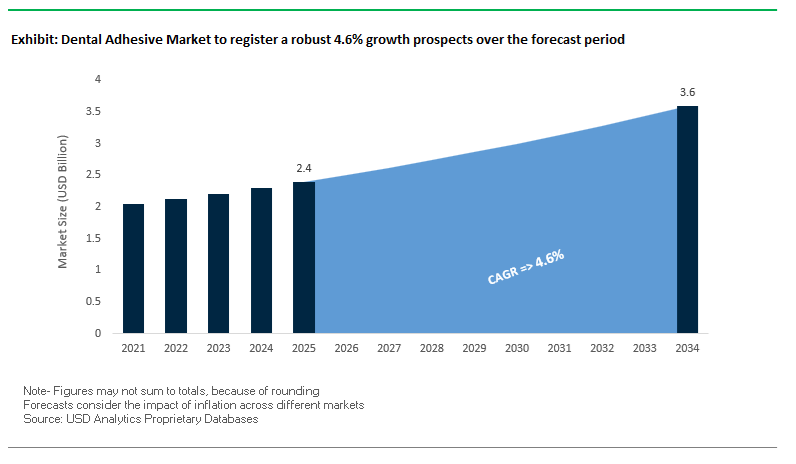

The global dental adhesive market is strategically relevant today because restorative dentistry is being reorganized around predictability, procedure consolidation, and long-term clinical stability rather than technique-driven variability. The market is projected to grow from USD 2.4 billion in 2025 to USD 3.6 billion by 2034, at a CAGR of 4.6%, reflecting sustained adoption of universal dental adhesives across restorative, prosthodontic, and aesthetic procedures. Growth is not volume-driven alone; it is anchored in the replacement of multi-step, substrate-specific bonding protocols with single-bottle systems that deliver consistent bond performance while reducing chair time and technique sensitivity. Aging patient populations, minimally invasive treatment philosophies, and rising demand for aesthetic restorations are reinforcing the need for adhesives that perform reliably across enamel, dentin, ceramics, zirconia, and metal substrates without procedural complexity.

Demand is being structurally reshaped by the clinical validation and routine use of 8th-generation universal dental adhesives, which represent a clear departure from earlier etch-and-rinse or self-etch silos. These systems consistently deliver bond strengths exceeding 25 MPa on both enamel and dentin, independent of etching mode, enabling clinicians to standardize workflows across direct composites, veneers, and indirect restorations. The integration of functional monomers capable of chemically interacting with metal oxides and tooth substrates has positioned universal adhesives as foundational materials rather than adjunct consumables. As a result, clinicians increasingly specify adhesives based on long-term interface stability and cross-compatibility with modern restorative materials, rather than brand-driven preference.

Material innovation is translating directly into measurable clinical and operational outcomes. The incorporation of radiopaque fillers allows adhesive layers to be visualized under X-ray, improving diagnostic clarity around marginal integrity and secondary caries without invasive intervention. Delivery-system engineering, such as high-efficiency pen applicators capable of providing up to four times more applications per milliliter, reduces material waste while improving dosing accuracy and infection control. Advanced desensitizing chemistries that effectively seal dentinal tubules under both wet and dry conditions have lowered post-operative sensitivity, reducing follow-up visits and restoration failures. Looking forward, market momentum will be shaped by manufacturers’ ability to maintain bond durability, hydrolytic resistance, and regulatory compliance while supporting high-throughput clinical workflows, reinforcing universal dental adhesives as clinically qualified, efficiency-driven bonding systems rather than interchangeable restorative supplies.

The global dental adhesive industry is witnessing rapid transformation as manufacturers focus on improving clinical outcomes, workflow efficiency, and material biocompatibility. The ongoing integration of digital workflows, radiopaque materials, and chemically stable monomers is shaping the next generation of restorative solutions.

In December 2024, Premier Dental introduced the VeneerNow™ Injectable Matrix System, a step toward streamlined anterior restorations, emphasizing simplified light-curing adhesives that reduce procedural time in aesthetic bonding workflows. Just a month earlier, in November 2024, Garrison Dental Solutions launched the Loop Curing Light, featuring closed-loop technology that dynamically adjusts light output for consistent polymerization across restorations. This innovation directly enhances the curing performance of photo-initiated dental adhesives, reducing failure rates and ensuring reliable bonding depth.

October 2024 was a pivotal month for corporate consolidation. HuFriedyGroup’s acquisition of SS White Dental expanded its product synergy in procedural tools—including adhesive application instruments—demonstrating the rising emphasis on integrated product portfolios. In the same month, Kuraray Noritake Dental extended its KATANA Zirconia product family, reinforcing the need for specialized resin cements and primers to achieve durable adhesion on high-strength ceramics.

Earlier, in July 2023, BISCO introduced the SureFil Universal Plus adhesive, showcasing the ongoing R&D race to enhance hydrolytic stability and cross-compatibility. Similarly, Rodin™ Bond entered the market in September 2023, offering a dual-use adhesive optimized for both direct and indirect restorations. Academic studies conducted in 2023 revealed that thermocycling (up to 5,000 cycles) had minimal impact on the microtensile bond strength (μTBS) of universal adhesives, confirming the durability of current adhesive-dentin interfaces.

On a regional scale, Europe’s aging population remains a long-term market driver. The rising need for durable restorative procedures, coupled with stricter biocompatibility standards, has amplified the use of long-lasting, hydrolysis-resistant adhesives and fixatives. As dental clinics increasingly adopt digital impression systems and CAD/CAM-based restorations, universal adhesives with optimized polymer crosslinking and chemical versatility are becoming the new clinical standard across Europe and North America.

The universal adhesive systems segment is emerging as a dominant force within the dental adhesives market, providing a single-bottle solution adaptable to multiple clinical techniques — including self-etch, selective-etch, and total-etch protocols. The movement aligns with the growing demand for simplified, technique-insensitive adhesives that maintain consistently high bond strength across enamel, dentin, metal, and ceramic substrates.

A 2024 comparative academic study found that updated universal adhesive formulations demonstrated a significantly thinner adhesive layer (p<0.001) and narrower oxygen inhibition zones compared to previous versions, resulting in improved polymerization efficiency and clinical marginal integrity. Such performance gains minimize postoperative sensitivity and technique variability, allowing dentists to achieve predictable results even under challenging clinical conditions.

In addition, the incorporation of HEMA-free adhesive chemistry has improved moisture tolerance and reduced hydrolytic degradation. Independent data published in 2023 reported that a leading HEMA-free universal adhesive achieved mean dentin bond strengths of 35.15 MPa after one year of simulated aging — a benchmark for long-term restoration stability. These innovations mark a shift toward next-generation universal adhesives that combine simplified application with extended restoration longevity, catering to high-throughput dental practices and multi-material bonding needs.

The transition from passive adhesion to bioactive and ion-releasing adhesive systems represents one of the most transformative advancements in restorative dentistry. These formulations not only secure the restoration but also contribute to active tooth remineralization and caries inhibition, effectively extending the service life of bonded restorations.

Recent ion-release studies under acidic challenge conditions (pH 4.0) have confirmed that bioactive resin materials can release up to 22.9 mg/L of calcium and 17.3 mg/L of fluoride, creating a localized ionic exchange at the adhesive-tooth interface that neutralizes acid attacks and encourages remineralization. The controlled ion release is a direct response to the global clinical challenge posed by secondary caries, which account for 40–60% of all composite restoration failures.

Incorporating fluoride-releasing glass fillers and bioactive nanoparticles into adhesive systems significantly improves the tooth-adhesive interface, fostering a self-healing microenvironment that reduces the recurrence of decay at restoration margins. With the global emphasis on preventive dentistry, these bioactive dental adhesives offer practitioners an evidence-backed pathway toward enhanced clinical outcomes and reduced retreatment frequency.

The growing global adoption of CAD/CAM and 3D printing technologies in digital dentistry is creating a high-value market for advanced adhesive systems optimized for indirect restorations. As clinicians increasingly rely on precision-milled materials like zirconia and lithium disilicate, there is a pressing demand for chemical coupling adhesives capable of forming durable bonds to non-etchable ceramics and hybrid materials.

Clinical guidelines for non-retentive zirconia restorations highlight that reliable adhesion requires the use of MDP-containing primers (phosphate monomer-based) following tribochemical silica coating or sandblasting with 30–50 µm alumina particles. These monomer-activated systems establish a chemical bond between zirconia’s metal oxide surface and the resin matrix, delivering long-term adhesion stability.

In addition, the rise of digital restorative materials like hybrid ceramics and polymer-infiltrated ceramics requires differentiated conditioning — hydrofluoric acid etching (up to 60 seconds) for feldspathic ceramics and silane-based coupling for hybrid ceramics. The complexity of these workflows drives the market need for material-specific or multi-substrate dental bonding agents tailored to CAD/CAM fabrication.

Manufacturers are responding with universal adhesives that include integrated silane and phosphate monomers, ensuring streamlined use in chairside milling and same-day digital restoration environments. The intersection between digital workflow integration and adhesive innovation represents a multi-billion-dollar growth frontier in restorative dentistry.

The surge in dental implant procedures worldwide is driving demand for implant-specific adhesive systems designed to optimize both retention and retrievability in cement-retained restorations. Unlike conventional prosthetic bonding, implant adhesives must maintain long-term biocompatibility while preventing microleakage and ensuring mechanical stability under continuous occlusal load.

Recent advancements in self-adhesive resin cements tailored for implant-supported crowns address key clinical challenges such as marginal sealing, easy cleanup, and reversible retention. These materials combine strong chemical adhesion to titanium or zirconia abutments with controlled bond strength that permits prosthesis retrievability when necessary — a vital requirement for maintenance and hygiene.

Further innovation is emerging through the integration of nanotechnology-enhanced fillers and antimicrobial components, designed to improve wear resistance, marginal adaptation, and peri-implant tissue compatibility. Research also drives the role of advanced zirconia implant biomaterials, which necessitate coupling agents capable of forming stable silane or phosphate bonds for enhanced crown-abutment longevity.

With the global dental implant market projected to grow in double digits due to population aging and aesthetic demand, manufacturers offering biocompatible, nanocomposite-based, and retrievable implant adhesives are well-positioned to capture a lucrative market segment in high-end prosthodontics.

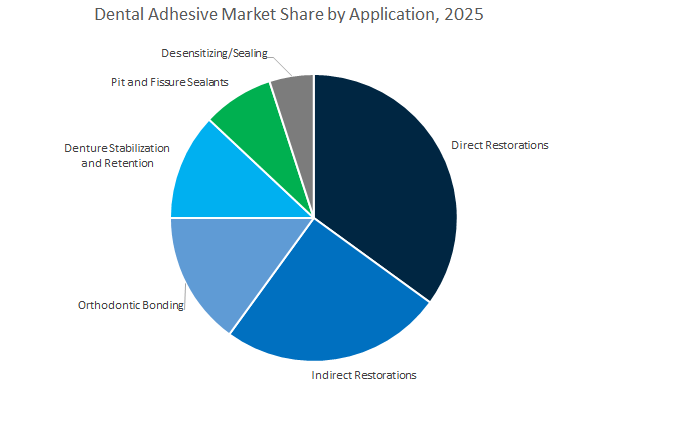

Dental Adhesive Market Share Insights, 2025-2034

Direct Restorations Lead the Global Dental Adhesive Market with 33.8% Share Owing to High Clinical Volume and Everyday Use

The direct restorations segment dominates the global dental adhesive industry, accounting for 33.8% of the market share in 2025, primarily driven by the widespread use of composite resin restorations in both developed and emerging markets. As amalgam usage declines due to mercury regulations and patient preference for aesthetic solutions, composite fillings have become the standard of care in restorative dentistry. Dental adhesives play a crucial role in this procedure by ensuring micromechanical bonding between enamel, dentin, and resin composites, improving both functional durability and aesthetic results. The ongoing shift toward universal adhesives—single-bottle systems compatible with multiple etching modes—is streamlining clinical workflows and reducing chair time, further supporting adoption among dental professionals. Additionally, the rise in minimally invasive dentistry and the growing prevalence of dental caries among children and adults continue to reinforce the segment’s dominance. Manufacturers are heavily investing in developing next-generation self-etch and nanofilled adhesives that offer enhanced bond strength, reduced technique sensitivity, and better long-term color stability—keeping the direct restorations segment as the backbone of the global dental adhesive market.

Indirect Restorations Account for 25.9% Market Share, Fueled by Growth in Cosmetic and Prosthetic Dentistry

The indirect restorations segment, which includes veneers, crowns, bridges, and inlays/onlays, represents a significant 25.9% share of the dental adhesives market. This growth is supported by the global surge in cosmetic and restorative dental procedures, driven by rising aesthetic awareness and increasing geriatric populations requiring prosthetic rehabilitation. Adhesives and resin cements are vital in ensuring durable bonds between the prosthesis and the prepared tooth surface, especially with the growing use of ceramic, zirconia, and hybrid materials. The transition from conventional luting cements to adhesive resin-based systems is transforming the workflow of indirect restoration placement, improving longevity, aesthetics, and marginal integrity. Furthermore, the rapid expansion of CAD/CAM-based digital dentistry is boosting demand for adhesives compatible with milled restorations, providing reliable, fast-curing bonds optimized for precision-fit restorations. These innovations, combined with the global increase in elective cosmetic dentistry, position the indirect restoration category as one of the most innovation-driven and profitable segments within the dental adhesive market.

Dental Clinics and Hospitals Dominate the Market with 72.6% Share as the Primary End-Use Channel

Dental clinics and hospitals hold an overwhelming 72.6% share of the global dental adhesives market, as nearly all restorative, orthodontic, and sealing procedures are performed within these facilities. General practitioners and specialists such as prosthodontists, orthodontists, and cosmetic dentists are the key decision-makers influencing adhesive selection, creating a market driven by clinical performance, ease of use, and brand reliability. The ongoing rise in private dental practices, coupled with increasing investments in advanced equipment and materials, particularly in emerging markets like China, India, and Brazil, continues to fuel adhesive demand. Furthermore, the global expansion of aesthetic dentistry and chairside digital workflows—including direct CAD/CAM restorations—has reinforced the use of high-quality adhesive systems. This professional end-user base also represents the primary target for companies offering continuing education programs, product demonstrations, and clinical research collaborations, strengthening brand loyalty and supporting consistent market dominance in this segment.

Dental Laboratories Emerge as a Key Technical Segment in Indirect Restoration Bonding

Dental laboratories form a vital B2B segment within the dental adhesive industry, focusing on the fabrication of indirect restorations such as crowns, veneers, and inlays. While their market share is smaller than clinical end-users, their technical role is indispensable. Labs require specialized adhesives and cements for pre-bonding, assembling, and final finishing of prosthetic components. The rise of digital dentistry workflows, including 3D-printed and CAD/CAM restorations, has driven demand for laboratory-grade bonding systems that can ensure compatibility with advanced restorative materials such as zirconia, lithium disilicate, and hybrid ceramics. Moreover, laboratories often act as innovation partners to manufacturers, testing new formulations under real-world conditions. The integration of digital technologies and resin bonding agents in dental labs signifies their growing influence on adhesive selection and performance optimization within clinical settings.

The global dental adhesive market is highly competitive, dominated by leading innovators such as 3M (Solventum), Dentsply Sirona, Ivoclar Vivadent, Kerr Corporation (Envista), and Kuraray Noritake Dental. These companies differentiate themselves through monomer technology leadership, integrated delivery systems, and clinically validated adhesive-dentin interface stability. Their strategies are focused on improving bond reliability, application efficiency, and regulatory compliance across key global markets.

3M’s Scotchbond™ Universal Plus Adhesive continues to set the gold standard in the universal dental adhesives market. It’s the first adhesive system with dentin-like radiopacity, helping clinicians distinguish adhesive layers from caries in radiographs. Designed for total-etch, self-etch, and selective-etch techniques, it ensures a consistent bond above 25 MPa on both enamel and dentin. Its integration with the 3M™ RelyX™ Universal Resin Cement simplifies workflows by eliminating separate primers for zirconia and glass ceramics, streamlining indirect restoration cementation.

Dentsply Sirona’s Prime&Bond active™ Universal Adhesive exemplifies innovation in hydrophilic-hydrophobic balance, ensuring consistent performance across moist and dry dentin conditions. Its Active-Guard Technology minimizes microleakage and enhances adhesive reliability in variable moisture environments, directly addressing post-operative sensitivity. Delivered via the CliXdish™ system, it allows up to 30 minutes of usability, optimizing multi-quadrant efficiency. The adhesive’s compatibility with all etching modes and restorative materials positions Dentsply as a leading provider of clinical versatility and workflow optimization.

Ivoclar Vivadent’s Adhese Universal and Tetric N-Bond Universal adhesives showcase a clinical balance between ease of use and desensitizing performance. The VivaPen delivery system allows direct intra-oral application, improving control and reducing material waste by up to 60%. With >25 MPa bond strength and built-in tubule sealing, these adhesives eliminate the need for separate desensitizers. Seamless compatibility with Ivoclar’s Tetric CAD composites and Variolink Esthetic luting materials enables efficient, integrated restorative workflows favored by aesthetic dentists worldwide.

Kerr’s OptiBond™ family, led by OptiBond FL and OptiBond XTR, continues to dominate through filled adhesive innovation. The inclusion of filler particles enhances mechanical retention by forming a hybrid layer with resin tags penetrating dentin tubules. This design minimizes microleakage and ensures long-term marginal integrity. With over a decade of proven success, OptiBond systems remain integral to restorative and cosmetic dentistry. As part of Envista, Kerr integrates these adhesives with Demetron curing lights and proprietary composite systems for consistent polymerization and bonding reliability.

Kuraray Noritake Dental stands as a pioneer in adhesive monomer technology. Its patented MDP monomer forms durable chemical bonds with hydroxyapatite, ensuring exceptional interface stability across multiple etching protocols. Products like CLEARFIL™ Universal Bond exemplify this stability, combining high hydrolytic resistance with broad substrate compatibility. The company continues to innovate with bonding systems engineered for its KATANA Zirconia line, ensuring optimized adhesion to metal oxides, ceramics, and glass substrates, critical for high-performance restorative dentistry.

The United States dental adhesive market continues to dominate global innovation, led by universal adhesive systems, bioactive materials, and FDA-driven regulatory clarity. Recent launches from leading manufacturers have focused on multi-mode adhesive systems compatible with total-, self-, and selective-etch techniques, integrating advanced monomers such as 10-MDP for superior bonding with zirconia and metal substrates.

The market is undergoing a major transformation with the emergence of bioactive dental adhesives that can release calcium and phosphate ions, fostering dentin remineralization and extending restoration longevity. The innovations, supported by NIH-backed dental school research, mark a paradigm shift toward functional restorative bonding. The FDA’s streamlined 510(k) pathway for new bonding agents has further accelerated product commercialization timelines.

Additionally, digital dentistry integration is gaining momentum, with adhesive systems designed specifically for 3D-printed restorations and resin-based cements optimized for CAD/CAM workflows. The growing preference for moisture-tolerant adhesives in esthetic veneer and indirect restorations is reshaping product development priorities. Strategic acquisitions by major U.S. dental corporations underscore the consolidation of proprietary adhesive technologies, ensuring sustained R&D competitiveness in the North American dental materials market.

Germany remains the European powerhouse for dental adhesive technology, renowned for its focus on precision, durability, and regulatory compliance. Companies such as Voco GmbH and Kulzer GmbH are leading the development of self-adhesive resin cements that eliminate separate priming steps, significantly enhancing chairside efficiency. German manufacturers are pioneering next-generation polymer systems with exceptional adhesion to ceramics and hybrid composites—key for long-lasting indirect restorations.

The nation’s academic institutions are heavily engaged in clinical trials on adhesive longevity and bond degradation, directly influencing international ISO standards and best practice protocols. Additionally, EU-mandated environmental goals are driving the adoption of solvent-free, low-VOC bonding agents, making Germany a model for sustainable material innovation.

Further, federal funding initiatives are supporting the development of antimicrobial dental adhesives, aiming to reduce secondary caries—a major clinical concern in long-term restorations. With expanding European logistics infrastructure and a strong “Made in Germany” reputation, the country continues to anchor the premium global dental materials supply chain, blending quality, innovation, and sustainability.

Japan maintains a leading role in the global dental adhesive market through its unmatched expertise in monomer chemistry, aesthetic resin cement production, and clinical innovation. Japanese chemical giants such as Kuraray Noritake Dental—inventors of the 10-MDP monomer—continue to define global bonding standards for universal adhesives and resin cements. The monomer’s chemical stability and compatibility with zirconia and metal oxides remain the benchmark in adhesive science.

Manufacturers like GC Corporation have expanded product lines with high-viscosity resin-based luting cements that enhance color retention and film uniformity for superior esthetic outcomes in ceramic restorations. Concurrently, the country’s aging population drives demand for specialized denture adhesives and bio-compatible formulations that improve retention for geriatric patients.

Japan’s innovation ecosystem thrives on collaboration between academia and chemical industries, ensuring steady development of high-purity, low-cytotoxicity monomers and rapid polymerization technologies. The promotion of Immediate Dentin Sealing (IDS) protocols in clinical education further sustains domestic demand for high-bond-strength adhesives. With its unmatched manufacturing precision and chemical formulation expertise, Japan remains a global epicenter for high-performance, aesthetic dental bonding materials.

China’s dental adhesive industry is expanding rapidly, powered by massive healthcare infrastructure investments, rising dental care awareness, and strong domestic R&D capabilities. The government’s emphasis on modernizing dental clinics and scaling digital dentistry has driven robust demand for universal adhesives and light-cured resin cements across public and private practices.

Domestic manufacturers are narrowing the technology gap with global leaders by developing affordable, high-quality universal bonding systems tailored for chairside convenience and digital workflows. The surge in CAD/CAM and 3D scanning adoption across urban centers has further boosted demand for high-strength luting cements compatible with ceramic restorations and milled prosthetics.

Simultaneously, innovation clusters within Chinese technology parks are directing R&D toward cost-effective monomer synthesis, focusing on developing proprietary alternatives to established Western chemistries. The National Medical Products Administration (NMPA) continues to simplify Class II and III adhesive approvals, reducing market entry barriers and promoting domestic product adoption. As a result, China has become a production powerhouse and demand hub in the Asia-Pacific dental adhesive market.

Switzerland remains synonymous with precision, reliability, and innovation in the premium dental adhesives and resin cements market. Companies such as Ivoclar are pioneering dual-cure resin cements that deliver exceptional adhesion to lithium disilicate and hybrid ceramics, supporting the global shift toward high-aesthetic restorations. The systems, packaged in automix syringe technology, enhance clinical efficiency and precision application.

Swiss R&D centers are spearheading studies on hydrolytic degradation resistance and polymer matrix durability, ensuring superior long-term stability in adhesive restorations. The country also acts as a strategic distribution hub for multinational dental manufacturers, facilitating rapid international rollout of adhesive product innovations.

Switzerland’s emphasis on premium-quality engineering, coupled with its role as a global exporter of high-performance bonding systems, strengthens its reputation as a center for advanced dental materials science.

Brazil is emerging as a key hub for dental adhesive consumption and innovation within Latin America, supported by its large population of dental professionals and high procedural volume. The market’s rapid growth is underpinned by domestic production of cost-competitive total-etch and self-etch adhesive systems, ensuring accessibility across public and private dental sectors.

Brazilian research institutions play a significant role in global adhesive performance studies, particularly in bond durability and ethanol-wet bonding techniques. Local manufacturers have developed efficient production chains catering to both domestic demand and exports across neighboring countries, positioning Brazil as a regional supply center for affordable, reliable dental bonding solutions.

South Korea’s dental adhesive market is thriving on its global leadership in cosmetic and aesthetic dentistry, where ultra-clear and color-stable resin cements are in high demand for all-ceramic restorations. Korean manufacturers are pioneering 7th and 8th-generation bonding agents, combining simplicity, high bond strength, and extended working times.

Innovation in delivery systems, including unit-dose capsules and smart applicators, ensures precise dispensing and consistent results, addressing common clinical challenges. Additionally, South Korean producers are broadening their export footprint across Asia-Pacific and Middle Eastern markets, offering competitive pricing and advanced adhesive chemistries.

With growing emphasis on esthetic precision and clinical efficiency, South Korea has established itself as a key exporter of next-generation dental adhesives, bridging the gap between advanced technology and affordability.

Dental Adhesive Market Report Scope

Dental Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.4 Billion

|

|

Market Size (2034)

|

$3.6 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Restorative Adhesives, Resin Cements, Glass Ionomer and Resin-Modified Glass Ionomer Cements, Denture Adhesives), By Application (Direct Restorations, Indirect Restorations, Pit and Fissure Sealants, Orthodontic Bonding, Denture Stabilization and Retention, Desensitizing/Sealing), By End-User (Dental Clinics and Hospitals, Dental Laboratories, Academic and Research Institutes, Retail Pharmacies and E-commerce

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Dentsply Sirona Inc., Ivoclar Vivadent AG, Kuraray Noritake Dental Inc., GC Corporation, VOCO GmbH, Ultradent Products, Inc., Kerr Corporation, Tokuyama Dental Corporation Inc., Shofu Inc., Procter & Gamble Co., GlaxoSmithKline plc, Coltene Whaledent AG, Bisco Inc., Prevest Denpro Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Restorative Adhesives

- Resin Cements

- Glass Ionomer and Resin-Modified Glass Ionomer Cements

- Denture Adhesives

By Application

- Direct Restorations

- Indirect Restorations

- Pit and Fissure Sealants

- Orthodontic Bonding

- Denture Stabilization and Retention

- Desensitizing/Sealing

By End-User

- Dental Clinics and Hospitals

- Dental Laboratories

- Academic and Research Institutes

- Retail Pharmacies and E-commerce

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- 3M Company

- Dentsply Sirona Inc.

- Ivoclar Vivadent AG

- Kuraray Noritake Dental Inc.

- GC Corporation

- VOCO GmbH

- Ultradent Products, Inc.

- Kerr Corporation

- Tokuyama Dental Corporation Inc.

- Shofu Inc.

- Procter & Gamble Co.

- GlaxoSmithKline plc

- Coltene Whaledent AG

- Bisco Inc.

- Prevest Denpro Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Dental Adhesive Market with analysis reviews that connect clinical performance, workflow efficiency, and regulatory readiness across restorative and prosthetic bonding. It highlights engineering breakthroughs in universal (multi-mode) adhesives, radiopaque layers that aid diagnosis, and hydrolysis-resistant monomer systems that sustain durable enamel–dentin interfaces, while assessing chairside delivery innovations that cut waste and reduce post-operative sensitivity. The study benchmarks suppliers on bond strength consistency, polymerization reliability, and substrate versatility for CAD/CAM and implant workflows, mapping adoption hurdles and cost-of-care impacts for high-volume practices. Built for evidence-driven decisions, this report is an essential resource for dentists, prosthodontists, clinic owners, dental lab managers, procurement leaders, and product strategists seeking clinically proven, time-saving bonding solutions.

Scope Highlights

Segmentation:

- By Product Type: Restorative Adhesives; Resin Cements; Glass Ionomer & Resin-Modified Glass Ionomer Cements; Denture Adhesives.

- By Application: Direct Restorations; Indirect Restorations; Pit & Fissure Sealants; Orthodontic Bonding; Denture Stabilization & Retention; Desensitizing/Sealing.

- By End-User: Dental Clinics & Hospitals; Dental Laboratories; Academic & Research Institutes; Retail Pharmacies & E-commerce.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historical data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analyses/profiles covering strategy, pipelines, key launches, and regional presence.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.