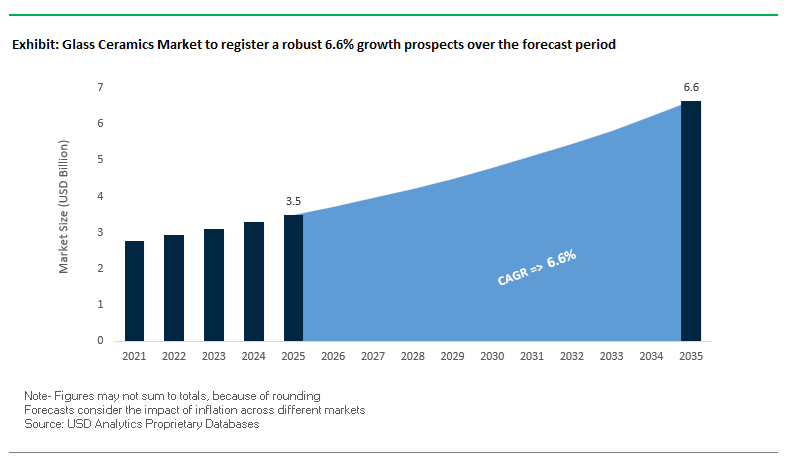

The global glass ceramics market is projected to grow from USD 3.5 billion in 2025 to USD 6.6 billion by 2035, reflecting a healthy CAGR of 6.6%. The steady growth is underpinned by the unique combination of zero thermal expansion, high flexural strength, biocompatibility, and extreme heat resistance, which makes glass ceramics indispensable in astronomy, semiconductor packaging, dental restorations, cooktops, and high-temperature industrial equipment.

The glass ceramics market is moving into a new phase of application diversification and performance specialization, driven by aerospace, semiconductor, solar, and dental innovation. In November 2025, SCHOTT AG launched SCHOTT™ Solar Glass exos, a high-performance cover glass tuned to a CTE of 6.9×10⁻⁶ K⁻¹ for GaAs solar cells, explicitly targeting next-generation satellite constellations. The highlights how glass ceramics and advanced glass are becoming central to space-grade power systems, where CTE matching and radiation resistance are essential for long mission lifetimes. In September 2025, SCHOTT further showcased its expanded portfolio of TTV-reduced glass carrier wafers at SEMICON Taiwan, following its early-2025 acquisition of QSIL GmbH. The combination of new product launches and M&A signals a strong strategic push into advanced IC packaging, where ultra-flat, stable glass and glass-ceramic carriers support high-density 3D chip stacking.

The dental glass ceramics segment is also evolving rapidly in line with digital dentistry and chairside workflows. In July 2025, Ivoclar Vivadent expanded its range of CAD/CAM blocks for lithium disilicate restorations, specifically targeting faster crystallization cycles to reduce in-office processing times. For dental labs and clinics, the translates into higher throughput, reduced chair time, and improved patient experience, reinforcing lithium disilicate’s position as the premium material for esthetic, metal-free crowns and veneers. On the consumer electronics front, Corning’s Q3 2025 announcement of USD 4.27 billion in core sales, with its Specialty Materials segment (including glass-ceramic Gorilla® lines) driving margins toward a 20% target by Q4 2025, underscores the strong adoption of glass-ceramic cover materials in smartphones, wearables, and tablets. The market sees glass ceramics as a route to combining thinness, scratch resistance, and controlled crystallization for enhanced drop performance.

In parallel, AGC Inc. is reinforcing the role of specialty glass and glass-ceramic technologies in emerging optics and AR/MR devices. Winning a CES 2025 Innovation Award in November 2024 for its M100/200 series glass substrates for AR/MR glasses, AGC demonstrates the importance of high refractive index and flatness for immersive optics and waveguides. Although these substrates are often pure glass rather than fully crystallized glass ceramics, they share similar production complexity and drive investments in coating, polishing, and surface engineering that also benefit glass-ceramic product lines. Meanwhile, SCHOTT’s August 2025 expansion of syringe and cartridge tubing production in India—while centered on high-purity borosilicate—shows that global capacity for precision specialty glass is being scaled up, ensuring robust supply chains and process capabilities that can be leveraged across glass and glass-ceramic platforms for medical, semiconductor, and industrial customers. Overall, these developments collectively reinforce a glass ceramics market narrative centered on precision, reliability, and cross-industry convergence.

For industry professionals and buyers, key questions today center on which glass-ceramic formulations can deliver the required dimensional stability, mechanical performance, and regulatory compliance while remaining cost-effective and scalable for series production. Lithium aluminosilicate (LAS), lithium disilicate (LS2), and β-spodumene-based glass ceramics are increasingly becoming the workhorse materials for telescope mirrors, metrology systems, CAD/CAM dental blocks, and furnace components, with suppliers differentiating through advanced processing, lower TTV, and robust quality standards (e.g., ISO 10993 for biocompatibility).

From the performance standpoint, LAS-based zero-CTE glass ceramics including ZERODUR™ enable mirror systems and metrology platforms to maintain dimensional changes of less than ±0.02×10⁻⁶/K between 0°C and 50°C, a level of stability that batch-fabricated optical glass or metals cannot achieve. In the dental sector, lithium disilicate glass ceramics with flexural strengths in the 370–420 MPa range are standard for posterior crowns and small FPDs, delivering a combination of aesthetics and durability that directly competes with metal-ceramic systems. Further, glass-ceramic wafers and carrier substrates with TTV values below 1 μm are becoming central to advanced semiconductor packaging and 3D integration, while heat-resistant glass ceramics capable of continuous operation up to 850°C support cooktops and LCD/semiconductor furnace linings. For OEMs, the sourcing decision increasingly revolves around suppliers that can guarantee tight process tolerances, stable CTE matching, and proven biocompatibility, backed by reliable global supply chains.

- Ultra-stable zero-CTE optics: LAS glass ceramics (e.g., ZERODUR™) achieve near-zero thermal expansion (≈±0.02×10⁻⁶/K from 0–50°C), enabling ultra-precise astronomy mirrors and metrology platforms.

- High-strength dental materials: Lithium disilicate glass ceramics deliver flexural strengths of roughly 370–420 MPa, supporting durable all-ceramic crowns and bridge restorations.

- Advanced packaging substrates: Glass-ceramic carrier wafers used in semiconductor packaging typically require TTV < 1 μm, supporting high-yield 3D stacking and fan-out packaging.

- Extreme heat applications: β-spodumene-based glass ceramics including NEOCERAM™ withstand continuous service up to 850°C, ideal for cooktops and harsh industrial furnace environments.

- Certified biocompatibility: Medical and dental glass ceramics designed with apatite or leucite phases are engineered to meet ISO 10993 biocompatibility requirements, ensuring non-cytotoxic interaction with oral and biological tissues.

High-Precision Electronics Demand and Energy-Efficient Material Engineering Driving Innovation in the Glass Ceramics Market

Trend 1 - Glass Ceramics Become the Premium Standard for Scratch-Resistant, High-Durability Smartphone and Smartwatch Covers

Demand for ultra-premium device durability is driving global OEMs to shift from traditional aluminosilicate glass to specialized glass ceramics-often marketed under brand names such as ceramic shield or crystalline glass. These engineered materials offer stronger scratch resistance, higher toughness, and improved drop resilience.

Technical performance data from leading suppliers show that advanced glass ceramics achieve Vickers hardness values up to 660 kgf/mm², outperforming conventional aluminosilicate covers, which typically range between 590–650 kgf/mm². This improvement directly enhances scratch protection for wearables and flagship mobile devices-a critical differentiator in the premium consumer electronics segment.

Glass ceramics also demonstrate significant gains in fracture toughness, with top-performing compositions reaching 1.15 MPa·m⁰·⁵, compared with 0.7–0.8 MPa·m⁰·⁵ for conventional strengthened glass. This increase in toughness correlates with better drop performance and reduced breakage in everyday use.

Manufacturers accept a small density increase-~2.48 g/cm³ vs. ~2.41 g/cm³ in aluminosilicate glass-as a deliberate engineering trade-off to achieve superior durability. For wearables, flexible glass-ceramic variants provide an optimal balance of surface hardness, thinness, and bend tolerance, enabling their integration into curved smartwatch displays without compromising premium feel or structural integrity.

Trend 2 - Ultra-Low Expansion Glass Ceramics Become Mission-Critical for EUV Lithography & Space Telescope Optics

Next-generation semiconductor fabrication and astronomical imaging rely on materials that offer extreme dimensional stability, a requirement fulfilled almost exclusively by ultra-low expansion (ULE) glass ceramics.

Substrates such as Schott ZERODUR® and Ohara CLEARCERAM®-Z achieve near-zero Coefficient of Thermal Expansion (CTE) values-0 ± 0.007 × 10⁻⁶/K between 0–50°C. In EUV lithography, this stability ensures that masks used for 5 nm and sub-5 nm nodes maintain nanometer-scale flatness, with allowed length changes of <0.01 nm per meter, even under fluctuating thermal loads.

For large astronomical mirrors-such as those used in the Extremely Large Telescope (ELT)-ULE glass ceramics offer both thermal stability and exceptional homogeneity. ZERODUR blanks of up to 18 tons exhibit homogeneity tolerances below 0.03 × 10⁻⁶/K, ensuring uniform optical performance across the full segmented mirror array.

Mechanical rigidity is equally critical. With a Young’s modulus of ~90.3 GPa, glass ceramics maintain shape under gravitational loading and dynamic forces, preserving optical precision in space telescopes, Earth observation systems, high-power laser platforms, and metrology instruments.

Opportunity 1 - Glass Ceramics as High-Temperature Sealing Materials for Solid Oxide Fuel Cells (SOFCs) & Green Hydrogen Electrolyzers

The global transition to a hydrogen-based energy infrastructure is creating a breakthrough opportunity for glass-ceramic sealants, which are indispensable for the commercialization of Solid Oxide Fuel Cells (SOFCs) and high-performance electrolyzers.

Research from Pacific Northwest National Laboratory (PNNL) confirms that engineered glass-ceramic formulations maintain hermetic bonding for over 4,000 hours at up to 950°C, demonstrating durability suitable for the targeted 50,000–75,000 hour service lifetimes of stationary SOFCs.

A key technical advantage is the ability to tune glass ceramics’ thermal expansion coefficient to match both ceramic cell components and metallic interconnects-typically within ±1 ppm/K. This alignment is essential to survive frequent thermal cycling between 600–900°C, preventing delamination or cracking during startup and shutdown cycles.

Unlike amorphous glass sealants, the crystalline phases in glass ceramics provide resistance to creep and viscous flow, ensuring that seals maintain mechanical integrity and prevent mixing of fuel and oxidant gases-both critical for system efficiency and safety.

These capabilities position glass ceramics as one of the most strategically important material classes for the scaling of green hydrogen technologies, SOFC micro-CHP systems, and industrial decarbonization initiatives.

Opportunity 2 - Tailored Radiative Cooling Glass-Ceramics for Energy-Efficient Building Envelopes & Automotive Coatings

A high-value innovation opportunity is emerging through the engineering of glass ceramics with spectrally selective emissivity and reflectivity for passive radiative cooling applications. These next-generation glass-ceramic coatings can significantly reduce HVAC loads in buildings and thermal stress in vehicles and electronics.

Effective radiative cooling requires high emissivity in the 8–13 μm atmospheric transparency window. Research demonstrates emissivity values up to 0.97 in engineered glass-ceramic matrices, enabling efficient heat dissipation into outer space.

Daytime cooling additionally requires high solar reflectance. Advanced radiative cooling coatings integrated into glass ceramics have achieved reflectivity levels of up to 0.95 across the 0.3–2.5 μm solar spectrum, minimizing heat absorption under direct sun.

Real-world applications confirm meaningful energy savings: experimental installations on building roofs reduced monthly cumulative cooling demand by 18.5–40.5 kWh/m², depending on climate and substrate type. Measured mid-day temperature reductions of up to 7.8°C below ambient under solar radiation intensities of ~640 W/m² validate the material’s performance potential.

These engineered glass ceramics offer transformative benefits for cool roofing systems, building façades, EV body panels, transportation infrastructure, and high-temperature industrial enclosures, positioning them as a major innovation frontier in sustainable materials engineering.

Glass Ceramics Market Share Analysis

Market Share by Type of Composition: Lithium Aluminosilicate Leads Through Near-Zero CTE, High Thermal Stability, and IR-Optimized Performance

Lithium Aluminosilicate (LAS) glass ceramics command the largest 45% share in the Glass Ceramics Market, driven by their unmatched thermal properties, which make them indispensable for high-temperature and thermal-shock–prone environments. The defining advantage of LAS compositions is their near-zero—or even slightly negative—Coefficient of Thermal Expansion (CTE), typically ranging from −86×10⁻⁷/°C to +9×10⁻⁷/°C, depending on the crystallization phase. This near-zero expansion is central to LAS dominance because it ensures the glass ceramic does not experience dimensional changes during sudden thermal transitions, preventing catastrophic cracking that traditional glass surfaces often suffer when moved from extreme heat to cold exposure. LAS materials also deliver exceptional high-temperature endurance, supporting continuous operation up to 950°C, which is essential for cooktops, high-power heating systems, and industrial furnace inspection windows. An additional competitive advantage is LAS’s engineered capability to allow infrared radiation transmission, losing only 15–20% of IR energy while enabling efficient heat transfer in radiant and halogen cooktop systems. This combination of thermal-shock resistance, temperature endurance, and functional IR transparency firmly positions LAS glass ceramics as the most technologically critical and commercially dominant composition class.

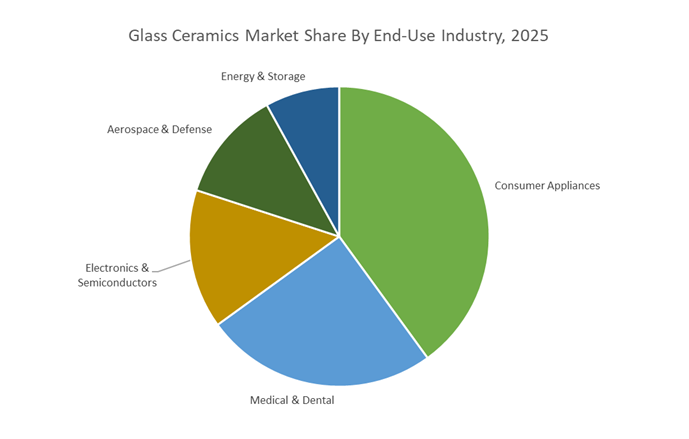

Market Share by End-Use Industry: Consumer Appliances Dominate Through High-Volume Cooktop Adoption and Aesthetic Durability Requirements

Consumer Appliances hold a commanding 40% share of the Glass Ceramics Market, primarily because LAS-based glass ceramic components have become the global standard for ceramic cooktops, induction surfaces, and oven door panels. Cooktop applications alone drive massive consumption volumes, as millions of new residential appliances integrate LAS glass ceramic panels each year, making this the single largest recurring use case for the material. The segment’s leadership is reinforced by the dual benefits LAS provides: enhanced energy efficiency and elevated aesthetic durability. In radiant and induction cooking systems, LAS’s low thermal conductivity allows rapid heating of the cookware zone while keeping surrounding areas cool, markedly improving heat transfer efficiency and user safety. Its high Vickers hardness (~7 GPa) delivers outstanding scratch resistance—superior to many metal surfaces—ensuring longevity despite daily kitchen abrasion. Coupled with its non-porous, chemically resistant, easy-to-clean finish, LAS glass ceramics support the modern consumer preference for sleek, minimalist, high-performance appliance design. As global residential upgrades, smart kitchen adoption, and premium appliance sales continue accelerating, the heavy integration of LAS panels in consumer appliances solidifies this segment as the dominant driver of market share in glass ceramics.

Country Analysis: Global Glass Ceramics Development Hubs

Germany: High-Performance Glass-Ceramic Innovation Strengthened by Circular Economy and Semiconductor Packaging Leadership

Germany continues to lead the global glass ceramics market through its advanced industrial ecosystem, strong specialty glass manufacturing base, and national commitment to decarbonizing energy-intensive industries. As home to SCHOTT AG, one of the most influential players in specialty glass and glass ceramics, Germany remains at the forefront of product innovation and circular manufacturing. In November 2025, SCHOTT achieved a major milestone by successfully remelting externally collected shards from used glass-ceramic cooktops, validating the feasibility of a circular economy model for high-performance glass-ceramic waste streams—traditionally considered extremely challenging to recycle due to material crystallinity. This breakthrough positions Germany as a leader in sustainable high-tech materials and aligns closely with Europe’s push for closed-loop manufacturing systems.

Germany is also strengthening its global leadership in semiconductor packaging materials. At SEMICON Taiwan 2025, SCHOTT showcased advanced glass-ceramic carrier wafers and panel substrates engineered for ultra-low Total Thickness Variation (TTV)—a critical performance metric in advanced semiconductor packaging and heterogeneous integration. To expand its capabilities even further, SCHOTT acquired QSIL GmbH Quarzschmelze Ilmenau in 2025, reinforcing its portfolio in high-purity fused silica and ceramics essential for next-generation microelectronics. The country’s research landscape is equally dynamic: the Fraunhofer IKTS is driving development of glass-like and ceramic solid electrolytes for solid-state batteries, emphasizing high ionic conductivity, non-flammability, and superior thermal stability—key enablers for next-generation EV energy storage.

Germany’s policy environment accelerates innovation and manufacturing transitions. SCHOTT is actively urging European policymakers to create supportive frameworks for separate collection of specialty glass, enabling scalable recycling pathways for glass-ceramic products. Meanwhile, the federal government’s “Climate Protection Contracts” program is injecting substantial financial support into energy-intensive glass manufacturing. A leading example is the €382.8 million climate grant awarded to Saint-Gobain Glass Deutschland GmbH in October 2024, reinforcing national backing for decarbonized production technologies. With its combined strengths in materials science, semiconductor packaging, energy storage innovation, and sustainability leadership, Germany remains the most influential hub in the global glass ceramics market.

United States: Advanced Packaging, Specialty Materials Expansion, and High-Precision Aerospace Glass Ceramics

The United States plays a pivotal role in the global glass ceramics market through its strong emphasis on high-growth electronics, advanced packaging technologies, and aerospace-grade glass-ceramic innovation. Corning Incorporated, a cornerstone of U.S. specialty materials capability, is executing its multiyear “Springboard” business expansion plan. By 2026, Springboard is expected to generate over $4 billion in new annualized sales, driven by surging demand for specialty materials used in generative AI infrastructure, data centers, advanced optics, and precision electronic packaging. This includes glass-ceramics engineered for high thermal stability and low dielectric loss—materials increasingly essential for high-frequency telecommunications and high-power computing devices.

In defense and aerospace applications, U.S. manufacturers remain unmatched. Corning’s ULE® (Ultra-Low Expansion) glass-ceramic mirror substrates continue to serve as foundational components for major telescopes, satellite optics, and spaceborne imaging systems. Their near-zero thermal expansion coefficient ensures dimensional stability under extreme temperature variations, making them indispensable for mission-critical aerospace applications. Simultaneously, U.S. R&D initiatives are focusing on next-generation glass-ceramic composites for 5G and 6G electronic substrates, engineered to offer low dielectric constants, low dielectric loss, and coefficient-of-thermal-expansion (CTE) matching with silicon. These properties are vital for enabling multi-GHz signal integrity, chiplet architectures, and advanced RF packaging. With strong capital investment, leadership in specialty materials, and cross-sector demand from AI, telecom, and aerospace, the U.S. is a central engine for glass-ceramic market growth.

Japan: Precision Glass-Ceramic Manufacturing Supporting Global Display, Appliance, and Optical Component Supply Chains

Japan maintains one of the world’s most sophisticated glass ceramics manufacturing ecosystems, anchored by companies like Nippon Electric Glass (NEG), which are critical suppliers of high-purity specialty glass and glass-ceramic substrates used in advanced displays, consumer appliances, semiconductor equipment, and optical devices. NEG’s portfolio spans precision-engineered substrates for high-resolution displays, ultra-clean materials for optical communications, and durable glass-ceramic components for household appliances such as induction cooktops—segments where consistency, chemical durability, and dimensional stability are essential.

In June 2025, NEG announced the closure of a subsidiary in the U.K. as part of its structural business reform, signaling a strategic consolidation around its highest-value specialty glass and glass-ceramic segments. This restructuring highlights Japan’s focus on quality-driven production rather than volume-driven competition. Japanese manufacturers also remain indispensable suppliers of glass-ceramic components for optical and electronic applications, including precision housings, protective windows, and hermetic components. With its unwavering commitment to precision, high reliability, and process stability, Japan continues to be a global linchpin for advanced glass-ceramic technologies across electronics, displays, and industrial systems.

China: Rapid Scale-Up of TGV and High-Density Glass-Ceramic Packaging for Semiconductors

China is emerging as a formidable competitor in the glass ceramics and advanced packaging sectors, driven by strong government support for semiconductor self-sufficiency and rapid domestic innovation in Through-Glass Via (TGV) and high-density interposer technologies. Chinese TGV developers—including 3D CHIPS and Sky Semiconductor—are advancing capabilities at an accelerated pace. Sky Semiconductor’s breakthrough in 4-micron via diameter technology, along with mastery of 2.5D high-density glass interposers reported in 2024, demonstrates China’s growing ability to compete with global leaders in advanced packaging substrates.

Major display manufacturer BOE is also entering the semiconductor packaging domain. With an 8-inch pilot line for TGV-based panel-level packaging, BOE has achieved meaningful progress in high aspect-ratio TGV formation and 3D interconnect density, targeting mass production after 2026. These developments are tightly aligned with Chinese industrial policy, which prioritizes glass core substrates, glass interposers, and advanced packaging materials as critical enablers for AI acceleration hardware, high-performance computing (HPC), and 5G/6G communications. As China scales both production capacity and process capabilities, it is becoming a major growth engine for next-generation glass-ceramic substrates in the global semiconductor value chain.

Competitive Landscape: Leading Glass Ceramics Manufacturers and Strategic Positions

The global glass ceramics market is concentrated among a set of specialized materials companies that combine deep glass science expertise, precision manufacturing, and strong application engineering. These players are not just supplying commodity glass; they are co-developing advanced materials and tailored glass-ceramic systems for astrophysics, semiconductor packaging, dental CAD/CAM, mobile devices, cooktops, and architectural fire protection. Their competitive advantage hinges on proprietary compositions, zero-CTE engineering, tightly controlled crystallization processes, and highly automated finishing lines capable of delivering ultra-flat, low-defect substrates at scale. Strategic moves including targeted acquisitions, capacity investments, and digital dentistry integration are reshaping how glass ceramics are specified and qualified in high-value end markets.

SCHOTT AG positions itself at the high end of the glass ceramics market with flagship brands including ZERODUR™ for zero-CTE optics and CERAN™/ROBAX™ for high-temperature cooktops and fireplace panels. ZERODUR is the material of choice for large telescope primary mirrors and metrology platforms, thanks to its near-zero thermal expansion and ability to maintain dimensional stability over large apertures and temperature swings. SCHOTT’s strategy is to couple the materials expertise with deeper penetration into semiconductor advanced packaging and specialty optics. The early 2025 acquisition of QSIL GmbH and the September 2025 showcase of TTV-reduced glass carrier wafers at SEMICON Taiwan reflect a deliberate push to supply glass and glass-ceramic carriers with sub-micrometer TTV for 3D IC integration. In parallel, the November 2025 launch of SCHOTT™ Solar Glass exos for GaAs solar cells underscores its move into space-grade power applications, reinforcing its status as a technical and commercial leader in high-performance glass ceramics.

Corning is a key competitor in glass-ceramic cover materials and specialty substrates, leveraging its proprietary Fusion Manufacturing Process to produce ultra-flat glass precursors that are subsequently crystallized and ion-exchanged. Its Gorilla® Glass Ceramic lines target smartphones, wearables, and other mobile devices where thinness, scratch resistance, and drop performance are critical. The company’s Specialty Materials segment—which includes these glass-ceramic offerings—was highlighted in Q3 2025 earnings as a major contributor to core sales of USD 4.27 billion and as central to achieving a 20% operating margin target by Q4 2025. Corning’s strategy is to integrate cover glass, glass-ceramic technology, and display substrates across form factors, from handheld devices to larger displays, combining optical clarity with controlled crystallization and strengthening. Its strong financial position and deep partnerships with leading OEMs make it a pivotal player in scaling glass ceramics for mass-market electronics.

Ivoclar Vivadent is a specialist in dental glass ceramics, with its IPS e.max™ lithium disilicate and zirconia-reinforced LiSi blocks forming the benchmark for esthetic, high-strength all-ceramic restorations. These materials offer flexural strengths in the 370–420 MPa range, guaranteeing long-term performance for crowns, veneers, inlays, and small FPDs under demanding occlusal loads. The company’s strategic focus is on digital dentistry integration, ensuring that IPS e.max is fully compatible with leading CAD/CAM workflows and chairside milling equipment. In July 2025, Ivoclar expanded its range of CAD/CAM blocks with formulations optimized for faster crystallization cycles, reducing processing time and enabling same-day restorative procedures. The commitment to workflow efficiency, coupled with compliance to ISO 10993 biocompatibility standards, positions Ivoclar as a critical partner for clinics and labs seeking reliable, esthetic glass-ceramic solutions.

Nippon Electric Glass (NEG) is a key provider of high-temperature glass ceramics, notably the NEOCERAM™ brand, which is engineered for continuous operation at temperatures up to around 850°C. These materials are widely used in cooktop panels, fireplace windows, and furnace components in LCD and semiconductor manufacturing, where thermal shock resistance and dimensional stability are non-negotiable. NEG’s strategic advantage lies in its ability to produce large-format, exceptionally flat substrates with stable thermal expansion properties, making them suitable for both consumer and industrial installations. Beyond domestic appliances, NEOCERAM and related glass-ceramic solutions serve as setter plates and furnace walls in electronics manufacturing, where they must withstand repeated thermal cycling. The company’s broader expertise in specialty thin glass complements its glass-ceramic portfolio, allowing NEG to serve customers across display, industrial, and thermal control applications.

AGC Inc. operates at the intersection of architectural fire protection, electronics, and advanced optics, offering specialized glass and glass-ceramic materials for demanding applications. In architectural markets, AGC supplies fire-resistant glass-ceramic products (e.g., Pyran™-type materials) that meet stringent E/EW fire codes, providing transparent fire barriers for façades, partitions, and doors. On the electronics and optics side, AGC is deeply involved in high-performance substrates for AR/MR glasses, recognized by its CES 2025 Innovation Award (announced in November 2024) for the M100/200 series, which combine high refractive index and flatness for immersive XR optics. The company’s strategy is to exploit the know-how across automotive displays, specialty glazing, and high-temperature glass-ceramic applications, aligning with trends in smart mobility and energy-efficient building envelopes. The diversified application footprint gives AGC a strong platform to grow within the global glass ceramics and specialty glass ecosystem.

Glass Ceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.5 Billion

|

|

Market Size (2035)

|

$6.6 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Type of Composition (Lithium Aluminosilicate, Lithium Disilicate, Alkali-Barium-Silicate, Fluorosilicate, NASICON-Type), By Application Function (Structural Components, Electronic Substrates, Optical Components, Biomaterials, Energy Storage), By Manufacturing Process (Controlled Crystallization, Sintering/Powder Processing, Micro-Structuring, Precision Machining/Polishing), By End-Use Industry (Consumer Appliances, Electronics & Semiconductors, Aerospace & Defense, Medical & Dental, Energy & Storage)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SCHOTT AG, Corning Incorporated, Nippon Electric Glass Co. Ltd., CoorsTek Inc., Saint-Gobain S.A., VITA Zahnfabrik, Kyocera Corporation, Heraeus Holding GmbH, 3D CHIPS (Chengdu Micro-Technology), BOE Technology Group Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Ceramics Market Segmentation

By Type of Composition

- Lithium Aluminosilicate (LAS)

- Lithium Disilicate

- Alkali-Barium-Silicate

- Fluorosilicate

- NASICON-Type

By Application Function

- Structural Components

- Electronic Substrates

- Optical Components

- Biomaterials

- Energy Storage

By Manufacturing Process

- Controlled Crystallization

- Sintering / Powder Processing

- Micro-Structuring

- Precision Machining / Polishing

By End-Use Industry

- Consumer Appliances

- Electronics & Semiconductors

- Aerospace & Defense

- Medical & Dental

- Energy & Storage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Glass Ceramics Manufacturers

- SCHOTT AG

- Corning Incorporated

- Nippon Electric Glass Co. Ltd.

- CoorsTek Inc.

- Saint-Gobain S.A.

- VITA Zahnfabrik

- Kyocera Corporation

- Heraeus Holding GmbH

- 3D CHIPS (Chengdu Micro-Technology)

- BOE Technology Group Co. Ltd.

*- List not Exhaustive