agencies under Horizon Europe’s Health R&D program are accelerating innovations in biocompatible, resorbable, and functionalized medical adhesives. The focus extends to urethane and epoxy-based adhesives designed for complex medical device assemblies, such as catheters, infusion systems, and surgical instruments that require strong, flexible bonding with varied materials.

Germany’s deep integration of medical polymer research and regulatory precision ensures its continued dominance in orthopedic, dental, and surgical adhesive innovations, contributing to a growing export footprint across Europe, the U.S., and Asia-Pacific.

China: Domestic Innovation and Regulatory Streamlining Propel Rapid Growth in Medical Adhesives

China’s medical adhesives and sealants market is witnessing rapid expansion, underpinned by the Made in China 2025 initiative and large-scale healthcare modernization efforts. The government’s prioritization of domestic production of advanced biomaterials is transforming China into a key global manufacturing hub for medical-grade adhesives used in wound care, surgical sealing, and diagnostic devices.

Regulatory advancements by the National Medical Products Administration (NMPA) have introduced fast-track approval programs for cyanoacrylate-based topical adhesives and bio-resorbable hydrogel sealants, enabling quicker commercialization of local innovations. Major domestic companies are scaling up automated manufacturing lines for polyethylene glycol (PEG) hydrogel adhesives, serving the growing demand in orthopedic and general surgery.

Academic institutions, notably Peking University, are at the forefront of biomimetic adhesive development, including mussel-inspired, double-crosslinked hydrogels that exhibit superior wet adhesion and biodegradability. Concurrently, the explosion in wearable and diagnostic device manufacturing is driving high consumption of medical-grade silicone adhesives for applications such as ECG electrodes and continuous monitoring patches. With streamlined regulation and innovation-driven scaling, China is emerging as a top global producer and exporter of next-generation medical adhesive materials.

Japan: Biocompatible and Bio-Resorbable Adhesives Support Advanced Surgical Innovation

Japan continues to lead the Asia-Pacific medical adhesives industry through breakthroughs in biocompatible and resorbable materials tailored for highly specialized medical applications. In 2025, Japanese firms reported triple-digit growth in silk-elastin-based internal sealants, highlighting a strong national focus on bioengineered adhesives that safely degrade within the human body.

The Pharmaceuticals and Medical Devices Agency (PMDA) plays a critical role in maintaining rigorous standards for ophthalmic and dental adhesive formulations, ensuring exceptional precision and safety. In parallel, Japan’s aging population is driving strong demand for low-trauma, skin-friendly adhesives in chronic wound management and home-based elderly care.

Japanese material science companies like Nitto Denko are advancing high-performance pressure-sensitive adhesives (PSAs) optimized for wearable medical sensors and diagnostics, balancing strong adhesion with gentle removability. Moreover, research partnerships between academic institutions and medical manufacturers continue to innovate fully degradable adhesives for minimally invasive and robotic surgeries, reinforcing Japan’s leadership in precision and biocompatible medical bonding systems.

United Kingdom: Strategic Acquisitions and Smart Wound Care Innovation Drive Growth

The United Kingdom’s medical adhesives industry is expanding rapidly through strategic acquisitions, export-led growth, and R&D in antimicrobial technologies. Advanced Medical Solutions (AMS), a key UK-based manufacturer, strengthened its global presence by acquiring Sealantis, broadening its product portfolio across surgical sealants, tissue adhesives, and wound closure systems.

UK research organizations, backed by UK Research and Innovation (UKRI), are driving the commercialization of polymeric hydrogel-based medical adhesives aimed at improving soft tissue repair and skin adherence performance. Simultaneously, UK medtech innovators are developing antimicrobial-coated closure systems and smart sutures integrated with bioadhesives, offering real-time infection control in surgical environments.

UK-based adhesive producers are also pursuing regulatory approvals in Asia-Pacific markets, expanding their global footprint for high-performance, biocompatible adhesives used in cardiovascular, neurological, and orthopedic surgeries. The initiatives position the UK as a key player in advanced wound care adhesives and minimally invasive surgical glues.

Israel: Pioneering Biotech-Driven Biomimetic Sealants and Injectable Adhesive Systems

Israel’s medical adhesives and sealants market is defined by cutting-edge biotechnology and start-up-driven innovation ecosystems. Companies like LifeBond have achieved significant milestones, securing EU regulatory approval for LifeSeal, a bioabsorbable surgical adhesive used in gastrointestinal and tissue sealing procedures.

The country’s medtech landscape is dense with biomimetic adhesive startups, developing solutions inspired by marine organism adhesion mechanisms, such as wet-surface bonding in complex surgical environments. Israeli R&D investment is particularly strong in injectable, minimally invasive sealants designed for laparoscopic and robotic surgeries, where precision and rapid polymerization are essential.

Israel’s blend of medical biotechnology expertise, venture capital funding, and export-oriented commercialization strategies continues to position it as a global innovation hub for next-generation surgical adhesives and hemostatic solutions.

Medical Adhesives Market Report Scope

Medical Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.8 Billion

|

|

Market Size (2034)

|

$61 Billion

|

|

Market Growth Rate

|

8.7%

|

|

Segments

|

By Resin Type (Synthetic (Acrylic, Silicone, Polyurethane, Epoxy, Polyethylene Glycol), Natural (Fibrin, Collagen, Albumin, Others)), By Technology (Reactive, Water-Based, Solvent-Based, Hot Melt), By Application (Internal Medical Applications, External Medical Applications, Dental, Medical Devices & Equipment

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Henkel AG & Co. KGaA , H.B. Fuller Company, Sika AG, Avery Dennison Corporation, The Dow Chemical Company, Nitto Denko Corporation, Arkema Group (Bostik), PPG Industries, Inc., Dymax Corporation, Master Bond, Inc., Permabond LLC, Johnson & Johnson (Ethicon), Baxter International, Ashland Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Adhesives Market Segmentation

By Product/Resin Type

- Synthetic (Acrylic, Silicone, Polyurethane, Epoxy, Polyethylene Glycol)

- Natural (Fibrin, Collagen, Albumin, Others)

By Technology

- Reactive

- Water-Based

- Solvent-Based

- Hot Melt

By Application

- Internal Medical Applications

- External Medical Applications

- Dental

- Medical Devices & Equipment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Medical Adhesives Market

- 3M Company

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Avery Dennison Corporation

- The Dow Chemical Company

- Nitto Denko Corporation

- Arkema Group (Bostik)

- PPG Industries, Inc.

- Dymax Corporation

- Master Bond, Inc.

- Permabond LLC

- Johnson & Johnson (Ethicon)

- Baxter International

- Ashland Inc.

*- List not Exhaustive

Research Coverage

USDAnalytics delivers a practitioner-first assessment of the Global Medical Adhesives Market, where this report investigates demand shifts across surgical closure, wearable fixation, and device assembly; benchmarks ISO-aligned biocompatibility and sterilization resilience; and maps commercialization pathways for UV/LED-curable, bioresorbable, and skin-conformal systems. Blending clinical evidence with manufacturing realities, our analysis reviews miniaturization-driven bonding needs, supply chain localization, and MDR/FDA documentation rigor; curates breakthroughs in conductive skin adhesives, PEG/fibrin sealants, and low-trauma PSAs; and highlights implications for cost-to-serve, automation readiness, and quality-by-design. Designed for R&D, regulatory, sourcing, and operations leaders, this report is an essential resource for aligning product roadmaps with safety standards, accelerating time-to-clearance, and de-risking scale-up across hospitals, ASCs, and OEM lines.

Scope Highlights

Segmentation (covered in this study):

- By Product/Resin Type: Synthetic (Acrylic, Silicone, Polyurethane, Epoxy, Polyethylene Glycol); Natural (Fibrin, Collagen, Albumin, Others)

- By Technology: Reactive; Water-Based; Solvent-Based; Hot Melt

- By Application: Internal Medical Applications; External Medical Applications; Dental; Medical Devices & Equipment

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies, including 3M Company; Henkel AG & Co. KGaA; H.B. Fuller Company; Sika AG; Avery Dennison Corporation; The Dow Chemical Company; Nitto Denko Corporation; Arkema Group (Bostik); PPG Industries, Inc.; Dymax Corporation; Master Bond, Inc.; Permabond LLC; Johnson & Johnson (Ethicon); Baxter International; Ashland Inc.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.