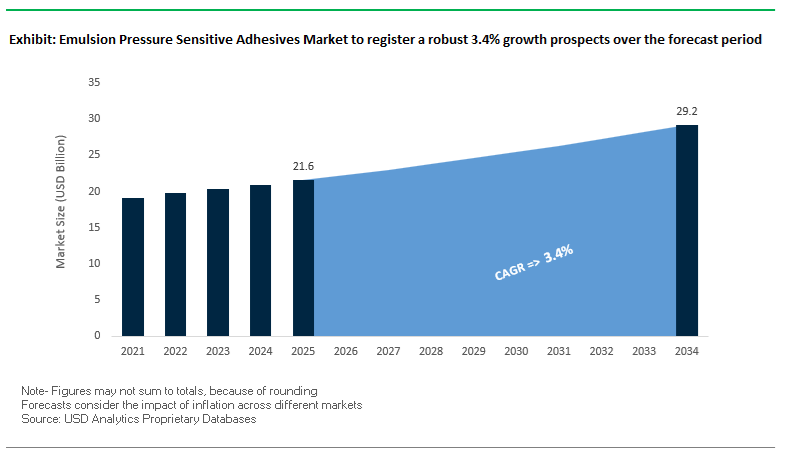

The Global Emulsion Pressure Sensitive Adhesives (PSA) Market is projected to grow from USD 21.6 billion in 2025 to USD 29.2 billion by 2034, reflecting a CAGR of 3.4%, as industrial bonding requirements realign around environmental compliance, worker safety, and application-specific performance. Water-based acrylic emulsion PSAs are increasingly displacing solvent-based systems as OEMs across packaging, medical devices, automotive interiors, and electronics respond to tightening VOC regulations and solvent exposure limits in North America and Europe. Beyond compliance, emulsion PSAs have become structurally advantaged due to their compatibility with high-speed coating, drying, and lamination processes, enabling manufacturers to maintain throughput while meeting solvent-free manufacturing mandates. This transition is not cyclical; it reflects a permanent shift in how adhesive performance is specified, qualified, and scaled across regulated industrial environments.

From a materials and formulation standpoint, manufacturers are closing historical performance gaps between solvent-borne and water-based PSAs through polymer architecture redesign and filler engineering. The incorporation of montmorillonite (MMT) nanofillers at 1–2 wt%, validated in commercial acrylic emulsion systems, has demonstrated up to 10,000-fold improvement in shear holding time, materially improving creep resistance in industrial tapes and labels. In parallel, advances in polymer backbones and tackifier chemistry have delivered approximately 50% higher peel strength on low-surface-energy substrates such as HDPE, expanding emulsion PSA adoption in polyolefin film packaging and laminated automotive components. These developments reflect a broader OEM requirement for adhesives that maintain cohesive strength and adhesion stability across temperature variation and substrate diversity without reverting to solvent-based chemistries.

Medical and bio-based applications represent a structurally important demand inflection within the market. Emulsion PSA platforms qualified under ISO 10993 cytotoxicity and sensitization standards, including established medical-grade acrylic families such as Flexcryl™ and Aroset™, are increasingly specified for transdermal patches, wound dressings, and wearable medical devices, where skin safety, breathability, and residue control are non-negotiable. At the same time, adhesive producers are scaling bio-based and renewable monomer content within emulsion PSAs to support sustainability targets without compromising bond reliability or process stability.

In October 2025, the European Union announced a sweeping policy mandating the phase-out of select solvent-based chemicals in industrial adhesives and coatings by 2027. This policy shift is expected to significantly bolster the adoption of high-solids, water-based emulsion PSAs across automotive, packaging, and construction industries. Such regulation-driven transitions are fostering heavy R&D investment in low-VOC polymer emulsions, particularly those offering improved tack, cohesion, and surface energy compatibility for diverse substrates.

The same month, Avery Dennison Corporation unveiled a new series of low-VOC acrylic emulsion tapes for EV battery pack thermal management, directly addressing thermal dissipation and emission compliance challenges in high-voltage automotive systems. These tapes, designed for NVH (Noise, Vibration, and Harshness) reduction and electrical insulation, demonstrate how water-based PSAs are penetrating mission-critical mobility applications.

In August 2025, DIC Corporation expanded production capacity at its Asia-Pacific facility for VONCOAT W-series water-based PSAs, aiming to serve demand from the industrial tape and specialty film markets. Around the same period, a July 2025 merger between a leading global chemical producer and a regional supplier of natural and synthetic latex compounds signaled deeper vertical integration in raw material sourcing — a strategic move ensuring supply chain control in the growing rubber emulsion PSA segment for hygiene and construction applications.

H.B. Fuller’s June 2025 breakthrough in bio-based PSA monomer integration — achieving up to 60% renewable content — underscored the market’s pivot toward sustainability-driven innovation. Shortly after, Ashland (May 2025) advanced its Flexcryl™ medical-grade PSA line, improving moisture vapor transmission rate (MVTR) and patient comfort for wound-care dressings and wearable medical devices, aligning with stringent ISO 10993 standards.

Earlier in April 2025, Arkema’s Bostik division commissioned a $50 million North American facility for high-solids acrylic PSAs, supporting flexible packaging and high-speed labeling lines — a move reinforcing its leadership in low-emission adhesive manufacturing. In March 2025, 3M expanded its water-based adhesive systems with the Fastbond™ portable cylinder solution, designed for foam bonding and insulation applications in green-certified buildings, offering low VOCs and non-flammability in compliance with LEED standards.

Across North America, Europe, and Asia-Pacific, regulatory enforcement of chemical compliance—including REACH, RoHS, and VOC restrictions—is pushing manufacturers toward the next generation of environmentally safe emulsion PSAs that meet both performance and sustainability requirements.

Leading industry producers are investing heavily in APEO-free acrylic copolymer systems, where alkylphenol ethoxylates (APEOs)—previously used as surfactants—are being eliminated in favor of next-generation, surfactant-stabilized emulsions. These new formulations deliver excellent cohesive strength, chemical resistance, and peel adhesion while aligning with REACH and Green Seal certification standards. For example, major global brands like Franklin International and Henkel have launched APEO-free acrylic-based products (e.g., Covinax® and Micronax® series) explicitly designed to meet European REACH and U.S. EPA safety thresholds.

In addition, the drive to meet California Air Resources Board (CARB) VOC regulations and the European Green Deal has intensified research into ultra-low VOC emulsion polymer adhesives with improved curing kinetics and long-term thermal stability. By eliminating solvents and using reactive acrylic dispersions, manufacturers are reducing VOC emissions to less than 5 g/L, enabling compliance with the most stringent indoor air quality (IAQ) criteria in industrial and packaging applications.

The growing global focus on plastic circularity and packaging recyclability is catalyzing the rapid adoption of wash-off Emulsion PSAs—adhesives engineered to detach cleanly from substrates during industrial recycling processes. These systems are crucial in ensuring high-quality material recovery, especially for PET bottles, HDPE containers, and polypropylene films.

In PET recycling, traditional PSAs contaminate the flake stream, degrading the quality and preventing re-use in food-grade rPET applications. In contrast, modern wash-off emulsion adhesives are formulated to disengage under standard caustic wash conditions (typically at 85–90°C, 1–2% NaOH solution), achieving >90% label separation efficiency. The allows clean PET recovery and drastically improves the recyclate yield—a critical factor in meeting EPR (Extended Producer Responsibility) targets and European Plastics Strategy goals.

Supported by regulatory frameworks such as the EU Circular Economy Action Plan, and guidelines from the Association of Plastic Recyclers (APR), adhesive manufacturers are channeling R&D investments into recycling-compatible PSAs optimized for packaging that complies with Design for Recyclability (DfR) principles. The technological evolution ensures that label and packaging adhesives no longer act as contaminants but as enablers of closed-loop recycling systems across the consumer goods supply chain.

The global e-commerce surge and the automation of warehouse and logistics operations have created a fast-growing market for high-performance Emulsion PSAs used in shipping labels, parcel tracking, and barcode applications. These PSAs must ensure instant tack, strong adhesion, and fast application speed across variable substrates—including recycled corrugated boards and flexible films—under fluctuating humidity and temperature conditions.

E-commerce packaging lines operate at application speeds exceeding 600 labels per minute, requiring optimized rheology and shear properties to prevent adhesive buildup, misalignment, or tearing during high-speed dispensing. In addition, the rise in recycled paperboard and low-energy surface (LES) packaging introduces further complexity, as these substrates are rough, porous, and often contaminated with dust or fibers. Advanced emulsion PSA formulations, based on acrylic or hybrid polymer dispersions, provide high wet tack, superior shear resistance, and residue-free removal even on uneven surfaces, making them the preferred choice for global logistics operations.

The transformation of the global packaging landscape toward bio-based and compostable solutions presents a critical expansion path for the Emulsion PSA industry. As brand owners and regulatory bodies increasingly demand certified industrial compostability (EN 13432) and renewable-content adhesives, water-based emulsion systems are emerging as the sustainable alternative to solvent-based or hot-melt PSAs.

Manufacturers are investing in renewable polymer feedstocks, such as bio-acrylics, modified starch, and lignin-derived monomers, to produce compostable PSAs compatible with PLA (Polylactic Acid), cellulose films, and bio-based paper laminates. These adhesives not only maintain excellent peel strength, clarity, and aging resistance, but also meet end-of-life environmental criteria—decomposing fully under industrial composting conditions within a regulated timeframe.

Certification to EN 13432 and ASTM D6400 standards is becoming a decisive factor for adhesive suppliers targeting packaging applications in the food, beverage, and personal care sectors, where sustainability labeling drives purchasing decisions. Companies like Henkel, BASF, and Sika have already invested in bio-based PSA platforms that combine renewable carbon content with functional compostability, positioning them to lead the emerging green flexible packaging adhesives segment.

Emulsion Pressure Sensitive Adhesives Market Share Insights, 2025-2034

Acrylic-based emulsion pressure-sensitive adhesives (PSAs) dominate the global market, holding the largest share thanks to their outstanding balance of tack, peel, and shear properties combined with superior UV, oxidation, and aging resistance. These waterborne acrylic dispersions have become the industry standard for labels, packaging tapes, and graphic films that require long-term clarity, non-yellowing performance, and weather durability. Unlike rubber-based systems, acrylic emulsions maintain adhesion over a wide temperature range and are resistant to moisture and chemicals—key advantages in automotive, electronics, and durable goods labeling. Their adaptability to high-speed coating lines and their ability to be formulated for both permanent and removable adhesives further solidify their dominance. The global push toward low-VOC, solvent-free adhesive technologies has also accelerated the adoption of acrylic emulsions in regulatory-sensitive markets such as North America and Europe. As sustainability and recyclability become core priorities in packaging and labeling, acrylic-based PSAs are increasingly tailored for recyclable paper and film substrates, strengthening their long-term leadership position in the emulsion PSA industry.

Rubber-based emulsion PSAs, derived from natural and synthetic latex, hold a significant secondary market position, particularly in high-tack and cost-driven applications such as carton sealing tapes, duct tapes, and masking tapes. Their primary advantage lies in their instant adhesion (quick stick), even on low-energy or rough surfaces—a performance attribute that acrylics typically cannot match without surface treatment. This makes them indispensable in industrial packaging, construction, and consumer applications where speed and affordability take precedence over long-term weather or UV stability. However, environmental and aging limitations—such as yellowing and reduced resistance to heat and solvents—have restricted their penetration in high-performance or outdoor markets. Nonetheless, manufacturers are enhancing rubber-based emulsions through formulation improvements like crosslinking and antioxidant stabilization to increase cohesion and durability. As developing economies expand their packaging, logistics, and manufacturing sectors, cost-competitive rubber-based PSAs are expected to maintain strong volume growth, particularly in Asia-Pacific and Latin America.

Permanent PSAs Account for 72.3% of the Global Market, Anchoring Industrial and Packaging Demand

The permanent PSA segment forms the backbone of the global emulsion pressure-sensitive adhesives market, dominating with more than 70% of total demand. Permanent adhesives are engineered for enduring adhesion that cannot be removed without damaging the substrate—an essential property in packaging tapes, shipping labels, graphic overlays, and industrial assembly films. Their strong, lasting bonds make them indispensable across manufacturing, logistics, and construction applications. Acrylic emulsions are the leading chemistry here, providing consistent adhesion, UV resistance, and temperature stability for long-term outdoor use. In addition, the rising demand for eco-friendly, water-based permanent PSAs—especially in e-commerce packaging, labeling, and film lamination—continues to fuel market expansion. Permanent PSAs are also widely used in automotive trim assembly, electronic components, and consumer appliances, where durability, vibration resistance, and cohesive strength are crucial. The combination of sustainability, performance, and reliability ensures that permanent adhesives will remain the dominant product category in both volume and value across global markets.

Removable and repositionable emulsion PSAs represent a fast-growing and strategically important segment, catering to markets that require temporary adhesion without leaving residue. This includes graphic films, retail shelf labels, protective films, window decals, and notepads, where easy removal and surface safety are critical. These adhesives are designed with tailored polymer architectures that balance tack and peel strength, ensuring reliable adhesion during service but effortless removal afterward. Growth in advertising graphics, e-commerce packaging, and protective masking—especially within automotive and electronics manufacturing—continues to boost this segment. The increasing use of removable PSAs in sustainable paper-based and recyclable film materials is also fueling innovation. Leading manufacturers are developing low-migration, ultra-clear, and residue-free acrylic emulsions to meet demands for clean removability, optical clarity, and compatibility with coated or printed substrates. As design flexibility and brand presentation gain importance in consumer packaging and marketing, repositionable PSA systems are rapidly evolving into one of the most dynamic submarkets in the emulsion adhesive industry.

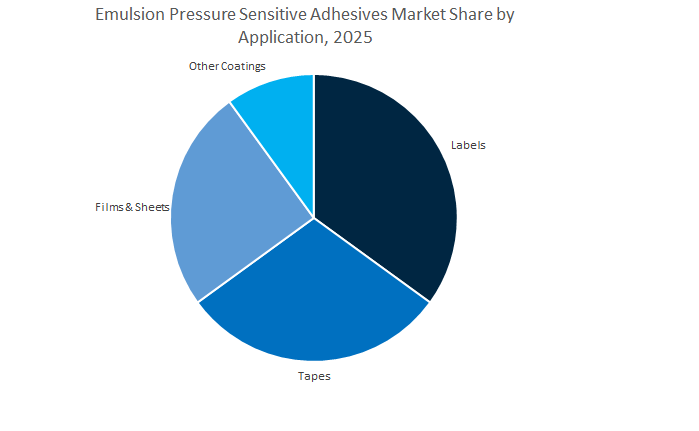

Market Share by Application

The global emulsion pressure sensitive adhesives market is dominated by multinational players like Avery Dennison, Arkema (Bostik), DIC Corporation, Ashland, and H.B. Fuller, each leveraging advanced R&D capabilities and integrated production networks to address evolving regulatory, sustainability, and performance requirements. These companies are investing in bio-based materials, advanced acrylic emulsion technologies, and smart adhesive solutions for EV batteries, flexible packaging, and medical devices.

Avery Dennison has positioned itself at the forefront of EV adhesive technologies, focusing on acrylic emulsion PSAs for battery pack assembly, thermal insulation, and interior NVH reduction. The company’s Volt Tough™ line delivers electrical insulation performance for high-voltage systems, enhancing safety in EV architectures. Additionally, its rBG Pure Liner range, made from recycled fibers, demonstrates Avery Dennison’s commitment to sustainability in label and tape production, while its Core Series™ Portfolio offers globally standardized PSA categories for industrial and automotive manufacturing efficiency.

Arkema’s Bostik division leverages Orevac® polymer expertise to create emulsion PSAs with enhanced barrier performance and cohesive strength for multilayer packaging and labeling applications. The company’s 2025 $50 million investment in North America expanded its production of high-solids acrylic PSAs, catering to flexible packaging and disposable hygiene products. With a strong focus on low-carbon adhesive technologies, Bostik actively participates in cross-value chain sustainability collaborations with partners like Dow and Nordson, reinforcing its leadership in renewable, water-based adhesive chemistry.

DIC Corporation benefits from full vertical integration, manufacturing its own proprietary resins to optimize emulsion PSA performance. Its VONCOAT W-series has become a flagship product, offering high holding power and excellent adhesion on non-polar surfaces like polyethylene films. Through polysiloxane-acrylic hybrid technology (CERANATE line), DIC extends its product lifespan in outdoor graphics and weather-resistant coatings. The company’s deep integration across fiber processing and paper coating markets gives it a distinct competitive edge in functional substrate applications.

Ashland remains a dominant force in medical pressure sensitive adhesives, particularly in wound care, transdermal patches, and wearable sensors. Its Flexcryl™ and Aroset™ emulsion acrylic brands are formulated for low monomer residue and latex-free performance, fully compliant with ISO 10993 cytotoxicity and sensitization tests. Ashland’s innovations emphasize skin comfort, sterilization stability, and regulatory compliance, positioning it as a leading supplier to medical device OEMs globally, supported by production and service hubs across North America, Europe, and Asia.

H.B. Fuller continues to lead in sustainable water-based PSA innovation, targeting replacement of solvent-based systems with bio-based, low-emission alternatives. Its PSAs deliver high adhesion to recycled substrates, enabling reliable tamper-evident labeling for e-commerce packaging. The company’s bio-based monomer R&D is pushing renewable content levels above 60%, while its extensive global supply chain supports both customized specialty tapes and high-volume label production, ensuring consistent quality and supply reliability worldwide.

The United States Emulsion Pressure Sensitive Adhesives market is at the forefront of sustainability-driven transformation, led by EPA regulations curbing Volatile Organic Compound (VOC) emissions and favoring low-VOC water-based acrylic PSAs. The EPA’s 2024 final rule restricting methylene chloride further accelerates the transition away from solvent-based formulations, positioning emulsion PSAs as the preferred choice for industries seeking compliance and environmental performance.

In October 2024, 3M Company introduced Fastbond™ PSA 1049, an ergonomically designed, solvent-free adhesive system for high-performance industrial applications, setting a new benchmark in sustainable adhesive delivery. Concurrently, FDA’s 21 CFR 175.125 regulations continue to drive innovation in food-contact-safe emulsion acrylic PSAs, sustaining strong demand across the food and beverage labeling market. Companies such as H.B. Fuller are expanding their North American footprint by offering low-VOC, waterborne adhesive portfolios for construction, packaging, and durable goods sectors.

The U.S. also leads in specialty material M&A activity, illustrated by Duraco Specialty Materials’ acquisition of Strata-Tac, Inc., which broadens its portfolio of custom-engineered, self-adhesive materials for specialized industrial applications. The convergence of green building codes, eco-friendly product innovations, and smart labeling technologies underscores the U.S. market’s position as a global leader in high-performance, sustainable emulsion PSA manufacturing.

China remains the largest global producer and consumer of Emulsion Pressure Sensitive Adhesives, supported by e-commerce expansion, eco-regulatory incentives, and industrial modernization. The national emphasis on green manufacturing—anchored in pollution reduction and the “Made in China 2025” strategy—continues to accelerate the adoption of low-VOC, water-based emulsion PSA systems across packaging, electronics, and construction industries.

The packaging and logistics sector, driven by a surge in online retail and fast-moving consumer goods, has created massive demand for flexible packaging adhesives, labels, and sealing tapes. Multinational companies like 3M China and H.B. Fuller have localized production to cater to the regional need for high-performance acrylic emulsions tailored for extreme humidity and temperature variations. The electronics manufacturing ecosystem, supported by China’s 11.6% growth in integrated circuit exports (2024), fuels demand for high-purity PSAs in displays, circuit protection, and component assembly.

Additionally, the EV market boom amplifies usage of thermal-resistant and non-conductive PSA tapes for battery packs and interior components. The acquisition of Shenzhen Landun Holding by Sika AG highlights increased foreign investment in waterproofing and adhesive technologies. With the government’s environmental framework prioritizing solvent-free formulations, China’s emulsion PSA industry is firmly positioned for high-volume, eco-compliant growth.

Germany’s Emulsion Pressure Sensitive Adhesives industry anchors the European market through its combination of regulatory rigor, innovation excellence, and high-value manufacturing. With Henkel AG and BASF SE leading the charge, Germany’s adhesive production emphasizes sustainable chemistry and recyclability. In April 2024, Henkel achieved a milestone with Aquence PS 3017 RE, a wash-off water-based acrylic PSA certified for PET recyclability—an innovation directly aligned with the EU Circular Economy Action Plan.

BASF SE’s Ludwigshafen facility, operating at double its acResin production capacity, supports the rising European demand for UV-curable and emulsion-based PSA systems used in labels, packaging, and automotive interiors. Germany’s automotive industry, driven by EV manufacturing and lightweight design, increasingly relies on durable emulsion PSAs for NVH damping, trim attachment, and cable harnessing. The cyclos-HTP Institute (CHI) continues to provide sustainability certifications, ensuring compliance with EU recyclability standards.

The UV-curable trend is also gaining momentum as German manufacturers adopt hybrid emulsion-UV PSA technologies offering low emissions and fast-curing efficiency for electronics and transportation applications. Germany’s chemical R&D ecosystem, supported by the Green Deal, cements its leadership in sustainable adhesive technologies and next-generation emulsion polymer design.

Japan’s Emulsion PSA market is driven by technological precision, material purity, and a relentless focus on performance reliability across electronics, automotive, and medical devices. Japanese manufacturers such as Nitto Denko Corporation and LINTEC Corporation lead in biocompatible and high-clarity water-based PSAs for medical applications, including wound dressings and wearable sensors. The country’s Green Procurement Law and national decarbonization goals continue to incentivize low-emission, solvent-free adhesive technologies.

Japan’s electronics and display sectors generate steady demand for ultra-thin, optically transparent acrylic emulsion adhesives in flexible OLEDs, touch panels, and sensors. Meanwhile, automotive and construction applications utilize emulsion-based PSAs with superior vibration and acoustic dampening performance, vital for interior noise control. Leading R&D programs emphasize the development of advanced monomers and additives to enhance the cohesive strength and adhesion of PSAs on low-energy surfaces.

The innovation-driven ecosystem positions Japan as a key exporter of precision emulsion PSA materials, catering to the world’s most demanding electronic and healthcare manufacturing standards.

India’s Emulsion Pressure Sensitive Adhesives market is expanding rapidly due to its booming e-commerce, packaging, and infrastructure sectors. The surge in FMCG and logistics industries has created consistent demand for cost-effective, eco-friendly packaging adhesives, especially in labeling, carton sealing, and lamination applications.

Global and domestic players are investing heavily in local production. Henkel Adhesive Technologies’ manufacturing facility in Kurkumbh, Pune, strengthens domestic supply chains for high-performance, low-VOC PSAs, while Pidilite Industries focuses on scaling affordable, consumer-grade emulsion adhesives for India’s diverse markets. Government initiatives, such as “Smart Cities Mission” and “Housing for All”, continue to stimulate consumption of construction-grade PSA tapes and membranes.

Additionally, the growing nonwovens and hygiene industry—particularly in diapers and sanitary products—has driven demand for skin-friendly, breathable emulsion adhesives. The trend toward bio-based and recyclable packaging further aligns India’s market trajectory with global sustainability standards, making it one of the fastest-growing PSA markets in the Asia-Pacific region.

Emulsion Pressure Sensitive Adhesives Market Report Scope

Emulsion Pressure Sensitive Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.6 Billion

|

|

Market Size (2034)

|

$29.2 Billion

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Chemistry (Acrylic, Rubber, Polyvinyl Acetate, Ethylene Vinyl Acetate, Polyurethane Dispersions, Other Elastomers), By Type (Permanent, Removable, Repositionable, Specialty), By Application (Tapes, Labels, Films & Sheets, Other Coatings), By End-Use Industry (Packaging, Automotive & Transportation, Healthcare & Medical, Building & Construction, Consumer Goods & DIY, Electronics, Graphics & Printing, Hygiene & Nonwovens

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, The Dow Chemical Company, Arkema S.A., 3M Company, Avery Dennison Corporation, Wacker Chemie AG, Sika AG, Ashland Global Holdings Inc., Pidilite Industries Ltd., Toyo Ink SC Holdings Co., Ltd., Scapa Group PLC, Franklin International, Inc., DIC Corporation, Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Acrylic

- Rubber

- Polyvinyl Acetate

- Ethylene Vinyl Acetate

- Polyurethane Dispersions

- Other Elastomers

By Type

- Permanent

- Removable

- Repositionable

- Specialty

By Application

- Tapes

- Labels

- Films & Sheets

- Other Coatings

By End-Use Industry

- Packaging

- Automotive & Transportation

- Healthcare & Medical

- Building & Construction

- Consumer Goods & DIY

- Electronics

- Graphics & Printing

- Hygiene & Nonwovens

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- The Dow Chemical Company

- Arkema S.A.

- 3M Company

- Avery Dennison Corporation

- Wacker Chemie AG

- Sika AG

- Ashland Global Holdings Inc.

- Pidilite Industries Ltd.

- Toyo Ink SC Holdings Co., Ltd.

- Scapa Group PLC

- Franklin International, Inc.

- DIC Corporation

- Jowat SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Emulsion Pressure Sensitive Adhesives (PSA) Market, delivering executive-ready analysis reviews of demand drivers, cost-to-serve dynamics, regulatory inflection points, and performance-in-use metrics across industrial and medical workflows. It highlights how water-based acrylic platforms, medical-grade certifications, wash-off label systems, and nanofiller-reinforced chemistries are translating into measurable gains in tack/peel balance, shear retention, LSE adhesion, and recyclability—pinpointing commercialization breakthroughs that de-risk scale-up on high-speed coating and converting lines. With clear benchmarking of technology pathways, pricing and sustainability trade-offs, and application-specific qualification checklists, this report is an essential resource for product managers, procurement leaders, technical service teams, and ESG strategists seeking solvent-free compliance and circular packaging alignment while preserving throughput and bond reliability.

Scope Highlights

Segmentation:

- By Chemistry: Acrylic; Rubber; Polyvinyl Acetate; Ethylene Vinyl Acetate; Polyurethane Dispersions; Other Elastomers.

- By Type: Permanent; Removable; Repositionable; Specialty.

- By Application: Tapes; Labels; Films & Sheets; Other Coatings.

- By End-Use Industry: Packaging; Automotive & Transportation; Healthcare & Medical; Building & Construction; Consumer Goods & DIY; Electronics; Graphics & Printing; Hygiene & Nonwovens.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies covering portfolios, capacity moves, partnerships, and sustainability roadmaps.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.