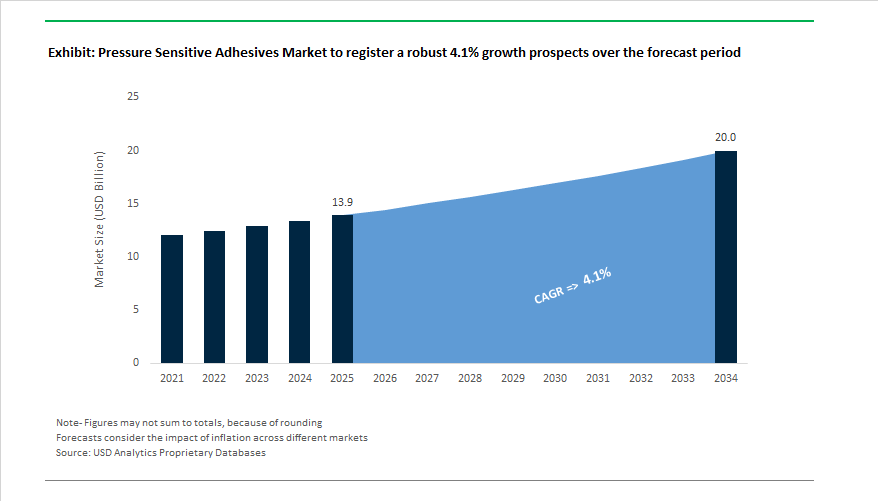

The Global Pressure Sensitive Adhesives (PSA) Market is projected to expand from USD 13.9 billion in 2025 to USD 20 billion by 2034, growing at a CAGR of 4.1%, as PSAs evolve from high-volume consumables into engineered materials tightly linked to sustainability, automation, and lightweight design strategies. Growth is increasingly shaped by how effectively PSA chemistries support regulatory compliance, line speed optimization, and multi-material integration across automotive, electronics, construction, and logistics-intensive industries.

From a technology standpoint, water-based PSA formulations are steadily gaining preference, reflecting tightening VOC and worker-exposure regulations across Europe, North America, and parts of Asia. Major producers such as Avery Dennison, 3M, tesa, and Arkema (Bostik) have expanded waterborne acrylic PSA portfolios specifically engineered to deliver high initial tack, clean removability, and long-term cohesion without solvent emissions. In parallel, acrylic-based PSAs continue to anchor the market because of their UV resistance, aging stability, and optical clarity, attributes critical for exterior automotive components, electronic displays, and transparent label constructions. These properties are increasingly specified at the OEM level, particularly where adhesive failure directly affects aesthetics, safety, or recyclability outcomes.

Labeling remains the structurally strongest application segment, but its value proposition has shifted. Growth is being reinforced by high-speed automated labeling, RFID integration, and cold-chain logistics, rather than simple FMCG expansion. PSA suppliers are responding with formulations optimized for low-temperature tack, high shear at elevated temperatures, and compatibility with recycled PET, HDPE, and paper substrates. Clean-removal and wash-off adhesive systems—commercialized by leading label-material suppliers—are increasingly required to meet design-for-recycling guidelines, positioning PSA selection as a determinant of packaging circularity rather than a downstream afterthought.

Automotive and transportation applications continue to represent the largest and most technically demanding end-use segment. PSAs are now routinely specified for interior trim bonding, wire harness fixation, NVH damping layers, battery insulation films, and sensor mounting, replacing mechanical clips and liquid adhesives to reduce weight and assembly complexity. OEM qualification programs increasingly emphasize creep resistance, vibration damping, and long-term thermal aging, areas where high-performance acrylic and rubber-modified PSA systems outperform lower-cost alternatives. This trend is particularly pronounced in electric vehicles, where reduced powertrain noise elevates the importance of rattle suppression and adhesive durability.

The Global Pressure Sensitive Adhesives Industry has entered a transformative phase, characterized by sustainability-driven product launches, regional capacity expansions, and strategic collaborations among leading players. The market is experiencing a surge in innovation across home-compostable PSAs, recyclable formulations, UV-curable systems, and industrial water-based technologies, each aligning with global decarbonization and performance enhancement goals.

In May 2025, Bio4Life made headlines with the introduction of BioTAK HC700, the industry’s first home-compostable and food-safe pressure-sensitive adhesive, certified under EN 13432 standards. This innovation marked a significant milestone in sustainable labeling, particularly for fresh produce and consumer packaging applications. Similarly, in April 2025, 3M Company launched its Scotch-Weld DP8000 Series, targeting the automotive lightweighting trend by offering structural adhesives with high bond strength and superior fatigue resistance.

Meanwhile, Mitsui Chemicals ICT Materia launched a water-based acrylic masking tape (January 2025) tailored for precision fiber laser cutting, emphasizing the growing adoption of PSAs in industrial and metal processing environments. Henkel’s August 2024 rollout of recyclable PSAs (Aquence PS 3017 RE) further advanced circular labeling systems, complementing TLMI-certified recycling processes. These moves are bolstered by Arkema’s July 2024 introduction of UV-curable PSAs, optimized for medical and electronic bonding, delivering rapid curing capabilities for high-throughput production lines.

On the strategic front, Sika AG’s June 2024 investment in a new manufacturing facility in Liaoning, China, enhanced its Asia-Pacific supply chain capacity, while its May 2024 collaboration with H.B. Fuller emphasized co-development of sustainable adhesive technologies. Further, 3M’s October 2024 launch of Fastbond™ PSA 1049 (PowerCore) demonstrated a shift toward solventless, high-performance bonding, reinforcing the company’s leadership in low-VOC industrial formulations.

Market Trend 1: The Automotive Industry’s Electrification Surge Catalyzes Demand for Functional and High-Performance PSAs

The global transition to electric vehicles (EVs) is fundamentally altering material engineering requirements, creating an entirely new class of functional pressure-sensitive adhesives designed for thermal management, weight reduction, and structural bonding. PSAs are emerging as key enablers of EV efficiency, performance, and safety, particularly in battery pack assembly, sensor integration, and component insulation.

Research drives the material significance of PSAs in EV battery thermal optimization. Studies on lithium-ion battery systems report that advanced thermal management enabled by functional PSA materials can achieve a 22% reduction in cooling subsystem energy consumption and a 37% improvement in thermal consistency, directly enhancing battery safety and service life. These results reinforce PSAs’ growing role in controlling thermal variance and managing the thermal runaway risk inherent to high-energy-density battery systems.

Within EV battery packs, high-precision die-cut PSA tapes are replacing metal fasteners and liquid adhesives. Their ability to conform to irregular surfaces, maintain electrical insulation, and accommodate cell expansion (“breathing”) during charge/discharge cycles makes them vital for compact, lightweight battery architectures. Specialized flame-retardant PSA tapes—often laminated with mica or ceramic layers—are also designed to meet UL 94 V-0 standards, slowing heat propagation between cells and providing an extra layer of fire protection.

In addition, PSA tapes are being engineered as functional safety barriers, capable of directing vent gases away from sensitive components during thermal events. The capability positions PSAs as critical safety materials within EV battery module and pack-level integration, supporting the sector’s shift to safer, lightweight, and fully electrified platforms.

Market Trend 2: Global Sustainability Mandates Accelerate the Shift Toward Bio-Based and Recyclable PSA Systems

As governments and brand owners align on circular economy goals, the PSA market is entering a pivotal phase of bio-based feedstock adoption and recycling compatibility reformulation. The move toward low-carbon, bio-derived, and separation-friendly adhesives is transforming how PSA tapes and labels are produced, applied, and recycled in global packaging and labeling systems.

Major adhesive manufacturers have begun introducing bio-based pressure-sensitive hot melt adhesives certified under the USDA BioPreferred program, reflecting a growing shift from petroleum-derived polymers to plant-based polyols, starches, and natural oils. For instance, recently commercialized BioBond™ adhesive systems demonstrate comparable performance to synthetic counterparts in terms of peel strength, tack, and temperature stability, marking a milestone in sustainable adhesive development.

R&D in the domain is heavily focused on improving thermal stability, water resistance, and cohesive strength of renewable PSAs to reach full technical parity with conventional solutions. Additionally, leading producers like Henkel and 3M are investing in the formulation of wash-off and recycling-compatible PSAs for labels on PET and HDPE bottles. These adhesive technologies are designed to detach cleanly during recycling, preventing contamination of post-consumer resin (PCR) streams and ensuring compliance with European Commission circular packaging standards.

The sustainability transition is not only regulatory—it’s also brand-driven. Over 80% of global consumer goods companies have announced targets for 100% recyclable or compostable packaging by 2030, making PSAs that support label separation, bio-content integration, and full recyclability essential for compliance with Extended Producer Responsibility (EPR) laws and global decarbonization mandates.

Market Opportunity 1: Next-Generation Electronics Assembly and Thermal Management Solutions

The evolution of high-density, miniaturized electronics—including smartphones, data center hardware, and AI processors—has created a lucrative new frontier for thermally conductive PSAs that deliver both heat dissipation and structural bonding performance. These materials function as Thermal Interface Materials (TIMs), replacing traditional thermal greases and mechanical components while streamlining high-speed automated assembly.

Recent product benchmarks indicate thermal conductive double-sided PSA tapes achieving conductivity up to 1.2 W/m·K, combined with dielectric strengths of up to 8.0 kV/mm—a specification vital for components such as LEDs, ICs, and power modules that demand simultaneous heat transfer and electrical insulation. Their rapid “instant bond” capability—measured in microseconds—significantly reduces assembly times compared to liquid-curing adhesives, enabling higher production throughput and precision control in surface-mount manufacturing.

These multifunctional PSAs also provide critical vibration damping, gap filling, and substrate compatibility benefits, allowing bonding of dissimilar materials like aluminum, glass, and flexible PCBs. As devices become thinner and more power-dense, the material versatility ensures structural integrity without mechanical stress points, supporting reliable high-speed electronics manufacturing and thermal management innovation in next-generation device architectures.

Market Opportunity 2: Expansion of Medical-Grade PSA Applications in Healthcare Wearables and Transdermal Delivery Systems

The intersection of healthcare and electronics is creating one of the most lucrative segments for the PSA market—biocompatible adhesives for medical wearables and drug delivery systems. The increasing adoption of Continuous Glucose Monitors (CGMs), biosensors, and microneedle patches is driving a new demand profile for PSAs that balance skin adhesion, moisture permeability, and patient comfort.

For skin-mounted wearables, PSAs must meet stringent Moisture Vapor Transmission Rate (MVTR) criteria—typically between 800 and 1,000 g/m²/24h—to prevent skin irritation while maintaining consistent adhesion during long-term wear. These materials are optimized for dynamic skin movement, sweat resistance, and temperature variations, ensuring device stability over 5 to 14-day wear periods.

In transdermal drug delivery applications, PSAs must exhibit chemical inertness to prevent any interaction with active pharmaceutical ingredients. Formulations are validated under ISO 10993 biocompatibility standards and engineered to maintain a consistent peel adhesion profile over multi-day usage while remaining compatible with gamma radiation and EtO sterilization processes.

Manufacturers in the segment are investing in medical-grade polyurethane and silicone-based PSAs that exhibit low cytotoxicity, rapid skin recovery after removal, and hypoallergenic performance. As digital therapeutics and connected medical devices expand globally, the convergence of electronics, materials science, and biocompatibility engineering will continue to position medical PSAs as one of the fastest-growing specialty adhesive submarkets worldwide.

Competitive Landscape: Global Leaders Driving Innovation in the Pressure Sensitive Adhesives Market

The competitive landscape of the Global Pressure Sensitive Adhesives Market is defined by a balanced mix of product diversification, regional expansions, and sustainability-oriented innovation. Leading companies such as Henkel, H.B. Fuller, Sika, Ashland Global Holdings, and 3M Company are continuously enhancing their PSA portfolios to meet stringent regulatory and performance demands across packaging, automotive, electronics, and medical applications.

Henkel remains the only global supplier offering a complete PSA chemistry portfolio — spanning solvent-acrylic, emulsion-acrylic, solvent-rubber, hot-melt rubber, and UV-curable systems (LOCTITE® DURO-TAK®, AQUENCE® PS, TECHNOMELT® PS). In 2025, the company’s strategic emphasis lies on supporting compliance with EU Packaging and Packaging Waste Regulation (PPWR) through wash-off and repulpable PSAs. Following its 2024 expansion in South Dakota (USA), Henkel has strengthened domestic production resilience for North American markets. Its medical and food-safe adhesive range also enhances its leadership in consumer safety and sustainability.

H.B. Fuller’s 2025 strategy underscores sustainability at the core of its innovation model, as showcased in its 2024 Sustainability Report. The company recently launched Swift®melt 1850, a bio-based hot melt PSA designed for eco-packaging applications, reducing fossil dependency and enabling recyclability. H.B. Fuller continues to expand globally, inaugurating a new plant in Cairo, Egypt, alongside eco-efficiency upgrades in Germany and the UAE. Its Ködispace 4SG insulating glass PSA technology exemplifies sustainable construction integration, enhancing thermal performance and durability in green buildings.

Under its Sika Strategy 2028, Sika AG emphasizes Innovation and Sustainability convergence, focusing on construction and automotive applications aligned with net-zero targets. The 2024 integration of MBCC Group expanded its product synergy, particularly in structural PSAs for digital infrastructure and data center bonding. Sika’s June 2024 joint venture on plastics recycling supports its circular economy objectives, ensuring closed-loop adhesive use in construction. The company continues to drive next-gen construction adhesives designed for durability and climate resilience.

Ashland Global Holdings leverages over five decades of medical PSA expertise, offering leading formulations such as Aroset™ (solvent acrylic), Arocure™ (UV-curable hotmelt), and Flexcryl™ (emulsion acrylic). Its dominance in transdermal delivery systems, ostomy care, and wound care adhesives highlights its specialization in non-cytotoxic and sterilization-resistant PSAs. In 2024, Ashland advanced water-based PSA technologies for labeling applications, addressing both performance and environmental sustainability demands.

A global leader in industrial and transportation PSAs, 3M continues to set industry standards in advanced materials science. Its Q4 2024 launch of Fastbond™ PSA 1049 with PowerCore technology positioned 3M at the forefront of solventless, water-based adhesive innovation. Focused heavily on EV battery assembly and high-performance tape manufacturing, 3M integrates safety, performance, and sustainability into its product pipeline. With its trusted brands Scotch-Weld and Fastbond, the company leads the transition toward efficient, low-labor, and environmentally responsible bonding systems.

Country Analysis: Regional Advancements in the Global Pressure Sensitive Adhesives (PSA) Industry

China: Rapid Expansion in High-Performance PSAs for Electronics, EVs, and E-commerce Packaging

China remains the largest global producer and consumer of Pressure Sensitive Adhesives (PSAs), anchored by its expansive manufacturing ecosystem spanning electronics, automotive, packaging, and flexible displays. The government’s industrial modernization programs and strong backing for semiconductor and electronic component manufacturing have dramatically increased demand for high-clarity, non-yellowing acrylic PSAs used in optical bonding and flexible display panels. The adhesive systems are crucial for OLED, micro-LED, and foldable device assembly, where thermal and chemical stability are key.

Environmental sustainability has become a cornerstone of China’s PSA industry evolution. Domestic and international manufacturers are scaling up water-based PSA production capacity to meet stringent VOC emission controls introduced under the nation’s latest Green Manufacturing Initiative. Simultaneously, the booming electric vehicle (EV) sector—underpinned by China’s aggressive electrification targets—is spurring innovation in high-temperature PSA tapes designed for battery cell-to-module bonding, insulation, and thermal management. The nation is also prioritizing bio-based and recyclable PSA development, particularly for FMCG and e-commerce packaging, as logistics demand surges in tandem with cross-border trade. New national eco-packaging standards, introduced in 2024, further reinforce China’s shift toward sustainable, low-VOC adhesive formulations, positioning it as the leading hub for eco-innovative and high-performance PSA materials in the Asia-Pacific region.

United States: Pioneering Sustainable and High-Performance PSA Solutions for Automotive, Medical, and Industrial Applications

The United States PSA market leads in technological sophistication and sustainability, driven by heavy R&D investment across automotive, healthcare, packaging, and electronics. Leading American adhesive producers are advancing silicone PSA technologies engineered for ADAS (Advanced Driver-Assistance Systems) sensors and EV components, delivering exceptional durability under extreme temperature and vibration conditions. Simultaneously, the EPA’s tightening of VOC regulations—coupled with California’s CARB directives—has accelerated the market-wide shift toward radiation-cured and water-based PSA systems, drastically reducing solvent dependency while maintaining performance standards.

In the healthcare and medical device space, U.S. firms are expanding portfolios of biocompatible and breathable medical-grade PSAs, particularly for wearable sensors, wound dressings, and transdermal drug delivery systems. The innovations combine skin-friendly adhesion with controlled peel strength for long-term comfort and efficacy. The packaging sector is witnessing large-scale investments in Hot Melt PSA (HMPSA) capacity, particularly for tamper-evident and security labeling applications in logistics and consumer goods. Further supporting the circular economy, major U.S. chemical companies are forming recycling-focused partnerships to develop wash-off and de-inking PSA technologies, aimed at improving paper and plastic recyclability.

Germany: Engineering Precision and Sustainable Chemistry Drive the European PSA Market

Germany stands as Europe’s most advanced market for Pressure Sensitive Adhesives, spearheading innovation in lightweight automotive bonding, industrial engineering, and circular chemistry. Major PSA suppliers are working closely with premium German automotive OEMs to develop high-strength acrylic foam tapes (AFT) for multi-material bonding in electric vehicle (EV) assembly, effectively replacing traditional welding methods. The bonding solutions not only enhance crash performance but also contribute to vehicle lightweighting and energy efficiency.

Germany’s leadership in sustainability is further solidified by the EU Ecodesign for Sustainable Products Regulation (ESPR), effective mid-2024, which is catalyzing the shift to solvent-free, water-borne, and bio-attributed PSAs. The country’s adhesive manufacturers are heavily investing in UV-curable PSA technologies that deliver instant curing and high line speeds for industrial applications, boosting productivity while minimizing energy consumption. Major facility modernization projects are underway to improve solvent recovery systems and energy efficiency in PSA tape coating lines, aligning with Germany’s carbon neutrality targets. Additionally, ongoing collaborations between R&D institutions and chemical companies are enhancing smart PSA systems that integrate real-time performance monitoring and predictive analytics, setting new standards for precision-engineered, sustainable adhesive technologies within the European market.

Japan: Global Leader in Optically Clear and High-Precision Electronic Adhesives

Japan continues to dominate the high-specification PSA segment, especially in consumer electronics, optical devices, and display technologies. The country’s adhesive manufacturers are recognized globally for producing Optically Clear Adhesives (OCA) with unmatched clarity, durability, and UV resistance—key components in OLED, micro-LED, and foldable display assemblies. Japanese firms are also pioneering ultra-thin, high-tack transfer adhesives, enabling precision bonding for miniaturized electronics, where micrometer-level uniformity and low thermal stress are critical.

In industrial and electronic insulation applications, Japan leads in high-temperature polyimide-based PSA tapes with silicone formulations, capable of withstanding extreme heat and voltage in electrical and industrial environments. The nation’s focus on precision and reliability extends to robotics and automotive manufacturing, where PSAs are used for sensor bonding, EMI shielding, and battery module sealing. With ongoing innovation in nanostructured adhesive chemistry and smart material integration, Japan’s PSA industry continues to set the global benchmark for quality, miniaturization, and optical performance.

India: Fast-Expanding PSA Market Driven by E-commerce and Infrastructure Development

India’s Pressure Sensitive Adhesives market is witnessing rapid growth fueled by e-commerce logistics, packaging, and infrastructure modernization. The nation’s thriving FMCG and retail sectors are driving record demand for low-cost, water-based acrylic PSAs used in labels, BOPP packaging tapes, and security sealing products. The rise of digital retail platforms has positioned India as one of the world’s largest consumers of commodity PSA tapes, prompting both domestic and multinational producers to expand manufacturing and distribution capacity across the country.

The Indian government’s “Make in India” initiative has played a pivotal role in attracting foreign direct investment (FDI) to establish new PSA manufacturing plants tailored for automotive, construction, and electronics applications. Major chemical multinationals have also launched application laboratories in India to customize PSA formulations for local climatic conditions and substrate variations. Additionally, rapid urban infrastructure growth, supported by smart city and highway development programs, has spurred demand for duct tapes, reflective safety tapes, and hazard barrier PSA products. Combined with the country’s strengthening manufacturing ecosystem and growing emphasis on eco-friendly adhesive systems, India is emerging as a global production and export hub for PSA materials.

South Korea: Technological Pioneer in Conductive and Thermal Management PSA Systems

South Korea has established itself as a global innovation center for advanced Pressure Sensitive Adhesives, particularly for flexible electronics, displays, and electric vehicle batteries. The country’s leadership in smartphone and OLED display manufacturing has spurred intensive R&D in next-generation Optically Clear Adhesives (OCA) with improved flexibility, transparency, and durability. Korean adhesive manufacturers are also focusing on thermally conductive and electrically insulating PSA tapes, essential for battery module assembly and thermal management in EVs and hybrid vehicles.

Government-backed initiatives supporting the Hydrogen Economy have created new research pathways for PSA formulations used in fuel cell stack sealing and composite bonding. Meanwhile, the drive toward smart factory automation and green chemistry has led to widespread adoption of solvent-free silicone PSAs, offering high resistance to temperature extremes and harsh chemicals. With a mature electronics ecosystem and export-oriented production base, South Korea continues to lead the global PSA market in innovation for flexible display, energy, and high-tech applications.

Pressure Sensitive Adhesives Market Report Scope

Pressure Sensitive Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.9 Billion

|

|

Market Size (2034)

|

$20 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Adhesive Chemistry (Acrylic, Rubber, Silicone, Polyurethane, Ethylene-Vinyl Acetate, Others), By Technology (Water-Based, Solvent-Based, Hot Melt, Radiation Cured), By Product (Tapes, Labels, Graphic Films, Other Products), By End-Use Industry (Packaging, Automotive & Transportation, Medical & Healthcare, Electrical & Electronics, Building & Construction, Consumer Goods, Others), By Substrate (Paper & Cardboard, Plastics, Metal, Glass, Foam, Fabrics & Textiles, Nonwovens, Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Henkel AG & Co. KGaA, H.B. Fuller Company, Avery Dennison Corporation, tesa SE, Arkema Group (Bostik), The Dow Chemical Company, Nitto Denko Corporation, Sika AG, Ashland Global Holdings Inc., Momentive Performance Materials Inc., Wacker Chemie AG, DIC Corporation, LG Chem Ltd., Shin-Etsu Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Adhesive Chemistry

- Acrylic

- Rubber

- Silicone

- Polyurethane

- Ethylene-Vinyl Acetate

- Others

By Technology

- Water-Based

- Solvent-Based

- Hot Melt

- Radiation Cured

By Product

- Tapes

- Labels

- Graphic Films

- Other Products

By End-Use Industry

- Packaging

- Automotive & Transportation

- Medical & Healthcare

- Electrical & Electronics

- Building & Construction

- Consumer Goods

- Others

By Substrate

- Paper & Cardboard

- Plastics

- Metal

- Glass

- Foam

- Fabrics & Textiles

- Nonwovens

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Pressure Sensitive Adhesives Market

- 3M Company

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Avery Dennison Corporation

- tesa SE

- Arkema Group (Bostik)

- The Dow Chemical Company

- Nitto Denko Corporation

- Sika AG

- Ashland Global Holdings Inc.

- Momentive Performance Materials Inc.

- Wacker Chemie AG

- DIC Corporation

- LG Chem Ltd.

- Shin-Etsu Chemical Co., Ltd.

*- List not Exhaustive

Research Coverage

Developed by USDAnalytics, this report investigates the Global Pressure Sensitive Adhesives (PSA) Market with analysis reviews on demand shifts, regulatory catalysts, and performance-by-chemistry benchmarking, and it highlights breakthroughs in low-VOC water-based systems, recycling-compatible label PSAs, bio-based hot melts, optically clear electronics PSAs, and EV-grade thermal/insulating solutions—making this report an essential resource for decision-makers across packaging, mobility, healthcare, electronics, and construction. Beyond headline growth, we decode cost-in-use levers (coat weight, line speed, liner choices), durability trade-offs (tack–shear–peel balance), substrate compatibility, and automation readiness, mapping supplier roadmaps to e-commerce logistics, miniaturized electronics, and circular packaging mandates to surface actionable opportunities in tapes, labels, and graphic films.

Scope Highlights

Segmentation:

- By Adhesive Chemistry: Acrylic; Rubber; Silicone; Polyurethane; Ethylene-Vinyl Acetate; Others.

- By Technology: Water-Based; Solvent-Based; Hot Melt; Radiation Cured.

- By Product: Tapes; Labels; Graphic Films; Other Products.

- By End-Use Industry: Packaging; Automotive & Transportation; Medical & Healthcare; Electrical & Electronics; Building & Construction; Consumer Goods; Others.

- By Substrate: Paper & Cardboard; Plastics; Metal; Glass; Foam; Fabrics & Textiles; Nonwovens; Others.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.