Market Overview: Regulatory-Driven Polymer Engineering Reshaping the Global Emulsion Adhesives Market

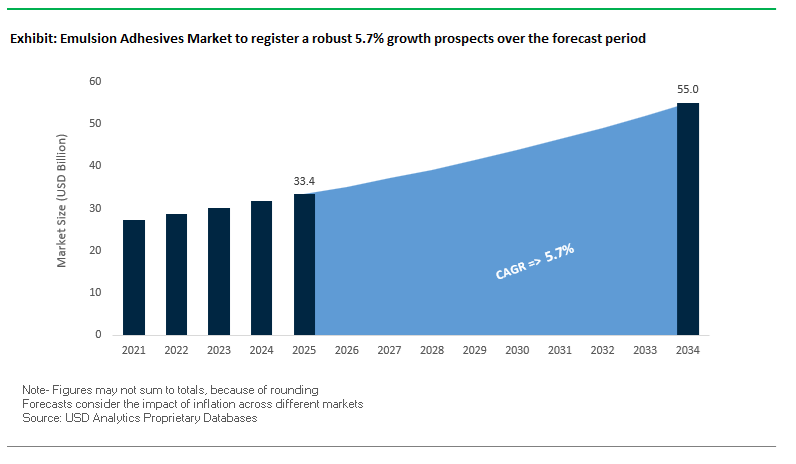

The Global Emulsion Adhesives Market is positioned to expand from USD 33.4 billion in 2025 to USD 55 billion by 2034, advancing at a CAGR of 5.7%, as regulatory pressure and OEM manufacturing requirements converge to structurally favor water-based adhesive chemistries. Across construction, packaging, hygiene, and engineered materials, solvent-free emulsion systems are displacing legacy solvent-borne adhesives due to enforceable air-quality regulations, tightening VOC thresholds, and the operational need for safer, scalable bonding solutions compatible with automated, high-throughput production lines. Manufacturers are responding by advancing Vinyl Acetate Ethylene (VAE) and styrene-acrylic emulsion platforms that deliver consistent adhesion, process stability, and compliance without sacrificing throughput or substrate versatility—an essential requirement for OEMs operating under ISO-aligned environmental and quality frameworks.

At the formulation level, the market’s momentum is being shaped by polymer redesign rather than incremental demand expansion. Adhesive producers are systematically reformulating emulsions to meet global emission limits—evidenced by the fact that more than 70% of new formulations register VOC content below 5 g/L—while simultaneously improving peel strength, moisture resistance, and thermal stability. High-solids emulsion technologies are a central lever in this shift, enabling faster line speeds and reduced drying or curing windows in packaging conversion, nonwoven assembly, and panel lamination. Advanced VAE emulsions maintaining stable peel strength from −10°C to 60°C are increasingly specified in hygiene and medical nonwovens, where dimensional stability and bond reliability must be maintained across storage, transport, and use conditions. This evolution reflects a broader OEM preference for adhesives that function as process enablers, not formulation constraints.

Performance differentiation is most visible in application-critical use cases. Acrylic pressure-sensitive emulsion adhesives achieving 95% shear strength retention after 72 hours of water immersion are setting new durability benchmarks in logistics labeling and moisture-exposed packaging environments. In parallel, bio-based material integration is moving from pilot scale to commercial adoption, with certain water-based packaging adhesives reaching 45% renewable raw material content by Q3 2025, supporting circular economy compliance without disrupting established converting equipment. In construction, styrene-acrylic emulsion binders enabling Class A fire-rated assemblies are reinforcing the role of emulsion adhesives in safety-critical urban infrastructure.

In October 2025, Sonoco Products Company announced a $30 million investment to boost its adhesives and sealants production capacity by over 100 million units annually, addressing global demand for packaging adhesives amid a surge in flexible packaging and e-commerce logistics. The same month, Henkel launched Technomelt Supra 079 Eco Cool, a low-emission, bio-based hot melt adhesive made with 49% renewable feedstock and 30% ISCC-certified mass-balanced material, cutting CO₂ emissions by 32% while operating at lower temperatures for energy-efficient packaging lines.

Parallel to these product expansions, global R&D spending on water-based adhesives increased by approximately 15% in the last year, driven by EU initiatives to enhance PET recyclability through caustic wash-off labeling adhesives. This shift is part of a larger circular economy transition emphasizing recycling compatibility and sustainable raw material sourcing.

In September 2025, Sibur began constructing Russia’s largest catalyst production facility in Kazan, expected to enhance the domestic supply chain for styrene-butadiene latex (SBL)—a key emulsion binder for paper coatings, construction materials, and textiles. Around the same period, BASF introduced Styronal® ES 7902, a next-generation SBR latex engineered for food-contact-safe paperboard coatings, offering migration compliance and improved printability for sustainable packaging applications.

The May 2025 partnership between Henkel, Dow, and Kraton Corporation aimed at decarbonizing adhesive feedstocks marked a key milestone in value chain collaboration. Their joint initiative integrates bio-based materials into existing emulsion adhesive lines, reinforcing sustainability without compromising bonding performance. In April 2025, R&D acceleration for Redispersible Polymer Powders (RDPs) was noted, emphasizing alkali-resistant, flexible, and waterproof formulations for EIFS and mortars, a critical enabler of green construction systems.

In November 2024, the INX Group Limited acquired Coatings & Adhesives Corporation (C&A), forming INX International Coatings and Adhesives, combining inks and emulsion adhesive solutions for packaging clients. This merger exemplifies a growing consolidation trend, where vertical integration enhances performance consistency, supply reliability, and value creation across the packaging and coating ecosystem.

The Emulsion Adhesives Market is experiencing a paradigm shift as regulatory pressure intensifies on the use of volatile and toxic chemical components. Manufacturers are actively reformulating their water-based adhesive systems to eliminate Alkylphenol Ethoxylates (APEOs) and minimize Volatile Organic Compounds (VOCs) to near-zero levels, ensuring compliance with global environmental standards.

Under the EU REACH Regulation, restrictions on harmful solvents such as N,N-dimethylacetamide (DMAC) and 1-ethylpyrrolidone (NEP)—set to take full effect between 2026 and 2029—are accelerating chemical reformulations in industrial and packaging adhesives. The reformulation trend is redefining product portfolios toward eco-compliant emulsion adhesives that can be safely used across packaging, automotive, and construction sectors without compromising performance.

Meanwhile, the California Air Resources Board (CARB) has introduced updated rules regulating VOCs based not just on weight, but on Maximum Incremental Reactivity (MIR)—a measure of smog-forming potential. The new standard compels adhesive formulators to adopt ultra-low reactivity monomers and binders, driving a surge in ultra-low VOC emulsion adhesives engineered for superior indoor air quality (IAQ) and compliance with LEED and Green Seal standards.

The Emulsion Adhesives Industry is rapidly aligning with circular economy principles, focusing on renewable feedstocks, bio-based polymer systems, and recyclability-enhancing properties. Innovation is concentrated on de-bondable, recyclable, and biodegradable adhesives that combine sustainability with high mechanical and chemical performance.

Leading chemical producers are increasingly relying on ISCC PLUS certified bio-circular feedstocks, incorporating renewable monomers into emulsion polymer matrices. These bio-based systems have demonstrated over 60% reductions in carbon emissions (cradle-to-gate) compared to conventional petrochemical formulations, positioning bio-circular adhesives as the next major growth driver in sustainable manufacturing.

Simultaneously, R&D is focused on recyclable adhesive formulations for the paper, packaging, and labeling industries. For example, starch-modified and natural resin-based emulsions are engineered to allow controlled de-bonding during repulping or recycling processes, enabling clean substrate separation without residue. The innovation directly supports mono-material packaging and enhances the recyclability of paper-based products, a critical step toward a waste-free materials cycle.

These new bio-based emulsion adhesives deliver comparable cohesion, tack, and thermal stability to petroleum-based systems, enabling their substitution in laminating, woodworking, textile, and pressure-sensitive adhesive (PSA) applications while reducing environmental impact.

The rapid acceleration of e-commerce and sustainable packaging adoption presents one of the most lucrative growth opportunities for the global emulsion adhesives industry. The increasing preference for mono-material flexible packaging and recyclable barrier films is boosting demand for water-based lamination adhesives that combine performance with recyclability.

The flexible packaging segment, which accounted for roughly 47% of the sustainable adhesives market in 2024, is leading the transformation. Manufacturers are leveraging high-performance vinyl acetate-ethylene (VAE) and acrylic-based emulsion systems to produce solvent-free, lightweight adhesive layers suitable for polyethylene (PE) and polypropylene (PP) films. These waterborne adhesives offer exceptional adhesion to low-surface-energy substrates, enabling fully recyclable, mono-material packaging solutions used across food, consumer goods, and logistics sectors.

As e-commerce packaging volumes rise globally, the market is witnessing large-scale adoption of cold-seal, heat-seal, and lamination-grade emulsion adhesives optimized for corrugated board, paper mailers, and recyclable flexible pouches. Their compatibility with high-speed coating and printing lines also enhances production efficiency and sustainability, cementing their position as essential materials for next-generation packaging design.

The ongoing shift toward mass timber construction—using Cross-Laminated Timber (CLT), Glulam, and other engineered wood systems—is fueling a parallel rise in demand for high-performance, low-emission emulsion adhesives suitable for structural and architectural bonding.

As the global construction industry targets carbon neutrality and energy efficiency, emulsion polymer isocyanate (EPI) and formaldehyde-free polyurethane (PUR) adhesive systems are emerging as preferred solutions for engineered wood assembly. These formulations provide excellent heat, moisture, and creep resistance, ensuring structural stability under variable environmental conditions.

Academic and industrial studies have underscored that wood’s hygroscopic nature causes significant dimensional movement (12–30% moisture-related variation), demanding elastic, flexible adhesives that can withstand expansion and contraction without delamination. Modern emulsion adhesives are thus engineered for cold-pressing performance, reducing production energy consumption while maintaining bond integrity.

In addition, indoor air quality (IAQ) compliance has become a non-negotiable feature. Formulations achieving zero-formaldehyde emissions and low VOC levels are increasingly specified in LEED, BREEAM, and WELL-certified projects, emphasizing the importance of health-conscious, environmentally responsible adhesive technologies in construction.

Emulsion Adhesives Market Share Insights, 2025-2034

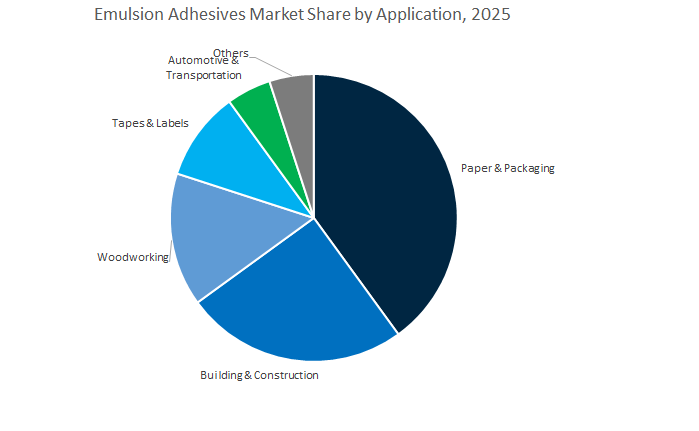

The paper and packaging segment dominates the global emulsion adhesives market, accounting for the largest share due to its critical role in corrugated box manufacturing, labeling, and flexible packaging. The surge in e-commerce and retail logistics has exponentially increased the global demand for packaging adhesives that combine strong tack, quick set, and recyclability. Emulsion-based formulations, primarily polyvinyl acetate (PVA) and acrylic emulsions, are favored for their low VOC emissions, water cleanup, and compatibility with paper and board substrates. These adhesives deliver excellent adhesion, smooth coating characteristics, and resistance to humidity—essential for case sealing, folding cartons, and label lamination. Furthermore, the global push for sustainable and repulpable packaging has accelerated the shift from solvent-based to waterborne emulsions. With rising regulatory pressure for plastic reduction and circular packaging, manufacturers are developing bio-based emulsion systems that align with eco-friendly and compostable packaging trends.

The building and construction industry is a key growth pillar in the emulsion adhesives market, driven by the need for eco-compliant, low-odor, and durable bonding solutions. These adhesives are extensively used in flooring installations, panel lamination, drywall attachment, and tile setting, offering strong adhesion to porous materials such as cement, wood, and gypsum. The waterborne nature of emulsion adhesives reduces harmful emissions, aligning with green building certifications (LEED, BREEAM) and modern indoor air quality standards. As urbanization surges across Asia-Pacific, Africa, and Latin America, the construction sector increasingly favors ready-to-use PVA and acrylic emulsions for ease of application and cost efficiency. Additionally, the rising use of prefabricated and modular construction methods has increased demand for fast-curing, flexible adhesive systems that enhance assembly speed while maintaining structural integrity.

Packaging Industry Holds 45.9% Market Share as Global Sustainability Mandates Transform Adhesive Demand

The packaging industry is the dominant end-use sector in the global emulsion adhesives market, driven by the explosive growth in e-commerce, food delivery, and retail-ready packaging. Emulsion adhesives are preferred for their eco-friendly, solvent-free composition, strong adhesion on paper substrates, and compatibility with high-speed packaging machinery. They are used extensively in carton sealing, corrugated box assembly, labeling, and flexible packaging lamination, providing both functionality and sustainability. The industry’s shift toward plastic-free packaging and recyclable fiber-based materials is fueling the adoption of bio-based and repulpable emulsions, especially in Europe and North America where regulatory pressure on single-use plastics is intense. In emerging markets, rapid consumption growth in FMCG and logistics has made emulsion adhesives a cost-effective and versatile solution. The trend toward waterborne adhesives with enhanced thermal and humidity resistance further reinforces the packaging segment’s leadership as the core growth engine of the emulsion adhesive market globally.

The building and construction sector represents the second-largest consumer of emulsion adhesives, leveraging their low-toxicity, strong adhesion, and environmental compliance. They are integral to bonding applications such as flooring installation, insulation panel lamination, drywall fixing, and acoustic tile bonding. The rise of green construction regulations and the transition toward zero-emission materials are driving contractors and builders to substitute solvent-based adhesives with waterborne emulsions. Additionally, urbanization and public infrastructure development, particularly in Asia-Pacific, are expanding the market for bulk emulsion adhesives used in residential, commercial, and industrial construction. Manufacturers are investing in modified acrylic and hybrid emulsions with improved moisture and alkali resistance to extend application performance in tropical and humid climates. As sustainability and indoor air quality become global priorities, emulsion adhesives are positioned as the preferred material for modern, environmentally responsible construction.

The wood and furniture industry is a reliable source of steady demand for emulsion adhesives, especially PVA and EVA-based systems, which are indispensable in laminating, veneering, and joint assembly processes. Their fast tack, low odor, and non-flammable nature make them the adhesive of choice in mass furniture production and joinery workshops worldwide. Simultaneously, the Consumer/DIY segment serves as a vital retail channel, representing millions of small-scale users purchasing emulsion adhesives for home repairs, arts and crafts, and light carpentry. The availability of ready-to-use emulsions in convenient packaging (tubes, jars, cartridges) has expanded their penetration across both professional and hobbyist markets. Growing consumer preference for eco-safe and child-friendly adhesives further enhances their market share.

The global emulsion adhesives market is shaped by the innovations of chemical giants and specialty formulators that are advancing low-VOC technologies, bio-based emulsions, and high-solid polymer systems. Key companies such as Celanese Corporation, Henkel AG & Co. KGaA, BASF SE, H.B. Fuller Company, and Sika AG are at the forefront of technology-driven transformation — leveraging R&D investments, acquisitions, and production expansions to align with sustainability mandates and high-performance demands from construction, packaging, and hygiene sectors.

Celanese Corporation remains the global leader in Vinyl Acetate Ethylene (VAE) emulsions, leveraging its fully integrated Acetyl Chain supply network. With strategic expansions in Nanjing, China and Geleen, Netherlands, Celanese added over 155,000 MTPA of VAE capacity between 2021 and 2023. Its flagship Vinamul® emulsion series delivers exceptional performance across nonwoven textiles, wood adhesives, and redispersible powders. The company’s continued investments aim to capitalize on Asia-Pacific’s demand growth, emphasizing sustainable polymer chemistry and supply security across global manufacturing hubs.

Henkel continues to reinforce its technological leadership through the Technomelt and Loctite brands, which integrate emulsion-based hot melt and waterborne systems for diverse industries. Its October 2025 launch of Technomelt Supra 079 Eco Cool highlighted Henkel’s commitment to carbon footprint reduction and energy-efficient adhesive processing. Collaborations with Dow and Kraton further solidify its leadership in bio-based adhesive development. Henkel’s products serve high-speed packaging, labeling, and consumer goods assembly, ensuring consistent performance under sustainability-driven regulations.

BASF SE remains the foremost supplier of Styrene-Butadiene (SBR) and styrene-acrylic dispersions, marketed under the Styronal® and Basonal® brands. Its innovative Styronal® ES 7902 represents a new generation of migration-compliant latexes for food-grade packaging coatings, while Basonal® PLUS 7988 offers optimized carbon footprint reduction. With strong positions in paper coatings and carpet backing, BASF continues to provide high-performance, eco-friendly solutions that balance mechanical strength, printability, and sustainability in industrial formulations.

H.B. Fuller focuses exclusively on adhesives and coatings, with an extensive portfolio of water-based and hot melt technologies. The company’s Gel-Tac® Microsphere Adhesives leverage acrylic emulsion chemistry to deliver ultra-removable and repositionable properties ideal for labels, tapes, and graphic films. Its innovative product range addresses critical needs such as low-temperature adhesion, caustic wash-off resistance, and linerless label performance, ensuring precision and reliability across diverse End-Use Industrys.

Sika AG, a global pioneer in construction chemicals, integrates emulsion adhesive systems within its expansive portfolio of sealants, coatings, and waterproofing solutions. Its proprietary Co-Elastic Technology (CET) enhances durability, flexibility, and water immersion resistance—key for facade bonding, panel fixing, and insulation systems. Backed by a global R&D network of over 1,800 specialists, Sika continues to innovate around resource-efficient construction materials, directly contributing to the green building and infrastructure development sectors worldwide.

China continues to dominate the Asia-Pacific emulsion adhesives market, powered by state-led industrial modernization and sustainability policies under the 14th Five-Year Plan. The national blueprint prioritizes green packaging materials and low-VOC water-based adhesive technologies, directly benefitting manufacturers producing vinyl acetate ethylene (VAE) and polyvinyl acetate (PVA) emulsions for the food, beverage, and consumer goods sectors. The ongoing boom in e-commerce packaging and ready-to-eat food delivery significantly boosts the need for flexible lamination and sealing adhesives with enhanced heat and moisture resistance.

The electric vehicle (EV) revolution adds another strong growth dimension, as major producers like SAIC, BYD, and NIO increasingly integrate lightweight, high-durability emulsion adhesives for module assembly and insulation. Chinese universities and corporate R&D divisions are accelerating research into bio-based adhesive chemistries, aligning with the national carbon neutrality target by 2060. Local producers such as Anhui Wanwei Group are reporting capacity expansions in VAE emulsions, supported by the rise in domestic construction and furniture production. With large-scale urbanization and modular housing projects continuing, construction and woodworking adhesives remain critical demand contributors across China.

The United States emulsion adhesives market is undergoing a structural shift toward sustainable and circular manufacturing practices, underpinned by initiatives from the U.S. Department of Energy (DOE) promoting low-VOC, water-based adhesives as part of decarbonization efforts. The U.S. Green Building Council (USGBC) has embedded material efficiency and VOC reduction into LEED-certified construction guidelines, leading to a measurable uptick in acrylic and VAE emulsion adhesive adoption in flooring, paneling, and insulation bonding.

Key polymer producers such as Celanese Corporation are reinforcing the market’s innovation backbone with over $100 million in annual R&D spending dedicated to bio-based and high-performance emulsions. In the automotive industry, manufacturers like Ford and General Motors increasingly substitute mechanical fasteners with lightweight emulsion adhesives to improve structural integrity while reducing vehicle weight. Simultaneously, the packaging sector—driven by the nation’s robust consumer base and recycling mandates—is adopting compostable and recyclable adhesive formulations, creating a favorable environment for manufacturers of eco-conscious waterborne adhesives.

Germany stands as the European hub for emulsion polymer innovation, integrating sustainability, precision manufacturing, and Industry 4.0 into adhesive production. Wacker Chemie AG’s €50 million investment in expanding its VAE emulsion capacity at Burghausen demonstrates how German manufacturers are scaling to meet growing demand across automotive, packaging, and construction sectors. Henkel, BASF, and other major players are driving advancements in functional coatings and low-temperature adhesive applications, enabling mono-material packaging essential for recyclability under EU sustainability directives.

The Energy Saving Ordinance (EnEV) and EU Green Deal policies have elevated demand for solvent-free, water-based adhesives in construction insulation and sealing. Germany’s extensive automotive production also continues to favor SMP-based (Silyl Modified Polymer) elastic adhesives for interior and body applications requiring superior flexibility and long-term stability. Moreover, the country is witnessing strong growth in UV-curable pressure-sensitive adhesives (PSAs), which reduce energy use during curing and eliminate solvent emissions—key innovations in the labels, tapes, and industrial laminates markets.

India’s emulsion adhesives market is rapidly expanding due to dual forces of infrastructure development and e-commerce growth. Massive government-led programs such as “Smart Cities Mission” and “Housing for All” are fueling steady demand for construction adhesives used in tiling, waterproofing, and structural bonding. Concurrently, the e-commerce packaging industry, boosted by logistics hubs in major cities like Mumbai, Delhi, and Bengaluru, is driving high consumption of lamination and sealing-grade PVA adhesives for flexible and corrugated packaging.

Domestic manufacturing initiatives under the “Make-in-India” policy have further strengthened the local supply chain for automotive and consumer goods adhesives, encouraging Indian producers like Pidilite Industries Ltd. to expand production capacity and distribution networks. In addition, the growing preference for modular furniture and interior design products is catalyzing the use of high-strength wood emulsion adhesives. Premium commercial projects are increasingly adopting low-VOC and eco-labeled adhesives, reflecting India’s gradual but steady alignment with green building certifications (IGBC, LEED India).

Japan remains at the forefront of technological innovation in the global emulsion adhesives industry, emphasizing bio-based, low-outgassing, and high-performance formulations. Industry leaders such as DIC Corporation and Asahi Kasei Corporation are pioneering the integration of nanotechnology and polymer chemistry to develop emulsion adhesives with superior adhesion, thermal stability, and clarity for electronics, optics, and medical devices. The innovation aligns with Japan’s commitment to achieving carbon neutrality and reducing petrochemical dependence.

Additionally, the country’s robust printing and paper industry continues to generate high demand for non-yellowing PVA emulsions in bookbinding and graphic arts, ensuring smooth machinability and longevity. In parallel, Japanese electronics and semiconductor manufacturers increasingly rely on specialty emulsion adhesives in display assembly and component lamination, where precision, low VOCs, and heat resistance are essential. The national shift toward biodegradable adhesive materials also indicates Japan’s focus on sustainable material innovation to meet global environmental targets.

Brazil remains a critical market for emulsion adhesives in Latin America, led by its dominant position in woodworking, furniture production, and civil infrastructure. The country’s furniture industry, concentrated in regions like Santa Catarina and Paraná, drives strong consumption of PVA and VAE emulsion adhesives due to their cost-effectiveness, flexibility, and durability. Simultaneously, the ongoing national infrastructure development programs—covering highways, residential housing, and industrial parks—fuel continuous demand for construction-grade emulsion adhesives in flooring, wall panels, and sealing systems.

Local manufacturers are increasingly shifting toward environmentally compliant, water-based adhesives to meet new VOC emission standards, while also enhancing export competitiveness across Latin American markets. As the regional focus on sustainable construction and green manufacturing grows, Brazil’s transition to low-VOC and solvent-free formulations positions it as a major contributor to regional sustainability goals within the emulsion adhesives segment.

Emulsion Adhesives Market Report Scope

Emulsion Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$33.4 Billion

|

|

Market Size (2034)

|

$55 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Resin Type (Acrylic Polymer Emulsion, Polyvinyl Acetate Emulsion, Vinyl Acetate Ethylene Emulsion, Styrene-Butadiene Latex, Polyurethane Dispersion, Others), By Application (Paper & Packaging, Woodworking, Tapes & Labels, Building & Construction, Automotive & Transportation, Others), By End-Use Industry (Packaging Industry, Building & Construction, Automotive & Transportation, Wood & Furniture, Consumer/DIY, Other Industries), By Technology (Water-based Adhesives), By Product Type (Permanent Adhesives, Removable Adhesives

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Wacker Chemie AG, BASF SE, Celanese Corporation, The Dow Chemical Company, Arkema S.A., Sika AG, DIC Corporation, Synthomer Plc, Pidilite Industries Ltd., Franklin International, Ashland Global Holdings Inc., Mitsubishi Chemical Holdings Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Acrylic Polymer Emulsion

- Polyvinyl Acetate Emulsion

- Vinyl Acetate Ethylene Emulsion

- Styrene-Butadiene Latex

- Polyurethane Dispersion

- Others

By Application

- Paper & Packaging

- Woodworking

- Tapes & Labels

- Building & Construction

- Automotive & Transportation

- Others

By End-Use Industry

- Packaging Industry

- Building & Construction

- Automotive & Transportation

- Wood & Furniture

- Consumer/DIY

- Other Industries

By Technology

By Product Type

- Permanent Adhesives

- Removable Adhesives

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Wacker Chemie AG

- BASF SE

- Celanese Corporation

- The Dow Chemical Company

- Arkema S.A.

- Sika AG

- DIC Corporation

- Synthomer Plc

- Pidilite Industries Ltd.

- Franklin International

- Ashland Global Holdings Inc.

- Mitsubishi Chemical Holdings Corporation

- Jowat SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Emulsion Adhesives Market through rigorous, decision-grade analysis reviews of technology shifts, procurement realities, and performance-in-use, and highlights how water-based platforms are scaling under low-VOC regulation, circular-design mandates, and high-speed converting. We map where polymer breakthroughs—VAE upgrades, styrene-acrylic innovations, polyurethane dispersions, and bio-circular inputs—unlock measurable gains in bond strength, humidity tolerance, and recyclability across packaging, woodworking, construction, tapes & labels, and transportation. With clear competitive benchmarking, cost-to-serve lenses, and adoption playbooks tied to converting lines and QA specs, this report is an essential resource for product leaders, sourcing managers, technical service teams, and sustainability officers aligning adhesive strategy with zero-solvent operations and mono-material packaging goals. The coverage also surfaces commercialization breakthroughs in high-solids emulsions, APEO-free surfactants, and de-bondable label systems that improve MRF yield and repulping efficiency.

Scope Highlights

Segmentation:

- By Resin Type: Acrylic Polymer Emulsion; Polyvinyl Acetate Emulsion; Vinyl Acetate Ethylene Emulsion; Styrene-Butadiene Latex; Polyurethane Dispersion; Others.

- By Application: Paper & Packaging; Woodworking; Tapes & Labels; Building & Construction; Automotive & Transportation; Others.

- By End-Use Industry: Packaging Industry; Building & Construction; Automotive & Transportation; Wood & Furniture; Consumer/DIY; Other Industries.

- By Technology: Water-based Adhesives.

- By Product Type: Permanent Adhesives; Removable Adhesives.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies covering portfolios, capacity moves, partnerships, and sustainability roadmaps.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.