The Global Pressure Sensitive Adhesive (PSA) Tapes Market is projected to expand from USD 14.8 billion in 2025 to USD 23.4 billion by 2034, growing at a CAGR of 5.2%, as PSA tapes move well beyond their historical role as convenience fastening solutions. Across automotive, electronics, healthcare, and logistics, tapes are increasingly specified as engineered bonding interfaces that combine adhesion, load distribution, damping, insulation, and surface protection in a single material system. This shift is closely tied to lightweighting mandates, higher levels of automation, and the need to eliminate solvents, cure time, and secondary fastening operations from high-throughput manufacturing lines.

In automotive and mobility applications, PSA tapes are steadily replacing clips, screws, and liquid adhesives in trim bonding, glazing support, battery pack assembly, and cable management. Acrylic foam tapes—such as 3M™ VHB™, tesa® ACXplus, and comparable structural tape platforms from Nitto and Lohmann—are increasingly qualified for exterior and semi-structural use because they deliver high shear strength, long-term creep resistance, and vibration damping while accommodating differential thermal expansion between dissimilar materials. As EV architectures reduce powertrain noise, the NVH contribution of PSA tapes is gaining importance in procurement decisions, particularly for interior components and battery-adjacent assemblies where rattle suppression and durability directly affect perceived quality.

From a formulation standpoint, acrylic-based PSAs continue to dominate due to their UV stability, aging resistance, and consistent adhesion across metals, plastics, and coated substrates. At the same time, water-based PSA systems are gaining share in packaging and construction, driven by brand-owner sustainability targets and regulatory pressure to reduce VOC emissions. Packaging specialists and label converters increasingly favor waterborne tapes that maintain tack and cohesion while enabling recyclability of corrugated board, paper, and mono-material packaging formats. Companies such as Avery Dennison and Berry Global are expanding portfolios around recyclable, repulpable, and low-migration PSA tape constructions, aligning tape selection with circular packaging strategies rather than treating it as an afterthought.

Healthcare and electronics represent structurally important growth vectors. In wearable medical devices, PSA tapes based on acrylic and silicone chemistries are being engineered for skin compatibility, breathability, and multi-day wear, while maintaining clean removal and sterilization tolerance. In electronics and flexible circuits, ultra-thin PSA tapes are enabling component fixation, EMI shielding integration, and thermal interface layering without adding thickness or requiring heat cure. Across these applications, the value of PSA tapes lies not in adhesion speed alone, but in their ability to simplify assembly architectures, reduce part counts, and improve reliability under real operating conditions.

Tapes Market Size Outlook, 2021-2034.png)

The pressure-sensitive adhesive tapes market has entered a new phase of sustainability, digital manufacturing, and eco-innovation, characterized by bio-based raw materials, solvent-free formulations, and recyclable product designs.

In October 2024, 3M Company launched its Fastbond™ Pressure Sensitive Adhesive 1049, a water-based, low-VOC formulation engineered for industrial applications. Delivered via a new ergonomic cylinder system, it underscores 3M’s strategy to minimize environmental impact while maintaining structural-grade adhesion in automotive and construction markets. In the same month, researchers at the University of Minnesota unveiled bio-based PSAs composed of up to 60% renewable content, delivering equivalent adhesion strength to petroleum-based alternatives—a key milestone in bio-resin PSA technology.

By September 2025, Bostik (Arkema) had expanded its North American facilities, introducing UV acrylic hot melt adhesive production lines to cater to high-performance PSA tape demand in industrial and building applications. Meanwhile, automotive OEMs globally adopted lightweight wire-harness PSA tapes, reducing vehicle weight and improving assembly efficiency—accelerating the EV manufacturing transformation.

In January 2025, 3M introduced a renewable-based PSA tape line designed specifically for e-commerce and logistics packaging, targeting the growing demand for sustainable shipping tapes. Around the same time, Avery Dennison expanded its healthcare portfolio by launching antimicrobial PSA tapes, reducing pathogen transmission in clinical environments.

Earlier, in April 2024, Intertape Polymer Group (IPG) launched 100% recyclable paper-based PSA carton sealing tapes, using natural rubber adhesives to reinforce circular economy principles. That same month, Henkel AG & Co. KGaA’s Aquence PS 3017 gained recyclability certification under EU packaging standards—enhancing its appeal for flexible packaging manufacturers.

Adding to sustainability trends, Bioaqualife (January 2024) launched marine-grade biodegradable shrink wrap PSA tapes, addressing niche environmental safety applications in maritime logistics. Additionally, Franklin Adhesives & Polymers (April 2024) debuted Covinax 625, an emulsion-based PSA formulated for durable label and tape performance across multiple substrates.

Market Trend 1: Rise of Ultra-Thin, Dual-Function Thermal Conductive PSA Tapes for Electronics Heat Management

The miniaturization of consumer and industrial electronics is driving unprecedented demand for ultra-thin thermal conductive PSA tapes that can simultaneously provide strong adhesion and efficient heat dissipation. With high-performance smartphones, wearables, and high-power computing devices generating more heat per cubic millimeter, these new-generation PSA tapes are engineered to serve as dual-function materials—mechanical attachment and thermal interface solutions.

Leading electronic material developers are introducing advanced thermal interface materials (TIMs) in tape format, achieving thermal conductivity values up to 38 W/m·K in the Z-direction (through-plane). These products replace traditional thermal greases and pastes by providing a more uniform thermal path for passive cooling and improved heat spreading within confined electronic housings.

For compact device architectures, ultra-thin dielectric PSA tapes—as slim as 5 to 15 mil—are gaining adoption in high-performance smartphones and computing processors, offering both electrical insulation and efficient heat transfer. In addition, stretch-release and shock-absorbing tapes are being developed for smartphone battery retention, providing residue-free removal during repair or recycling—an increasingly critical consideration for OEM sustainability mandates.

Further, with the advent of 5G-enabled electronics, PSA thermal tapes are becoming indispensable for antenna and chip mounting applications. Recent product launches highlight tapes optimized for 5G antenna temperature regulation, directly improving device reliability and consumer comfort by managing localized thermal hotspots. The convergence of miniaturization, thermal regulation, and multifunctionality marks a pivotal technological inflection for the electronics PSA tape market.

Market Trend 2: Reformulation of PSA Tapes for Recycling-Compatible and Monomaterial Packaging

Sustainability imperatives and Extended Producer Responsibility (EPR) legislation are reshaping the packaging adhesives and tapes landscape, driving the transition to recycling-compatible and monomaterial PSA systems. The EU Packaging and Packaging Waste Regulation (PPWR) is central to the shift, requiring packaging recyclability of at least 70% by 2030 (Grade C) and 80% by 2038 (Grade B)—standards that extend to labels, closures, and adhesive layers.

In the polyolefin packaging sector, new-generation PSA tapes must align with Association of Plastic Recyclers (APR) guidelines mandating that mono-material polyethylene (PE) or polypropylene (PP) structures comprise more than 90% of total package weight. The forces PSA tape manufacturers to redesign adhesive formulations for compatibility with polyolefin recycling streams, ensuring no contamination during mechanical reprocessing or extrusion.

A critical innovation area involves mitigating the fragmentation of adhesive particles during paper recycling. Traditional PSA systems tend to produce “stickies” that clog paper mills, whereas reformulated PSA films are engineered to remain intact, allowing larger residual fragments to be easily screened and removed through standard contaminant filtration processes.

In North America, the proliferation of state-level EPR laws—with implementation targets between 2028 and 2030—means producers will soon face differentiated fees based on packaging recyclability. The regulatory shift transforms recycling-compatible PSA tapes from an environmental option into a financial necessity for brands. Manufacturers adopting these monomaterial and de-inkable adhesives are therefore positioned to capture substantial first-mover advantages in sustainable packaging supply chains.

Market Opportunity 1: PSA Tape Integration in Semi-Solid-State and Lithium Metal Battery Manufacturing

The global transition to electric mobility and high-energy-density storage technologies is catalyzing the development of advanced PSA tapes for EV batteries, where precision bonding and thermal control are critical. In pouch and prismatic cell designs, PSA tapes are increasingly replacing liquid adhesives due to their dimensional stability, ease of automation, and consistent performance under heat cycling.

Patent filings for battery adhesives specify stringent mechanical and thermal parameters—peel adhesion ≥0.1 N/10mm at 23°C and shift displacement ≤0.2 mm under 500g load at 40°C—ensuring stability during assembly and long-term operation. These parameters enable exact alignment of electrodes and separators in multi-cell stacks, reducing production errors and enhancing performance uniformity.

Additionally, dielectric PSA tapes for insulation between cells and modules offer dielectric breakdown strengths of 3–10 kV (AC) in ultra-thin formats (≈2.0 mil), balancing electrical safety and space optimization. With UL® 94 V-0 flammability compliance, these materials meet the stringent safety standards required by leading automotive OEMs.

Emerging multi-layer laminates integrate PSA layers with ceramic or mica sheets to combine thermal propagation resistance and mechanical cushioning, crucial for managing thermal runaway risks in high-power EV and solid-state batteries. Compared to liquid adhesives, PSA tapes streamline battery module assembly, prevent porous pad contamination, and enhance manufacturing automation, offering both safety and scalability advantages for next-generation electric vehicles.

Market Opportunity 2: Expanding Role of PSA Tapes in Thin-Film Photovoltaic (PV) Installation and Maintenance

The accelerating growth of solar energy installations, particularly thin-film PV systems, presents a rapidly expanding market for high-performance PSA tapes engineered for long-term outdoor durability. As governments push renewable energy deployment, PSA tapes are becoming integral to solar module mounting, cable management, grounding, and seam sealing applications.

In India, the Central Financial Assistance (CFA) program provides subsidies of up to 40% for rooftop solar systems up to 3 kW, targeting 40,000 MW of installed rooftop solar capacity by 2026. Such large-scale rollouts exponentially increase demand for PSA tapes used in panel assembly and installation processes.

High-performance acrylic foam and VHB (Very High Bond) tapes are specifically designed for UV resistance, moisture endurance, and temperature cycling, maintaining bond integrity for over 25 years of outdoor exposure. These materials replace traditional fasteners, reducing metal fatigue, corrosion risk, and mechanical stress concentration, thus extending module lifespan and lowering maintenance costs.

Beyond structural mounting, PSA tapes are vital for secondary applications, including junction box bonding, wire fixation, and dielectric insulation rated up to 5.0 kV, enabling compact and safe electrical layouts within PV systems. The increasing adoption of lightweight and flexible solar modules further amplifies the demand for pressure-sensitive adhesive solutions that deliver both mechanical stability and electrical insulation in harsh field conditions.

Pressure Sensitive Adhesive (PSA) Tapes Market Share Insights, 2025-2034

Market Share by Adhesive Chemistry

Acrylic Pressure Sensitive Adhesives (PSAs) dominate the global PSA tapes market, accounting for an estimated 52.1% market share in 2025, reflecting their unmatched combination of UV resistance, oxidation stability, and excellent adhesion–cohesion balance. Acrylic PSAs have become the industry standard for applications requiring long-term durability, transparency, and weatherability, making them ideal for packaging, labels, and electronic devices. Their ability to maintain performance over a wide temperature range, resist yellowing, and adhere well to diverse surfaces—including metals, plastics, and glass—has cemented their dominance in both consumer and industrial applications. Moreover, the shift toward solvent-free, emulsion-based acrylic PSAs aligns with global sustainability goals and VOC reduction regulations, reinforcing their leadership position.

Rubber-Based PSAs continue to hold a significant portion of the market due to their high initial tack and aggressive adhesion strength, particularly in carton sealing, masking, and general-purpose tapes. Their lower cost and excellent performance on rough or low-energy substrates make them the preferred choice in packaging, construction, and industrial maintenance. Silicone PSAs remain crucial in high-temperature and electronic applications, offering superior release properties and thermal stability beyond 200°C, essential for aerospace and semiconductor production. Hybrid PSAs, combining acrylic and rubber chemistries, are gaining attention for their ability to provide enhanced adhesion and performance versatility, while bio-based PSAs represent the industry’s most promising innovation frontier—addressing sustainability and circular economy goals by leveraging renewable raw materials.

Market Share by End-Use Industry

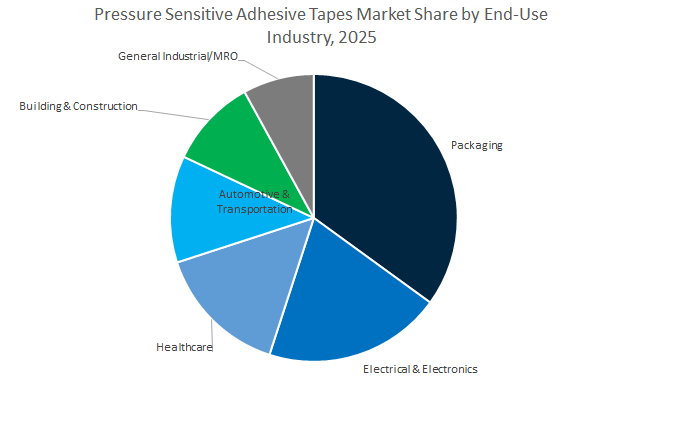

The packaging sector is the largest consumer of pressure-sensitive adhesive tapes, projected to hold 37.3% of global market share in 2025. This dominance is driven by the explosive growth of e-commerce, logistics, and consumer goods packaging, which collectively demand billions of square meters of carton sealing, labeling, and tamper-evident tapes each year. PSA tapes are favored for their ease of use, instant adhesion, and versatility across substrates, enabling faster packaging lines and reduced operational costs. In addition, sustainability-driven innovations—such as recyclable and paper-based PSA tapes—are reshaping the packaging landscape, as brand owners and packaging converters prioritize eco-friendly adhesive solutions.

The electrical and electronics industry represents a rapidly growing, high-value segment, relying on PSA tapes for thermal management, insulation, shielding, and bonding of components in smartphones, EV batteries, and semiconductor devices. Healthcare applications form another critical area, with medical-grade PSAs used extensively in wound dressings, surgical drapes, transdermal patches, and wearable health monitoring devices, where biocompatibility, breathability, and skin adhesion are essential. The automotive and transportation segment continues to expand as PSAs replace mechanical fasteners in interior trims, emblems, sensors, and lightweight assemblies, supporting the shift toward noise reduction, lightweighting, and electric mobility. In building and construction, PSA tapes are used for sealing, glazing, HVAC insulation, and weatherproofing, benefiting from their fast application and long-term flexibility. The general industrial and MRO sector provides consistent baseline demand for repair, surface protection, and assembly tasks, reinforcing the PSA tape market’s broad industrial reach.

The global Pressure Sensitive Adhesive (PSA) Tapes Market features a consolidated yet innovative landscape led by diversified conglomerates and specialty material manufacturers. Each key player is investing in sustainable formulations, next-gen polymers, and advanced coating technologies to capture growing demand from automotive, packaging, medical, and electronics sectors.

3M maintains its leadership through a vast product portfolio, including the iconic VHB™ (Very High Bond) acrylic foam tape series, a structural alternative to mechanical fasteners in construction and automotive assembly. In line with its PFAS phase-out strategy, 3M will exit fluorochemical production by the end of 2025, redirecting R&D toward non-fluorinated, water-based PSA chemistries. The company recently launched its Fastbond™ low-VOC adhesive series, optimizing performance for sustainable industrial bonding. With USD 1.3–2.3 billion in R&D reallocation, 3M reinforces its long-term commitment to eco-safe, next-generation PSA technology.

Tesa SE, a subsidiary of Beiersdorf AG, is heavily investing in its “Rethink Materials” initiative, developing recyclable and bio-based PSA tapes for packaging and automotive sealing. Its tesa® ACXplus acrylic core tapes provide permanent structural bonding for exterior automotive components, while BSR (Buzz, Squeak, and Rattle) tapes address NVH reduction in EV interiors. The company is expanding its European production network to ensure supply chain resilience, showcasing new eco-tape lines at major industry events such as Fachpack 2025 and Empack Madrid 2025.

Nitto Denko leverages its vertical integration and expertise in Optronics and Flexible Sensing to develop fiber-based and high-cohesion PSA films. Products like Nitto 5711LE and SPV 9300 series tapes exemplify precision engineering for automotive displays, sensor systems, and flexible electronics. The company’s low-emission, high-adhesion acrylic tapes are widely used in vehicle interior assemblies and consumer electronics, meeting strict VOC emission standards. Nitto’s “Fiber PSA” line showcases innovation in next-gen conformable adhesives, optimized for both industrial and wearable device applications.

Avery Dennison continues to lead in solvent-free PSA innovations with its rBG Pure Liners made from recycled, unbleached fibers, underscoring its dedication to circularity. Its AFB™ (Acrylic Foam Bond) and HPA™ (High-Performance Acrylic) adhesive systems address critical EV applications, including mirror assembly and thermal insulation. Avery Dennison’s UV acrylic and hot-melt adhesive technologies align with global air quality standards while delivering high adhesion for automotive interiors. Through material innovation and digital integration, the company is bridging performance, sustainability, and traceability within its Performance Tapes Division.

Henkel, through its Adhesive Technologies business, is advancing recyclable and low-VOC PSA solutions for the packaging and electronics sectors. The Aquence PS 3017 certification validates Henkel’s commitment to sustainable packaging in compliance with EU recycling directives. The company’s portfolio includes high-speed hot-melt PSAs designed for automated industrial and hygiene applications. Additionally, Henkel continues to expand its R&D for weather-resistant PSA tapes used in construction insulation and sealing. Its integration of digital process monitoring and low-carbon raw material sourcing enhances both performance and traceability, setting new industry benchmarks.

IPG has positioned itself as a frontrunner in the eco-packaging revolution with its 100% recyclable paper-based PSA tapes, catering to the food, retail, and e-commerce industries. These products feature natural rubber adhesives that combine strong adhesion with full recyclability, contributing directly to circular economy initiatives. IPG continues to scale its North American operations, developing sustainable pressure-sensitive tapes for high-speed carton sealing and logistics applications.

Country Analysis: Regional Market Insights and Strategic Developments in the Global Pressure Sensitive Adhesive (PSA) Tapes Industry

China: Expanding Manufacturing Capacity and Specialty PSA Tape Innovation for Electronics and New Energy Vehicles

China remains the global powerhouse in Pressure Sensitive Adhesive (PSA) tapes manufacturing, driven by rapid industrial expansion, government policy support, and the surging domestic electric vehicle (EV) and electronics sectors. Major international producers have accelerated local production investments, establishing new facilities aimed at supplying high-performance PSA tapes for EV battery insulation, component protection, and lightweight bonding. The expansion aligns with the country’s new energy transition goals, where adhesive tapes play a vital role in improving battery safety, vibration dampening, and heat management.

The government’s “Made in China 2025” strategy and continued emphasis on 5G and renewable energy infrastructure have significantly boosted demand for thermal management tapes and protective PSA films used in electronics, semiconductors, and high-speed communication systems. Domestic manufacturers, supported by state-owned enterprises, are scaling up acrylic monomer and resin production to secure raw material availability amid global supply fluctuations. Moreover, the e-commerce logistics boom is fueling widespread adoption of tamper-evident PSA security tapes and water-activated carton sealing tapes to meet packaging integrity standards. Innovation is also thriving in polyimide-based high-temperature PSA tapes, now essential for aerospace, high-speed rail, and solar applications. With strict low-VOC compliance measures and a strong emphasis on circular economy policies, China’s PSA tape industry is strategically positioned to dominate both commodity and specialty adhesive markets in Asia-Pacific.

United States: Strengthening Sustainable PSA Tape Production through Green Chemistry and Advanced Material Engineering

The United States PSA tapes market continues to lead in sustainability, innovation, and application diversity, particularly across automotive, aerospace, construction, and packaging sectors. Leading U.S.-based manufacturers have announced large-scale R&D investments to develop next-generation bio-based and solvent-free pressure sensitive adhesive formulations using renewable feedstocks. The trend is reinforced by the U.S. Environmental Protection Agency (EPA) tightening VOC emission regulations, compelling manufacturers to transition toward water-based acrylic and silicone PSA systems that deliver both environmental and performance benefits.

In the automotive sector, the rapid pace of EV manufacturing has catalyzed the adoption of acrylic foam tapes (AFT) for structural bonding, replacing conventional mechanical fasteners to enhance aerodynamics, reduce weight, and mitigate noise, vibration, and harshness (NVH). Federal infrastructure spending under the Infrastructure Investment and Jobs Act (IIJA) is also driving demand for high-tack construction tapes, flashing tapes, and building envelope sealants used in energy-efficient infrastructure. Simultaneously, leading packaging companies are piloting chemical recycling initiatives in partnership with PSA label producers to reclaim silicone release liners and backing films, fostering a closed-loop recycling model. In aerospace and defense, high-shear PSA tapes are gaining traction for composite bonding, masking, and vibration control, showcasing the U.S. market’s expanding footprint in advanced engineered adhesive solutions.

Germany: Innovating Bio-Based and High-Performance PSA Tape Solutions for Automotive and Industrial Applications

Germany stands at the forefront of Europe’s PSA tape innovation, integrating sustainability mandates, automotive engineering precision, and material science excellence. The country’s PSA tape manufacturers are closely aligned with premium automotive OEMs, developing lightweight bonding solutions that replace welding and bolts in multi-material car body assemblies, improving range efficiency and vehicle performance. Compliance with the EU’s REACH regulation and the European Green Deal has accelerated the shift toward fully repulpable PSA tapes, low-migration adhesives, and recyclable packaging solutions, particularly for food and consumer goods applications.

A leading European adhesive technology company has invested heavily in automation upgrades at its German facility, optimizing the production of double-sided foam tapes and ensuring uniform adhesive coating thickness for high-speed assembly lines. Concurrently, research institutions are pioneering high-temperature silicone-based PSA formulations capable of withstanding extreme thermal conditions in industrial machinery, energy storage, and aerospace applications. The integration of Industry 4.0 smart manufacturing systems, including embedded sensors for real-time adhesive monitoring, highlights Germany’s leadership in digitalized adhesive production. Additionally, ongoing government-supported biotechnology programs are supporting the commercialization of bio-based rubber PSA derived from sustainable feedstocks, cementing Germany’s role as the European epicenter for high-value, eco-innovative adhesive technologies.

India: E-Commerce and Infrastructure Growth Fueling Explosive Demand for Packaging and Industrial PSA Tapes

India’s Pressure Sensitive Adhesive Tapes market is expanding at record pace, driven by infrastructure development, logistics modernization, and digital retail growth. The country’s booming e-commerce sector has dramatically increased demand for BOPP carton sealing tapes, tamper-proof packaging tapes, and dispenser-grade box sealing products, critical to ensuring package integrity in cross-border logistics. Simultaneously, large-scale public infrastructure initiatives, including national highway construction, metro projects, and smart cities, are stimulating the uptake of duct PSA tapes, reflective road marking tapes, and hazard barrier tapes used in safety and visibility applications.

Under the “Make in India” initiative, the country is attracting substantial foreign direct investment (FDI) in local adhesive tape manufacturing, particularly in medical-grade and industrial PSA segments. New assembly facilities in the consumer electronics and smartphone sectors are further boosting domestic demand for die-cut PSA tapes, used for component mounting, cushioning, and temporary protection during assembly. The pharmaceutical packaging segment is also witnessing a shift toward tamper-evident PSA labels and specialty adhesives, ensuring compliance with stricter drug traceability and safety regulations. To meet sustainability targets, Indian producers are rapidly expanding water-based PSA emulsion capacity, offering low-cost, low-VOC alternatives for commodity and industrial tapes. With its rising manufacturing base and robust logistics infrastructure, India is emerging as a key global production hub for high-volume and specialty PSA tape applications.

Japan: Leading the Development of Ultra-Thin PSA Films and High-Precision Electronic Tapes

Japan maintains a global leadership position in ultra-thin PSA film manufacturing, driven by its strong presence in electronics, precision engineering, and advanced automotive production. The nation’s adhesive tape manufacturers are world-renowned for developing extremely thin, uniform, and high-durability PSA layers used in semiconductors, flexible displays, and mobile device assembly. The innovations support next-generation electronic components, where reliability under micro-thermal and mechanical stress is essential.

The Japanese market continues to push the boundaries in heat-resistant, transparent, and conductive PSA films for wearable devices and flexible OLED display panels. The country’s automotive industry also utilizes specialty PSA bonding tapes for exterior panel mounting, sensor attachment, and acoustic insulation, aligning with its broader push toward lightweight and fuel-efficient vehicle designs. Research institutions are conducting long-term performance studies on PSA durability under temperature and humidity cycling, supporting Japan’s commitment to reliability and product longevity. With precision as its hallmark, Japan remains the global benchmark for quality and innovation in high-performance PSA tapes.

South Korea: Emerging Leader in Conductive PSA Tapes for Flexible Displays and EV Battery Applications

South Korea’s Pressure Sensitive Adhesive Tapes industry is gaining international prominence due to its expertise in display technology and electric vehicle (EV) battery manufacturing. The nation’s R&D efforts are heavily focused on conductive and thermally stable PSA tapes, designed for flexible OLED panels, lithium-ion battery insulation, and heat dissipation layers. The advanced materials enable safer, thinner, and more efficient electronics and mobility components, aligning with South Korea’s dominant position in semiconductor and display production.

Korean adhesive producers are also collaborating with major automotive OEMs to deliver high-performance PSA bonding solutions for direct glazing, interior lamination, and lightweight structural reinforcement in EVs. The country’s commitment to carbon neutrality and smart factory automation further supports the adoption of solvent-free and hybrid PSA technologies. With its robust technological foundation and global export capability, South Korea is emerging as a key innovation hub for next-generation PSA materials catering to high-tech electronics and green mobility applications.

Brazil: Industrial Growth and Localization Driving PSA Tape Demand in Construction and Automotive Sectors

Brazil’s Pressure Sensitive Adhesive Tapes market is accelerating in tandem with the nation’s construction, automotive, and industrial growth. As Latin America’s largest economy, Brazil is witnessing increased consumption of heavy-duty PSA tapes used in building insulation, flooring systems, and waterproofing applications. The automotive sector—bolstered by rising domestic production and foreign OEM investment—is driving the adoption of high-strength bonding tapes for trim attachment, cable harnessing, and acoustic insulation, replacing mechanical fasteners in assembly operations.

To meet The demand, local manufacturers are expanding production facilities for both industrial and packaging-grade PSA tapes, supported by government incentives for import substitution and manufacturing localization. Additionally, construction activity related to energy and infrastructure modernization projects is increasing the use of high-adhesion weatherproof and reflective PSA tapes. With ongoing industrial diversification and a growing export-oriented adhesive sector, Brazil is steadily positioning itself as Latin America’s key production and application hub for industrial-grade PSA tapes.

Pressure Sensitive Adhesive (PSA) Tapes Market Report Scope

Pressure Sensitive Adhesive (PSA) Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.8 Billion

|

|

Market Size (2034)

|

$23.4 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Backing Material (Polymer Films, Paper, Foils, Cloth, Foam), By Adhesive Chemistry (Acrylic, Rubber-Based, Silicone, Hybrid, Bio-Based/Renewable), By Technology (Water-Based, Solvent-Based, Hot-Melt, Radiation-Cured), By Product Type (Single-Sided, Double-Sided, Transfer, Specialty), By End-Use Industry (Packaging, Automotive & Transportation, Electrical & Electronics, Building & Construction, Healthcare, General Industrial/MRO

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Nitto Denko Corporation, tesa SE, Avery Dennison Corporation, Henkel AG & Co. KGaA, Lintec Corporation, H.B. Fuller Company, Arkema Group (Bostik), Intertape Polymer Group Inc. (IPG), Lohmann GmbH & Co. KG, Sika AG, Scapa Group Plc, Shurtape Technologies, LLC, Dow Inc., Saint-Gobain Tape Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Backing Material

- Polymer Films

- Paper

- Foils

- Cloth

- Foam

By Adhesive Chemistry

- Acrylic

- Rubber-Based

- Silicone

- Hybrid

- Bio-Based/Renewable

By Technology

- Water-Based

- Solvent-Based

- Hot-Melt

- Radiation-Cured

By Product Type

- Single-Sided

- Double-Sided

- Transfer

- Specialty

By End-Use Industry

- Packaging

- Automotive & Transportation

- Electrical & Electronics

- Building & Construction

- Healthcare

- General Industrial/MRO

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Pressure Sensitive Adhesive Tapes Market

- 3M Company

- Nitto Denko Corporation

- tesa SE

- Avery Dennison Corporation

- Henkel AG & Co. KGaA

- Lintec Corporation

- H.B. Fuller Company

- Arkema Group (Bostik)

- Intertape Polymer Group Inc. (IPG)

- Lohmann GmbH & Co. KG

- Sika AG

- Scapa Group Plc

- Shurtape Technologies, LLC

- Dow Inc.

- Saint-Gobain Tape Solutions

*- List not Exhaustive

Research Coverage

Crafted by USDAnalytics, this report investigates the Global Pressure Sensitive Adhesive (PSA) Tapes Market, delivering analysis reviews on regulatory inflection points, materials innovation, and end-market adoption, and it highlights breakthroughs in water-based acrylics, recyclable/mono-material designs, ultra-thin thermal PSA interfaces, and high-shear foam constructions for EVs and electronics. We translate technical performance (tack–shear balance, UV/weathering, dielectric safety, and processability) into sourcing and cost-in-use benchmarks, compare supplier roadmaps, and map risk from VOC limits and EPR fees—making this report an essential resource for executives, engineers, and procurement leaders seeking solvent-free, automation-ready, and circular PSA tape solutions across packaging, mobility, healthcare, construction, and advanced electronics.

Scope Highlights

Segmentation:

- By Backing Material: Polymer Films; Paper; Foils; Cloth; Foam.

- By Adhesive Chemistry: Acrylic; Rubber-Based; Silicone; Hybrid; Bio-Based/Renewable.

- By Technology: Water-Based; Solvent-Based; Hot-Melt; Radiation-Cured.

- By Product Type: Single-Sided; Double-Sided; Transfer; Specialty.

- By End-Use Industry: Packaging; Automotive & Transportation; Electrical & Electronics; Building & Construction; Healthcare; General Industrial/MRO.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034.

Companies Covered: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.